")

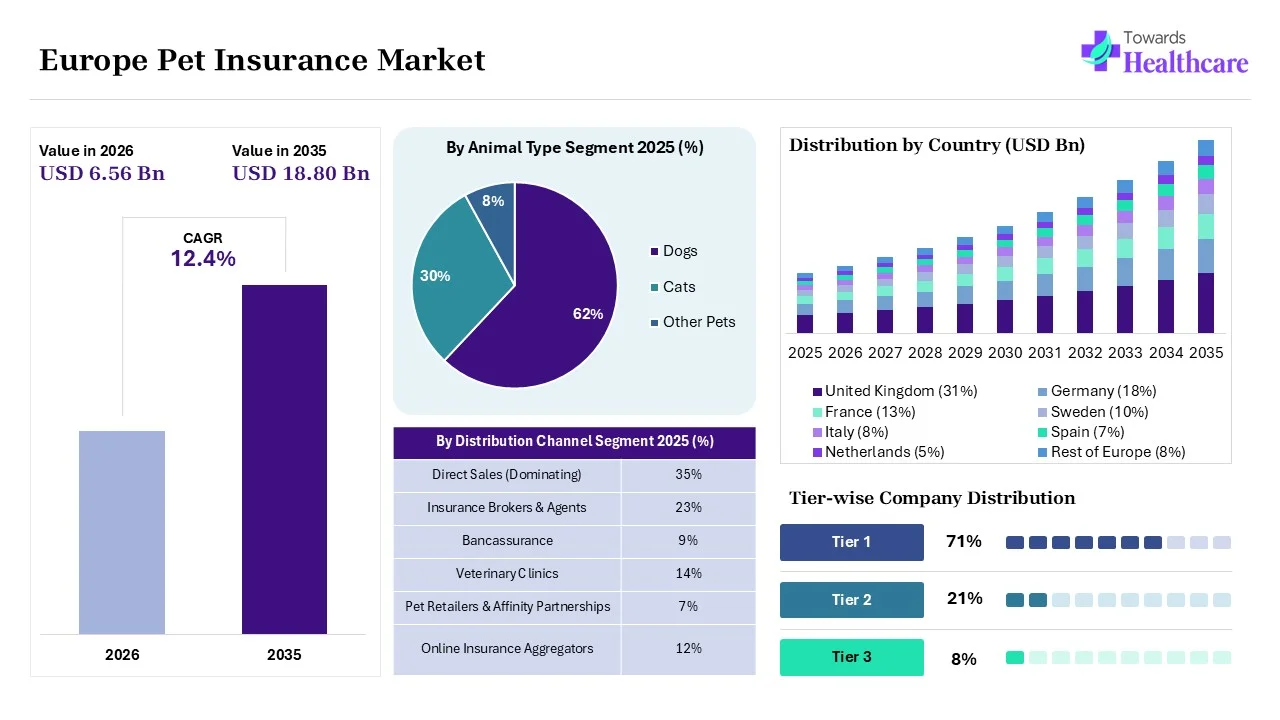

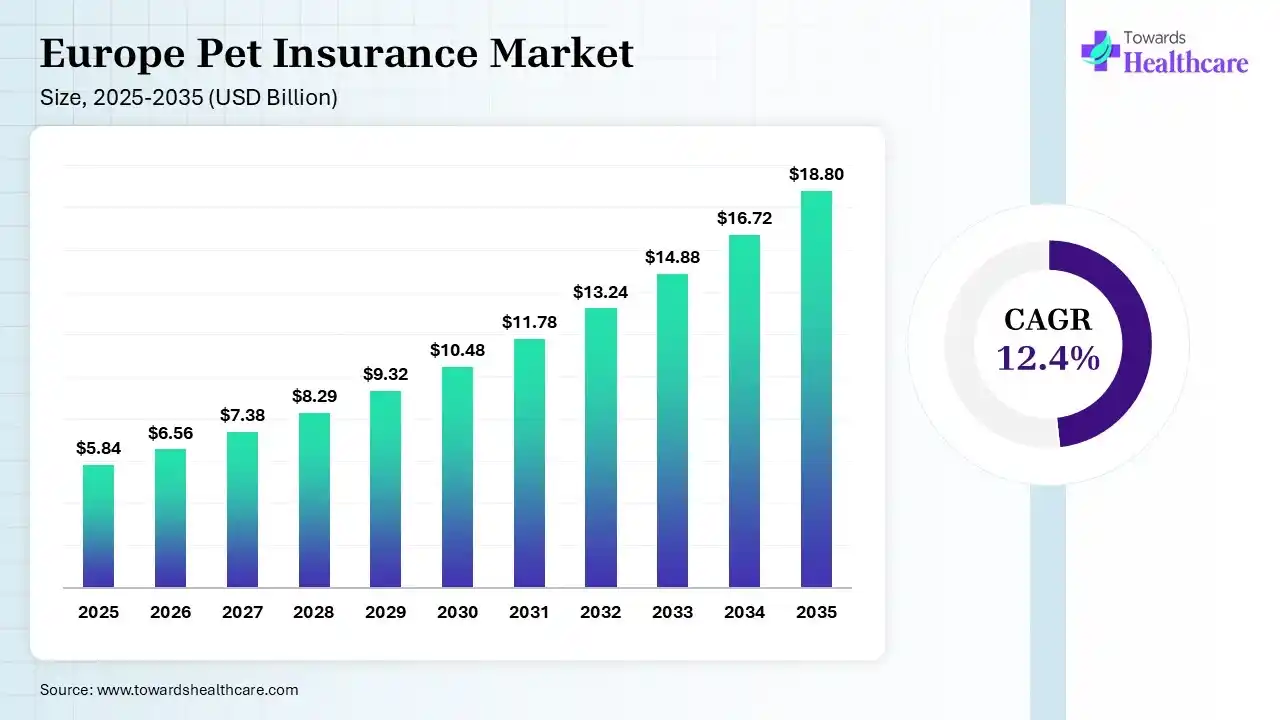

The Europe pet insurance market size stood at US$ 5.84 billion in 2025, grew to US$ 6.56 billion in 2026, and is forecast to reach US$ 18.8 billion by 2035, expanding at a CAGR of 12.4% from 2026 to 2035.

")

The Europe pet insurance market is driven by rising veterinary care costs, companion adoption rates, and a shift towards AI-powered digital claim systems. The Europe pet insurance encompasses insurance policies covering veterinary and healthcare expenses for pets across Europe. With the growing pet ownership, health awareness, higher disposable income, and rise in the demand for comprehensive healthcare coverage across Europe, the demand for pet insurance is increasing. The growing accidents, injuries, illnesses, diseases, and surgeries are also increasing the demand for pet insurance, where the advancement in hospitalization, diagnostic tests, wellness care, prescription medication, and preventive home healthcare are also increasing their use.

At the same time, the growing costs associated with veterinary treatment and spending on animal healthcare are also increasing the use of various European pet insurance services. They help in reducing financial burden, enhancing access to quality veterinary services, and encouraging diagnosis and treatment. The common type of insurance coverage for pets involves accident-only insurance, accident and illness insurance, preventive care plans, and lifetime coverage policies. Additionally, the growing pet humanization trends, advancements in veterinary medicine, digital enrollment, and customized insurance plans are also fueling the market growth.

AI offers a wide range of applications in European pet insurance claim processing, where it automatically scans veterinary invoices. It also helps in the analysis of animal breed and age for predicting risk underwriting, and it also helps in symptom analysis with digital video-vet triage. AI also helps in automated fraud detection by identifying unsual patters and duplicate transactions, where it is also being used in the development of connected wearable data to track pet activity levels.

Rising Pet Humanization

The growing pet humanization trends in Europe are increasing the use of various veterinary treatment options. This, in turn, is increasing the demand for pet insurance solutions due to the growing willingness to spend on high-quality veterinary treatments and preventive healthcare. At the same time, they are also being preferred for covering rising costs associated with accidents, surgeries, illness, nutrition support, wellness care, and advanced veterinary care services.

Advancements in Pet Policies

To meet the changing consumer expectations, the insurance providers are focusing on enhancing policy offerings, which is driving the advancement in pet insurance. They are driving the development of various customized plans, lifetime coverage policies, and multi-pet plans, which are attracting pet owners. Furthermore, their long-term protection, flexible payment structures, improved transparency, enhanced coverage, and simplified policies are also encouraging their use for chronic conditions.

Expanding Digitalization

Expanding healthcare digitalization across Europe is increasing the accessibility and benefits of pet insurance, promoting personalized policy recommendations, and their growing integration with tele-veterinary services is also increasing their use. The companies are also launching various online platforms and mobile applications to offer simplified policy comparison, easy policy management, claim tracking, and enhanced customer experience. Their digital claim submission and data analytics are also reducing processing time and enhancing operational efficiency, faster claim approval, and enhanced customer engagement.

| Table | Scope |

| Market Size in 2026 | USD 6.56 Billion |

| Projected Market Size in 2035 | USD 18.8 Billion |

| CAGR (2026 - 2035) | 12.4% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Coverage Type, By Animal Type, By Policy Provider, By Distribution Channel, By End User, By Policy Duration, By Claim Type, By Region |

| Top Key Players | Agria Djurforsakring, DFV Deutsche Familienversicherung AG, Petplan UK,Lassie AB, ManyPets, RSA Insurance Group, AXA SA |

")

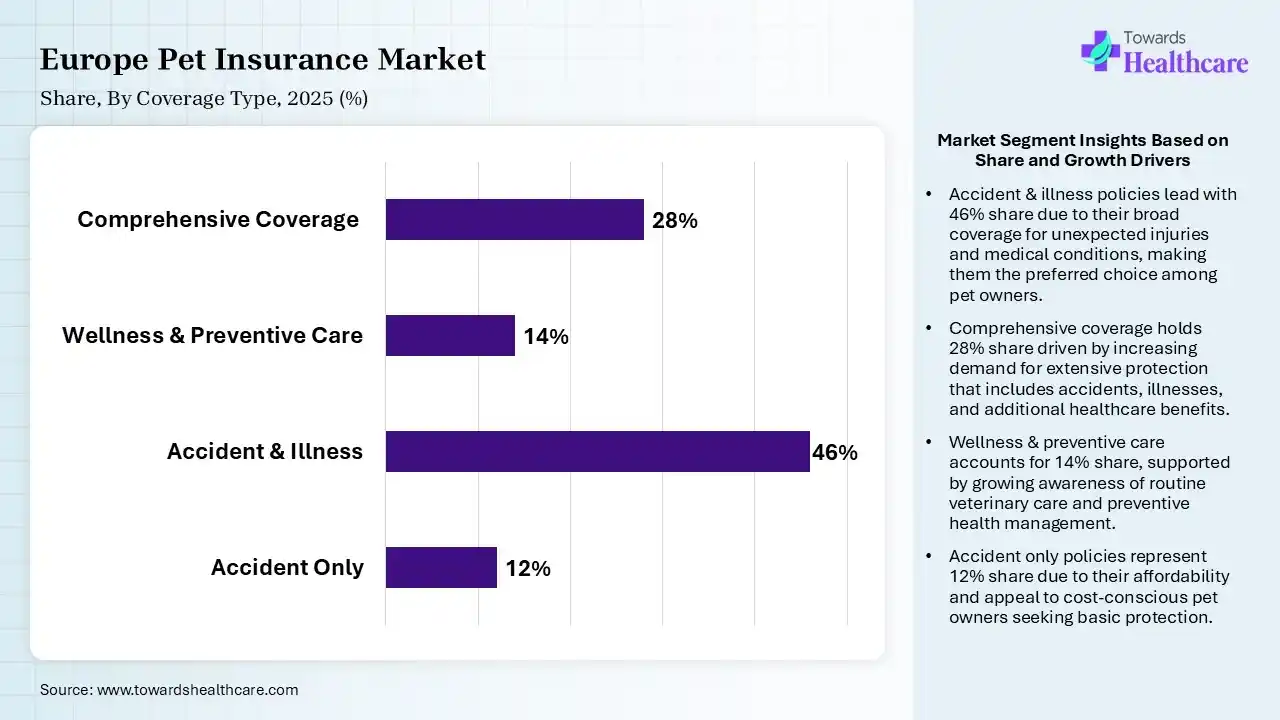

| Segment | Share 2025 (%) |

| Accident Only | 12% |

| Accident & Illness | 46% |

| Wellness & Preventive Care | 14% |

| Comprehensive Coverage | 28% |

The Accident & Illness Segment Dominated the Market With 46% in 2025

The accident & illness segment led the Europe pet insurance market with a 46% share in 2025, due to a rise in veterinary treatment costs, which encouraged broader coverage. Owners seek financial protection against chronic diseases, which has also increased the demand for pet insurance. Expansion of the insurer offerings also enhanced the penetration of these insurance coverages.

The comprehensive coverage segment held the second-largest share of 28% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 15.10% during the forecast period, as it covers extensive medical needs. The growing humanization of pets also boosts premium policy purchases. Advanced diagnostics and specialty care, expanding utilization, are also driving their demand.

The wellness & preventive care segment held 14% of the Europe pet insurance market share in 2025, due to a shift towards preventive healthcare, which increases demand. Rising routine checkup coverage is also attracting younger pet owners. Subscription-style packages are also encouraging their use, supporting the market growth.

The accident-only segment held 12% of the market share in 2025, as it appeals to budget-conscious owners. Increasing awareness also supports their adoption as an entry-level insurance product offering various affordable coverage options. Provides affordable protection for unexpected injuries, where their lower premiums and simple insurance options also drive their demand.

")

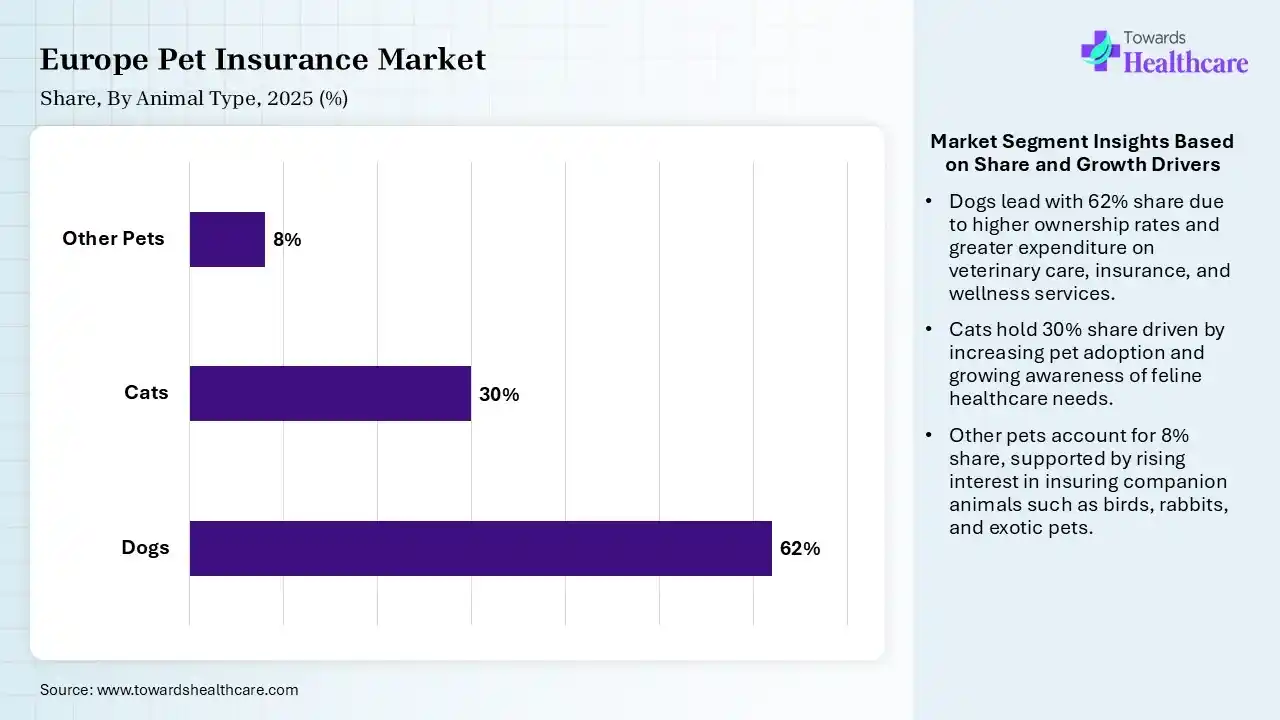

| Segment | Share 2025 (%) |

| Dogs | 62% |

| Cats | 30% |

| Other Pets | 8% |

The Dogs Segment Dominated the Market With 62% in 2025

The dogs segment accounted for the highest revenue share of 62% of the Europe pet insurance market in 2025, driven by higher veterinary expenditure for dogs, which supported insurance uptake. A larger dog ownership base also increased policy demand. A rise in the chronic disease treatment costs also encouraged the demand for their insurance coverage.

The cats segment held the second-largest share of 30% of the market in 2025, due to rising cat adoption, which increases insurance penetration. Indoor pet healthcare spending continues to grow, which drives the demand for various pet insurance policies across Europe. Additionally, growing digital insurance channels are also improving their accessibility.

The other pets segment held 8% of the Europe pet insurance market share in 2025 and is expected to show the highest growth with a CAGR of 15.40% during the forecast period, driven by growing ownership of exotic pets, which creates new opportunities. Specialized policies are also expanding market reach. Expanding veterinary care availability also increases spending.

")

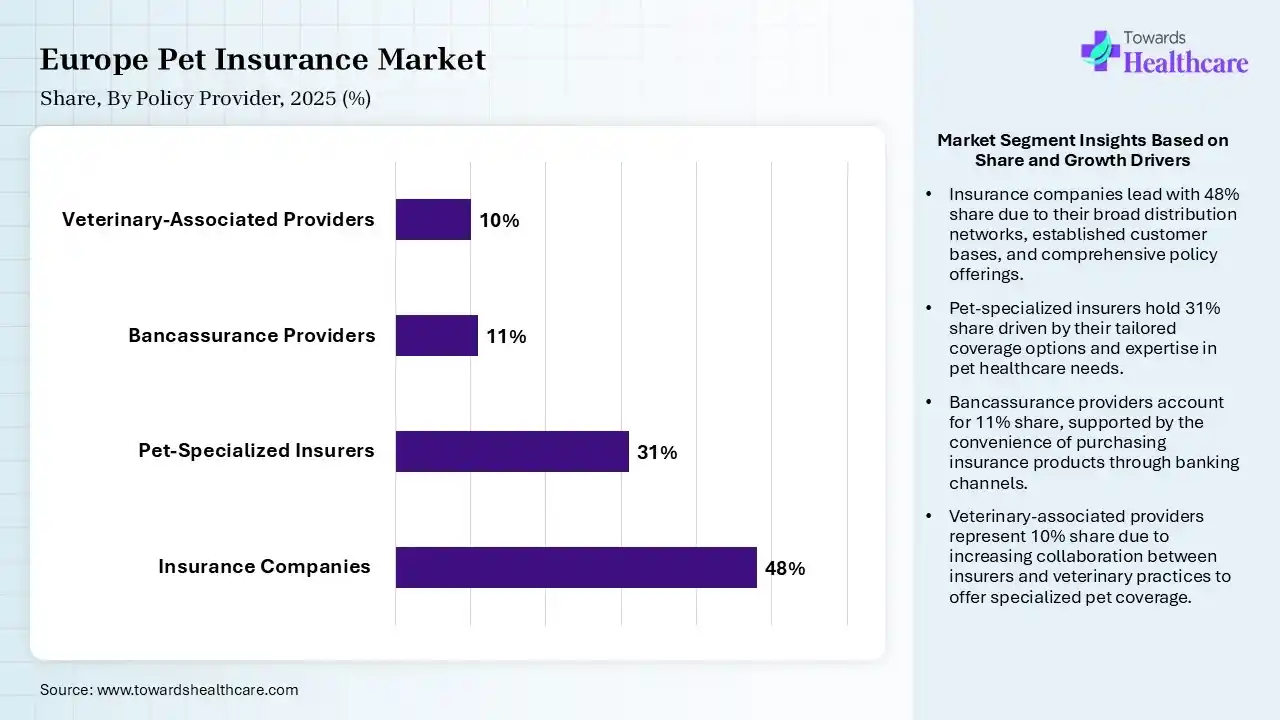

| Segment | Share 2025 (%) |

| Insurance Companies | 48% |

| Pet-Specialized Insurers | 31% |

| Bancassurance Providers | 11% |

| Veterinary-Associated Providers | 10% |

The Insurance Companies Segment Dominated the Market With 48% in 2025

The insurance companies segment held a major revenue share of 48% of the Europe pet insurance market in 2025, due to established underwriting expertise, which attracted customers. Strong distribution networks also supported their market leadership. At the same time, brand trust remained a key advantage, which increased their acceptance rates.

The pet-specialized insurers segment held the second-largest share of 31% of the market in 2025 and is expected to expand rapidly with a CAGR of 14.70% during the forecast period, driven by tailored pet health products that improve competitiveness. Digital-first business models are also accelerating their expansion. Growing consumer awareness is also supporting their adoption.

The bancassurance providers segment held 11% of the Europe pet insurance market share in 2025, due to existing banking relationships that facilitate cross-selling. Their enhanced convenience, increasing market penetration, and digital policy support are also encouraging policy purchases. Financial institutions broaden insurance portfolios, promoting their acceptance rates.

The veterinary-associated providers segment held 10% of the market share in 2025, driven by increasing veterinarian recommendations, which are enhancing trust. Point-of-care enrollment also improves conversion rates, driving their demand. At the same time, growing partnerships and strengthening customer engagements are also promoting their use.

")

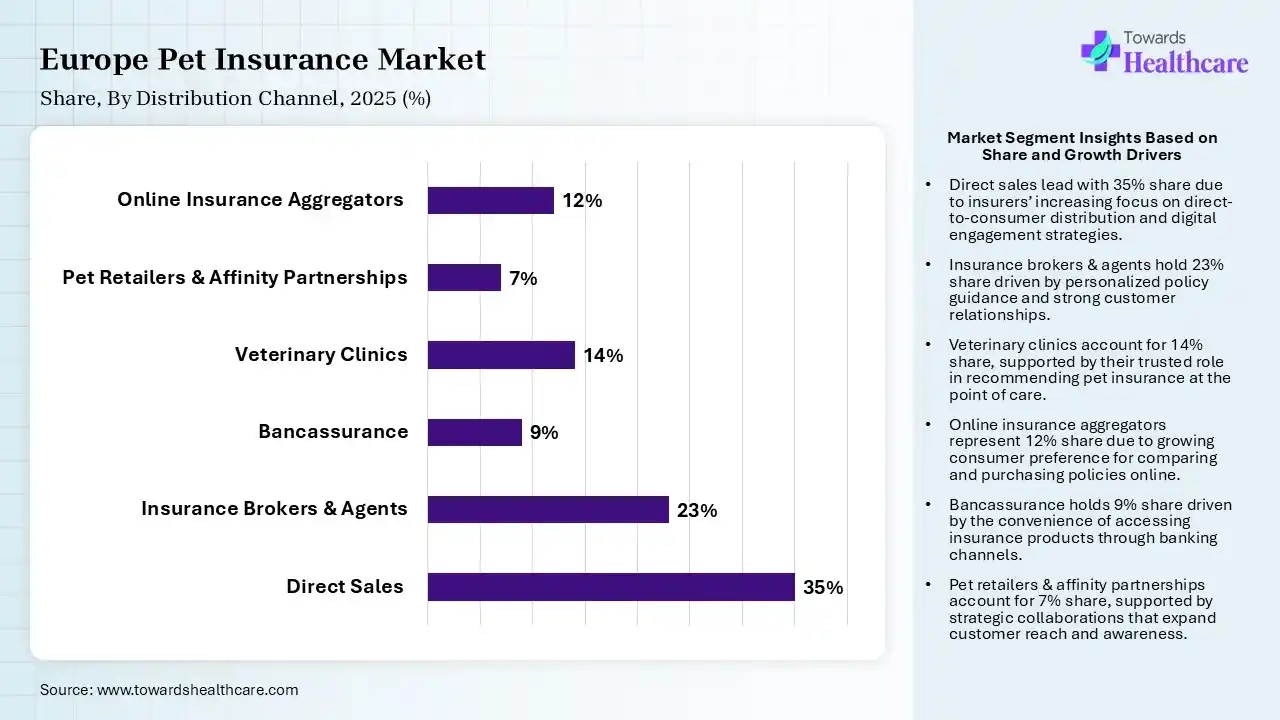

| Segment | Share 2025 (%) |

| Direct Sales | 35% |

| Insurance Brokers & Agents | 23% |

| Bancassurance | 9% |

| Veterinary Clinics | 14% |

| Pet Retailers & Affinity Partnerships | 7% |

| Online Insurance Aggregators | 12% |

The Direct Sales Segment Dominated the Market With 35% in 2025

The direct sales segment contributed the biggest revenue share of 35% of the Europe pet insurance market in 2025, driven by heavy investments by the insurers in digital platforms. They also offered direct engagement, which improved customer acquisition. Their online purchasing also simplified enrollment, which encouraged their use.

The insurance brokers & agents segment held the second-largest share of 23% of the market in 2025, due to personalized policy advice supporting sales. Established relationships are also driving their renewals. Complex policy comparisons favor intermediaries. Their enhanced claim processing and customer services are also increasing their use.

The veterinary clinics segment held 14% of the Europe pet insurance market share in 2025, driven by the point-of-care recommendations that are influencing purchasing decisions. Their trusted veterinary guidance is also increasing their uptake. At the same time, growing clinic partnerships and enhancing benefits are also expanding their reach.

The online insurance aggregators segment held 12% of the market share in 2025 and is expected to gain the highest share with a CAGR of 16.20% during the forecast period, due to consumers increasingly comparing policies online. Transparent pricing is also attracting buyers. Expanding digital ecosystems are also accelerating market growth.

")

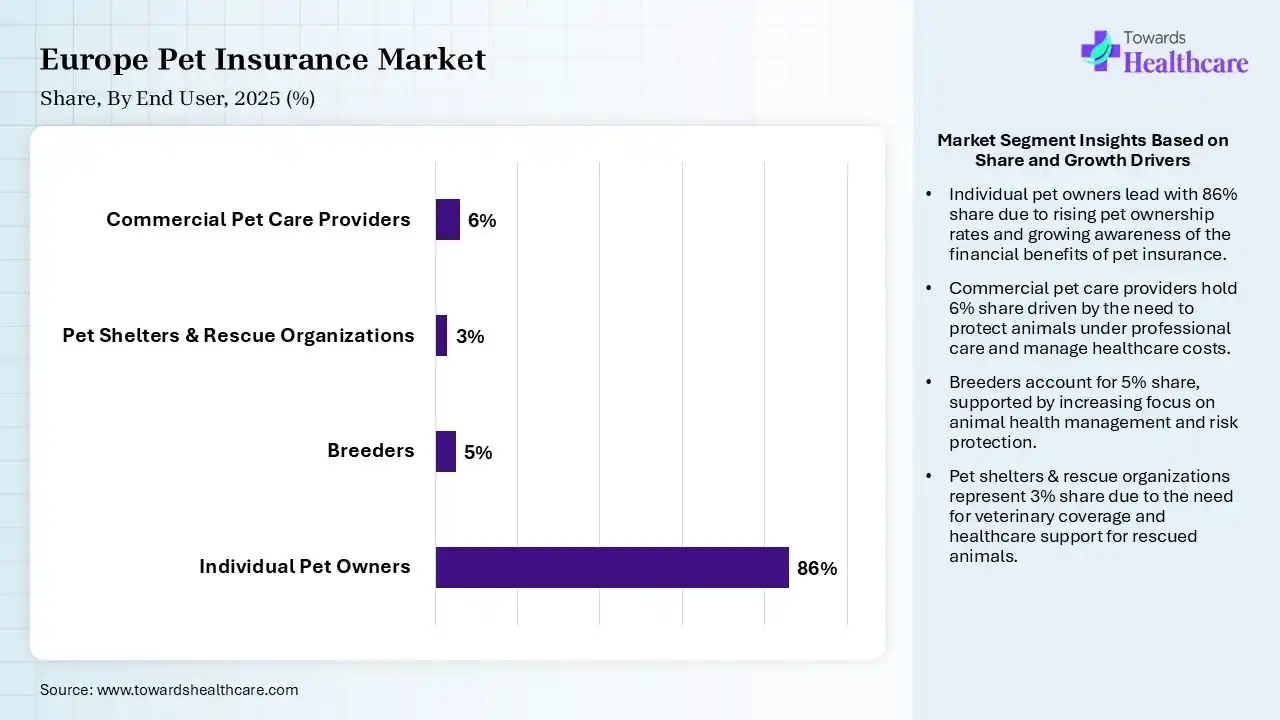

| Segment | Share 2025 (%) |

| Individual Pet Owners | 86% |

| Breeders | 5% |

| Pet Shelters & Rescue Organizations | 3% |

| Commercial Pet Care Providers | 6% |

The Individual Pet Owners Segment Dominated the Market With 86% in 2025

The individual pet owners segment held the largest revenue share of 86% of the Europe pet insurance market in 2025, due to a large pet ownership base, which increased their demand. A rise in emotional attachment also encouraged their spending. A rise in preventive healthcare awareness also supported their growth.

The commercial pet care providers segment held the second-largest share of 6% of the market in 2025 and is expected to grow with the fastest CAGR of 14.20% during the forecast period, driven by expanding pet daycare and boarding services, which create demand. Businesses seek liability and healthcare protection, which increases their use. Premium animal care trends also support their growth.

The breeders segment held 5% of the Europe pet insurance market share in 2025, driven by breeding operations, which seek risk mitigation. High-value animals require coverage, which drives the demand for various pet insurance coverages. Expanding regulatory standards, the need for continuous health monitoring, and maintaining breeding quality standards are also supporting their insurance adoption.

The pet shelters & rescue organizations segment held 3% of the market share in 2025, due to rising animal welfare initiatives and increasing healthcare spending. A rise in donor funding also supports insurance purchases. Increasing veterinary partnerships, advanced veterinary treatments, and routine healthcare services are also enhancing their access.

Europe pet insurance market is expected to grow significantly during the forecast period, due to growth in pet ownership. A rise in veterinary treatment costs and pet humanization trends has also increased the demand for pet insurance plans. Furthermore, the rapid expansion of insurance services and healthcare digitalization also enhanced the market growth.

UK Market Trends

The UK dominated the Europe pet insurance market with 31% in 2025 due to a highly developed pet insurance culture, which enhanced premiums. Strong insurer competition also improved coverage, which increased the use of various European pet insurance services. At the same time, high pet ownership also supported their growth.

The rest of Europe held an 8% share of the Europe pet insurance market in 2025 and is expected to grow at the fastest CAGR of 13.80% during the forecast period, driven by the improvement in penetration in emerging markets. New insurer entries are also expanding their access. Steadily expanding veterinary infrastructure is also enhancing accessibility to the various pet insurance plans.

| Companies | Headquarters | Europe Pet Insurance Solutions |

| Agria Djurforsakring | Stockholm, Sweden | Agria Lifetime Cover and Agria Vet Guide Integrated Plan |

| DFV Deutsche Familienversicherung AG | Frankfurt am Main, Germany | DFV Tierkrankenschutz and PETPROTECT |

| Petplan UK | Munich, Germany | Essential Plan and Petplan Lifetime Plan |

| Lassie AB | Stockholm, Sweden | Mini, Midi, and Maxi Plans |

| ManyPets | London, UK | Regular, Pre-existing, MoneyBack, and Value Policies |

| RSA Insurance Group | London, UK | MORE THAN Premier, MORE THAN Basic, and MORE THAN Classic |

| AXA SA | Paris, France | Formule Confort, Happy Pet and Formule Vitale |

In February 2025, after securing £12 million in a Series B funding round by Napo its co-founder and CEO, Jean-Philippe Doumeng, stated that “Our approach isn’t about cutting corners or offering cheap policies that don’t cover what matters,” “We’ve built Napo to offer proper protection that works, whether it’s dental care, behavioural support, or quick and fair claims handling”.

By Coverage Type

By Animal Type

By Policy Provider

By Distribution Channel

By End User

By Policy Duration

By Claim Type

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar