The global personalized cancer vaccine market size accounted for USD 4.2 billion in 2025 and is predicted to increase from USD 4.99 billion in 2026 to approximately USD 23.32 billion by 2035, expanding at a CAGR of 18.7% from 2026 to 2035. A shift towards precision medicine, major technological breakthroughs, growing cancer burden, expanding R&D activities, and increasing healthcare investments are promoting the market growth.

Tailored Cancer Care: Unlocking the Personalized Vaccine Trends

The personalized cancer vaccine is developed by utilizing the tumor-associated antigen of an individual patient to stimulate their immune system and attack their specific tumors. They offer high specificity, low side effects, and enhanced immune responses, which increase their use. Moreover, their ability to prevent cancer recurrences and offer synergistic effects is also increasing their use in the treatment of multiple cancer types.

The Next Frontier: The Opportunities Powering the Market Growth

- The growth in multiple cancer cases is increasing the adoption of personalized cancer vaccines.

- The growing shift towards precision medicine also drives the adoption of personalized cancer vaccines.

- Increasing advancements in drug delivery systems like lipid nanoparticles and viral vectors are enhancing the vaccine efficacy, promoting innovations.

- Growing interest in combination therapies and long-term immune memory development is also increasing the development of new personalized cancer vaccines with improved efficacy.

- A rise in the collaborations among industries and institutions supported by government funding is also accelerating the development of new personalized cancer vaccines.

- The growing technological integration is promoting faster, more accurate neoantigen prediction as well as driving the development of multi-epitope vaccine designs.

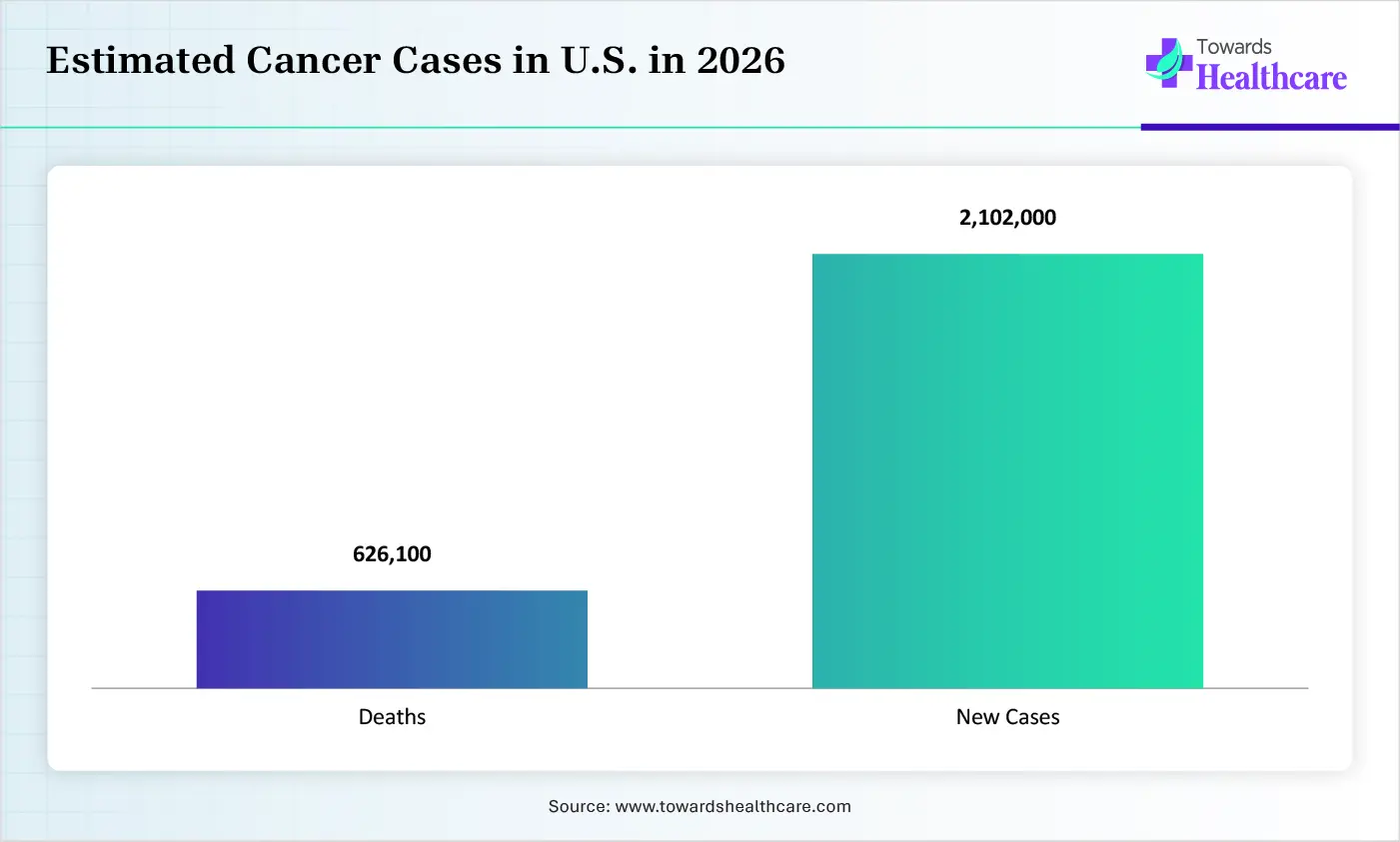

The graph represents the estimated number of cancer deaths and new cases in the U.S. for the year 2026. It indicates that there will be a rise in cancer burden, which will drive the demand for safe, effective, and target-specific treatment options. This, in turn, will increase the adoption of personalized cancer vaccines for the effective management and treatment of multiple cancer types, which will ultimately promote the market growth.

Market Segmentation Overview

- By vaccine type, the neoantigen-based vaccines segment accounted for the highest revenue share of 48% of the personalized cancer vaccine market in 2025 and is expected to grow at the fastest CAGR during the upcoming years, due to their high tumor specificity. Their strong immune response and minimal off-target toxicity also increased their use. Their enhanced personalization capability also increased their acceptance rates.

- By cancer type, the melanoma segment held a major revenue share of 26% of the market in 2025, due to its strong immunogenicity and mutation burden. Their high relapse risk also increased the use of personalized cancer vaccines. Additionally, their proven success rates and accessible tumor tissue have also increased their use and innovations.

- By technology platform type, the mRNA-based platform segment contributed the biggest revenue share of 38% of the personalized cancer vaccine market in 2025 and is expected to grow at the fastest CAGR during the predicted time, due to its rapid development and high flexibility. Their strong immune activation and enhanced safety also increased their use. The growth in investments also accelerated their innovations.

- By treatment approach type, the combination therapy segment led the market with 66% of market share in 2025 and is expected to grow at the fastest CAGR during the predicted time, due to its enhanced efficacy and synergistic effect. Their ability to overcome tumour resistance also increased their adoption. Additionally, their improved clinical outcomes also increased their use in a wide range of cancer treatments.

Regional Analysis

North America registered its dominance over the global personalized cancer vaccine market with 42% in 2025, due to the presence of advanced healthcare infrastructure and a robust biotech ecosystem. This increased the early adoption of personalized cancer vaccines, where growth in R&D investments also increased their innovations. Growth in clinical trials also increased their approval rates, which enhanced the market growth.

Asia Pacific held 19% share of the personalized cancer vaccine market in 2025 and is expected to grow at the fastest CAGR during the predicted time, due to a high patient population. Expanding healthcare and investments for various sources are also driving the personalized cancer vaccine innovations. Growing health awareness and clinical trials are also increasing their adoption and innovations, promoting market growth.

The Power Player: The Key Companies Driving Personalized Cancer Vaccines

Moderna, Inc. dominated the market with the launch of its mRNA-4157, where BioNTech SE was its closest competitor offering iNeSt and autogene cevumeran. Gritstone Bio, Inc. also sustained its market position by providing GRANITE platforms, where CureVac SE also contributed to the market growth with its proprietary mRNA platform.

Segments Covered in the Report

By Vaccine Type

- Neoantigen-Based Vaccines

- DNA-based Neoantigen Vaccines

- RNA-based Neoantigen Vaccines

- Peptide-based Neoantigen Vaccines

- Dendritic Cell Vaccines

- Autologous Dendritic Cell Vaccines

- Allogeneic Dendritic Cell Vaccines

- Tumor Cell Vaccines

- Autologous Tumor Cell Vaccines

- Allogeneic Tumor Cell Vaccines

- Viral Vector-Based Vaccines

- Adenoviral Vectors

- Lentiviral Vectors

By Cancer Type

- Melanoma

- Lung Cancer

- Non-Small Cell Lung Cancer (NSCLC)

- Small Cell Lung Cancer (SCLC)

- Breast Cancer

- Prostate Cancer

- Colorectal Cancer

- Others

- Pancreatic Cancer

- Ovarian Cancer

- Glioblastoma

By Technology Platform

- mRNA-based Platform

- DNA-based Platform

- Cell-based Platform

- Peptide-based Platform

- Viral Vector Platform

By Treatment Approach

- Monotherapy

- Combination Therapy

- With Immune Checkpoint Inhibitors

- With Chemotherapy

- With Radiotherapy

By End User

- Hospitals

- Cancer Research Institutes

- Specialty Clinics

By Distribution Channel

- Direct Sales

- Hospital Pharmacies

- Specialty Pharmacies

By Region

- North America

- U.S.

- Canada

- Mexico

- Rest of North America

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Europe

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific

- China

- Taiwan

- India

- Japan

- Australia and New Zealand

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA