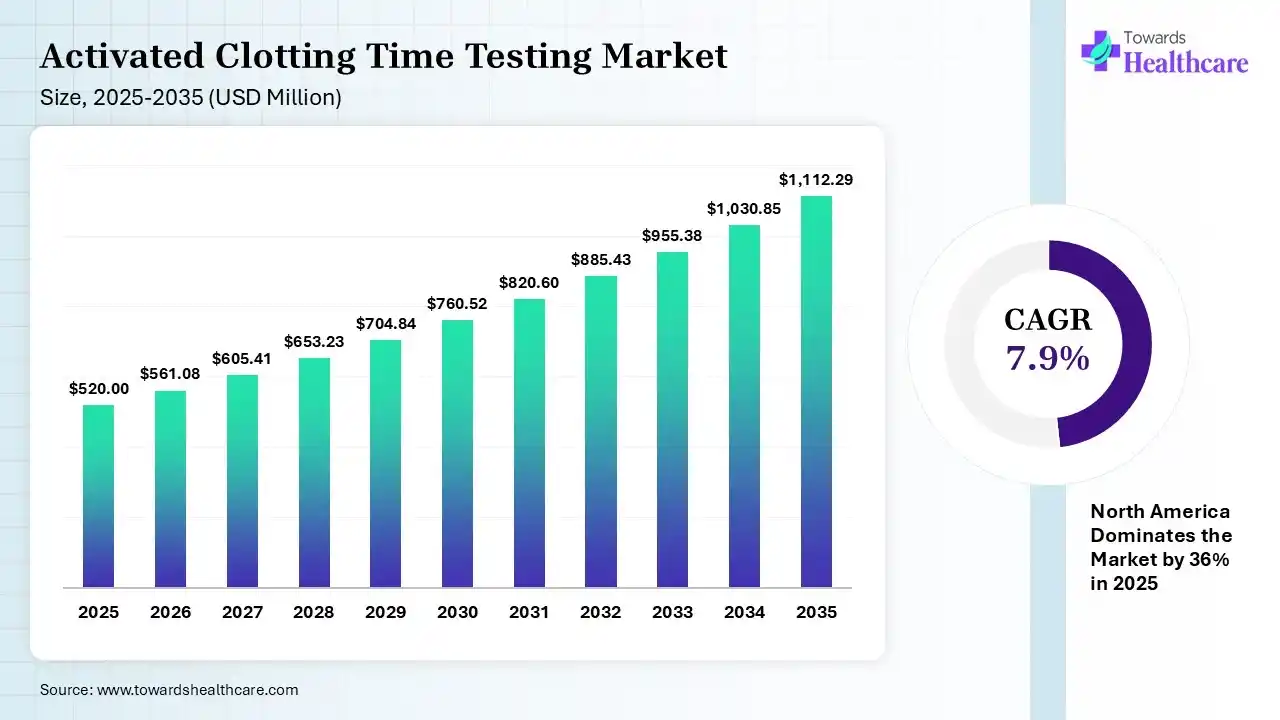

The global activated clotting time testing market size was estimated at USD 520 million in 2025 and is predicted to increase from USD 561.08 million in 2026 to approximately USD 1112.29 million by 2035, expanding at a CAGR of 7.9% from 2026 to 2035. The growing chronic disease burden globally is increasing the use of activated clotting time (ACT) testing solutions. Growing demand for point-of-care diagnostics, expanding healthcare, growing government initiatives, technological advancements, and the launch of new products are also enhancing the market growth.

The activated clotting time testing market is driven by growing incidences of cardiovascular diseases and increasing volume of complex surgical procedures. The activated clotting time testing refers to the diagnostic test developed for the measurement of blood clotting time. These tests are used for monitoring anticoagulation during various surgical procedures, detecting coagulation abnormalities, guiding heparin dosing, and preventing any complications.

Activated clotting time (ACT) testing is a point-of-care diagnostic method used to measure the time required for blood to clot, primarily to monitor high-dose anticoagulants therapy during procedures such as cardiac surgery, extracorporeal membrane oxygenation (ECMO), and interventional cardiology. The activated clotting time testing market is expanding due to the increasing number time testing market is expanding due to the increasing number of cardiovascular surgeries, growing use of anticoagulants, and rising demand for rapid bedside coagulation assessment.

Technological advancements in portable analyzers, automated testing system, and digital connectivity are improving testing accuracy and workflow efficiency. The integration of data management software and hospital information systems is enhancing clinical decision-making. Future opportunities lie in expanding point-of-care diagnostics, increasing adoption in ambulatory surgical centers, and developing next-generation devices with faster turnaround times, improved precision, and seamless connectivity for personalized patient management.

AI offers a wide range of applications in the activated clotting time testing market, such as real-time data analysis, providing rapid interpretations. They also help in autocalibration and adjustments of various parameters to enhance the test accuracy, where they also promote easy integration with healthcare systems for long-term tracking of cardiovascular status. They are also used for anticoagulant therapy adjustments and personalized heparin dosing, with reduced errors and complications.

Growing Surgical and Dialysis Procedures

The growing cardiovascular and kidney diseases are increasing the demand for activated clotting time testing during their surgical procedures, angioplasty, and hemodialysis for real-time heparin and coagulation monitoring.

Expanding Point-of-Care Testing

A rise in bedside or rapid diagnostics is driving the adoption of activated clotting time testing solutions due to their accuracy and user-friendly approaches, as well as encouraging the development of portable and automated devices.

Blooming Technological Innovations

The growing technological advancements are propelling the development of new activated clotting time testing solutions with enhanced accuracy and clinical decisions, with reduced human errors by integrating digital health tools.

| Table | Scope |

| Market Size in 2026 | USD 561.08 Million |

| Projected Market Size in 2035 | USD 1112.29 Million |

| CAGR (2026 - 2035) | 7.9% |

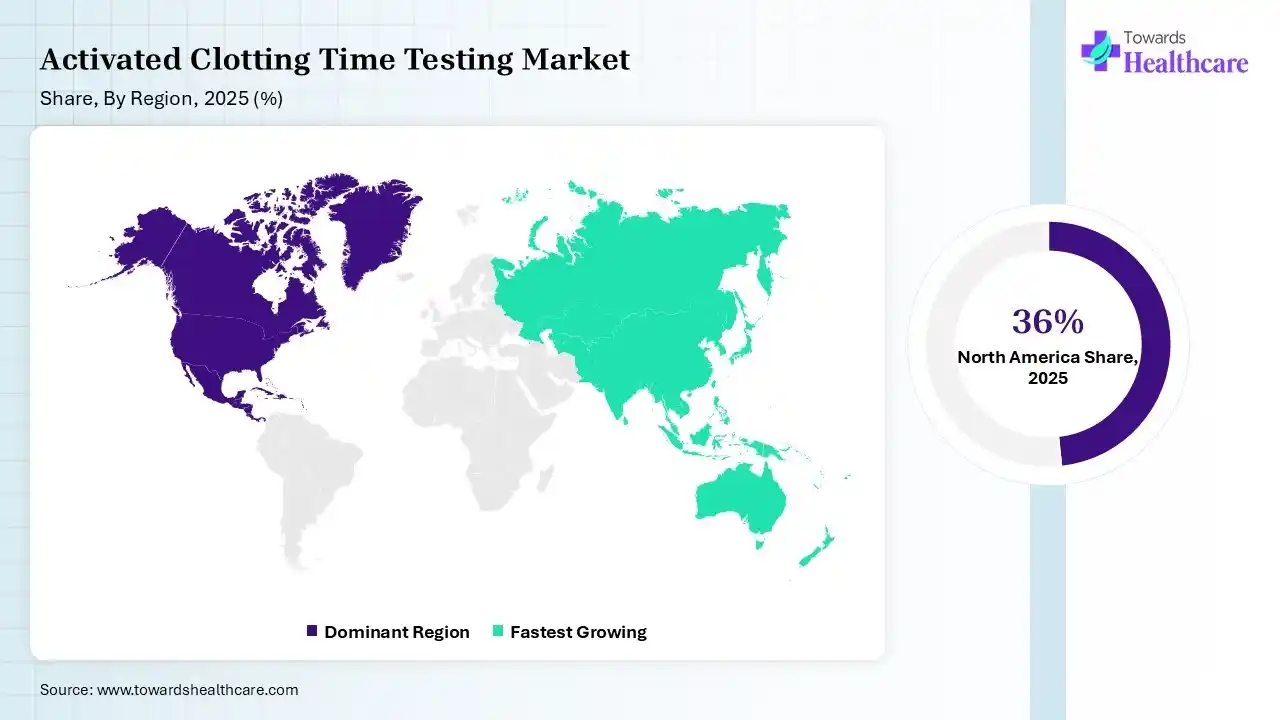

| Leading Region | North America by 36% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Test Type, By Application, By End-Use, By Region |

| Top Key Players | Abbott Laboratories, Werfen, Medtronic plc, Helena Laboratories, Roche Diagnostics, Sysmex Corporation, Haemonetics Corporation, Diagnostica Stago SA, Accriva Diagnostics, Siemens Healthineers AG |

| Segment | Share 2025 (%) |

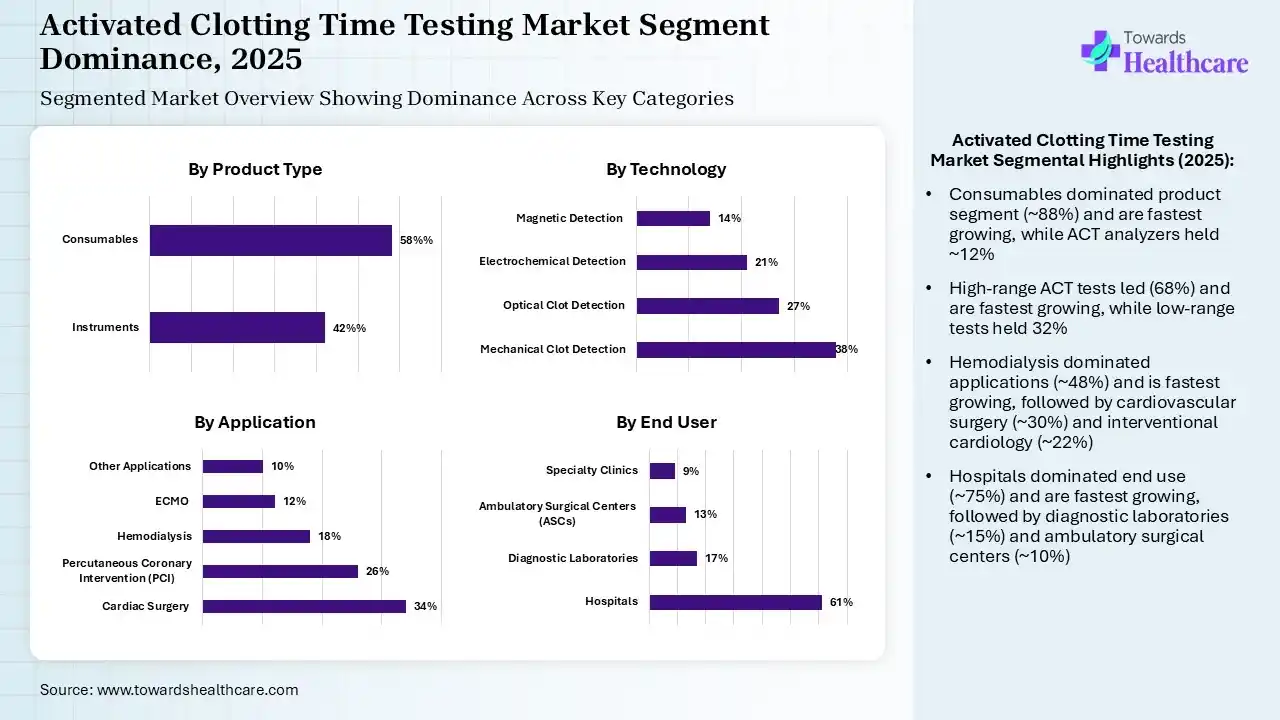

| Instruments | 42% |

| Consumables (Dominating, Fastest Growing) | 58% |

The Consumables Segment Dominated the Market With an Approximate 88% in 2025

The consumables segment led the activated clotting time testing market with an approximate 88% share in 2025 and is expected to grow at the fastest CAGR during the predicted time, due to their single-time use, which increased their continuous demand across the healthcare sector. Each ACT test requires new reagents, activators, or cartridges, which increases their use. Additionally, growth in the testing volumes also increased their adoption rates.

The ACT analyzers segment held the second-largest share of approximate 12% of the market in 2025, driven by their high adoption for point-of-care testing. Their easy use and minimal errors are also increasing their demand. Additionally, the growing number of surgical procedures and personalized medicine demands are also increasing their use for real-time anticoagulation monitoring and precise heparin dosing.

| Segment | Share 2025 (%) |

| Mechanical Clot Detection | 38% |

| Optical Clot Detection | 27% |

| Electrochemical Detection | 21% |

| Magnetic Detection | 14% |

The High-Range ACT Tests Segment Dominated the Market With an Approximate 68% in 2025

The high-range ACT tests segment accounted for the highest revenue share of approximate 68% of the activated clotting time testing market in 2025 and is expected to show the highest CAGR growth during the predicted time, due to growth in the cardiac surgeons. They were used for high-dose heparin therapy and real-time coagulation monitoring. Moreover, their widespread availability also increased their adoption rates.

The low-range ACT tests segment held the second-largest share of approximate 32% of the market in 2025, due to a growing shift towards minimally invasive procedures. The growing adoption of precision medicines and increasing disease screening programs are also increasing their use. At the same time, technological advancements are also driving their innovations.

| Segment | Share 2025 (%) |

| Cardiac Surgery | 34% |

| Percutaneous Coronary Intervention (PCI) | 26% |

| Hemodialysis | 18% |

| ECMO | 12% |

| Other Applications | 10% |

The Hemodialysis Segment Dominated the Market with an Approximate 48% in 2025

The hemodialysis segment held a major revenue share of approximate 48% of the activated clotting time testing market in 2025 and is expected to expand rapidly with the fastest CAGR during the upcoming years, due to frequent anticoagulation requirements. Growth in patient volume and demand for point-of-care testing also increased their use. Their real-time and safe anticoagulation monitoring also increased their acceptance rates.

The cardiovascular surgery segment held the second-largest share of approximate 30% of the market in 2025, due to growing demand for high-dose heparin. The growing focus on patient safety and point-of-care testing solutions is also increasing the use of activated clotting time tests. Their rapid and accurate results and real-time monitoring are also increasing their adoption rates to tackle the growing surgical volume.

The interventional cardiology segment held approximate 22% of the activated clotting time testing market share in 2025, due to a growing shift toward minimally invasive procedures. This, in turn, is increasing the demand for activated clotting time testing solutions for procedures like angioplasty. The growing cardiovascular diseases and outpatient care options are also increasing their use, offering bedside monitoring, careful anticoagulation, and safe and precise heparin dosing.

| Segment | Share 2025 (%) |

| Hospitals | 61% |

| Diagnostic Laboratories | 17% |

| Ambulatory Surgical Centers (ASCs) | 13% |

| Specialty Clinics | 9% |

The Hospitals Segment Dominated the Market with an Approximate 75% in 2025

The hospitals segment contributed the biggest revenue share of approximate 75% of the activated clotting time testing market in 2025 and is expected to gain the highest CAGR share during the upcoming years, due to the presence of high patient volume, which increased the demand for anticoagulation monitoring. At the same time, growth in the surgical procedures also increased the use of activated clotting time tests. The presence of trained personnel, the availability of point-of-care devices, and regulatory compliance also increased their acceptance rates.

The diagnostic laboratories segment held the second-largest share of approximate 15% of the market in 2025, due to growing demand for outpatient testing, which is increasing the use of activated clotting time tests for preoperative and routine anticoagulant testing. Expanding laboratories and growing health awareness are also increasing their use for early disease detection. The growing cardiovascular and kidney diseases are also increasing their use, where their affordable solution are also attracting the patients.

The ambulatory surgical centers segment held approximate 10% of the activated clotting time testing market share in 2025, due to expanding outpatient procedures, where the growing minimally invasive surgeries are also increasing the demand for activated clotting time testing solutions. Growing demand for rapid anticoagulation monitoring and point-of-care testing is also increasing their use. Additionally, their cost-effective alternative and same-day surgeries are also increasing their acceptance rates.

")

North America dominated the activated clotting time testing market with approximate 39% in 2025, due to the presence of advanced healthcare infrastructure, which increased the adoption of activated clotting time testing solutions. The presence of strong companies and a high cardiovascular disease burden also increased their use. The growth in surgical procedures and high healthcare spending also increased their use, which contributed to the market growth.

U.S. Market Trends

The growing incidence of cardiovascular disease and the surgical procedures in the U.S. are driving the demand for activated clotting time testing solutions. The presence of advanced healthcare, medical device companies, and a robust R&D ecosystem is also increasing their use and innovations. Technological advancements and high healthcare spending are also driving their innovations.

Canada Strengthens Growth in Activated Clotting Time Testing

Canada is witnessing significant growth in the activated clotting time testing market due to the increasing prevalence of cardiovascular diseases, rising volume of cardiac and vascular surgeries, and widespread adoption of point-of-care diagnostics. String healthcare infrastructure, growing investments in advanced coagulation monitoring technologies, and the integration of automated testing systems are improving clinical efficiency. Ongoing research initiatives and supportive healthcare funding are further accelerating market expansion.

Asia Pacific held approximately 22% share of the activated clotting time testing market in 2025 and is expected to grow at the fastest CAGR during the forecast period, due to rapid healthcare expansion and high patient population. Growing cardiovascular and kidney diseases are increasing the use of activated clotting time testing during their surgical procedures. Expanding point-of-care testing and government initiatives are also driving the market growth.

Japan Market Trends

The presence of advanced healthcare systems in Japan is increasing the use of activated clotting time testing to deal with the rising cardiovascular disease burden. The growing geriatric population and surgical volumes are also increasing their use. High healthcare expenditure, expanding medical device companies, and technological advancements are driving their innovations.

India Accelerates Growth in Activated Clotting Time Testing

India is significantly in the activated clotting time testing market due to the rising burden of cardiovascular diseases, increasing number of cardiac surgeries, and growing adoption of point-of-care diagnostics. Expanding healthcare infrastructure, greater availability of advanced coagulation analyzers, and increasing investment in critical care and interventional cardiology are driving demand. Government initiatives to improve healthcare access and rising hospital modernization are further supporting market growth.

Europe held approximately 26% share of the market in 2025 and is expected to grow significantly in the activated clotting time testing market during the forecast period, due to the growing cardiovascular burden and high geriatric population. This is increasing the adoption of activated clotting time testing across healthcare systems for surgical procedures. Growing technological advancements and expanding medical device companies are also increasing their innovations and use, promoting the market growth.

UK Market Trends

The UK consists of robust healthcare systems and medical device companies, which are driving the adoption and advancements of the activated clotting time testing solutions. The growing demand for anticoagulant monitoring and point-of-care testing is also increasing their adoption rates. Growing focus on patient safety and quality care is also increasing their use.

R&D

Clinical Trials and Regulatory Approvals

Formulation and Final Dosage Preparation

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Companies | Headquarters | Activated Clotting Time Testing Solutions |

| Abbott Laboratories | Abbott Park, U.S. | i-STAT System |

| Werfen | Barcelona, Spain | Hemochron Signature Elite System |

| Medtronic plc | Dublin, Ireland | ACT Plus Automated Coagulation Timer System |

| Helena Laboratories | Beaumont, U.S. | Point-of-Care (POC) hemostasis products |

| Roche Diagnostics | Rotkreuz, Switzerland | Integrated coagulation testing platforms |

| Sysmex Corporation | Kobe, Japan | Comprehensive automated coagulation analyzers |

| Haemonetics Corporation | Boston, U.S. | Blood management technologies and surgical blood salvage |

| Diagnostica Stago SA | Asnieres-sur-Seine, France | Wide portfolio of hemostasis analyzer and reagents for thrombosis and hemostasis diagnostic |

| Accriva Diagnostics | San Diego, U.S. | VerifyNow and Hemochron brands |

| Siemens Healthineers AG | Erlangen, Germany | Automated coagulation systems |

In July 2026, “For the first time, we've demonstrated that Spark's core technology, transcutaneous auricular neurostimulation (tAN®), can engage neural pathways to enhance platelet function in humans," said Navid Khodaparast, PhD, chief science officer and co-founder at Spark Biomedical.

Strengths

Weaknesses

Opportunities

Threats

By Product

By Test Type

By Application

By End-Use

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar