")

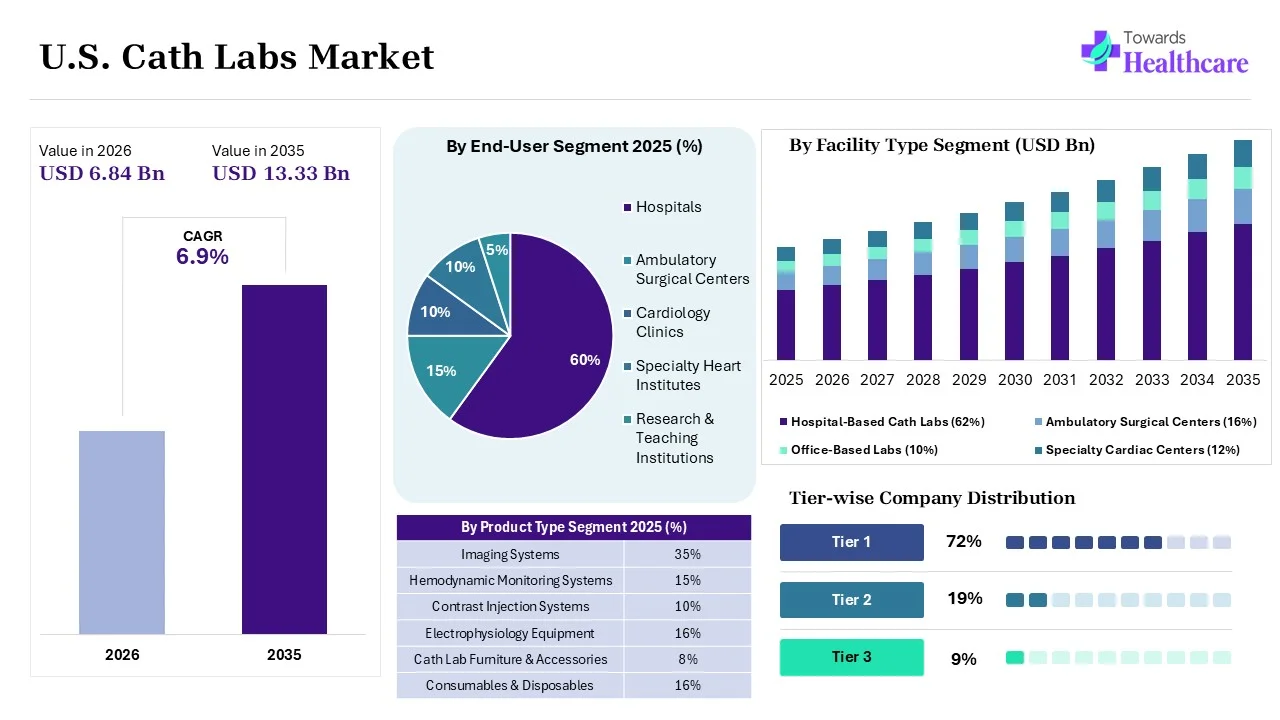

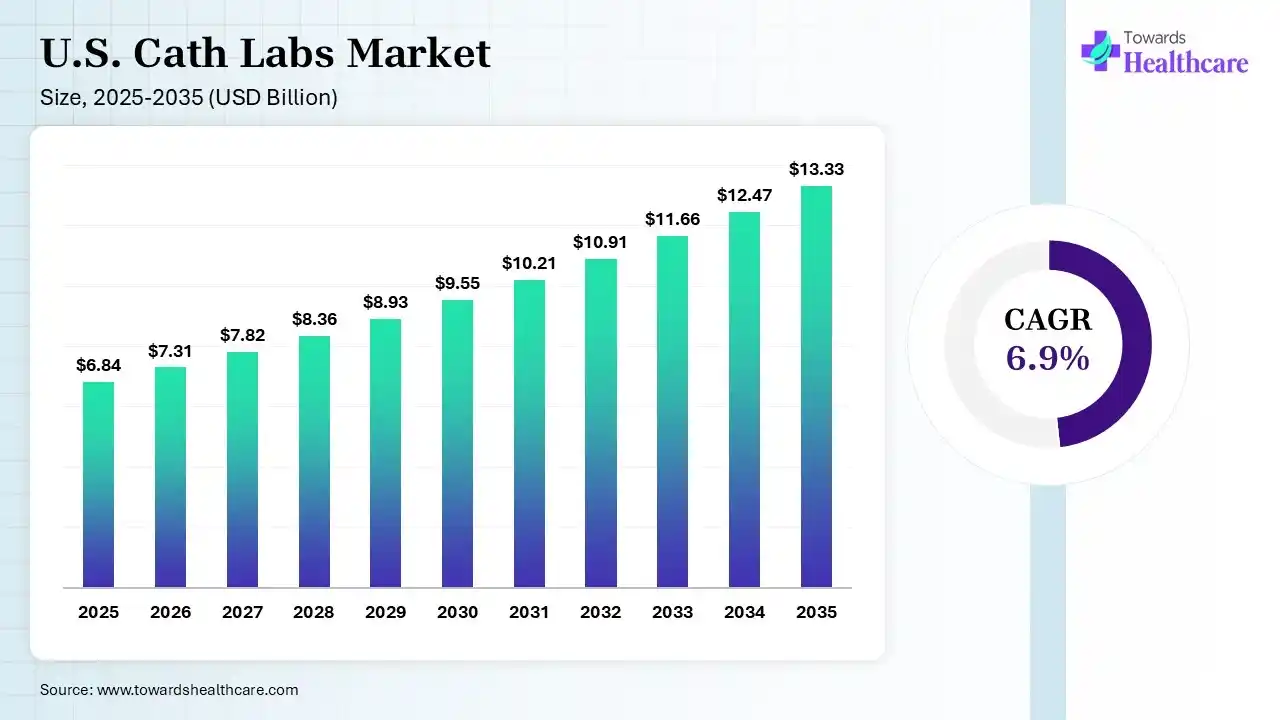

The U.S. cath labs market size was estimated at USD 6.84 billion in 2025 and is predicted to increase from USD 7.31 billion in 2026 to approximately USD 13.33 billion by 2035, expanding at a CAGR of 6.9% from 2026 to 2035. The increasing cardiovascular disease burden in the U.S. is increasing the dependence on the cath labs. Growing outpatient services, health awareness, AI innovations, and new product launches are also enhancing the market growth.

")

The U.S. cath labs market is driven by a growing geriatric population and a shift towards minimally invasive procedures. The U.S. cath labs, also known as catheterization laboratories, refer to the hospital or clinical rooms offering diagnosis and treatment of heart conditions with the use of flexible and thin catheters across the U.S. They offer coronary angiography, angioplasty, stent placement, promoting the treatment of heart valve disorders, heart attacks, etc., as well as provide implantation of various cardiac devices.

AI offers a wide range of applications in the U.S. cath labs, driving real-time image analysis and enhancing decision-making. It also helps in assessing disease progression, enhanced procedural planning, and optimized implant placements. AI also helps in offering 3D imaging, predicting patient outcomes, navigating complex catheter-based procedures, and reducing operator variability.

Minimally Invasive Procedures on the Rise

Increasing health awareness across the U.S. is driving the demand for minimally invasive approaches. This, in turn, is increasing the use of cath labs offering minimally invasive diagnostics, catheter-based treatment with shorter recovery times, and lower complications.

Expanding Structural Heart Interventions

The growing cardiovascular disease burden in the U.S. is promoting advancements in structural heart interventions. This is in turn, is promoting the use of transcatheter aortic valve replacement, left atrial appendage closure, transcatheter mitral valve repair and replacement, and patent foramen ovale closure procedures.

Blooming Imaging Technologies

The growing investments in the cath labs are promoting the development of advanced imaging technologies. This is driving the development of 3D imaging systems, fusion imaging, intravascular ultrasound, and optical coherence tomography systems.

| Table | Scope |

| Market Size in 2026 | USD 6.84 Billion |

| Projected Market Size in 2035 | USD 13.33 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Procedure Type, By Application, By End User, By Technology, By Facility Type, By Ownership Model |

| Top Key Players | GE HealthCare, Abbott Laboratories, Koninklijke Philips N.V., Edwards Lifesciences Corporation, Siemens Healthineers AG, Merit Medical Systems, Inc., Medtronic plc, Cordis, , Terumo Medical Corporation |

")

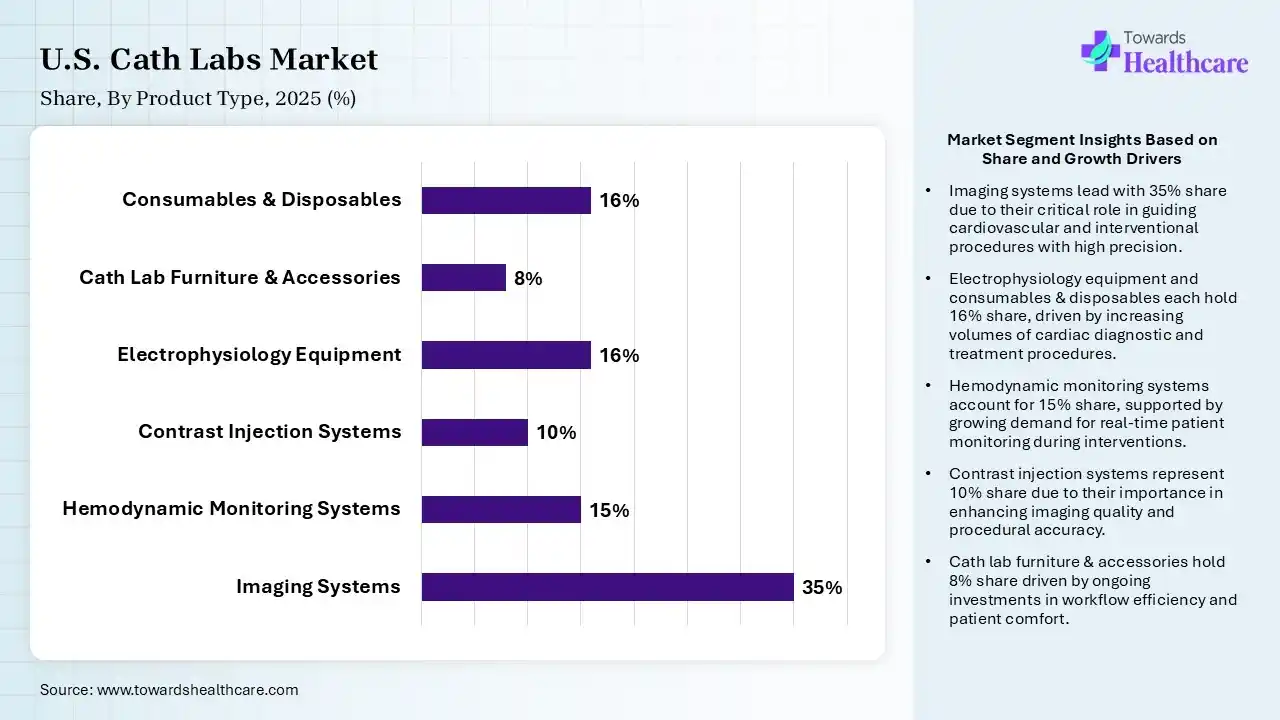

| Segment | Share 2025 (%) |

| Imaging Systems | 35% |

| Hemodynamic Monitoring Systems | 15% |

| Contrast Injection Systems | 10% |

| Electrophysiology Equipment | 16% |

| Cath Lab Furniture & Accessories | 8% |

| Consumables & Disposables | 16% |

The Imaging Systems Segment Dominated the Market With 35% in 2025

The imaging systems segment led the U.S. cath labs market with a 35% share in 2025, due to growth in hospitals replacing aging fluoroscopy platforms. The rise in hybrid imaging demand has also increased its use. Advanced visualization also improved procedural outcomes.

The electrophysiology equipment segment held the second-largest share of 16% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 8.8% during the forecast period, due to the rising prevalence of arrhythmia, which expands EP procedures. Advanced mapping technologies also improve their precision. Growing ablation volumes also increase their use.

The consumables & disposables segment held 16% of the U.S. cath labs market share in 2025, driven by high procedure volumes, which drive recurring demand. Single-use devices also improve safety. Growth in interventional procedures also boosts their consumption.

The hemodynamic monitoring systems segment held 15% of the market share in 2025 due to real-time physiological assessment, which supports complex interventions. Digital integration also helps in enhancing workflow. Growing procedure volumes also sustain their adoption.

")

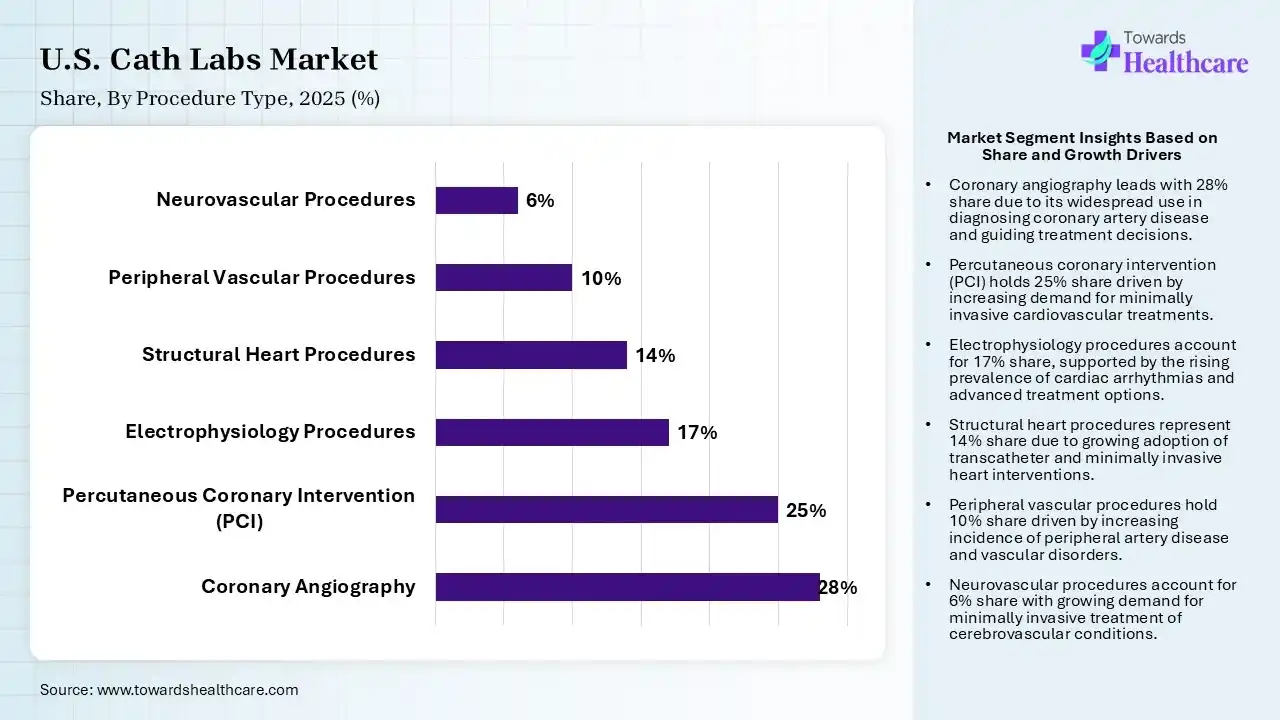

| Segment | Share 2025 (%) |

| Coronary Angiography | 28% |

| Percutaneous Coronary Intervention | 25% |

| Electrophysiology Procedures | 17% |

| Structural Heart Procedures | 14% |

| Peripheral Vascular Procedures | 10% |

| Neurovascular Procedures | 6% |

The Coronary Angiography Segment Dominated the Market With 28% in 2025

The coronary angiography segment accounted for the highest revenue share of 28% of the U.S. cath labs market in 2025, as it remained the primary diagnostic cardiac procedure. An aging population also expanded the patient pool, driving demand. A rise in early disease detection also supported their increased use.

The percutaneous coronary intervention (PCI) segment held the second-largest share of 25% of the market in 2025, due to the increasing coronary artery disease burden, which drives its demand. Improved stent technologies also enhance their outcomes. Rapid treatment protocols also support their utilization.

The electrophysiology procedures segment held 17% of the U.S. cath labs market share in 2025 and is expected to show the highest growth with a CAGR of 8.7% during the forecast period, driven by the rising atrial fibrillation incidence, which expands EP volumes. Mapping innovations helps in improving their success rates. Growing physician expertise also supports their adoption.

The structural heart procedures segment held 14% of the market share in 2025, due to TAVR and valve repair procedures continuing to expand. Elderly patients seek minimally invasive treatment, promoting their use. Clinical evidence also strengthens their adoption.

")

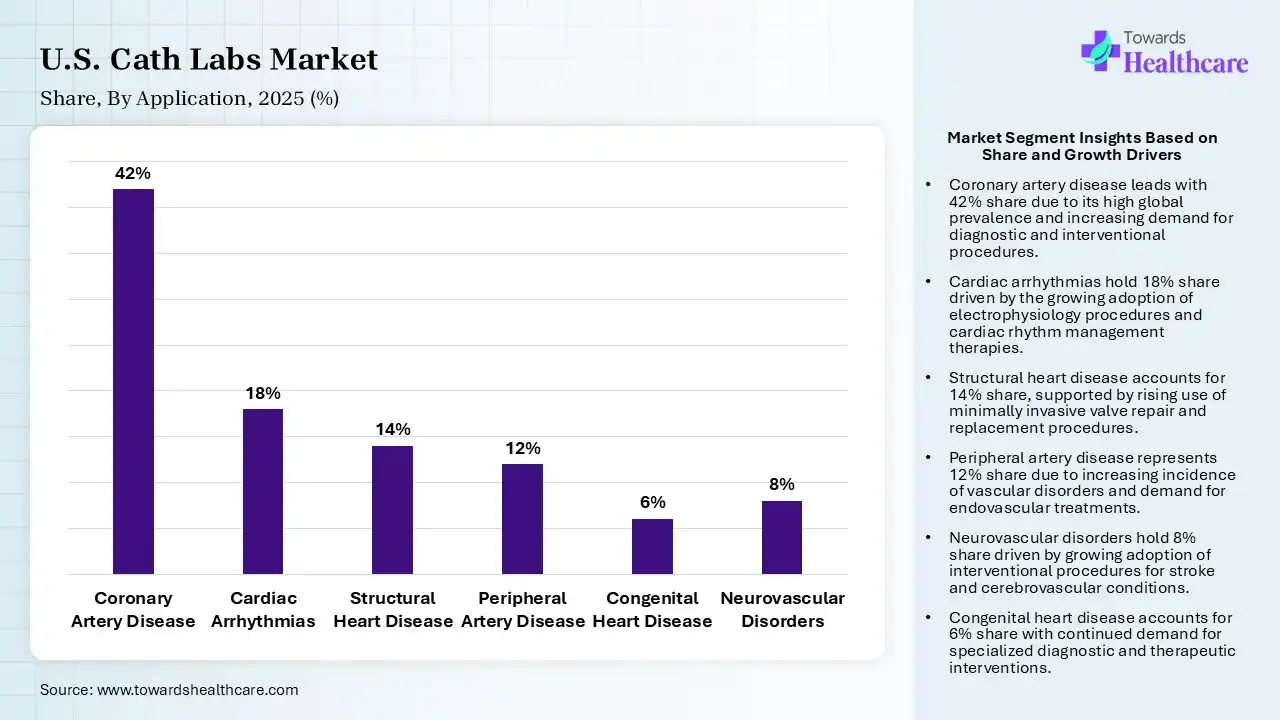

| Segment | Share 2025 (%) |

| Coronary Artery Disease | 42% |

| Cardiac Arrhythmias | 18% |

| Structural Heart Disease | 14% |

| Peripheral Artery Disease | 12% |

| Congenital Heart Disease | 6% |

| Neurovascular Disorders | 8% |

The Coronary Artery Disease Segment Dominated the Market With 42% in 2025

The coronary artery disease segment held a major revenue share of 42% of the U.S. cath labs market in 2025, as CAD remained the leading cardiovascular indication. Lifestyle risk factors also increased disease burden, promoting the use of cath labs. Growth in the intervention rates also increased their use.

The cardiac arrhythmias segment held the second-largest share of 18% of the market in 2025 and is expected to expand rapidly with a CAGR of 8.9% during the forecast period, driven by the rising AFib prevalence, which increases treatment demand. EP technologies also help in improving procedural success. Earlier diagnosis also expands patient volumes.

The structural heart disease segment held 14% of the U.S. cath labs market share in 2025, due to the growing elderly population, which requires valve interventions. Minimally invasive procedures are also enhancing their acceptance rates. Their improving clinical outcomes also drive their demand.

The peripheral artery disease segment held 12% of the market share in 2025, driven by growing diabetes prevalence, which increases vascular complications. Endovascular treatment adoption also promotes their expansion. Increasing screening initiatives also increases their diagnostic rates.

")

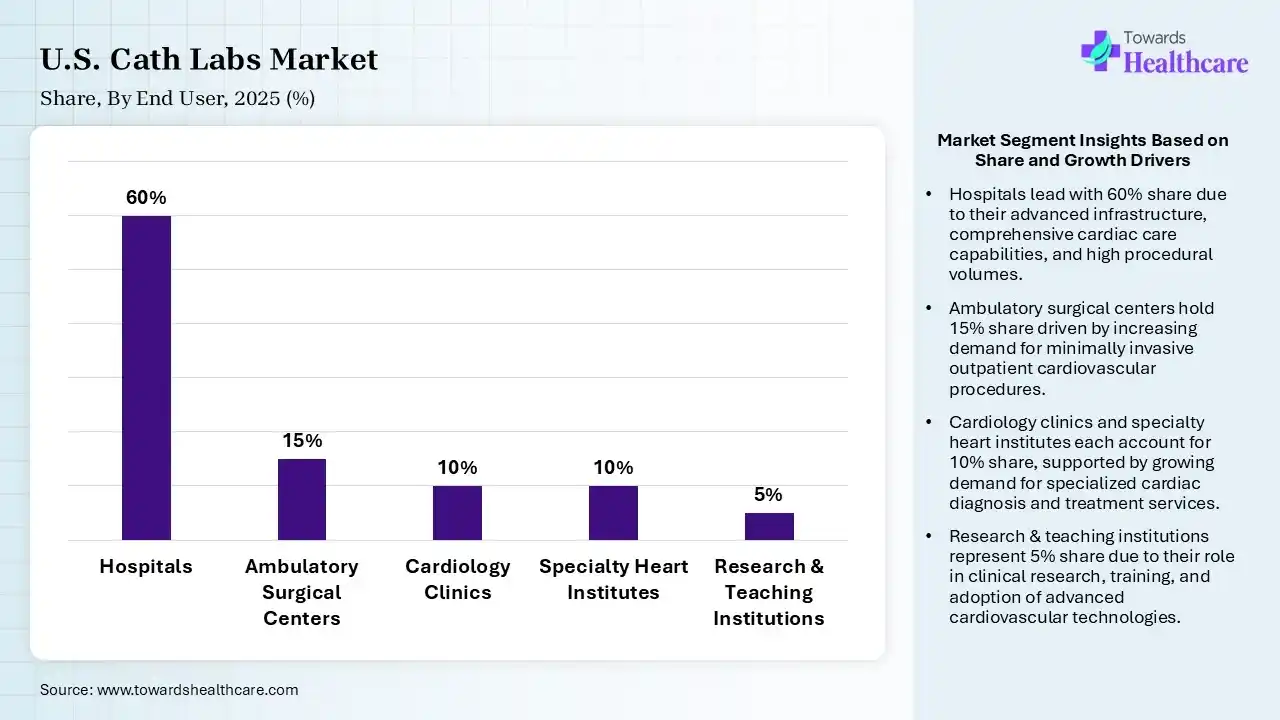

| Segment | Share 2025 (%) |

| Hospitals | 60% |

| Ambulatory Surgical Centers | 15% |

| Cardiology Clinics | 10% |

| Specialty Heart Institutes | 10% |

| Research & Teaching Institutions | 5% |

The Hospitals Segment Dominated the Market With 60% in 2025

The hospitals segment contributed the biggest revenue share of 60% of the U.S. cath labs market in 2025, due to major cardiovascular procedures remaining hospital-centered. Large budgets also supported technology upgrades. High patient throughput also sustained their demand.

The ambulatory surgical centers segment held the second-largest share of 15% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.4% during the forecast period, as outpatient interventions continue expanding. Expanding cost-efficient care models are also increasing their acceptance rate. Reimbursement support also accelerates their growth.

The cardiology clinics segment held 10% of the U.S. cath labs market share in 2025, driven by increased diagnostic procedures. Their enhanced patient convenience also increases their utilization. Integrated care pathways also drive their growth.

The specialty heart institutes segment held 10% of the market share in 2025, due to advanced cardiac programs attracting referrals. Focusing on innovation also supports investments. Growing procedural complexity also increases their demand.

")

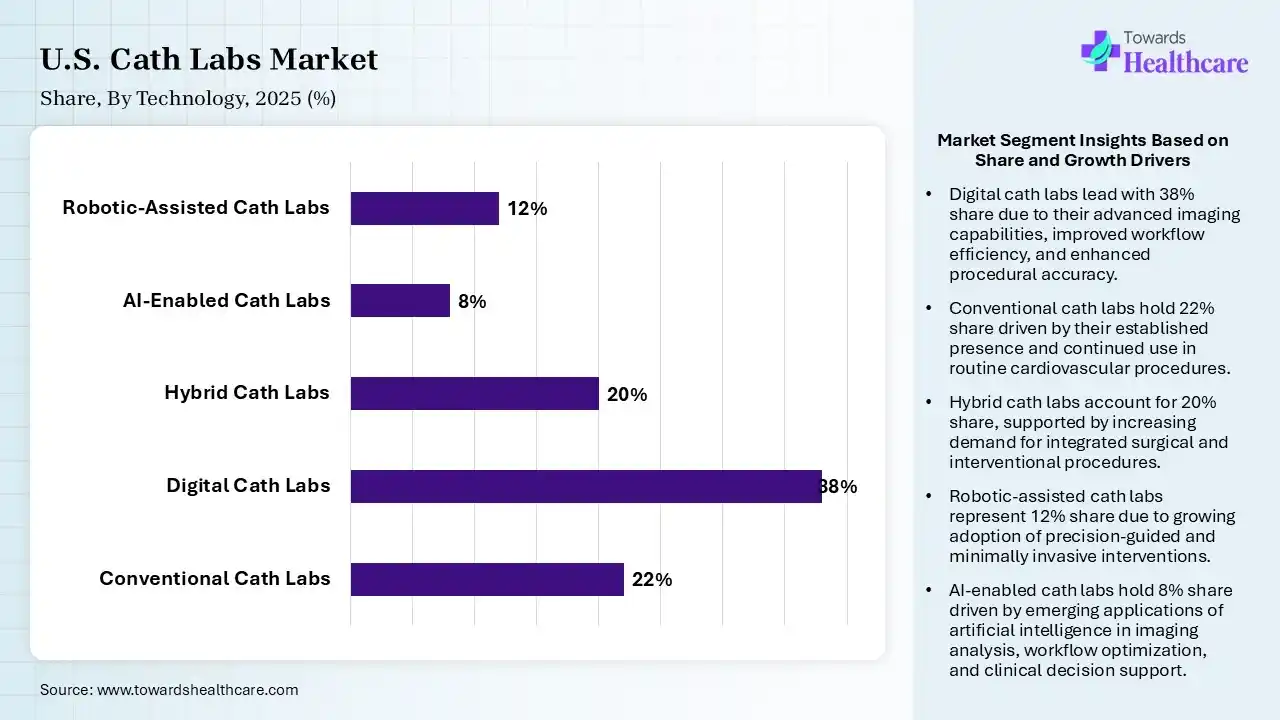

| Segment | Share 2025 (%) |

| Conventional Cath Labs | 22% |

| Digital Cath Labs | 38% |

| Hybrid Cath Labs | 20% |

| AI-Enabled Cath Labs | 8% |

| Robotic-Assisted Cath Labs | 12% |

The Digital Cath Labs Segment Dominated the Market With 38% in 2025

The digital cath labs segment held the largest revenue share of 38% of the U.S. cath labs market in 2025, driven by digital imaging, which improved workflow and visualization. Hospitals prioritized modernization, which encouraged their use. Better data integration also promoted their adoption.

The conventional cath labs segment held the second-largest share of 22% of the market in 2025, due to the existing installed base remaining substantial. Budget-conscious facilities also continue their utilization. Replacement cycles also remain gradual.

The hybrid cath labs segment held 20% of the U.S. cath labs market share in 2025, driven by complex structural procedures requiring hybrid environments. Multidisciplinary care also expands its demand. Increasing hospitals' investments in advanced infrastructure is also promoting their growth.

The AI-enabled cath labs segment held 8% of the market share in 2025 and is expected to grow with the fastest CAGR of 11.2% during the forecast period, as AI enhances image analysis and workflow optimization. Predictive insights also improve efficiency. Hospitals are also accelerating digital transformation.

The U.S. cath labs market is expected to show considerable growth during the forecast period, due to the growth in cardiovascular diseases. A rise in the geriatric population and health awareness has also increased their dependence on the cath labs. Advancements in medical devices and structural heart procedures also contributed to the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | U.S. Cath Labs Solutions |

| GE HealthCare | Chicago, U.S. | Innova IGS series and Allia IGS interventional imaging suites |

| Abbott Laboratories | Abbott Park, U.S. | XIENCE and TriClip/MitraClip structural heart transcatheter systems |

| Koninklijke Philips N.V. | Amsterdam, Netherlands | Azurion series and Allura FD image-guided systems |

| Edwards Lifesciences Corporation | Irvine, U.S. | SAPIEN 3 Ultra transcatheter heart valves |

| Siemens Healthineers AG | Erlangen, Germany | Artis icono and Artis zee angiography C-arm systems |

| Merit Medical Systems, Inc. | South Jordan, U.S. | Prelude sheath introducers and diagnostic catheters |

| Medtronic plc | Dublin, Ireland | Resolute Onyx drug-eluting stents and Evolut FX TAVR system |

| Cordis (A Cardinal Health Company) | Miami Lakes, U.S. | VISTA BRITE TIP guiding catheters and EMERALD diagnostic guidewires |

| Boston Scientific Corporation | Marlborough, U.S. | Synergy bioabsorbable polymer drug-eluting stents |

| Terumo Medical Corporation | Tokyo, Japan | Glidesheath Slender and Glidecath radial access systems |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Procedure Type

By Application

By End User

By Technology

By Facility Type

By Ownership Model

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar