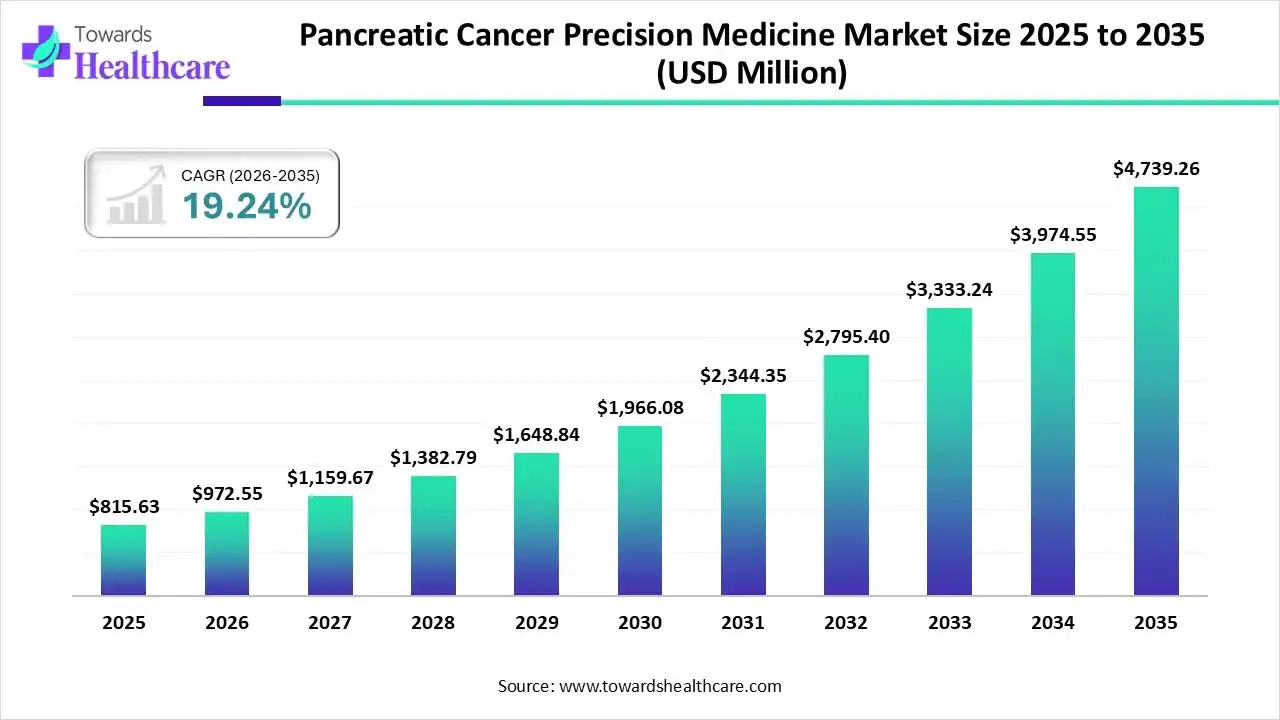

The global pancreatic cancer precision medicine market size was estimated at USD 815.63 million in 2025 and is predicted to increase from USD 972.55 million in 2026 to approximately USD 4739.26 million by 2035, expanding at a CAGR of 19.24% from 2026 to 2035.

")

The pancreatic cancer precision medicine market is growing, as an advanced precision strategy at the level of the individual patient supports repurposing drugs in pancreatic cancer and recognizes more exceptional patients.

The pancreatic cancer precision medicine market is growing because precision medicine majorly focuses on recognizing clinically related molecular subtypes of pancreatic cancers, it involving the discovery of actionable targets, which are exclusive molecular traits in tumours that are targeted with novel therapies. Targeted genome medication in pancreatic cancer via multi-centre creativities merging unparalleled expertise in clinical trial leadership and results data analysis, state-of-the-art tumour genomic profiling, bioinformatics, and scientific analysis. Advancement of more efficient treatments requires a better understanding of the genetic variety of cancers and biological molecules found in bodily fluids. Precision medicine identifies patients early in the course of their pancreatic disease and prevents progression to long-term or severe illness.

Integration of AI-driven technology in pancreatic cancer precision medicine drives market growth, as AI-driven medical devices in precision medicine to identify pancreatic cancer needs to complete and precise training, testing datasets, and validation. AI-based healthcare tools in precision medicine have both positively and negatively affected the pillars of availability, accessibility, and acceptability. This doctoral project specifically scrutinises the quality pillar of the right to health. AI-based medical devices in precision medicine, thereby enhancing the health of individuals in the demographics of the population.

| Table | Scope |

| Market Size in 2026 | USD 972.55 Million |

| Projected Market Size in 2035 | USD 4739.26 Million |

| CAGR (2026 - 2035) | 19.24% |

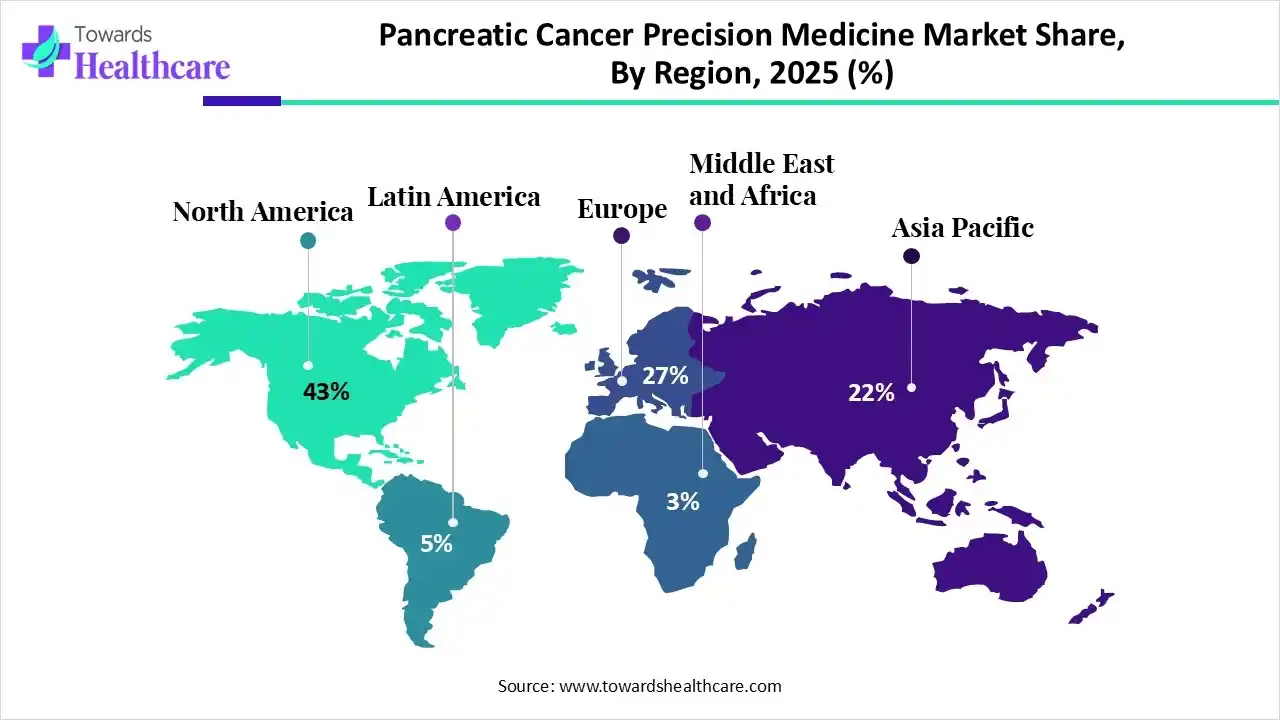

| Leading Region | North America by 43% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapeutic Approach, By Diagnostic Technology, By End-User, By Region |

| Top Key Players | AstraZeneca plc, Pfizer Inc., F. Hoffmann-La Roche Ltd., Novartis AG, Merck & Co., Inc., Amgen Inc. |

Which Therapeutic Approach Led the Pancreatic Cancer Precision Medicine Market in 2025?

In 2025, the targeted therapy segment held the dominant market share with approximately 57% share in 2025, due to targeted therapy supporting the targeting of the mutated proteins responsible for managing growth, division, and metastasis of tumors in the pancreatic cancer cells. It is significant to consider all the attributes of the patient to offer suitable targeted treatment to avoid any serious adverse effects. These therapies are drugs or ingredients that target particular features of cancer cells, which differ between cancer types.

Chemotherapy-Precision Combinations

Whereas the chemotherapy-precision combinations segment is the fastest-growing in the market, merging immunotherapy with epigenetic medicines improves immune activity in resistant pancreatic tumors. A combination treatment has boosted the one-year pancreatic cancer survival rate by more than 60 %. Combining chemotherapy with precision medicine in pancreatic cancer has improved treatment effectiveness by directing specific molecular pathways.

Why did the Genomic Testing Segment Dominate the Market in 2025?

The genomic testing segment is dominant in the pancreatic cancer precision medicine market, with approximately 41% share in 2025, as this testing has altered cancer care from a one-size-fits-all model to precision medicine in cancer care that authorizes decisions based on the cancer’s molecular blueprint. Genomic testing plays a significant role in targeted oncology by examining a patient's tumor DNA to identify unique hereditary mutations. This testing allows clinicians to craft treatment plans that exactly target those mutations, improving the effectiveness and lowering the adverse effects of therapies.

Liquid Biopsy

Whereas the liquid biopsy segment is the fastest-growing in the market, as liquid biopsy holds great potential for the diagnosis, treatment, and monitoring of patients with cancer. Liquid biopsy has many advantages in the diagnosis and treatment of various types of cancer, including being non-invasive and quick. It offers major advantages over tissue biopsy, including lower risk, repeatability, and the ability to capture tumor heterogeneity and temporal evolution.

Why did the Hospitals & Cancer Centers Segment Dominate the Market in 2025?

The hospitals & cancer centers segment is dominant in the pancreatic cancer precision medicine market with approximately 52% share in 2025, as hospitals and cancer centers provides with more detailed treatment processes, cancer patients could have an advanced quality of life and live longer. These development plays significant role in targeted medicine in enhancing pancreatic cancer treatment. Centers use progressive diagnostics (NGS) to cancer tumour DNA, enablling physician to select treatments that match the cancer’s hereditary profile.

Diagnostic Laboratories

Whereas the diagnostic laboratories segment is the fastest-growing in the market, as lab test-based diagnostics offer significant insights into the body's health, helping early diagnosis, specific treatment, and continuing disease monitoring. Diagnostic labs contribute to preventive healthcare by allowing early disease discovery and timely intervention. From early detection of health challenges to precise diagnoses, inclusive testing, and useful discussions with medical care professionals.

")

In 2025, North America dominated the pancreatic cancer precision medicine market with approximately 43% share, as the adoption of early identification of pancreatic cancer via screening improves survival and reduces mortality through finding cancer at an early stage in this region. Investing in affordable screening saves lives and lowers financial burdens. Imaging technologies play a significant role in the diagnosis of irregularities and therapy, which contributes to the growth of the market.

U.S. Market Trends

In the U.S., demand is increasing significantly due to the essential role of advanced scans in diagnosis and new therapies, and the increasing requirement for imaging-driven care with an older population. more precise diagnoses, specific treatments guided through imaging, and more reachable care via portable and outpatient solutions.

Asia Pacific is expected to see rapid growth in the pancreatic cancer precision medicine market, driven by a growing aging population and low fertility rates, as 36 percent of the global population is over 65 years old. Increasing spending effectiveness was higher when switching governmental investment predisposition in the aspect of medical care infrastructure construction toward developed regions, which drives the growth of the market.

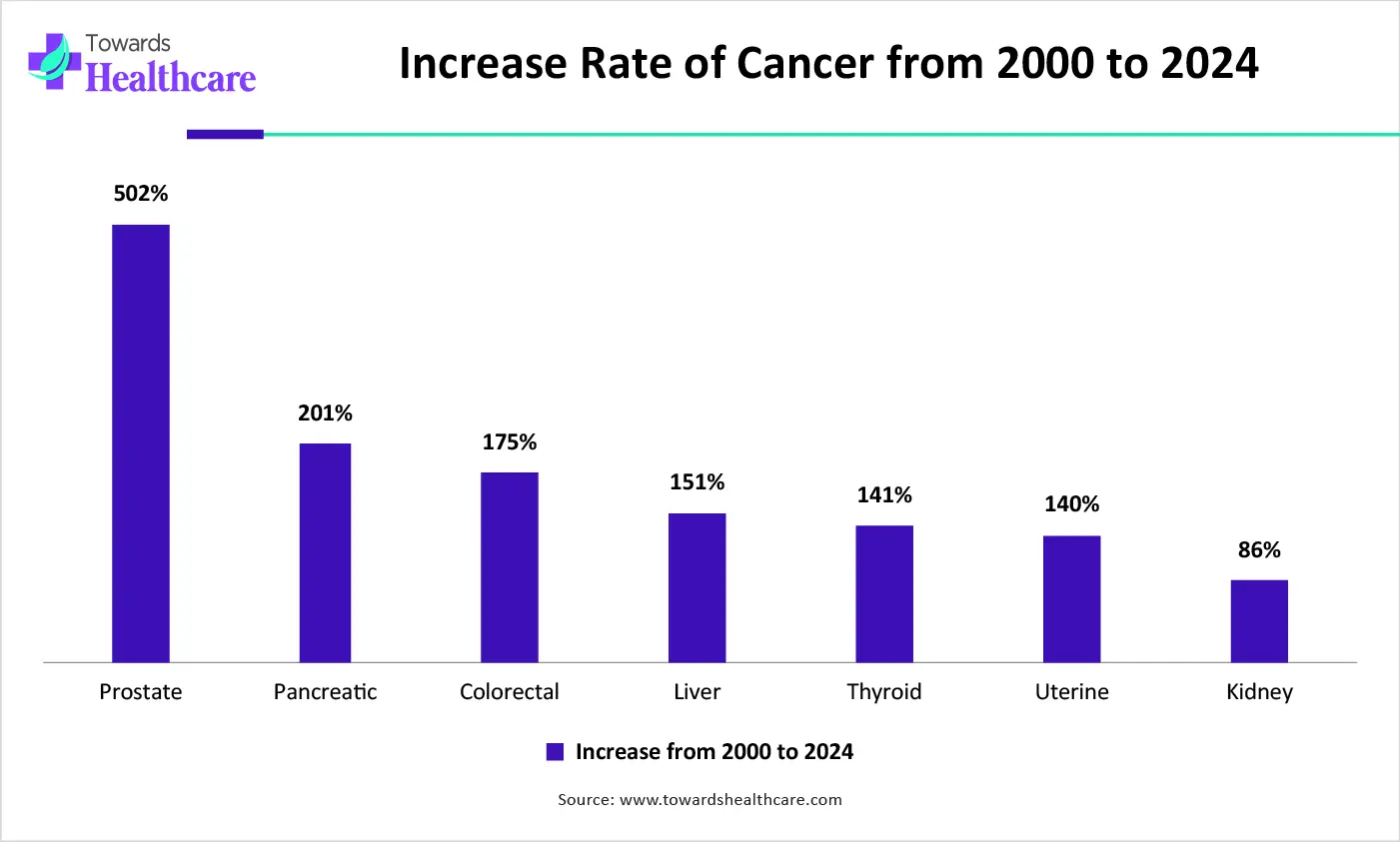

| Types of Cancer | Increase from 2000 to 2024 |

| Prostate | 502% |

| Pancreatic | 201% |

| Colorectal | 175% |

| Liver | 151% |

| Thyroid | 141% |

| Uterine | 140% |

| Kidney | 86% |

India Market Trends

India's pancreatic cancer has been on a steady increase over the last 5-10 years, which is attributed to dietary shifts related to Western lifestyles, like increased consumption of processed foods, high-fat diets, and sugary drinks. Cancer hospitals in India use automation and artificial intelligence technology to advance treatment outcomes via their positions.

Europe is significantly growing in the pancreatic cancer precision medicine market, as increasing advancements in precision medicine and integration in treatments are improving survival rates and expanding the therapeutic. Europe travels to explore the broader impacts of disease on society to progress a greater understanding of the true scale and nature of the disease problem. A technical platform for mixing and strengthening the capacity for disease assessment in Europe.

| Company | Headquarters | Latest Update |

| AstraZeneca plc | United Kingdom | AstraZeneca Plc expects profit to increase further this year, driven by sales of its cancer drugs, as it works to offset the patent expiry of a blockbuster diabetes medicine. |

| Pfizer Inc. | United States | Pfizer Inc. presents data in its portfolio of potential advanced cancer medicines at the 2025 American Society of Clinical Oncology. |

| F. Hoffmann-La Roche Ltd. | Switzerland | Recent cancer developments are transforming the strength to identify and treat cancer, enabling more effective care. |

| Novartis AG | Switzerland | Novartis is reimagining cancer care with RLT for patients with advanced cancers. By harnessing the power of targeted radiation and applying it to advanced cancers, RLT is designed to deliver treatment straight to target cells anywhere in the body. |

| Merck & Co., Inc. | United States | Merck announced the presentation of novel oncology data in more than 12 tumor types at ASCO 2025. |

| Amgen Inc. | United States | Amgen is advancing a pan-KRAS inhibitor, AMG 410, designed to target multiple mutations (both G12C and G12D), as well as wild-type forms of the KRAS protein. |

By Therapeutic Approach

By Diagnostic Technology

By End-User

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar