.webp "U.S. Healthcare Payers Core Administrative Processing Solutions Market to Grow USD 4.07 Billion in 2026")

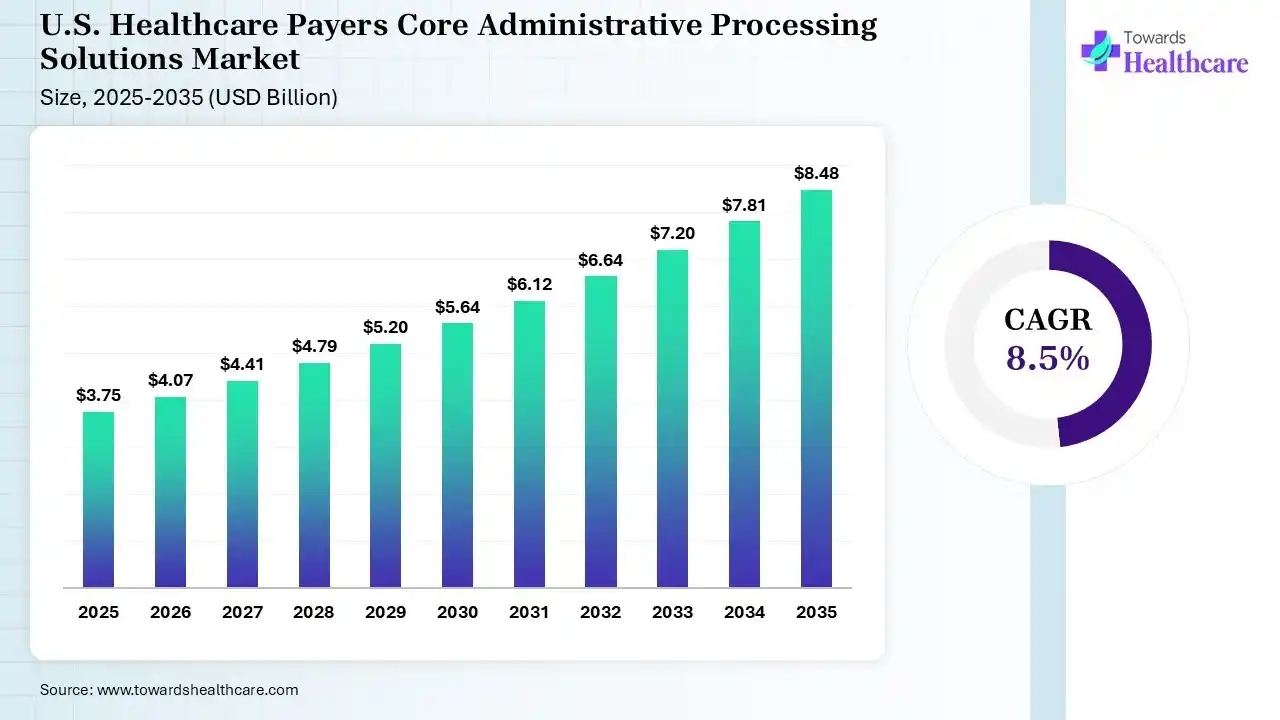

The U.S. healthcare payers core administrative processing solutions market size was estimated at USD 3.75 billion in 2025 and is predicted to increase from USD 4.07 billion in 2026 to approximately USD 8.48 billion by 2035, expanding at a CAGR of 8.5% from 2026 to 2035.

")

The healthcare payers' core administrative processing solutions (CAPS) are software platforms that help health insurers manage critical operations such as claims processing, member enrollment, eligibility verification, billing, benefits administration, and provider management. These solutions improve efficiency, accuracy, compliance, and customer service. Growth is driven by rising healthcare complexity, increasing claims volumes, and evolving regulatory requirements. Key trends include cloud adoption, automation, and interoperability, while opportunities lie in value-based care and digital member engagement. Technological advancements such as AI, machine learning, robotic process automation (RPA), and predictive analytics are enhancing operational performance, fraud detection, and decision-making capabilities.

The U.S. healthcare payers core administrative processing solutions market has grown steadily due to rising health insurance enrollment, increasing claims volumes, and evolving regulatory requirements. Payers have increasingly adopted automated and cloud-based administrative platforms to improve efficiency, reduce operational costs, enhance claims accuracy, and support value-based care models, driving continuous market expansion over the years.

Artificial intelligence is transforming U.S. healthcare payers’ core administrative processing solutions by automating claims adjudication, eligibility verification, fraud detection, and customer support processes. AI-powered analytics enhance decision-making, reduce administrative costs, improve accuracy, and accelerate processing times. As payers seek greater efficiency and personalized member services, AI adoption is becoming a key driver of operational modernization and competitive advantage.

Accelerating Shift to Cloud-Based Solutions

Healthcare payers are increasingly adopting cloud-based core administrative platforms to improve operational flexibility, scalability, and cost efficiency. These solutions enable faster deployment, easier system upgrades, and better integration with healthcare ecosystems, helping organizations respond more effectively to changing business and regulatory requirements.

Rising Focus on Interoperability and Data Exchange

Payers are prioritizing interoperable systems that enable seamless data sharing among providers, members, and healthcare stakeholders. Enhanced connectivity improves care coordination, reduces administrative complexities, supports regulatory compliance, and facilitates more accurate and efficient management of healthcare information.

Growing Adoption of Value-Based Care Models

The transition from fee-for-service to value-based care is driving demand for advanced administrative solutions. Payers are investing in platforms that support quality measurement, population health management, and outcome-based reimbursement, helping improve patient care while controlling healthcare costs and enhancing long-term operational effectiveness.

| Table | Scope |

| Market Size in 2026 | USD 4.07 Billion |

| Projected Market Size in 2035 | USD 8.48 Billion |

| CAGR (2026 - 2035) | 8.5% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Solution Type, By Deployment Type, By End User |

| Top Key Players | Cognizant, HealthEdge, SS&C Technologies, Optum, Oracle Health |

")

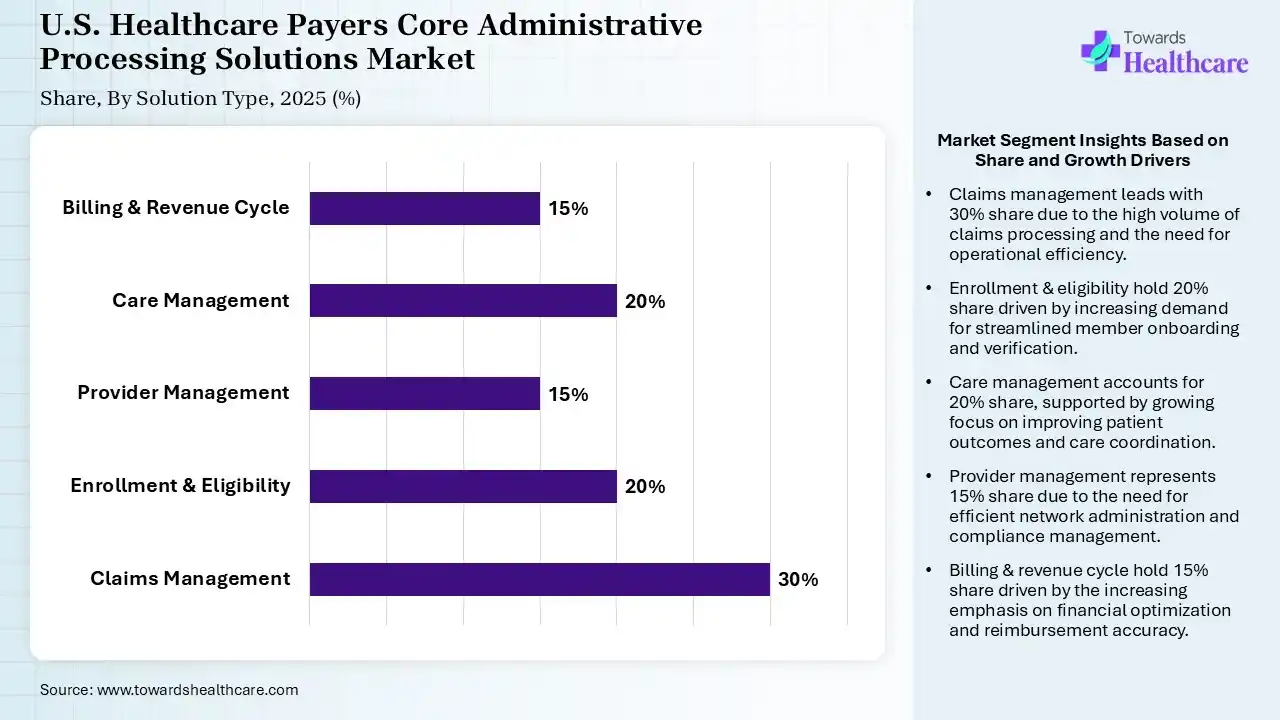

| Segments | Shares % |

| Claims Management | 30% |

| Enrollment & Eligibility | 20% |

| Provider Management | 15% |

| Care Management | 20% |

| Billing & Revenue Cycle | 15% |

The Claims Management Segment Dominated the Market in 2025

The claims management segment held a dominant share of 30% in the U.S. healthcare payers core administrative processing solutions market in 2025 due to the high volume and complexity of healthcare claims processed daily. Health insurance relies on advanced claims management systems to improve adjudication accuracy, reduce processing time, minimize payment errors, ensure regulatory compliance, and control administrative costs. Growing healthcare utilization and reimbursement requirements have further strengthened demand for efficient claims management solutions.

The enrolment & eligibility segment held the second-largest share of 20% in 2025 and is expected to grow at the fastest CAGR of 9% in the U.S. healthcare payers core administrative processing solutions market during the forecast period due to the growing need for accurate member onboarding and coverage verification. These solutions help insurers streamline enrollment processes, reduce administrative errors, ensure compliance with healthcare regulations, and improve member experiences. Rising insurance participation and frequent eligibility updates have further increased demand for efficient enrollment and eligibility management systems.

The care management segment held 20% of the U.S. healthcare payers core administrative processing solutions market share due to the increasing focus on improving patient outcomes and reducing healthcare costs. Healthcare payers are adopting care management solutions to support clinics’ disease management, care coordination, risk assessment, and population health initiatives. The growing shift toward value-based care models and preventive healthcare strategies is further driving demand, helping payers enhance care quality while optimizing resource utilization.

The provider management segment held a 15% market share as healthcare payers seek to streamline provider onboarding, credentialing, contract administration, and network management processes. Growing provider network, increasing regulatory requirements, and the need for accurate provider data are driving adoption. These solutions help improve operational efficiency, strengthen payer-provider collaboration, reduce administrative burden, and ensure better access to quality healthcare services for members.

")

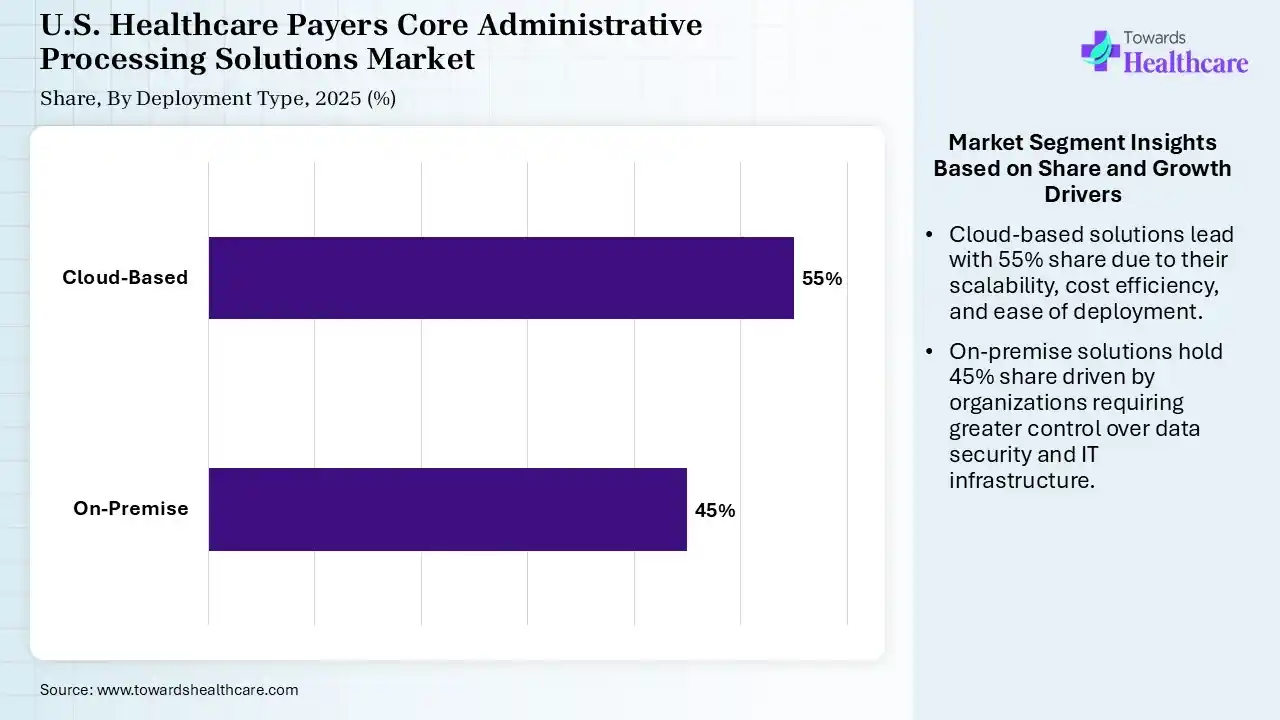

| Segments | Shares % |

| On-Premise | 45% |

| Cloud-Based | 55% |

The Cloud-based Segment Led the Market in 2025 with the Largest Share

The cloud-based segment led the U.S. healthcare payers core administrative processing solutions market with a share of 55% in 2025 and is expected to grow at the fastest CAGR of 11% in the market during the forecast period due to its scalability, flexibility, and cost-effectiveness. Cloud platforms enable payers to efficiently manage large volumes of claims and member data while supporting real-time access, seamless systems integration, and faster updates. Growing demand for operational agility, remote accessibility, and reduced IT infrastructure costs has further accelerated cloud adoption across payer organizations.

The on-premise segment held the second-largest share of 45% in 2025 due to its strong data control, security, and customization capabilities. Large healthcare payers often prefer on-premise deployment to meet strict regulatory requirements, protect sensitive patient and claims data, and maintain direct oversight of critical operations. Existing IT investments and legacy system integration also continue to support demand for on-premise solutions.

")

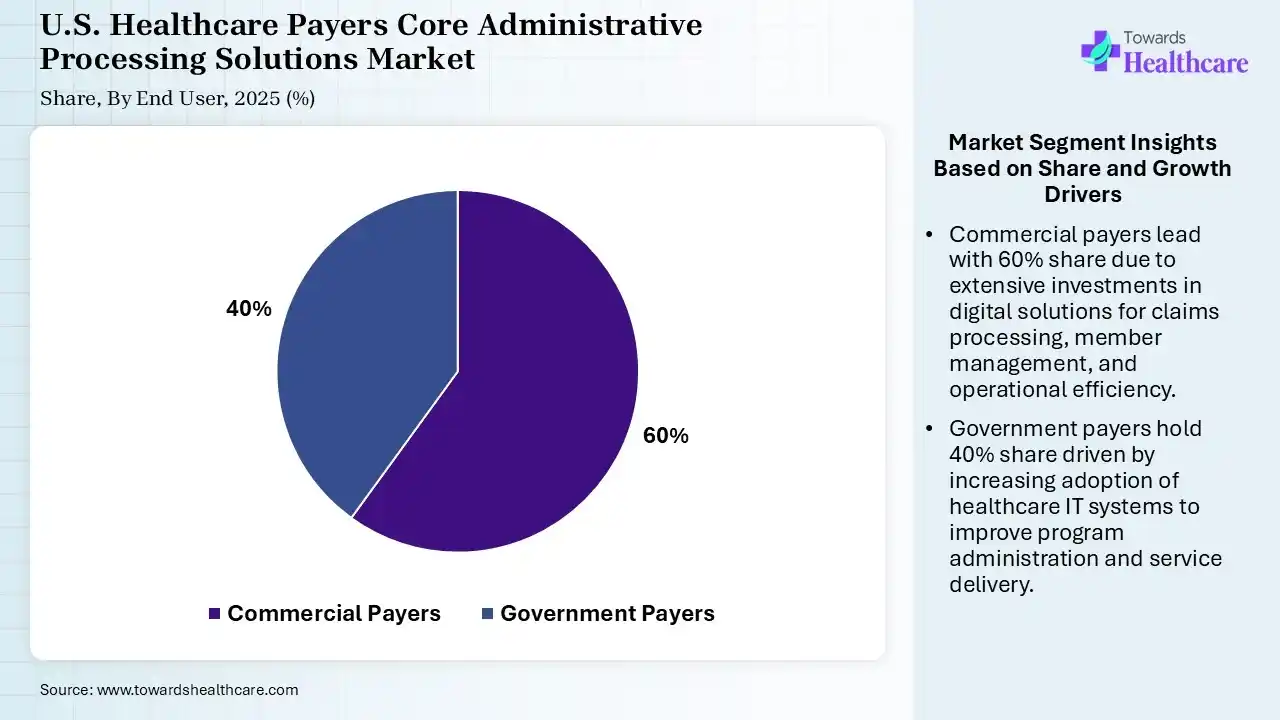

| Segments | Shares % |

| Commercial Payers | 60% |

| Government Payers | 40% |

The Commercial Payers Segment Led the Market in 2025 with the Largest Share

The commercial payers segment held a dominant share of the U.S. healthcare payers core administrative processing solutions market of 60% in 2025 due to its large membership base, high claims volumes, and extensive administrative requirements. Commercial insurers rely heavily on advanced processing solutions to manage enrollment, claims adjudication, provider networks, billing, and compliance activities efficiently. Growing demand for operational efficiency, enhanced member experience, and cost control has further strengthened adoption among commercial payer organizations.

The government payers segment held the second-largest share of 40% in 2025 due to the large enrolment base in programs such as Medicare and Medicaid. These organizations require robust administrative systems to manage complex claims processing, eligibility verification, regulatory compliance, and beneficiary services. Increasing healthcare expenditures and ongoing modernization initiatives have further driven the adoption of advanced processing solutions among government payers.

The Medicaid sub-segment held a 15% share in 2025 and is expected to grow at the fastest CAGR of 10% in the U.S. healthcare payers core administrative processing solutions market during the forecast period due to expanding beneficiary enrollment, increasing state healthcare spending, and ongoing program modernization efforts. Medicaid organizations are investing in advanced administrative platforms to improve claims management, eligibility determination, care coordination, and regulatory compliance. The growing focus on digital transformation and efficient healthcare delivery is further accelerating adoption.

The Medicare sub-segment held a 25% market share due to the increasing aging population and rising enrollment in Medicare and Medicaid. Advantage plans across the United States. Healthcare payers are adopting advanced administrative processing solutions to efficiently manage claims, member services, regulatory compliance, and the reimbursement process. Growing healthcare utilization among seniors and the need for streamlined operations are further driving demand for core administrative processing solutions in the Medicare segment.

The U.S. healthcare payers core administrative processing solutions market benefits from a well-established health insurance industry, high healthcare expenditure, and a large insured population. Rising claims volumes, complex regulatory requirements, and increasing demand for operational efficiency are driving solutions adoption. The presence of major technology providers, growing cloud implementation, expanding value-based care programs, and continuous investments in healthcare IT modernization further strengthened the market’s growth across the country.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| Cognizant | Teaneck, New Jersey, USA | Core administration platforms, claims processing, member enrollment, eligibility management, provider management, and care management solutions. |

| HealthEdge | Massachusetts, USA | Payer administration systems, claims adjudication, payment integrity, care management, and member engagement solutions. |

| SS&C Technologies | Connecticut, USA | Healthcare administration software, claims management, billing solutions, workflow automation, and analytics platforms. |

| Optum | Eden Prairie, Minnesota, USA | Claims administration, payment solutions, healthcare analytics, interoperability tools, and population health management services. |

| Oracle Health | Austin, Texas, USA | Healthcare data management, payer administration, interoperability solutions, cloud platforms, and analytics tools. |

In September 2025, Kevin Adams, CEO of HealthEdge, stated: “Health plans are looking for new ways to manage rising costs, regulatory complexity, and member expectations. Our integrated approach provides a more effective and streamlined solution for healthcare payers.”

In September 2025, HealthEdge combined its capabilities with UST HealthProof to create a more integrated payer administration platform. The collaboration strengthened solutions for claims management, payment accuracy, operational efficiency, and member engagement, while expanding the use of advanced automation and intelligent technologies across payer operations.

By Solution Type

By Deployment Type

By End User

.webp)

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar