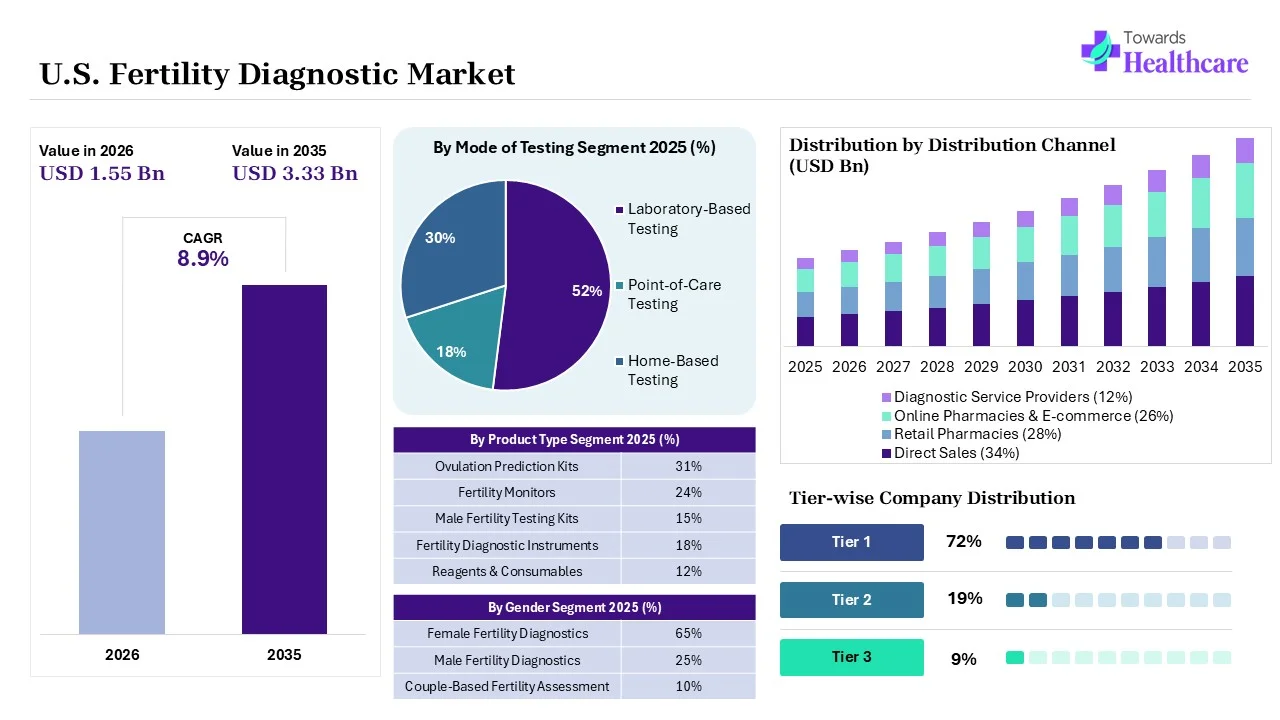

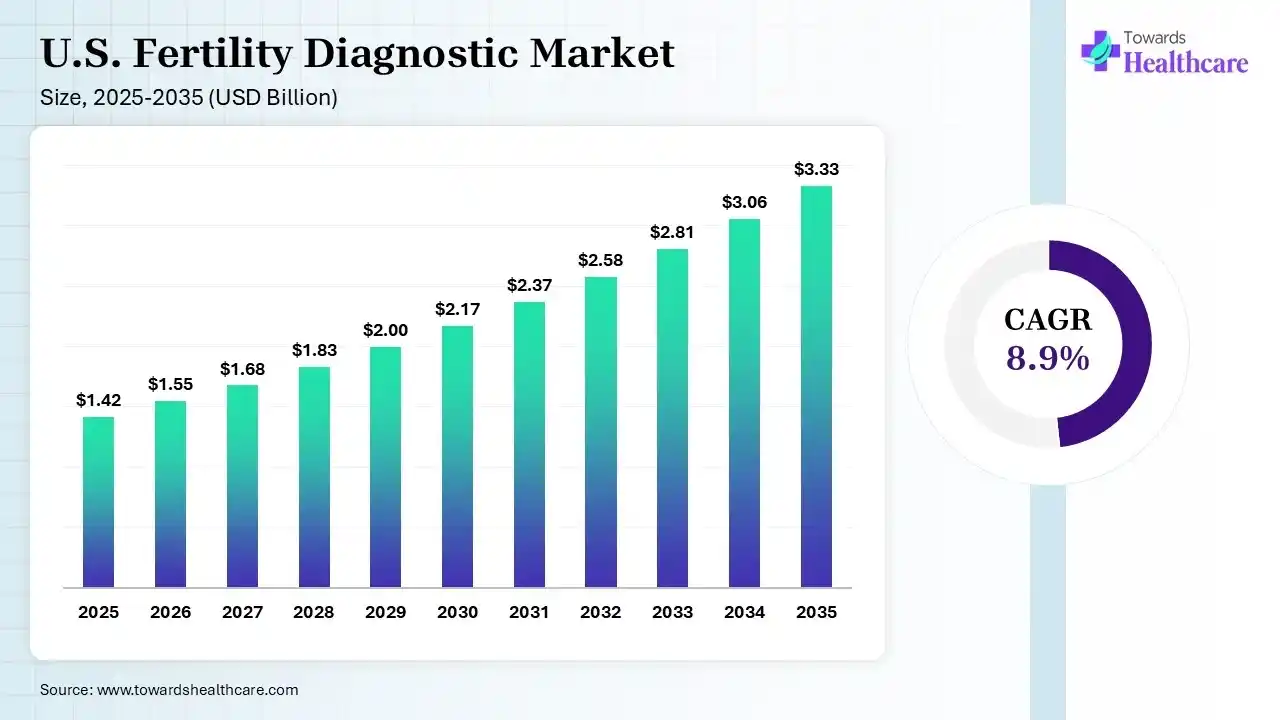

The U.S. fertility diagnostics market size was estimated at USD 1.42 billion in 2025 and is predicted to increase from USD 1.55 billion in 2026 to approximately USD 3.33 billion by 2035, expanding at a CAGR of 8.9% from 2026 to 2035.

")

A fertility diagnostic is a health history discussion, particularly to check for ovulation or menstrual cycle challenges. Blood tests to check hormone levels and ovarian reserve, the number of potential eggs remaining in a woman's ovaries. This diagnostic enables easy and early detection, diagnosis, and management of endometritis, vaginitis, and microbiome dysbiosis, which have been significantly related to female reproductive system pathologies and infertility, RIF, RPL, chemical pregnancies, and severe problems of the second and third trimesters. Fertility tests for women support detecting the cause of infertility so the condition can be treated correctly and the couple has the best chance to conceive. According to the American Society for Reproductive Medicine, sterility affects men and women similarly, so both partners must be tested.

Six-in-ten (61%) people have received fertility testing for themselves or their partner, and 43% have used drugs to improve ovulation. The U.S. is still one of the highest-volume ART consumers worldwide, with more than 435,000 ART cycles performed yearly and over 94,000 ART-assisted births per year, which shows approximately 2.6 % of all births. More than 371 certified fertility clinics operate in the U.S., and assisted reproduction is used by more than 251,000 patients yearly.

The provisional vital statistics for the United States in 2025 reveal shifting fertility patterns and rising surgical delivery rates, according to the CDC National Center for Health Statistics.

Birth and Fertility Rates

Delivery and Gestation Statistics

Total Cesarean Deliveries: The rate increased to 32.5%, up from 32.4% in 2024.

Low-Risk Cesarean Deliveries: The rate rose to 26.9%, up from 26.6% in 2024.

Preterm Births: The rate remained completely unchanged at 10.41%.

AI-based technology has the strength to improve infertility diagnosis and assisted reproductive technology (ART) results, like pregnancy and live birth rates, specifically in cases of recurrent ART failure. As AI continues to be integrated into different healthcare sectors, it merges knowledge and computer science through machine learning algorithms. AI-powered automation enhances efficiency, accuracy, and consistency, reducing variability among IVF centres and operators. The use of AI and advanced technology in IVF treatment improves fertility care with AI-based embryo selection and innovative IVF techniques. These technologies employ machine learning, computer vision, predictive analytics, robotics, and big data to improve precision, efficiency, and success rates during the IVF process. AI utilizes computational models like neural networks, deep learning, and machine learning algorithms to analyze large datasets from imaging systems, lab results, patient histories, and treatment cycles.

| Table | Scope |

| Market Size in 2026 | USD 1.55 Billion |

| Projected Market Size in 2035 | USD 3.33 Billion |

| CAGR (2026 - 2035) | 8.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Test Type, By Mode of Testing, By Gender, By User |

| Top Key Players | GE HealthCare, Koninklijke Philips N.V., Samsung Healthcare, CooperSurgical, Inc., Femasys Inc. |

")

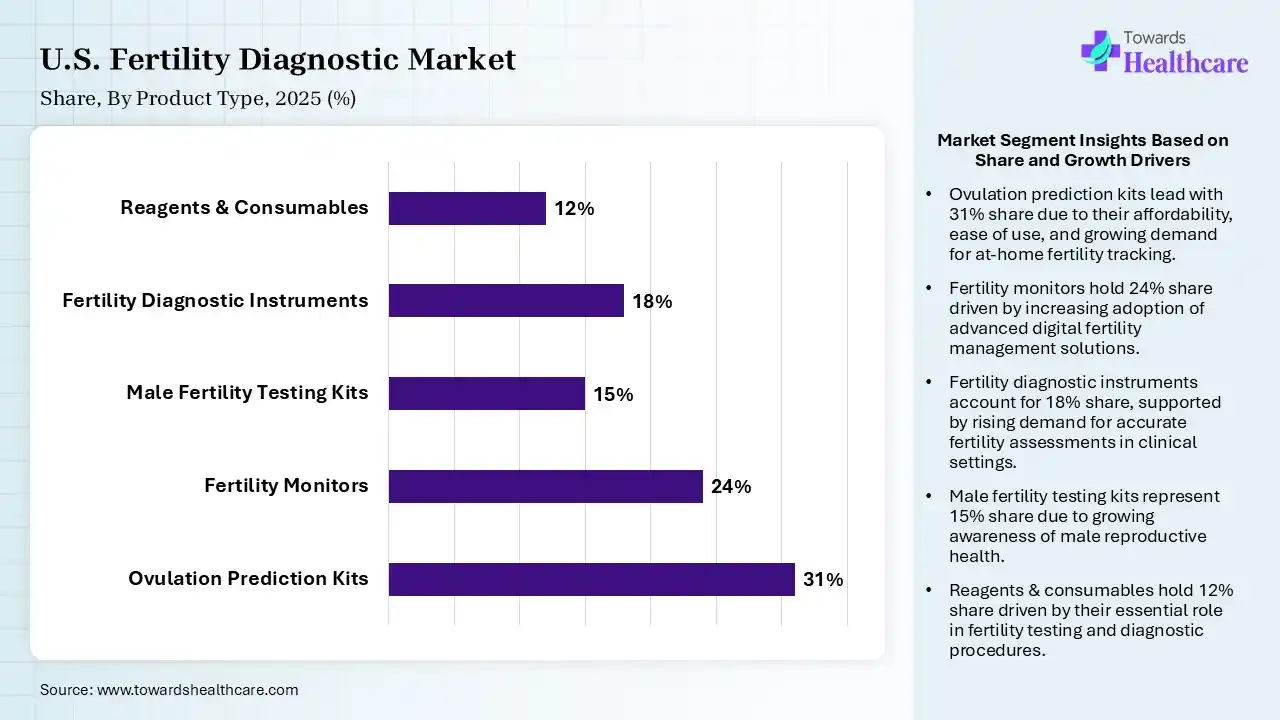

| Segments | Shares % |

| Ovulation Prediction Kits | 31% |

| Fertility Monitors | 24% |

| Male Fertility Testing Kits | 15% |

| Fertility Diagnostic Instruments | 18% |

| Reagents & Consumables | 12% |

The Ovulation Prediction Kits Segment Led the U.S. Fertility Diagnostic Market in 2025

The ovulation prediction kits segment contributed the largest market share of 31% in 2025, as ovulation kits look for a rise in the luteinizing hormone, which causes women to ovulate and release an egg. OPKs are more accurate than any other process for identifying ovulation and are 97% efficient in the detection of the LH surge. It offers precise outcomes in most cases, but it is significant if used in combination with other processes of monitoring ovulation.

The fertility monitors segment held a significant share of 24% and is expected to grow at the fastest CAGR of 10.8% during the forecast period in the market. This is a very thorough test as it measures both luteinizing hormone levels and basal body temperature. In addition, the monitor measures estrogen and progesterone and provides information concerning ovulation times and the menstrual cycle.

The fertility diagnostic instruments segment held a significant share of 18% in the U.S. fertility diagnostic market, as fertility tests support detecting significant issues with fertility in both males and females. Tests involve ultrasounds, semen samples, or blood tests. Testing supports them, detects potential challenges, and develops a precise plan to support maximizing the ability to have children.

The male fertility testing kits segment held a significant share of 15%, as at-home semen analysis kits offer a quick, affordable tool for assessing fertility strength in couples seeking pregnancy, which is affected by male factor infertility. They detect genetic causes of infertility, involving conditions that affect the Y chromosome. A home sperm test states whether there are sperm in the semen sample. Some at-home tests report how well the sperm move.

")

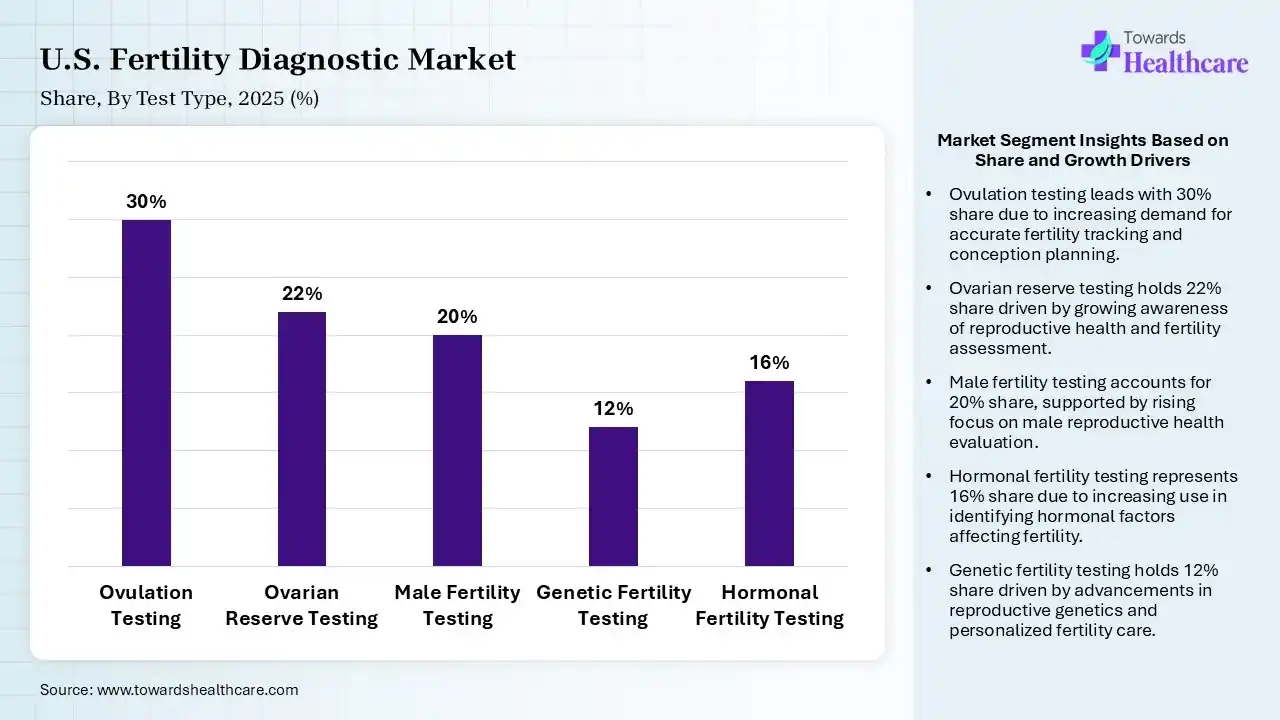

| Segments | Shares % |

| Ovulation Testing | 30% |

| Ovarian Reserve Testing | 22% |

| Male Fertility Testing | 20% |

| Genetic Fertility Testing | 12% |

| Hormonal Fertility Testing | 16% |

Ovulation Testing Segment Led the U.S. Fertility Diagnostic Market in 2025

The ovulation testing segment contributed the largest market share of 30%. Ovulation tests actually significant for women looking to get pregnant. They spot the LH surge, which happens before ovulation, to figure out the optimal time to conceive. This supports increasing a woman's probability of getting pregnant. Ovulation predictor kits in place of serum testing lower clinic staff burden on holidays, weekends, and during peak visit times, such as morning monitoring.

The ovarian reserve testing segment held a significant share of 22% of the market, as ovarian reserve testing is used to support patients in anticipating the ovarian response to stimulation, particularly the number of oocytes. The test supports gauging the probability of successful conception and offers valuable data about fertility treatment choices. Ovarian reserve testing is applied to evaluate the number of eggs available for fertilization.

The male fertility testing segment held a significant share of 20% of the U.S. fertility diagnostic market, as male fertility tests earlier in evaluations offer more precise guidance for a couple's pregnancy journey. Sperm DNA integrity supports differentiating fertile from infertile men. A semen analysis test assesses the quality and quantity of sperm in a semen sample.

The genetic fertility testing segment held a significant share of 12% of the market and is expected to grow at the fastest CAGR of 11.5% during the forecast period. Genetic testing significantly enhances the chance of achieving a positive pregnancy. This testing prevents the birth of a child with deadly genetic conditions. Genetic testing before IVF includes advanced implantation rates, reduces miscarriages, and lowers transfer cycles.

")

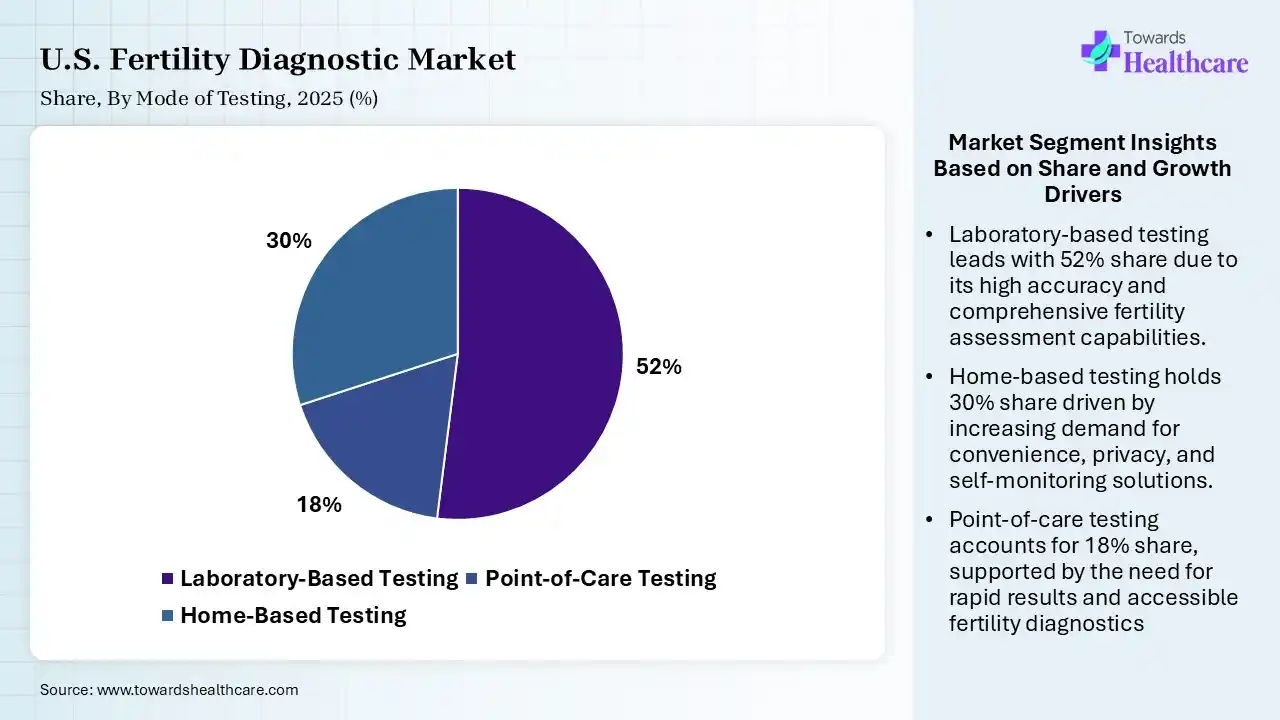

| Segments | Shares % |

| Laboratory-Based Testing | 52% |

| Point-of-Care Testing | 18% |

| Home-Based Testing | 30% |

The Laboratory-Based Testing Segment led the U.S. Fertility Diagnostic Market in 2025

The laboratory-based testing segment held a major share of 52% in the market, as fertility tests support identifying challenges with fertility, like hormonal imbalances, low egg count, and poor semen quality. Fertility testing is significant to understanding reproductive health and identifying potential complexities in conception.

The home-based testing segment contributed the second-largest market share of 30%, and is expected to grow at the fastest CAGR of 11.2% during the forecast period, as at-home testing choice available, which measure a diversity of fertility features, involving particular hormones and semen quality. The precision of these tests is based on an individual’s health history, when the tests are finished, and where the samples are analysed.

The point-of-care testing segment held a significant 18% share of the market, as POCT offers rapid turnaround of output as compared to core laboratory testing, as POCT removes transportation of blood specimens and considerably lowers processing and preanalytical steps needed for laboratory tests.

")

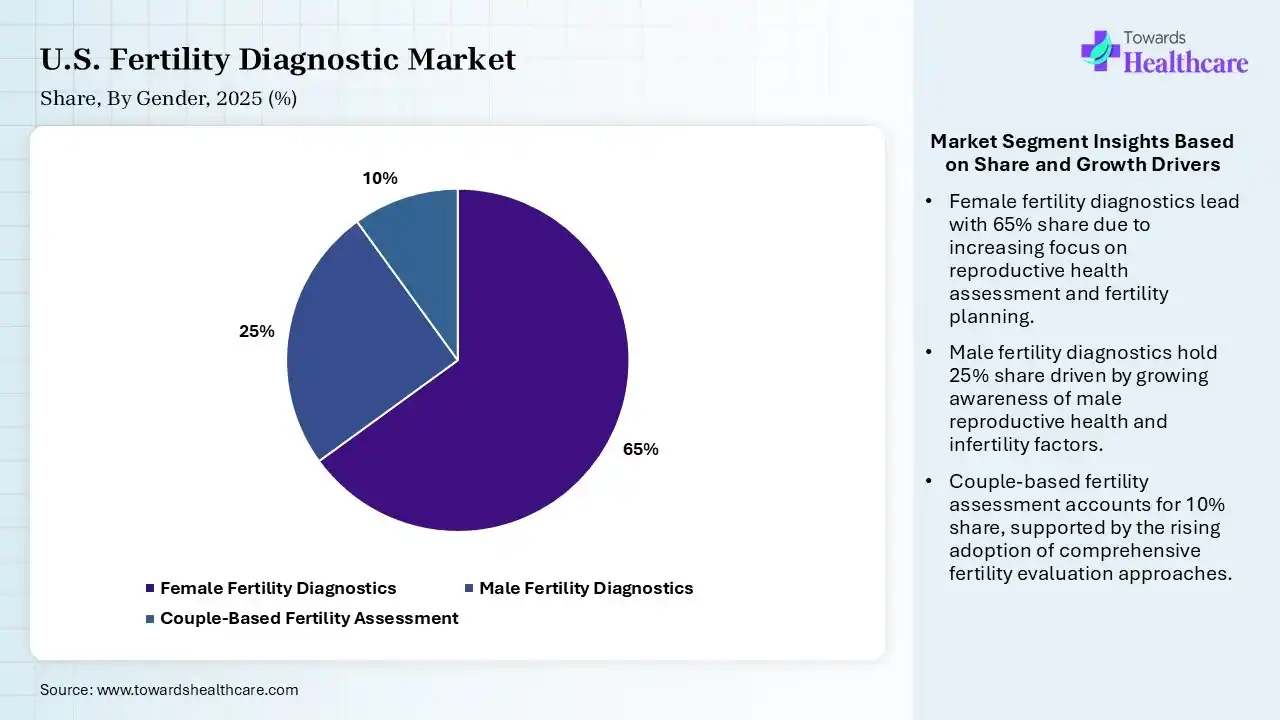

| Segments | Shares % |

| Female Fertility Diagnostics | 65% |

| Male Fertility Diagnostics | 25% |

| Couple-Based Fertility Assessment | 10% |

The Female Fertility Diagnostics Segment led the U.S. Fertility Diagnostic Market in 2025

The female fertility diagnostics segment contributed the largest market share of 65%, as this testing helps identify problems early and gives women the best chance to become mothers. Early diagnosis provides emotional advantages, lowering frustration and stress while managing couples via appropriate treatment pathways.

The male fertility diagnostics segment held a significant share of 25% in the market and is expected to grow at the fastest CAGR of 10.1% during the forecast period. Male fertility tests earlier in evaluations provide more precise guidance for a couple's pregnancy journey. A male fertility test is a significant step in detecting the reasons behind delayed conception. It’s easy, rapid, and leads to life-changing outputs when followed by accurate treatment.

The couple-based fertility assessment segment held a significant share of 10% in the market, as this test offers better control over fertilisation and embryo selection, which is more efficient for women with serious infertility challenges. IVF has significant possible benefits for couples and single women who want children.

")

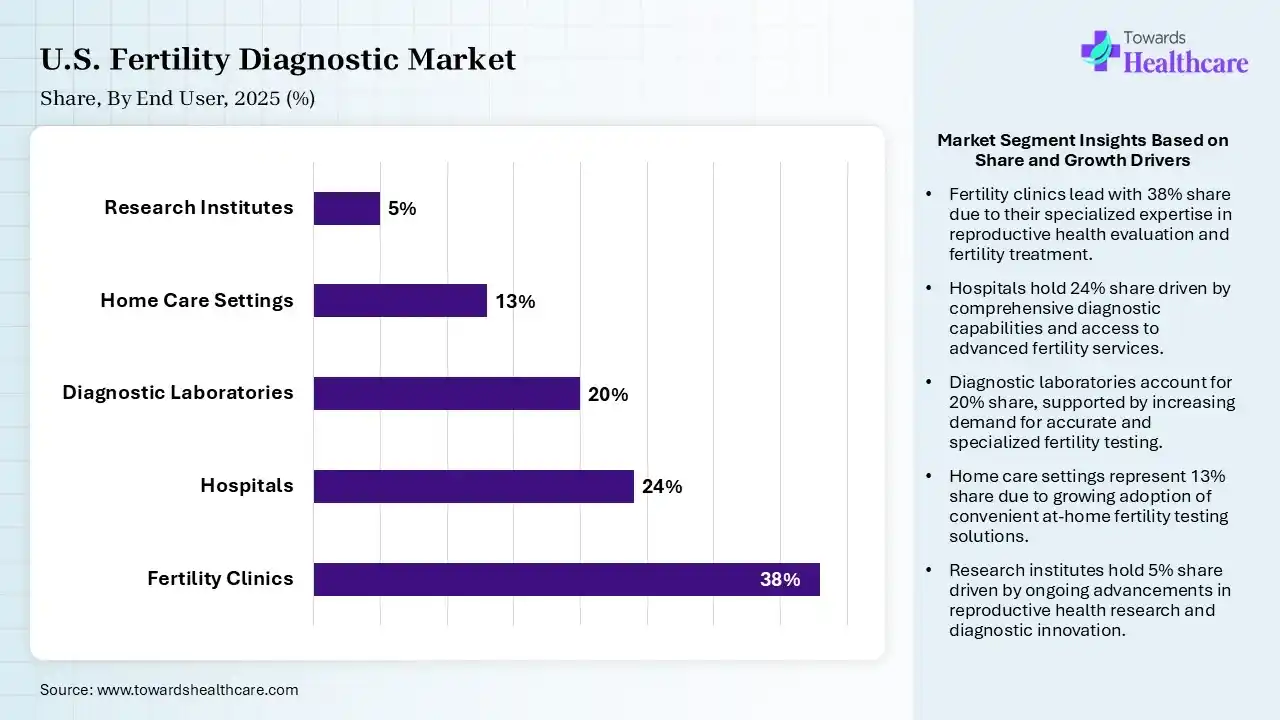

| Segments | Shares % |

| Fertility Clinics | 38% |

| Hospitals | 24% |

| Diagnostic Laboratories | 20% |

| Home Care Settings | 13% |

| Research Institutes | 5% |

The Fertility Clinics Segment led the U.S. Fertility Diagnostic Market in 2025

The fertility clinics segment contributed the largest market share of 38%, as this clinic has access to advanced ART such as IVF, high-precision diagnostics, and expert embryology laboratories, which bypass challenging biological complexes. These specialized centers offer targeted, evidence-driven care, which significantly increases conception probabilities. Fertility clinics have excellent fertility management.

The hospitals segment held a significant share of 24% in the market, as these hospitals offer a seamless incorporation of general gynaecological care and targeted fertility treatments. This means patients receive inclusive care in the same hospital, from initial consultations and diagnostics to advanced reproductive processes and follow-up care.

The diagnostic laboratories segment held a significant share of 20% in the U.S. fertility diagnostic market, as this laboratory testing helps bring any underlying medical conditions to light, so patients and doctors find the standard way to manage their problems. Fertility testing is provided to find the root of an inability to conceive children and supports making a precise diagnosis and fertility management plans.

The home care settings segment held a significant share of 13% in the market and is expected to grow at the fastest CAGR of 11.4% during the forecast period. A fertility-friendly home care includes making conscious adaptations to optimize the environment, lower stress, and promote healthy living. It enables the identification and amendment of health challenges to the potential mother before conception.

In the U.S., financial, racial, ethnic, geographic, and various disparities prevent access to fertility management and affect treatment results, which increases the demand for fertility diagnostics. Rising interest in at-home testing is sharply increasing in this region. There is a significant shift from early consumer-grade pregnancy kits to comprehensive, high-standard at-home diagnostics for both men and women. DTC ovarian reserve testing is an advanced tool in a major medical and social project to lessen anticipated future infertility. Most U.S.-driven research on IVF-treated patients has centered on quantitative clinical results relating to pregnancy and childbirth, which drives the growth of the U.S. fertility diagnostic market.

R&D:

Manufacturing Processes:

Patient Services:

| Company | Headquarters | Latest Update |

| GE HealthCare | U.S. | In 2025, GE HealthCare generated $20.6 billion in revenue, with products accounting for approximately 66% and services accounting for around 34%. |

| Koninklijke Philips N.V. | U.S. | In 2025, Philips innovations improved the lives of 2 billion people. The ambition is to enhance 2.5 billion lives each year by 2030. |

| Samsung Healthcare | U.S. | In 2025, Samsung Medison showcased its upgraded HERA Z20 AI-driven ultrasound system intended for women’s healthcare across all life stages, from fertility and pregnancy to menopause. |

| CooperSurgical, Inc. | U.S. | In April 2025, The Wyatt Foundation and The Conceive Fertility Foundation announced the launch of their 2025 IVF grant services, which will award $15,000 grants to five couples who require in vitro fertilization (IVF) to build their families. |

| Femasys Inc. | U.S. | In December 2025, Femasys Inc., it has received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its FemVue Controlled device, an advanced diagnostic service intended for controlled contrast delivery to evaluate fallopian tube status. |

In June 2026, "Most fertility products were designed for a woman to use alone, often with the quiet assumption that her partner would cheer her on from the sidelines," said Scarlett Joowon Jung, CEO of Vespexx. "We've spent the last three years proving with Signaling that couples want to share this experience, and Soonr brings that conviction into the moment that matters most. The science backs it up, and the experience of trying to conceive deserves to reflect that."

In June 2026, Vespexx Inc., a femtech organization building products around the science of dyadic health, announced the official U.S. launch of Soonr Health, a preconception health platform intended for couples who are trying to conceive.

In January 2026, U.S. Fertility, the nation’s largest collaboration of physician-owned fertility practices, announced that the Piedmont Reproductive Endocrinology Group (PREG) has combined its growing network of leading fertility practices and IVF laboratories.

By Product Type

By Test Type

By Mode of Testing

By Gender

By End User

By Distribution Channel

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar