")

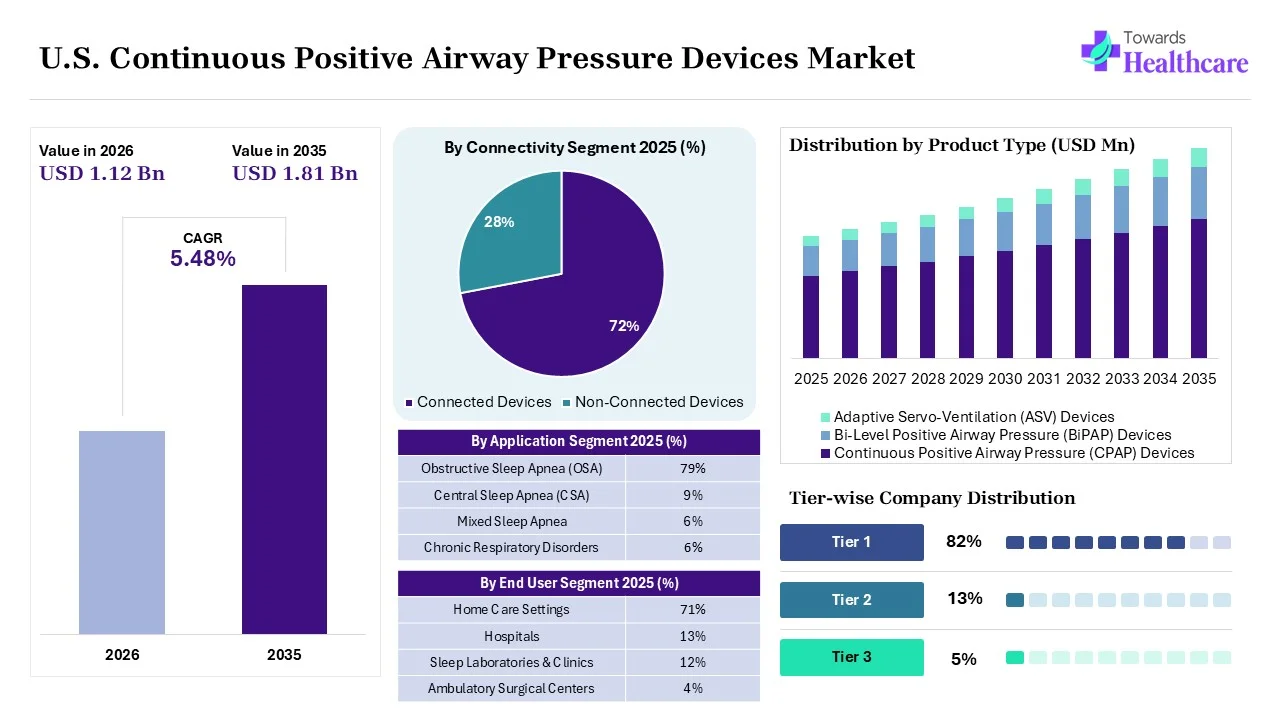

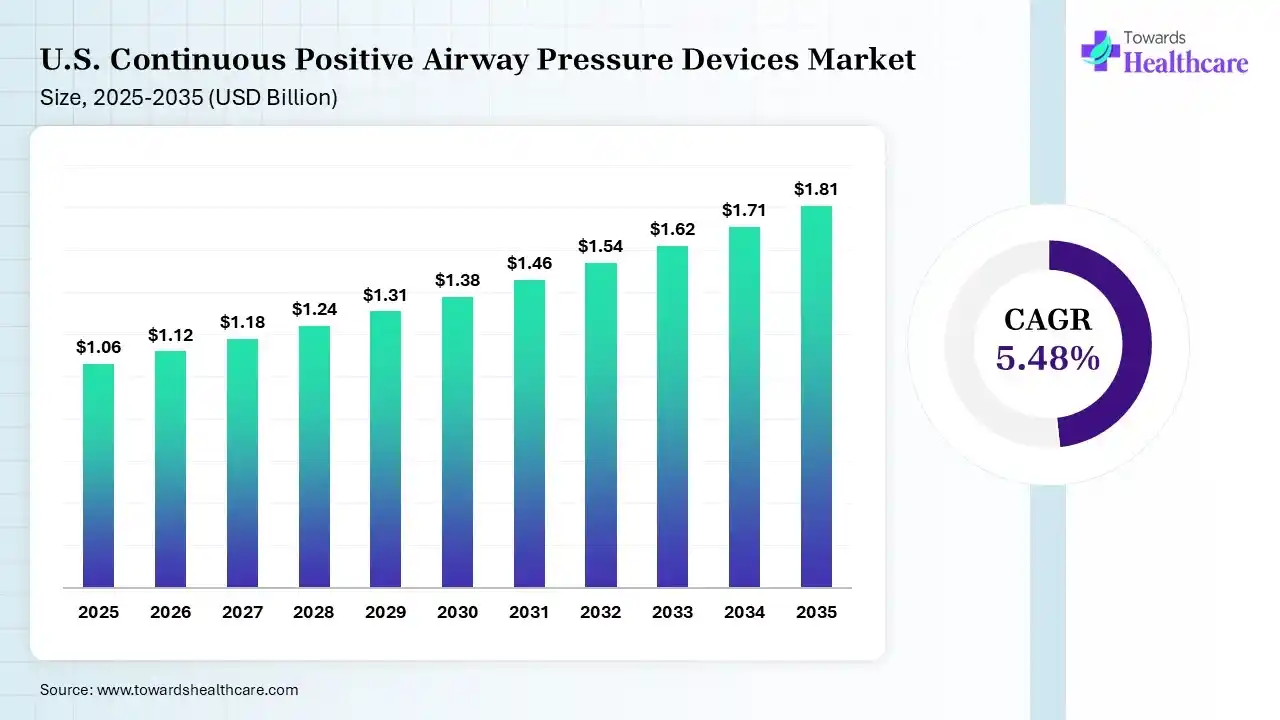

The U.S. continuous positive airway pressure devices market size was estimated at USD 1.06 billion in 2025 and is predicted to increase from USD 1.12 billion in 2026 to approximately USD 1.81 billion by 2035, expanding at a CAGR of 5.48% from 2026 to 2035. The market grew in 2025 due to increasing sleep apnea prevalence and growing awareness of CPAP therapy. In 2026, demand is rising with improved homecare adoption and smart CPAP technologies. Future growth will be driven by wearable integration and expanding sleep disorder diagnosis. The U.S. leads through advanced healthcare infrastructure, high diagnosis rates, and favorable reimbursement.

")

A medical device that delivers a sustained stream of pressurized air through a mask to maintain airways open while sleeping, which has been transforming highly across the U.S. U.S. continuous positive airway pressure devices market is bolstering as these machines are majorly prescribed in diverse conditions, like obstructive sleep apnea, heavy snoring, & other breathing-related sleep disorders. The overall market progression is impacted by the growing instances of obesity & a notable rise in the geriatric population. Another key driver is emerging AI-driven coaching, cloud-based data access, & remote patient monitoring platforms that coordinate directly with health providers.

The upcoming years will focus on adopting ML models that process breathing patterns, use stats & feedback to estimate early adherence patterns, and identify which patients are at risk of abandoning CPAP therapy. Recent developments include the latest ML models rolled out by Mount Sinai Hospital, which assess individual sleep data to estimate whether a patient will benefit from CPAP therapy or experience cardiovascular harm, fostering CPAP treatment into the era of tailored medicine.

Day by day, the U.S. market is increasingly promoting devices that show seamless connection via cellular or Bluetooth to cloud-based platforms and mobile apps. Whereas patients & providers can review sleep metrics daily, it also enables remote prescription updates and troubleshooting. Moreover, the leading firms are spurring innovation into minimalist designs to lower claustrophobia & facial pressure. Furthermore, these groundbreakings cover custom, 3D-printed CPAP masks molded exactly to the unique contours of a user's face for the virtual elimination of unintentional air leaks.

Spurring Miniaturization for Travel

The U.S. is experiencing a massive demand for ultra-compact, travel-friendly CPAP machines that are FDA-cleared & battery-operable, with priority for portability without compromising the core pressure delivery mechanisms.

Progressing Material Science Innovations

Prospective era will raise developments into quieter motors, sophisticated sound-dampening materials, & optimized heated humidification systems to mitigate rainout and dry mouth.

Investigating Clinical Outcomes & Comorbidities

Ongoing observational studies, such as those by the US Department of Veterans Affairs, are researching the unification of consumer wearables with CPAP usage for accurate tracking of sleep quality, systemic conditions, and blood pressure reductions.

| Table | Scope |

| Market Size in 2026 | USD 1.12 Billion |

| Projected Market Size in 2035 | USD 1.81 Billion |

| CAGR (2026 - 2035) | 5.48% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Connectivity, By End User, By Application, By Distribution Channel |

| Top Key Players | ResMed, Koninklijke Philips N.V. (Philips Respironics), Fisher & Paykel Healthcare, React Health (formerly 3B Medical), BMC Medical Co., Ltd. Transcend Inc. (Somnetics International), Breas Medical, Wellell Inc. (formerly Apex Medical), Drive DeVilbiss Healthcare, Löwenstein Medical |

")

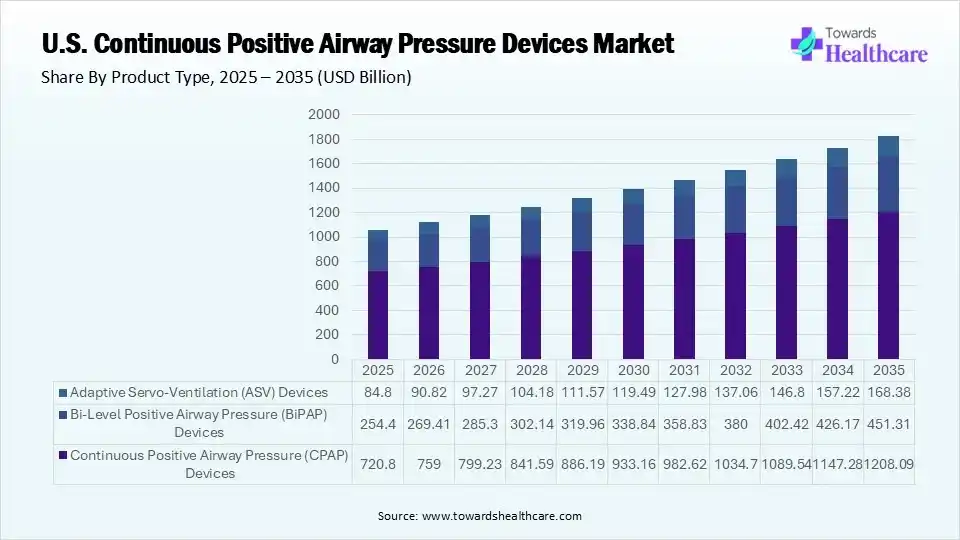

| Segment | Share 2025 (%) |

| Continuous Positive Airway Pressure (CPAP) Devices | 68% |

| Bi-Level Positive Airway Pressure (BiPAP) Devices | 24% |

| Adaptive Servo-Ventilation (ASV) Devices | 8% |

The Continuous Positive Airway Pressure (CPAP) Devices Segment Led the Market in 2025

In 2025, the continuous positive airway pressure (CPAP) devices segment held a major share of 68.00% of the U.S. continuous positive airway pressure devices market. Dominance is driven by its prominent use to treat Obstructive Sleep Apnea (OSA) cases across the U.S. Alongside, advanced, latest CPAP devices are enabling an integration with smartphone apps, which enable patients to track their therapy & give doctors remote access to adherence data.

The bi-level positive airway pressure (BiPAP) devices segment held the second-largest share of a 24.00% in 2025. These devices are highly employed among patients who need higher pressure support. Also, devices enhance comfort for complex cases, coupled with the expansion of reimbursement that supports uptake.

On the other hand, the adaptive servo-ventilation (ASV) devices segment captured a 8.00% share in 2025 & is predicted to expand at the 7.10% CAGR. Respective demand is fueled by the emergence of advanced algorithms that improve treatment results. In addition, the widespread adoption of these devices for complex sleep-disordered breathing, along with developing technological innovations, is boosting their effectiveness.

")

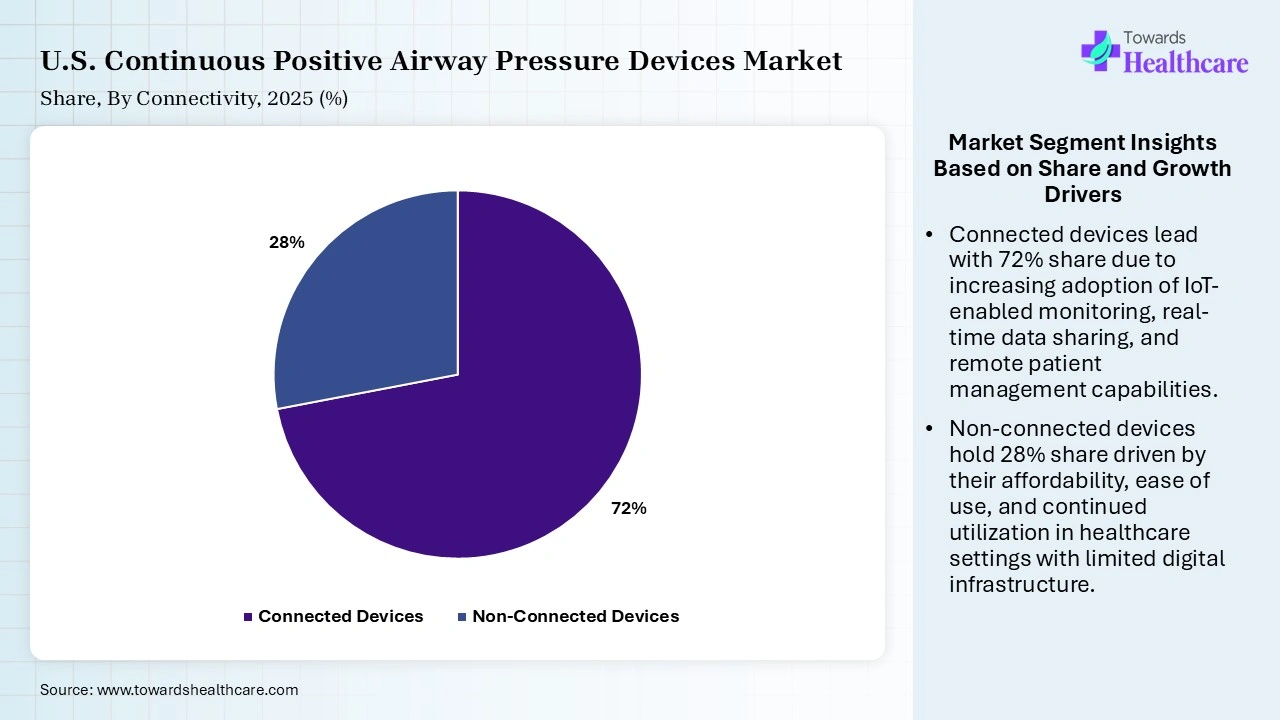

| Segment | Share 2025 (%) |

| Connected Devices | 72% |

| Non-Connected Devices | 28% |

The Connected Devices Segment Dominated the Market in 2025

The connected devices segment led with a 72.00% share in 2025 & is estimated to show rapid expansion at the 6.60% CAGR in the U.S. continuous positive airway pressure devices market. These kinds of devices enable healthcare providers to monitor nightly use, cover leaks, & therapy efficacy in real time. Continuous advances are promoting home-based testing & ambulatory respiratory care, naturally guiding patients toward connected home-care medical equipment.

The non-connected devices segment accounted for the second-largest share of a 28.00% in 2025, due to the demand persisting in cost-sensitive settings. These devices offer a simpler operation that appeals to selected users. Moreover, they are considered legacy installed bases, which assists in accelerating sales.

")

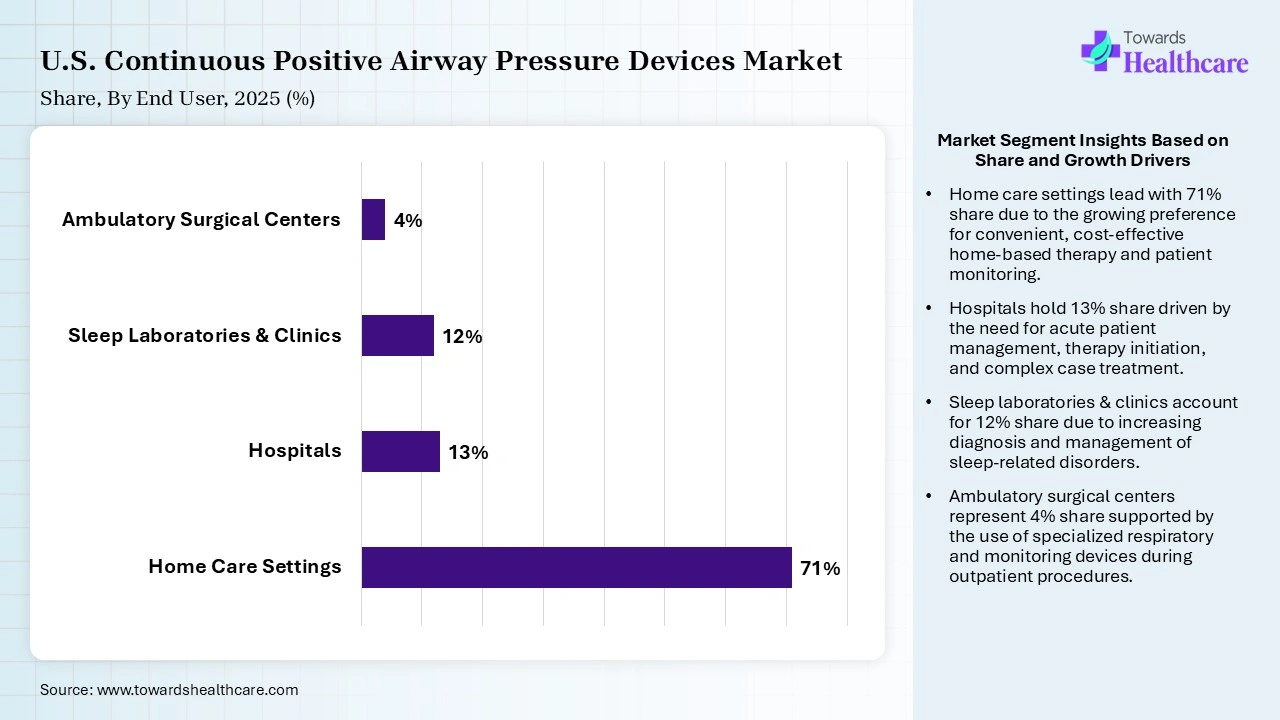

| Segment | Share 2025 (%) |

| Home Care Settings | 71% |

| Hospitals | 13% |

| Sleep Laboratories & Clinics | 12% |

| Ambulatory Surgical Centers | 4% |

The Home Care Settings Segment Was Dominant in the Market in 2025

The home care settings segment dominated with a 71.00% share in 2025 & is anticipated to expand at the 6.20% CAGR in the U.S. continuous positive airway pressure devices market. Increasing demand for decentralized diagnostics, surged patient preference for comfort, & the broader adoption of remote patient-monitoring solutions, driving the segmental expansion. Nowadays, key firms are exploring modern CPAP systems that are more compact, travel-friendly, with adaptive pressure adjustments & comfortable mask designs that have raised patient compliance.

In 2025, the hospitals segment accounted for a notable share of 13.00% in 2025, due to higher facilities of diagnosis & treatment initiation. The U.S. is expanding awareness regarding sleep disorders, which ultimately increases demand for the advanced devices & hospital assistance. Ongoing steps into the development of a better respiratory care infrastructure are aiding growth.

The sleep laboratories & clinics segment held a 12.00% share of the market in 2025. Massively rising sleep testing volumes are driving the use of advanced equipment. These end users facilitate specialized care centers with a wide range of services. Surging diagnosis rates are also impacting the overall growth of these clinics & supporting demand.

The ambulatory surgical centers segment held a 4.00% share of the U.S. continuous positive airway pressure devices market. Consistent expansion of outpatient procedures necessitates respiratory support. Also, these centers provide affordable care models that encourage their utilization across the U.S. Besides this, developing clinical monitoring requirements is sustaining demand for these centers.

")

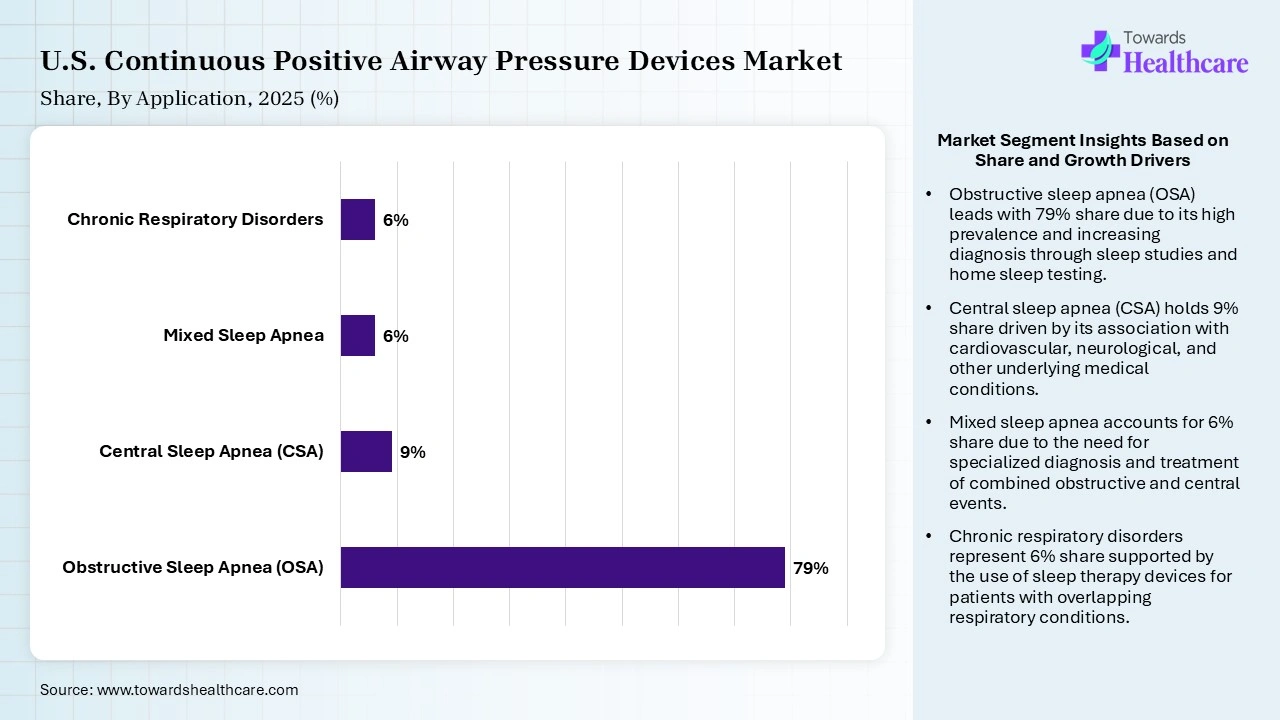

| Segment | Share 2025 (%) |

| Obstructive Sleep Apnea (OSA) | 79% |

| Central Sleep Apnea (CSA) | 9% |

| Mixed Sleep Apnea | 6% |

| Chronic Respiratory Disorders | 6% |

The Obstructive Sleep Apnea (OSA) Segment Led the Market in 2025

In 2025, the obstructive sleep apnea (OSA) segment held a dominant share of 79.00% of the market. According to a survey, there were nearly 77 to 83.7 million affected adults found with OSA in the U.S., which is fueled by a rise in obesity cases, the geriatric population, anatomical factors, & rising diagnoses among females. Certain medical conditions, including type 2 diabetes, hypertension, congestive heart failure, & endocrine disorders, are closely linked with OSA development.

Whereas the central sleep apnea (CSA) segment accounted for a lucrative share of 9.00% in 2025. Key drivers are rising cases of brainstem injuries, strokes, & degenerative neurological disorders that directly disturb the brain's respiratory center. Alongside, the U.S. is facing chronic, high-dose use of opioids, which represses the central nervous system & changes the body’s chemical response to CO2 levels.

The chronic respiratory disorders segment captured a 6.00% share in 2025 & is estimated to witness the fastest growth at the 6.80% CAGR in the U.S. continuous positive airway pressure devices market. Significantly, the surging burden of an ageing population is resulting in these cases, which bolsters the use of PAP therapy to assist respiratory management. Furthermore, elevating particulate matter, ozone, & industrial emissions are majorly exacerbating chronic respiratory symptoms & lead to lung diseases.

The mixed sleep apnea segment accounted for a 6.00% share in 2025, due to the use of better diagnostic technologies that identify these mixed conditions. In addition, the accelerating use of opioids and sedatives, coupled with metabolic/cardiovascular comorbidities, fuels the demand for personalised therapy in mixed sleep apnea. The growing shift towards Auto-titrating PAP & Adaptive Servo-Ventilation systems supports the finding of mixed apnea.

")

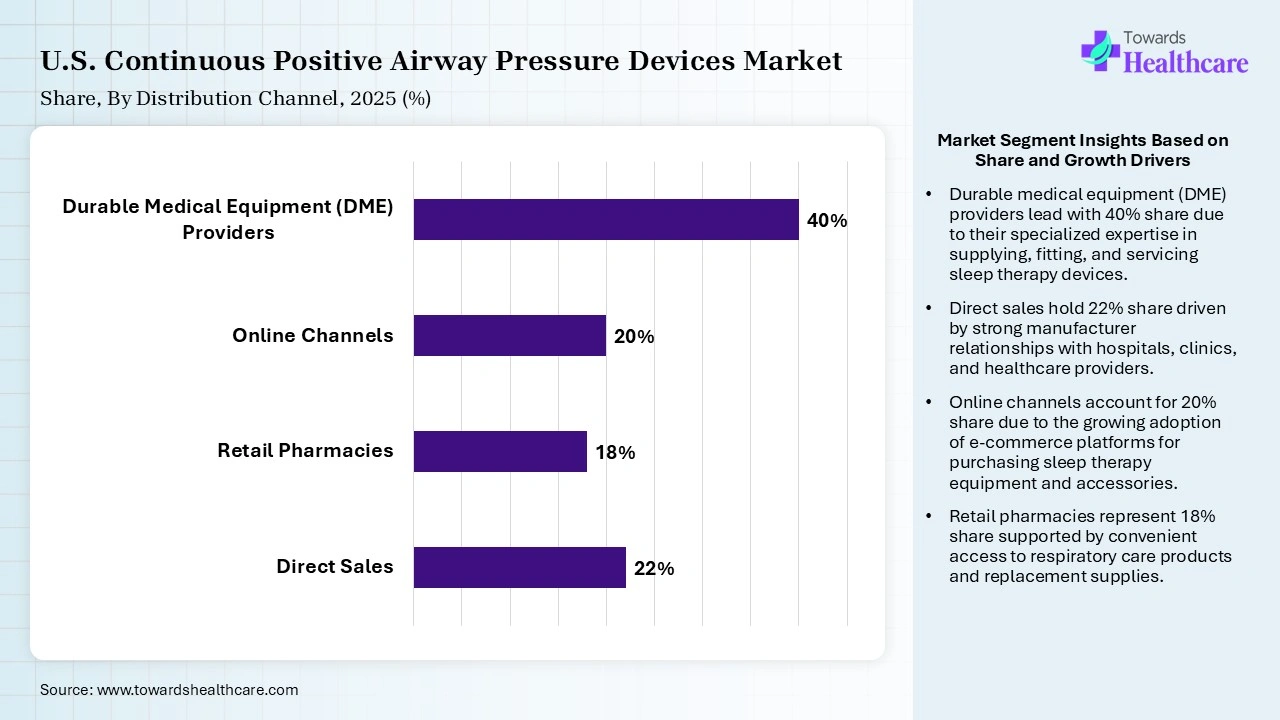

| Segment | Share 2025 (%) |

| Direct Sales | 22% |

| Retail Pharmacies | 18% |

| Online Channels | 20% |

| Durable Medical Equipment (DME) Providers | 40% |

The Durable Medical Equipment (DME) Providers Segment Dominated the Market in 2025

The durable medical equipment (DME) providers segment held a major share of 40.00% of the market in 2025. The dominance is propelled by manufacturers developing portable, lightweight, & quieter devices, which impels DME providers to stock advanced models that foster higher patient adherence. Major supply chain transitions are pushing DME providers to modify vendor relationships & shift patients to alternative OEM brands.

However, the direct sales segment captured the second-largest share of 22.00% of the U.S. continuous positive airway pressure devices market. Nowadays, robust manufacturers are reinforcing direct customer relationships. Alongside, they are offering better service support that improves retention.

However, the online channels segment held a 20.00% share in 2025 & is predicted to expand rapidly at the 7.40% CAGR in the market. These types of channels are facilitating digital purchasing that enables convenience & competitive pricing. Ongoing progression of telemedicine is spurring online prescriptions. Additionally, massive e-commerce penetration is accelerating sales.

In 2025, the retail pharmacies segment accounted for a 18.00% share of the U.S. continuous positive airway pressure devices market. These pharmacies offer accessibility, which fosters consumer purchases. The widespread expansion of respiratory product offerings is raising availability. Many trusted pharmacy networks are aiding adoption.

The U.S. continuous positive airway pressure devices market has been bolstering, with the new execution of new manufacturing rules by the FDA, which require medical device makers to synchronize with global standards (ISO 13485). This further shows the impact of how CPAP manufacturers document & control the design, production, & distribution of their devices. Alongside, the Centers for Medicare & Medicaid Services (CMS) continues to implement adherence thresholds, generally necessitating a 90-day trial where patients must showcase adequate compliance before long-term coverage is approved.

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Company | Distribution |

| ResMed | They have introduced AirSense 11 AutoSet, AirMini, & AirFit series masks |

| Koninklijke Philips N.V. (Philips Respironics) | Their key products include DreamStation 2 Auto CPAP & DreamWear mask systems. |

| Fisher & Paykel Healthcare | A firm has developed robust SleepStyle Auto CPAP & F&P Evora/Simplus masks |

| React Health (formerly 3B Medical) | They implemented diverse affordable products, such as Luna G3 Auto-CPAP, Luna II, & Brio travel CPAP. |

| BMC Medical Co., Ltd. | Their economical solutions cover RESmart Auto CPAP & the iBreeze series. |

| Transcend Inc. (Somnetics International) | A leader offers micro-sized, extremely lightweight, battery-powered systems, like Transcend Micro and Transcend 365 miniCPAP. |

| Breas Medical | A company has unveiled Z2 Auto Travel CPAP, the iSleep series. |

| Wellell Inc. (formerly Apex Medical) | They have explored the iCH Auto CPAP and XT series. |

| Drive DeVilbiss Healthcare | They marketed AutoPAP/IntelliPAP systems, which have medical-grade durability, smartCode compliance tracking, & reliable, streamlined controls. |

| Löwenstein Medical | Their prominent offering is the prismaLINE series |

In June 2026, ProSomnus Sleep Technologies & MonitAir, LLC announced a partnership to foster connected, longitudinal & tailored care for patients with Obstructive Sleep Apnea (OSA). Edward Mezerhane, MD, Chief Executive Officer of MonitAir, LLC, commented that the integration of the high-fidelity data from the ProSomnus RPMOâ‚‚ OSA Device directly into MonitAir's extensive monitoring platform gives clinicians the longitudinal visibility they need.

In February 2026, Resmed launched the AirTouch F30i Comfort, a new full face CPAP mask with a soft, breathable fabric tested by the company for its moisture-wicking properties.

By Product Type

By Connectivity

By End User

By Application

By Distribution Channel

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar