Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

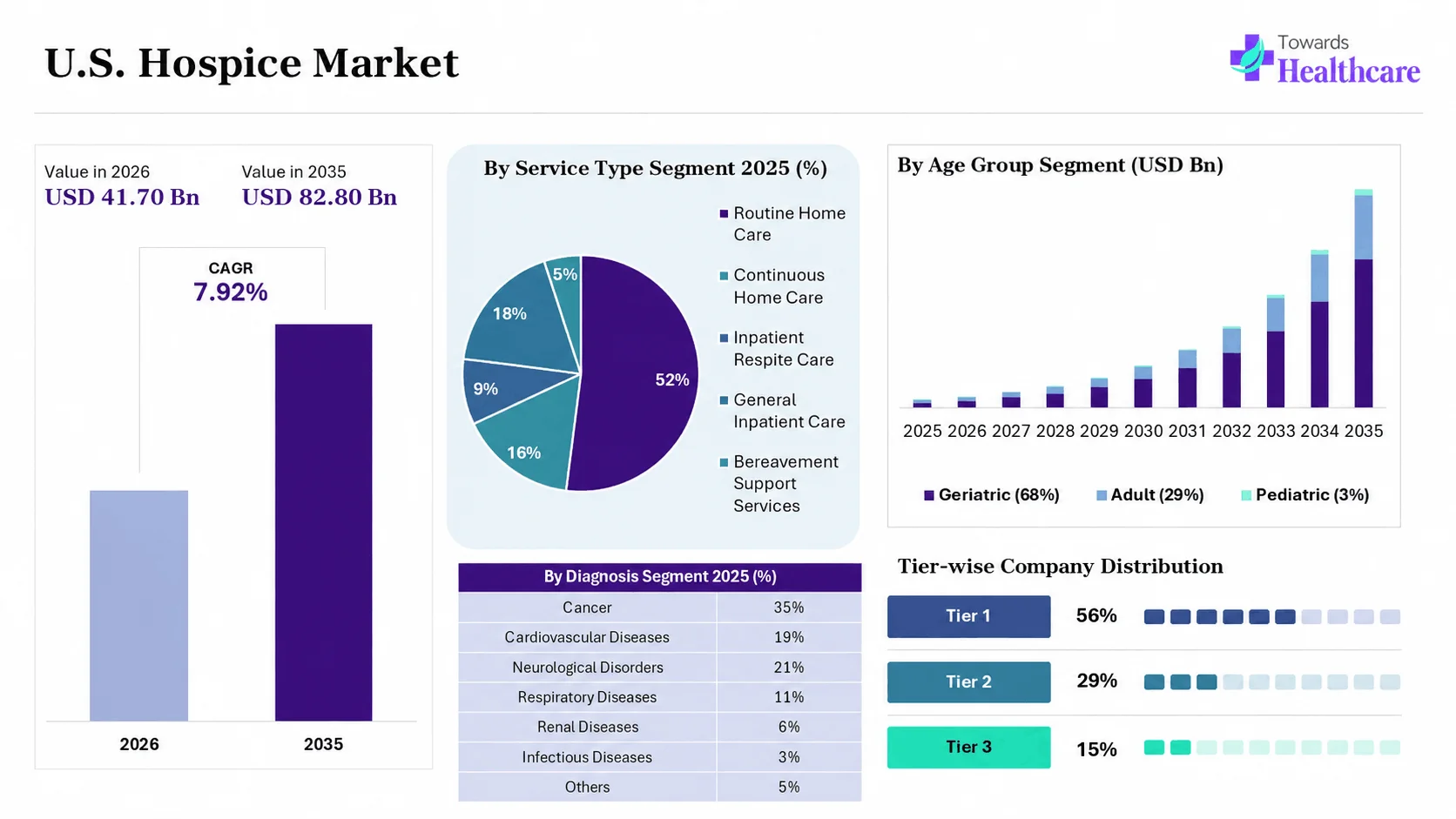

The U.S. hospice market size was estimated at USD 38.64 billion in 2025 and is predicted to increase from USD 41.7 billion in 2026 to approximately USD 82.8 billion by 2035, expanding at a CAGR of 7.92% from 2026 to 2035. The market is growing steadily due to an increasing aging population, rising incidence of chronic and life-limiting diseases, and greater demand for compassionate end-of-life care services. Market expansion is further supported by broader access to home-based hospice care, favorable reimbursement frameworks, and continuous improvements in palliative care delivery.

")

")

Hospice is specialized care that focuses on improving the quality of life and providing comfort, pain management, and emotional support for individuals with illness, typically when curative treatment is no longer the primary goal. The U.S. hospice market is growing due to the growing elderly population, increasing prevalence of chronic and terminal illness, and rising preference for patient-centered end-of-life care. Greater awareness of hospice benefits, improved access to home-based services, and supportive Medicare reimbursement policies are further encouraging adoption. Additionally, healthcare providers are increasingly focusing on enhancing quality of life and comfort for patients with advanced-stage diseases.

Artificial intelligence is transforming the market by enabling predictive analytics for patient care planning, improving symptom monitoring, and supporting timely clinical interventions. AI-powered tools help optimize resource allocation, streamline administrative tasks, and enhance communication between caregivers and healthcare providers. These capabilities can improve care quality, reduce operational burdens, and support more personalized end-of-life care experiences for patients and families.

| Table | Scope |

| Market Size in 2026 | USD 41.7 Billion |

| Projected Market Size in 2035 | USD 82.8 Billion |

| CAGR (2026 - 2035) | 792% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Diagnosis, By Care Setting, By Ownership, By Age Group, By End User, By Payment Source |

| Top Key Players | Chemed Corporation (VITAS Healthcare), Amedisys, Gentiva, Brookdale Senior Living, Inc., Seasons Hospice & Palliative Care |

")

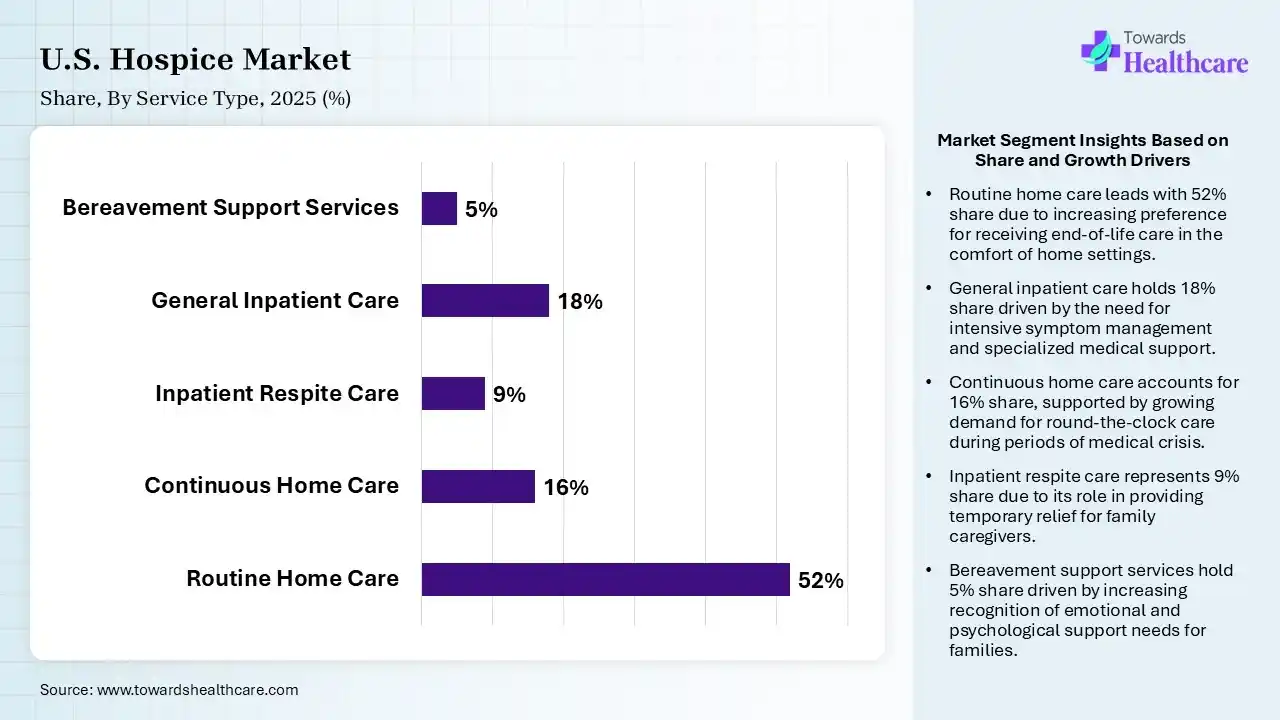

| Segment | Share 2025 (%) |

| Routine Home Care | 52% |

| Continuous Home Care | 16% |

| Inpatient Respite Care | 9% |

| General Inpatient Care | 18% |

| Bereavement Support Services | 5% |

The Routine Home Care Segment Dominated the U.S. Hospice Market in 2025

The routine home care segment held a dominant share of 52% in 2025 because it allows patients to receive continuous end-of-life care in the comfort of their homes, while maintaining independence and family involvement. This service is more cost-effective than inpatient hospice care and is supported by favorable reimbursement policies. Increasing preference for personalized, home-based care and the growing aging population further strengthen the segments leafing position.

The general inpatient care held the second-largest share of 59% in 2025 because it provides intensive symptom management and round-the-clock medical supervision for patients experiencing severe pain or an acute complication that cannot be managed at home. Growing demand for specialized end-of-life care, coupled with increasing cases of advanced chronic diseases, continues to support the segment’s significant market presence.

The continuous home care segment held a 16% share in 2025 and is expected to grow at the fastest CAGR of 8.90% in the U.S. hospice market during the forecast period due to the rising demand for intensive nursing support at home during periods of acute symptom crises. Patients and families increasingly prefer receiving advanced care in familiar surroundings, reducing hospital visits and improving comfort. Growing adoption of the home-based healthcare model and advancements in remote patient monitoring are further accelerating market growth.

The inpatient respite care segment held a 9% market share due to families and caregivers increasingly seeking temporary professional care for hospice patients during periods of caregiver exhaustion, personal commitments, or emergencies. These services ensure continuity of quality care while reducing caregivers' stress and burnout. Rising awareness of caregivers’ well-being, along with the growing number of hospice patients requiring long-term support, is contributing to the segment’s steady growth.

")

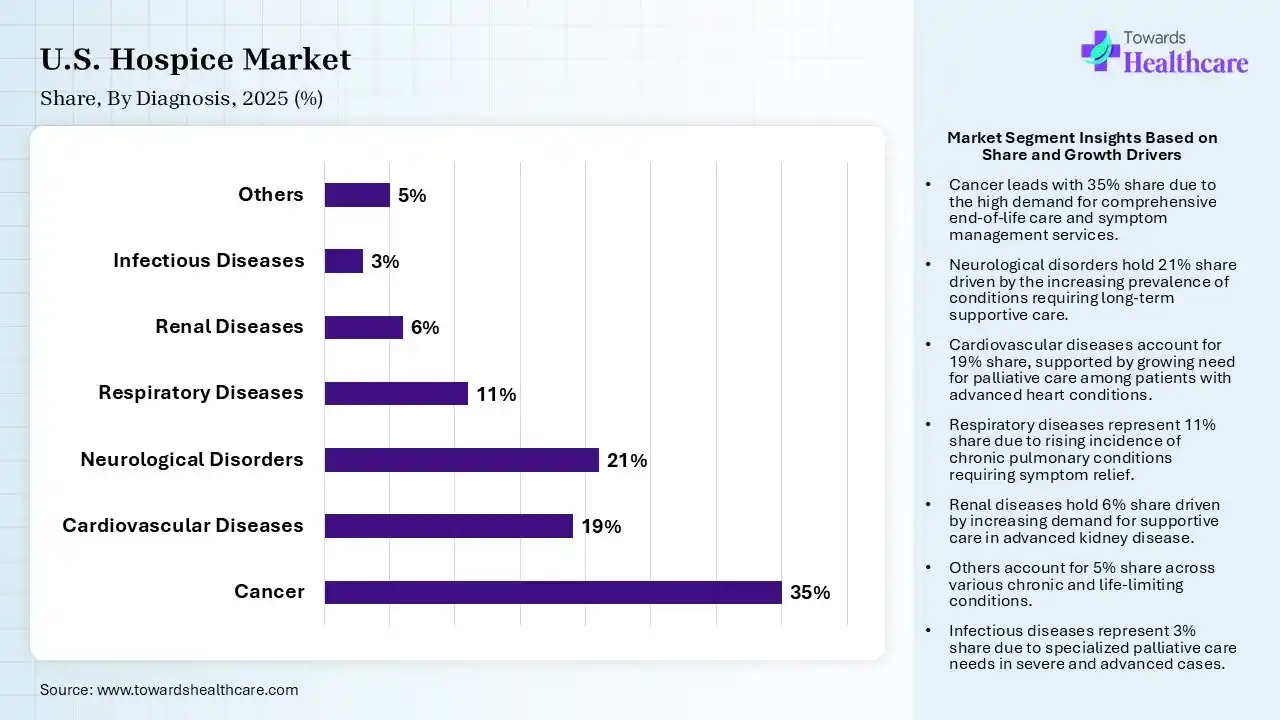

| Segment | Share 2025 (%) |

| Cancer | 35% |

| Cardiovascular Diseases | 19% |

| Neurological Disorders | 21% |

| Respiratory Diseases | 11% |

| Renal Diseases | 6% |

| Infectious Diseases | 3% |

| Others | 5% |

The Cancer Segment Led the U.S. Hospice Market in 2025 with the Largest Share

The cancer segment led the market with a share of 35% in 2025 due to patients with advanced-stage cancer often require comprehensive pain management, symptom control, and end-of-life support. The high prevalence of cancer, a well-defined disease progression, and greater awareness of hospice benefits encourage early hospice enrollment. Additionally, healthcare providers frequently recommend hospice services for terminal cancer patients to improve comfort, quality of life, and emotional support.

The neurological disorders segment held the second-largest share of 21% in 2025 and is expected to grow at the fastest CAGR of 8.70% in the market during the forecast period due to the increasing prevalence of conditions such as Alzheimer’s disease, Parkinson’s disease, and other progressive neurodegenerative disorders. These diseases often require long-term symptom management, specialized supportive care, and continuous assistance with daily activities. Growing aging demographics and rising demand for quality end-of-life care are further driving hospice utilization among neurological disorder patients.

The cardiovascular diseases segment held 19% of the U.S. hospice market share due to the rising prevalence of heart failure, stroke, and other advanced cardiac conditions among the aging population. Patients with end-stage cardiovascular diseases often require symptom relief, pain management, and supportive care to improve quality of life. Increasing awareness of hospice benefits and a greater focus on patient-centered end-of-life care are further driving segment growth.

The respiratory diseases segment held an 11% market share due to the increasing prevalence of chronic obstructive pulmonary disease (COPD), pulmonary fibrosis, and advanced lung disorders. The conditions often cause severe breathing difficulties and require ongoing symptom management and supportive care. Growing awareness of hospice services, an aging population, and the need to improve patient comfort and quality of life are further supporting segment growth.

")

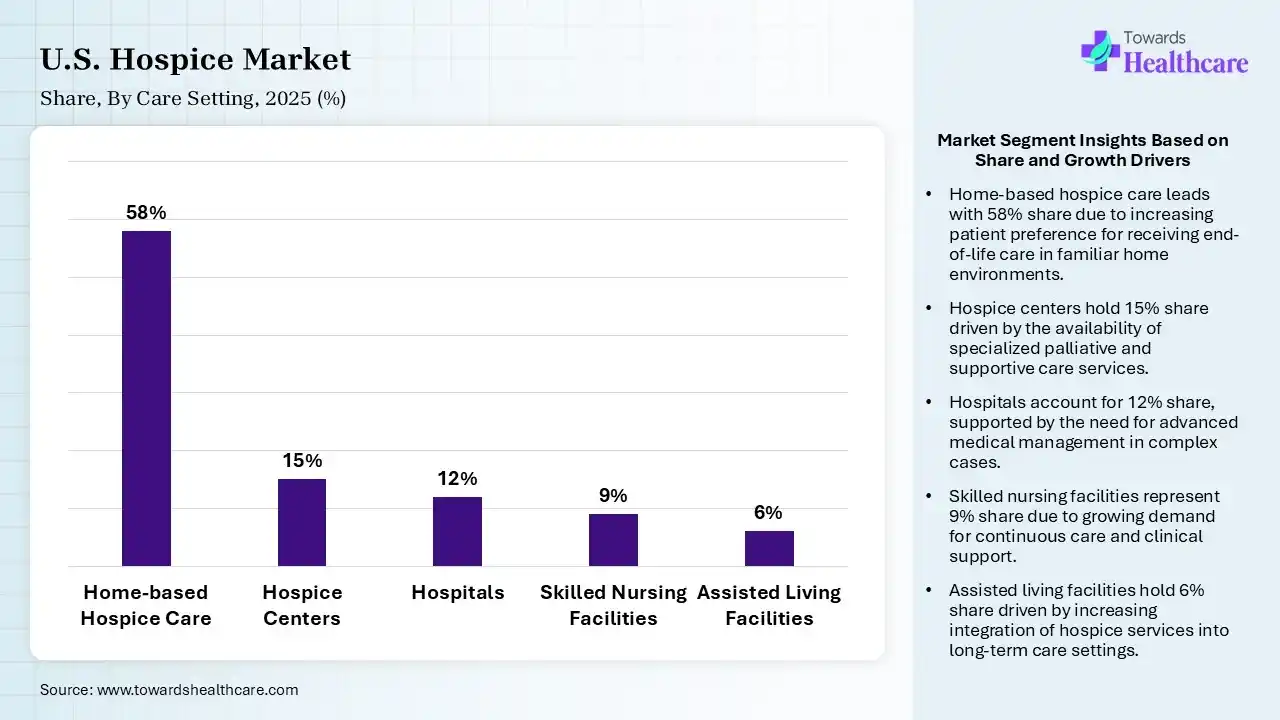

| Segment | Share 2025 (%) |

| Home-based Hospice Care | 58% |

| Hospice Centers | 15% |

| Hospitals | 12% |

| Skilled Nursing Facilities | 9% |

| Assisted Living Facilities | 6% |

The Home-based Hospice Care Segment Led the Market in 2025 with the Largest Share

The home-based hospice care segment led the U.S. hospice market with a share of 58% in 2025 and is expected to grow at the fastest CAGR of 8.40% in the market during the forecast period because it allows patients to receive personalized end-of-life care in a familiar and comfortable environment while remaining close to family members. These settings are often more cost-effective than institutional care and align with patient preferences for aging in place. Expanding home healthcare services and supportive reimbursement policies further strengthen the segment’s market leadership.

The hospice centers segment held the second-largest share of 15% in 2025 because it provides dedicated end-of-life care and specialized symptom management for patients whose needs cannot be fully addressed at home. These facilities offer a structured care environment with multidisciplinary teams, making them a preferred option for managing complex medical conditions and ensuring comprehensive patient comfort.

The hospitals segment held 12% of the U.S. hospice market share due to the increasing number of patients with complex and advanced illnesses requiring specialized medical supervision. Hospitals play a key role in identifying eligible hospice patients and facilitating timely referrals to end-of-life care services. Growing integration of palliative and hospice programs within hospital settings, along with rising demand for coordinated care, is further supporting segment growth.

The skilled nursing facilities segment held a 9% market share due to the increasing elderly population and rising prevalence of chronic and debilitating conditions requiring continuous medical attention. These facilities provide comprehensive nursing care, rehabilitation support, and hospice comprehensive nursing care, rehabilitation support, and hospice services in a structured environment. Growing demand for long-term care solutions, coupled with the need for specialized end-of-life, coupled with the need for specialized end-of-life, is driving the segment’s growth.

")

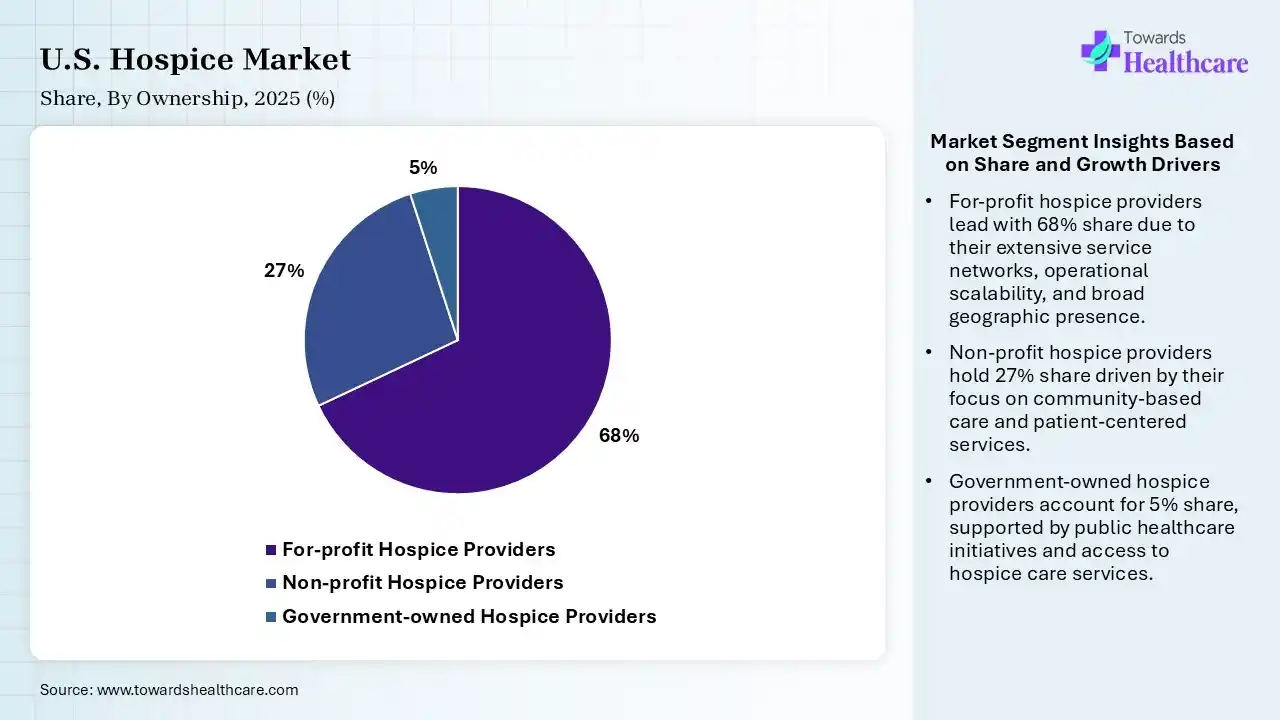

| Segment | Share 2025 (%) |

| For-profit Hospice Providers | 68% |

| Non-profit Hospice Providers | 27% |

| Government-owned Hospice Providers | 5% |

The For-profit Hospice Providers Segment Dominated the U.S. Hospice Market in 2025

The for-profit hospice providers segment held a dominant share of 68% in 2025 and is expected to grow at the fastest CAGR of 8.40% in the market during the forecast period due to its broad geographic presence, strong operational capabilities, and ability to expand services efficiently. These providers benefit from significant investment in home-based care, technology adoption, and patient outreach programs. Their focus on improving accessibility, care coordination, and service availability has enabled them to serve a large patient population and maintain a leading market position.

The non-profit hospice providers segment held the second-largest share of 27% in 2025 due to its long-standing community presence, mission-driven care approach, and focus on patient well-being rather than profitability. These organizations often offer comprehensive support services, including counselling, bereavement care, and caregiver assistance. Strong community trust, charitable funding, and collaborations with healthcare systems continue to support their significant market position.

The government-owned hospice providers segment held a 5% U.S. hospice market share due to increasing public healthcare initiatives aimed at improving access to end-of-life care services, particularly for underserved and vulnerable populations. These providers play a vital role in delivering affordable, high-quality hospice care through publicly funded programs. Rising demand for hospice services, coupled with efforts to strengthen healthcare infrastructure and support aging populations, is contributing to the segment’s growth.

")

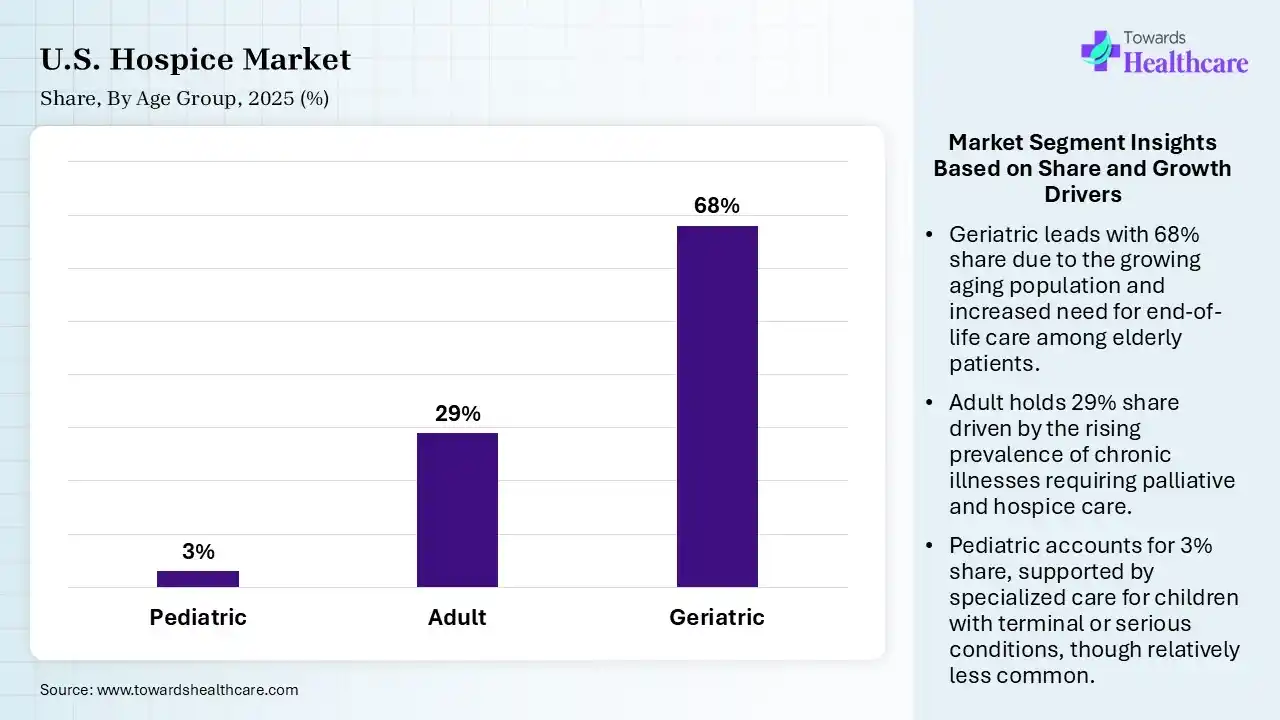

| Segment | Share 2025 (%) |

| Pediatric | 3% |

| Adult | 29% |

| Geriatric | 68% |

The Geriatric Segment Dominated the U.S. Hospice Market in 2025

The geriatric segment dominated the market with a share of 68% in 2025 and is expected to grow at the fastest CAGR of 8.50% in the market during the forecast period due to the large and growing elderly population, which is more susceptible to chronic, progressive, and life-limiting illnesses. Older adults often require comprehensive symptom management, palliative support, and end-of-life care services. Increasing life expectancy, higher rates of age-related diseases, and growing awareness of hospice benefits have significantly contributed to the segment’s leading market position.

The adult segment held the second-largest share of 29% in 2025 due to the significant prevalence of advanced chronic conditions such as cancer, cardiovascular diseases, and neurological disorders among middle-aged and older adults. These patients often require specialized symptom management and supportive care services. Growing awareness of hospice benefits, increasing disease burden, and rising demand for quality end-of-life care have contributed to the segment’s substantial market share.

The pediatric segment held a 3% U.S. hospice market share due to rising awareness of specialized end-of-life and palliative care services for children with life-limiting and complex medical conditions. Increasing emphasis on family-centered care, emotional support, and symptom management is driving demand. Advancements in pediatric healthcare and improved access to hospice programs tailored to children’s unique needs are further contributing to segment growth.

")

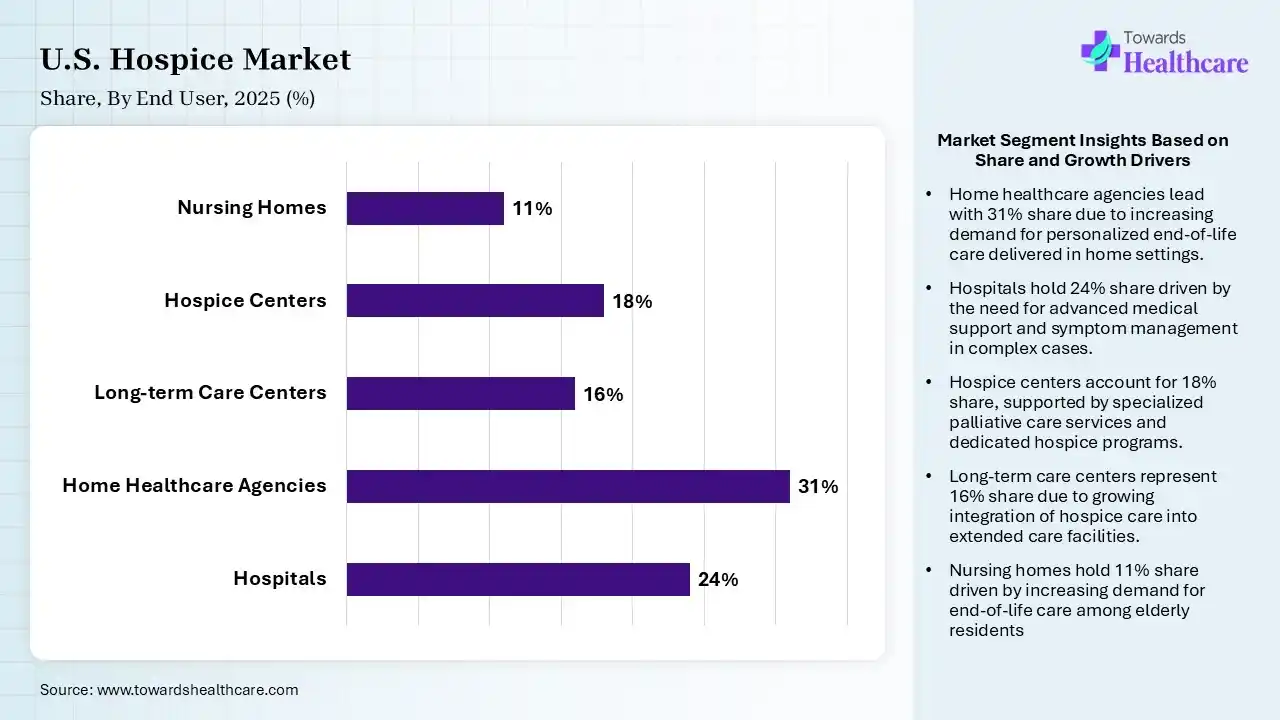

| Segment | Share 2025 (%) |

| Hospitals | 24% |

| Home Healthcare Agencies | 31% |

| Long-term Care Centers | 16% |

| Hospice Centers | 18% |

| Nursing Homes | 11% |

The Home Healthcare Agencies Segment Led the Market in 2025 with the Largest Share

The home healthcare agencies segment led the U.S. hospice market with a share of 31% in 2025 and is expected to grow at the fastest CAGR of 8.60% in the market during the forecast period due to the growing preference for receiving end-of-life care in the comfort of patients' homes. These agencies provide personalized care, symptom management, and caregiver support while reducing the need for hospital stays. Expanding home healthcare infrastructure, cost-effective, favorable reimbursement policies, and increasing demand for patient-centered care have further strengthened the segment’s market leadership.

The hospitals segment held the second-largest share of 24% in 2025 because hospitals serve as key referral centers for patients with advanced terminal illness who require hospice services. Their access to multidisciplinary care teams, specialized medical expertise, and integrated palliative care programs supports timely hospice enrolment. Increasing focus on care transitions, reducing hospital readmissions, and improving end-of-life outcomes further contribute to the segment’s significant market share.

The hospice centers segment held an 18% of the U.S. hospice market share due to increasing demand for dedicated facilities that provide comprehensive end-of-life care, symptoms managements, and round-the-clock clinical support. These centers offer a comfortable and specialized environment for patients whose needs cannot be adequately met at home. Rising awareness of hospice services, growing chronic disease prevalence, and an aging population are further driving segment growth.

The long-term care centers segment held a 16% market share due to the growing aging population and increasing prevalence of chronic, disabling, and life-limiting conditions. These facilities provide continuous medical supervision, nursing care, and hospice support for residents requiring long-term assistance. Rising demand for integrated care services, coupled with the need for specialized end-of-life care in residential settings, is driving the segment’s growth.

")

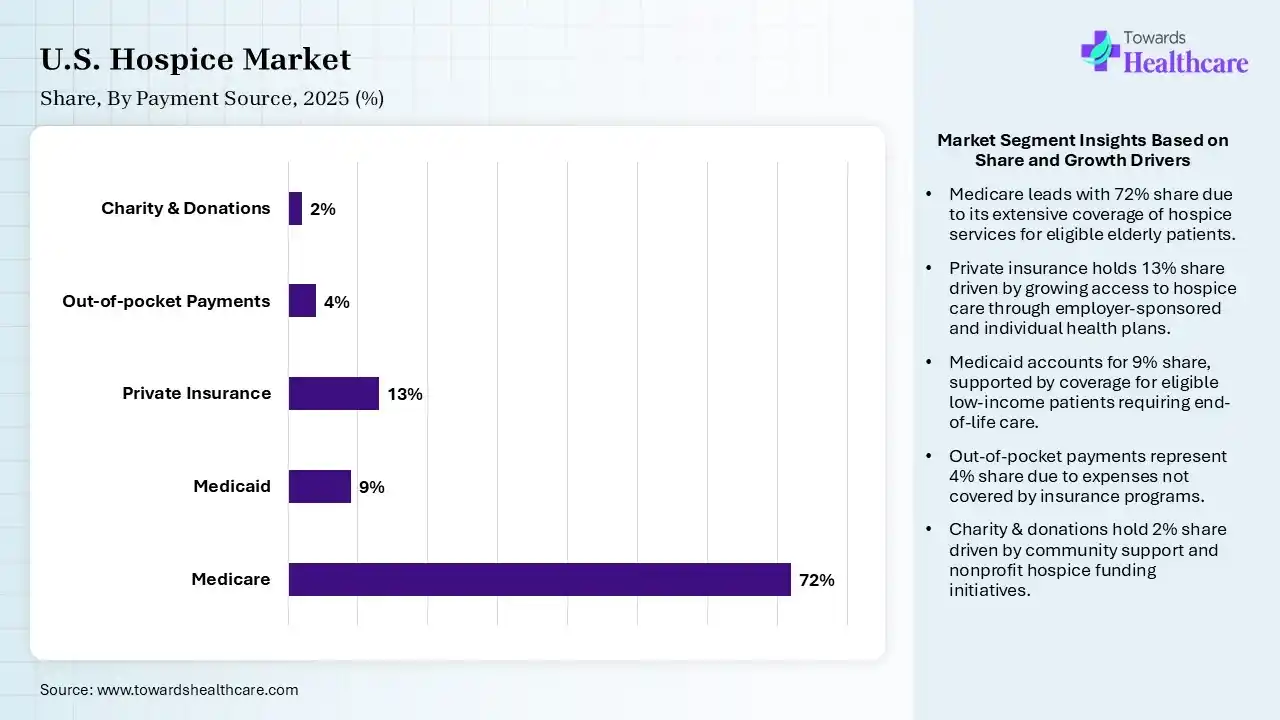

| Segment | Share 2025 (%) |

| Medicare | 72% |

| Medicaid | 9% |

| Private Insurance | 13% |

| Out-of-pocket Payments | 4% |

| Charity & Donations | 2% |

The Medicare Segment Led the U.S. Hospice Market in 2025 with the Largest Share

The Medicare segment dominated the market with a share of 72% in 2025 because it provides comprehensive coverage for hospice services, making end-of-life care more accessible and affordable for eligible patients. As the primary healthcare payer for the elderly population, Medicare supports a large share of hospice admissions. The growing number of aging Americans, favorable reimbursement policies and extensive hospice benefits coverage continue to reinforce Medicare’s leading role in the market.

The private insurance segment held the second-largest share of 13% in 2025 and is expected to grow at the fastest CAGR of 8.20% in the market during the forecast period due to widespread employer-sponsored and individual health insurance plans that cover hospice and palliative care services. Growing enrollment in private health plans, increasing awareness of end-of-life care benefits, and expanding coverage for home-based hospice services have supported utilization. Additionally, faster access to specialized care and flexible service options continues to drive segment growth.

The Medicaid segment held 9% of the U.S. hospice market share due to increasing healthcare coverage for low-income individuals, disabled populations, and eligible elderly patients. Growing enrollments in Medicaid programs and expanding state-level support for hospice services are improving access to end-of-life care. Rising demand for affordable healthcare solutions, coupled with efforts to reduce healthcare disparities, is further driving the growth of this segment.

The out-of-pocket payments segment held a 4% market share due to patients and families seeking additional services not fully covered by insurance or government programs. These may include enhanced caregiver support, specialized therapies, and customized end-of-life care options. Rising awareness of hospice benefits, growing preference for personalized care, and increasing willingness to invest in quality-of-life services are contributing to segment growth.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| Chemed Corporation (VITAS Healthcare) | Cincinnati | Hospice care, palliative care, home hospice services, inpatient hospice care, and bereavement support. |

| Amedisys | Baton Rouge | Hospice care, home health care, palliative care, personal care services, and chronic disease management. |

| Gentiva | Atlanta | Hospice care, palliative care, personal care services, grief counseling, and advanced illness management. |

| Brookdale Senior Living, Inc. | Brentwood | Hospice services, assisted living, memory care, skilled nursing, and senior care solutions. |

| Seasons Hospice & Palliative Care | Rosemont | Hospice care, palliative care, bereavement services, spiritual care, and caregiver support. |

Strengths

Weaknesses

Opportunities

Threats

By Service Type

By Diagnosis

By Care Setting

By Ownership

By Age Group

By End User

By Payment Source

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar