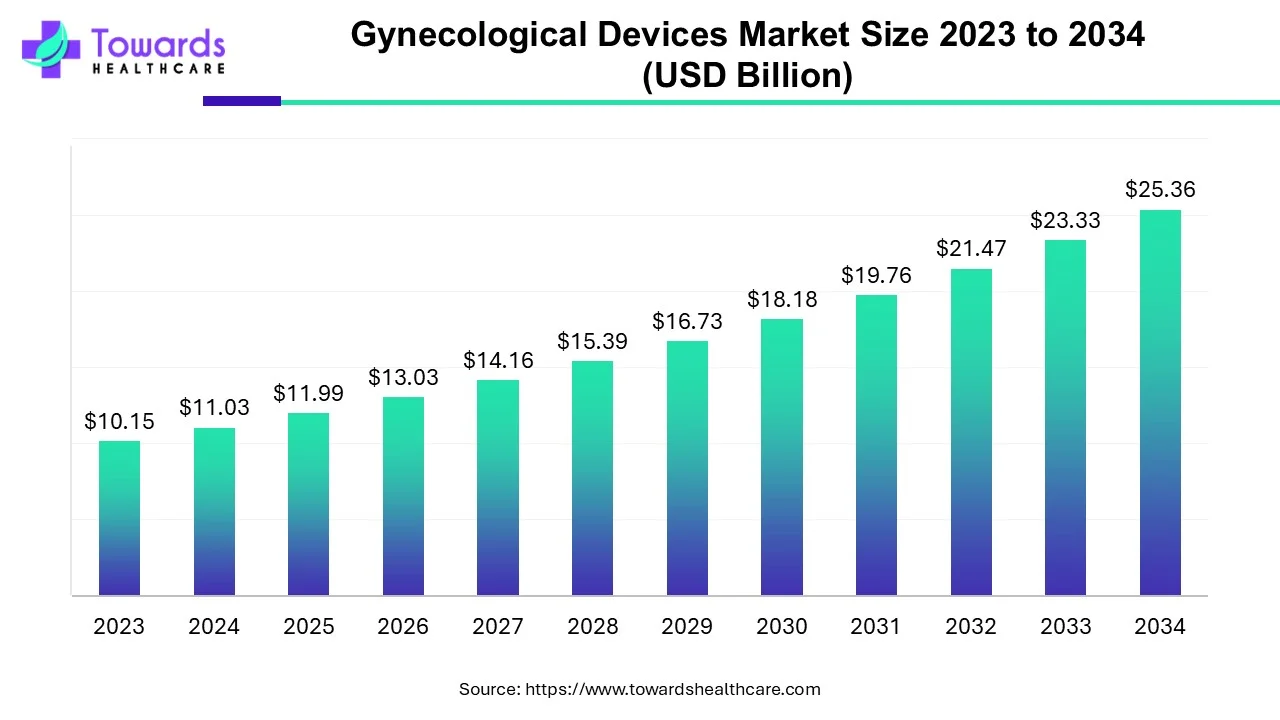

The global gynecological devices market size is calculated at USD 11.99 billion in 2025, grew to USD 27.56 billion in 2026, and is projected to reach around USD 27.56 billion by 2035. The market is expanding at a CAGR of 8.68% between 2026 and 2035. The growing demand for enhanced women’s health, combined with technological advancements, drives the market.

| Key Elements | Scope |

| Market Size in 2026 | USD 13.03 Billion |

| Projected Market Size in 2035 | USD 27.56 Billion |

| CAGR (2026 - 2035) | 8.68% |

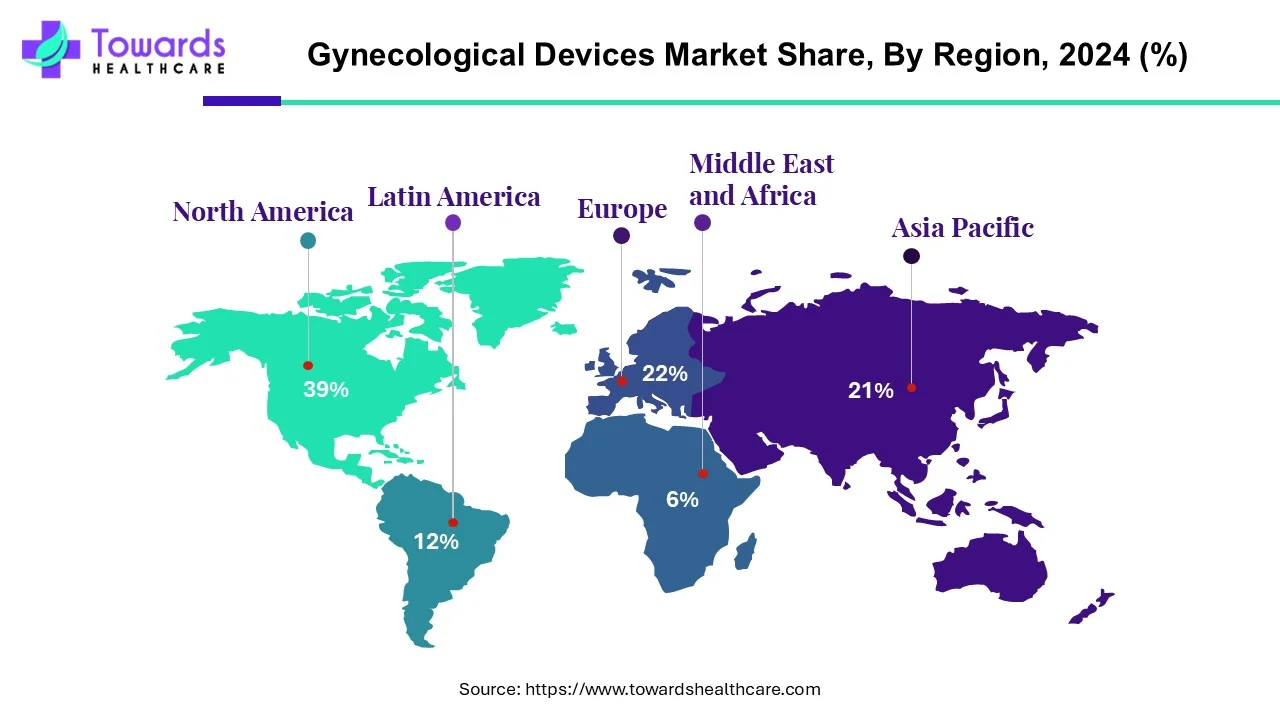

| Leading Region | North America by 39% |

| Market Segmentation | By Product, By End-Use, By Region |

| Top Key Players | Bioteque America, Boston Scientific, CooperSurgical, Inc., GE Healthcare, Gynemed, Gynex Corporation, Gynocare Services Pvt. Ltd., Medtronic plc, Olympus Corporation, Samsung Medison, Sonio SAS, Stryker Corporation, Veol Medical Technologies |

Gynecological devices are medical devices specifically designed for the care and treatment of women’s health. These devices aid in the diagnosis, treatment, and prevention of several gynecological disorders. Some common examples of gynecological devices include forceps & clamps, cervical dilators, vaginal speculums, scissors and retractors. These devices are used for a wide range of applications, from routine check-ups and prenatal care to surgical procedures. They are also used for managing gynecological cancers. These devices enable healthcare providers to diagnose conditions earlier, monitor pregnancies more effectively, and perform surgeries with greater precision and less invasiveness.

The rising prevalence of gynecological disorders increases the demand for gynecological devices. The increasing investments and collaborations lead to the development of gynecological devices. Favorable government policies and initiatives also support market growth. The growing research and development activities, as well as technological advancements, drive the latest innovations in gynecological devices. The burgeoning field of gynecology and obstetrics, along with the growing demand for women’s health, is driving market growth.

Integrating artificial intelligence (AI) and machine learning (ML) algorithms in gynecological devices introduces automation and enhances efficiency. AI aids in interpreting imaging data from diagnostic gynecological equipment, increasing precision and reducing manual errors. The advent of wearable devices and the Internet of Things (IoT) facilitate real-time monitoring of patient’s vital signs. This enables continuous surveillance of maternal health parameters, eliminating the need for patients to physically visit any healthcare setting. AI-enabled robots assist surgeons in performing complex surgeries, minimizing human intervention. Additionally, AI and ML can streamline the entire manufacturing process, enhancing reproducibility. AI-enabled predictive analytics detect potential errors in manufacturing, allowing manufacturers to make timely decisions.

Rising Prevalence of Gynecological Disorders

The major growth factor of the gynecological devices market is the rising prevalence of gynecological disorders. Endometriosis, fibroids, polycystic ovarian syndrome (PCOS), menstrual disorder, and cervical cancer, urinary incontinence are some common gynecological disorders affecting millions of women worldwide. According to the World Health Organization (WHO), PCOS affects around 6-13% of reproductive-aged women globally. While endometriosis affects around 10% of women globally, accounting for 190 million women. These disorders are majorly caused by improper female hygiene routines, unprotected intercourse, abortion, and insufficient diet and stress. These disorders result in an increasing number of gynecological surgeries. Additionally, the geriatric population is more prone to developing gynecological disorders, necessitating the use of gynecological devices. Hence, the growing geriatric population also contributes to market growth.

Stringent Regulatory Frameworks

The market faces formidable challenges, including stringent regulatory frameworks. Regulatory challenges include stringent safety standards and a lengthy approval process. Manufacturers must keep pace with evolving regulations across global markets, which can restrict market growth.

Sustainability

The future of the gynecological devices market is promising, driven by the growing demand for environmental sustainability. The rapidly changing climatic conditions, combined with favorable government initiatives, have led to a growing need for environmental sustainability. This encourages numerous manufacturers to develop eco-friendly gynecological devices. They mostly prefer environmentally friendly manufacturing processes and the development of single-use medical devices. Developing eco-friendly gynecological devices not only helps manufacturers adhere to local government policies but also benefits healthcare professionals. These devices reduce direct costs as well as reprocessing and administrative costs. A sustainable manufacturing process reduces waste generation, as well as energy and water consumption. Thus, by reducing their carbon footprint, medical facilities demonstrate their commitment to creating a more sustainable future for the planet.

Which Product Type Segment Held the Dominating Share of the Gynecological Devices Market?

By product, the surgical devices segment held a dominant presence in the gynecological devices market in 2024 and is expected to grow at the fastest CAGR during the forecast period. Surgical devices are classified into endoscopy devices, imaging systems, fluid management systems, and sterilization and contraceptive devices. The increasing number of gynecological surgeries, driven by the rising prevalence of gynecological disorders, boosts the segment’s growth. The growing demand for minimally invasive surgeries and technological advancements such as robotic systems have revolutionized gynecological surgeries. According to a recent survey by the KFF Women’s Health in the U.S., including 3,901 women, 8 out of 10 women used contraception. 21% of women preferred female sterilization, and 24% preferred intrauterine devices or contraceptive implants.

Diagnostic Imaging Systems Segment: Significantly Growing

By product, the diagnostic imaging systems segment is predicted to witness significant growth in the gynecological devices market over the forecast period. Gynecological disorders are detected using several diagnostic imaging systems such as ultrasound, CT scan, MRI, sonohysterography, PET/CT, etc. Several government organizations have launched initiatives and policies to promote the early detection of gynecological disorders. Advanced technologies such as AI and ML enhance the diagnostic accuracy of these systems, potentiating the segment’s growth. The growing awareness of women’s health has also encouraged women to have early disease diagnosis.

What Made Hospitals & Clinics the Dominant Segment in the Gynecological Devices Market?

By end-use, the hospitals & clinics segment led the global gynecological devices market in 2024. Hospitals & clinics possess experts from the multidisciplinary departments, providing multidisciplinary expertise to the patients. The availability of specialized equipment for different disorders, suitable capital investment, and favorable infrastructure boost the segment’s growth. Favorable reimbursement policies increase the accessibility and affordable of people, especially from middle- and low-income groups.

Ambulatory Surgical Centers (ASCs) Segment: Fastest-Growing

By end-use, the ambulatory surgical centers (ASCs) segment is anticipated to grow with the highest CAGR in the gynecological devices market during the studied years. ASCs offer state-of-the-art outpatient services to numerous patients, as they don’t require an overnight hospital stay. The growing demand for minimally invasive or non-invasive surgeries fuels the segment’s growth. ASCs contain specialized equipment and trained professionals. Tubal ligation, endometrial ablation, and cervical biopsy are the most common surgical procedures performed in ASCs.

")

North America dominated the global gynecological devices market share by 39% in 2024. The market's main drivers of growth are the emergence of big companies and the growing incidence of gynecological problems. In North America, the market is dominated by key companies, including Boston Scientific, CooperSurgical, Inc., LiNA Medical, and Surgmed Group. The industry is boosted by the growing use of cutting-edge technology for gynecological diagnosis and treatment. The market is supported by favorable government policies and rising investment. Modern research and development centers and sophisticated healthcare infrastructure support market expansion.

U.S. Market Trends

The National Institute of Child Health and Human Development (NICHHD)’s Gynecologic Health and Disease Branch (GHDB) supports gynecologic research and career development programs to improve women’s reproductive health. The increasing number of gynecologists and obstetricians also contributes to market growth. There are currently 46,554 obstetricians and gynecologists in the U.S.

Canada Market Trends

The Minister of Health, Government of Canada, announced an investment of $1.7 million to support projects related to women’s reproductive health. More than $1.2 million will be provided to the Society of Obstetricians and Gynecologists of Canada to develop and distribute tools and resources, improving access to menopause-specific health services.

Asia-Pacific is projected to host the fastest-growing gynecological devices market in the coming years. The increasing geriatric population and the growing awareness of women’s health drive the market. Several government and private institutions organize workshops, symposiums, and conferences to create awareness among the general public. Favorable reimbursement policies by both government and private organizations facilitate advanced care and treatment. Government bodies are making constant efforts to increase the accessibility of women’s treatment.

China Market Trends

The increasing number of maternal health facilities govern the market in China. China has more than 26,000 maternal health facilities, allowing over 90% of Chinese households to reach the nearest facility within 15 minutes. The Chinese government promotes the indigenous manufacturing of medical devices and attracts foreign investors and manufacturers to set up their manufacturing facilities.

India Market Trends

India plans to set up a national registry for women with endometriosis to enhance research efforts, improve diagnosis and care, and support the development of targeted policies and interventions. The Indian government announced an investment of Rs 6000 crore under the PLI scheme in Budget 2024 for the medical device and pharma sectors.

Europe is observed to grow at a considerable growth rate in the gynecological devices market in the upcoming period. The growing research and development activities and the rising adoption of advanced technologies propel the market. The European government plays a vital role in promoting market growth by improving standards of care and supporting research and innovation in the field. The increasing prevalence of gynecological disorders favors the market. The rising healthcare expenditure and increasing awareness of women’s reproductive health foster market growth.

Germany Market Trends

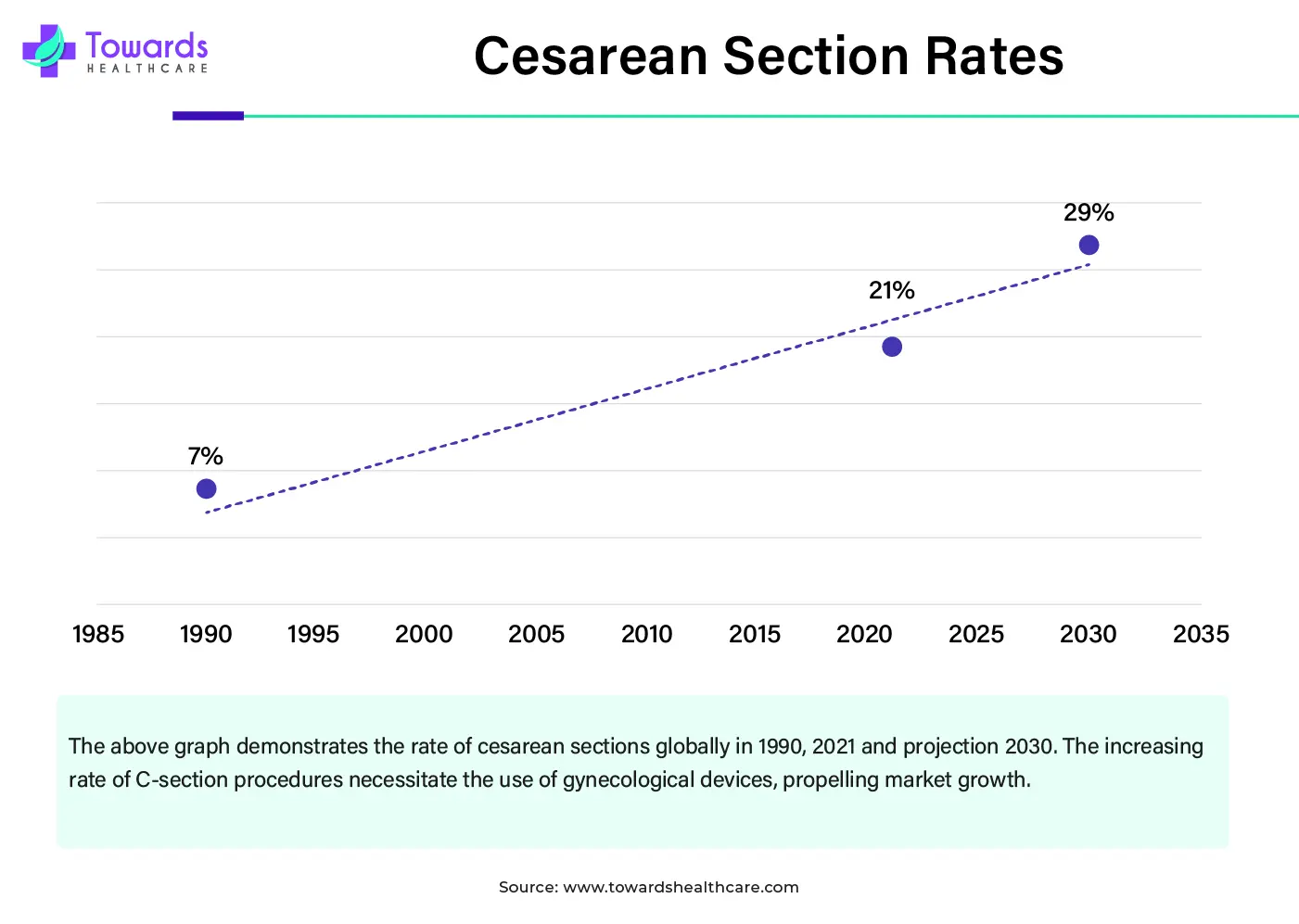

Germany performs the highest number of cesarean sections, accounting for 230,200 surgeries annually. The German government’s Federal Ministry of Education and Research (BMBF) provided an additional 800,000 euros to support research in reproductive health in Leipzig and the training of young individuals. The funding will be used for installing modern equipment to conduct advanced research, enabling detailed data analysis with greater precision.

South America is expected to grow significantly in the gynecological devices market during the forecast period, due to growing women’s health awareness. The increasing government campaigns are also increasing awareness, driving the demand for various gynecological devices. Additionally, increasing gynecological conditions are also increasing their use, promoting the market growth.

Brazil Gynecological Devices Market Trends

The expanding industries in Brazil are increasing the production of gynecological devices, where the increasing screening programs are raising women’s health awareness. The growing gynecological disorders are also increasing their demand, and companies are also developing advanced technologies.

MEA is expected to grow significantly in the gynecological devices market during the forecast period, due to the expanding healthcare sector. At the same time, the growing government women's health campaign is also increasing awareness, driving the early diagnosis of various gynecologic disorders. The companies are actively developing new devices, which are backed by investment, enhancing the market growth.

Saudi Arabia Gynecological Devices Market Trends

The growing incidence of gynecological disorders across Saudi Arabia is increasing the demand for gynecological devices. The growing focus on minimally invasive procedures and expanding fertility clinics is also increasing their adoption rates. The growing government support is also encouraging their use.

R&D

Clinical Trials and Regulatory Approvals

Formulation and Final Dosage Preparation

Packaging and Serialization

Patient Support and Services

Yong Kwan Kim, CEO of Samsung Medison, commented that the acquisition of Sonio will continue to deliver upon their promise to improve the quality of people’s lives with technology. He added that the collaboration was made to combine Sonio’s best-in-class ultrasound AI technology and reporting capabilities to bring a paradigm shift in the prenatal ultrasound exam.

By Product

By End-Use

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar