Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

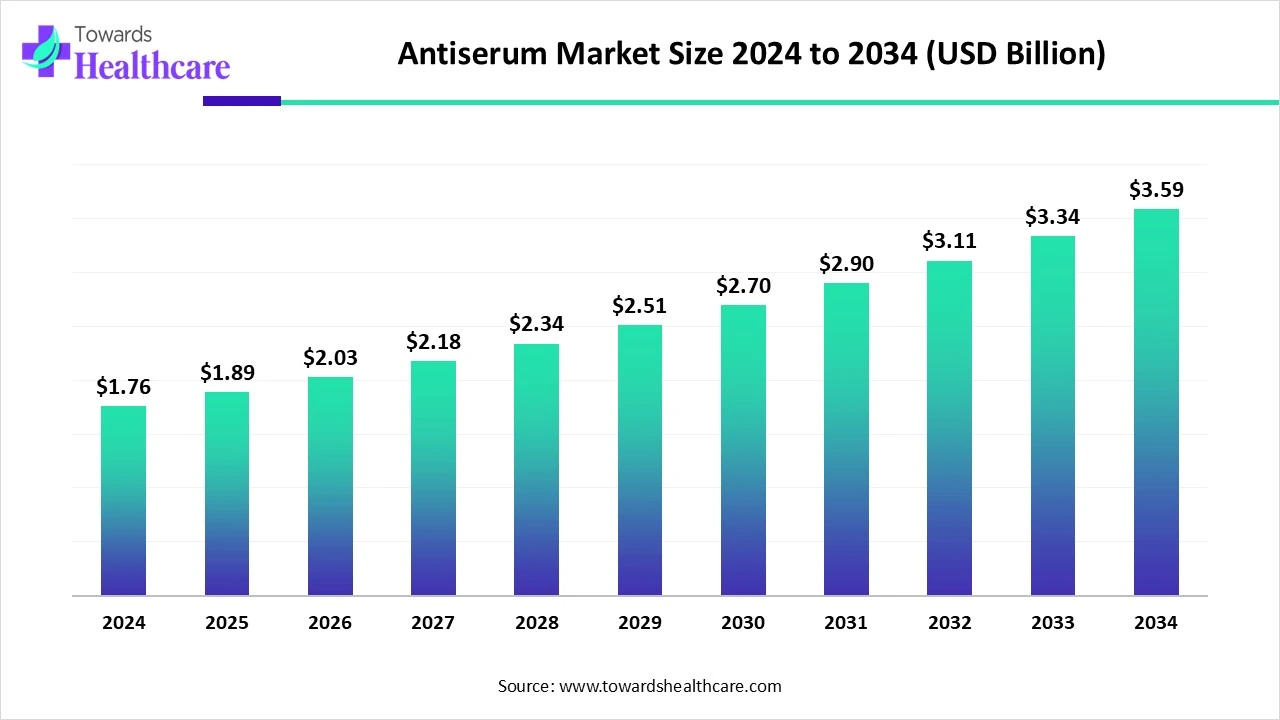

The global antiserum market size is calculated at US$ 1.89 in billion 2025, grew to US$ 2.03 billion in 2026, and is projected to reach around US$ 3.88 billion by 2035. The market is projected to expand at a CAGR of 7.44% between 2026 and 2035.

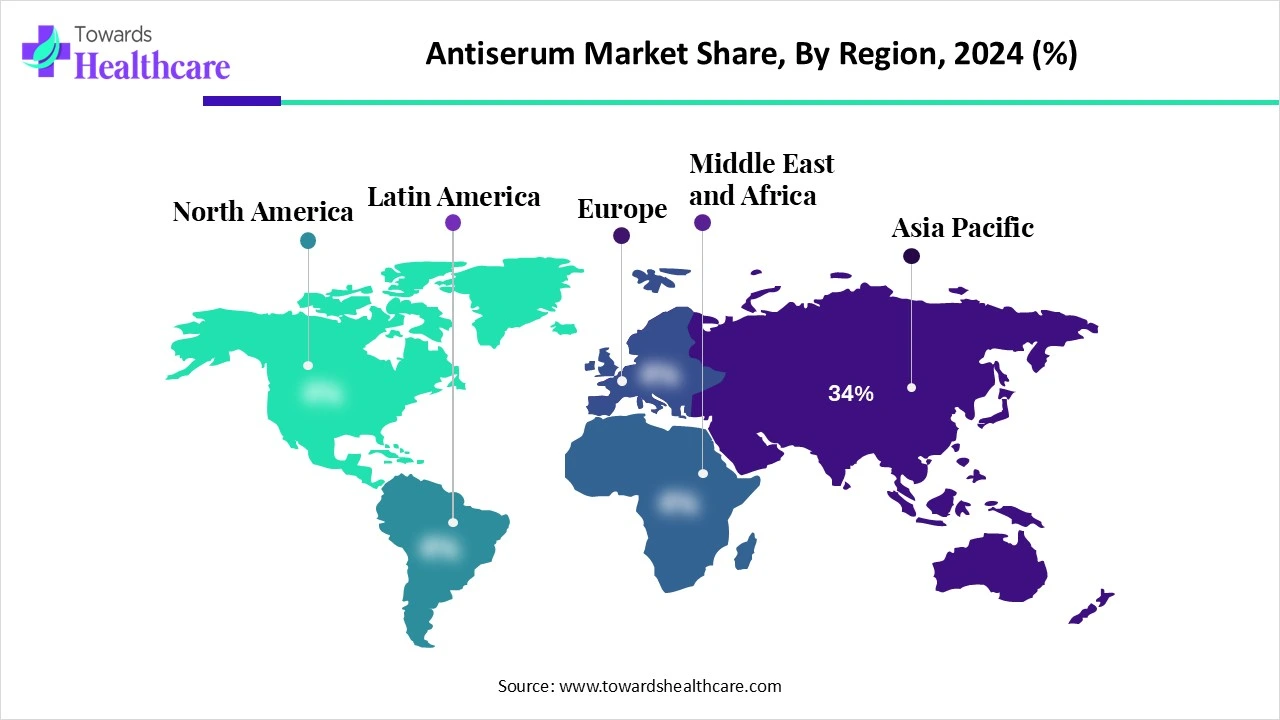

The antiserum market is expanding due to the growing infectious and zoonotic diseases, biotechnological advancements, including recombinant antibody production. North America is dominated by expanding adoption in emergency diagnostics and therapeutics. Asia Pacific is fastest fastest-growing due to the growing disease burden and increasing technological advancement in antibody production.

| Metric | Details |

| Market Size in 2026 | USD 2.03 Billion |

| Projected Market Size in 2035 | USD 3.88 Billion |

| CAGR (2025 - 2034) | 7.44% |

| Leading Region | Asia Pacific Share by 34% |

| Market Segmentation | By Product Type, By Source, By Indication, By End User, By Distribution Channel, By Region |

| Top Key Players | Bharat Serums and Vaccines Ltd., CSL Behring, Grifols S.A., Sanofi (Sanofi Pasteur), MassBiologics, Kamada Ltd., Instituto Bioclon, Microgen (Russia), Vins Bioproducts Ltd., Haffkine Bio-Pharmaceutical Corporation Ltd., Serum Institute of India, Instituto Butantan, Bioniche Life Sciences, Zoetis Inc., Boehringer Ingelheim Animal Health, Bharat Biotech, Incepta Pharmaceuticals, Bio-Rad Laboratories,Shanghai Institute of Biological Products, Techpool Bio-Pharma (part of China Biologic Products) |

Antiserum is a blood-derived biological product containing polyclonal antibodies used to provide passive immunity against specific pathogens, toxins, or venom. It is produced by immunizing humans or animals (commonly horses or sheep) with an antigen, then collecting and purifying the resulting antibodies from the serum. Antiserum is primarily used in the treatment or prophylaxis of infectious diseases (e.g., rabies, diphtheria, tetanus), envenomation (e.g., snake bites, scorpion stings), and certain autoimmune disorders. It plays a vital role in emergency and therapeutic settings, particularly in regions where vaccines or alternative treatments are limited.

Integration of AI in the antiserum drives the growth of the market as AI-driven technology allows developers to recognize and validate potential biomarkers and medicine candidates with extraordinary effectiveness, by helping traditional research strategies. AI-driven technology enables the prediction and design of antibody sequences, complementarity-determining regions (CDRs), 3D structures, epitopes, paratopes, and antigen-antibody interactions. These AI-driven revolutions address longstanding risks in antibody advancement, meaningfully enhancing speed, accuracy, and specificity in therapeutic design.

Increasing Applications of Antiserum in Pharmaceutical

Antiserum/antisera play a crucial role in diagnostics, therapeutics, and targeted drug delivery, benefiting not only infectious diseases caused by bacteria, viruses, and protozoa but also cancer, metabolic, and hormonal disorders. They are utilized in diagnosing lymphoid and myeloid malignancies, tissue typing, enzyme-linked immunosorbent assays, radioimmunoassays, microorganism serotyping, and immunological interventions such as passive antibody therapy, anti-idiotype inhibition, and magic bullet treatments with cytotoxic agents linked to anti-mouse antibodies. These applications contribute significantly to the growth of the antiserum market.

High Cost of Antiserum Production

Producing high-quality antiserum demands substantial capital expenditure on infrastructure, reagents, and skilled personnel. These costs are high due to the complex manufacturing process, which involves advanced techniques, strict regulatory compliance, costly raw materials, and major infrastructure investments. This complexity limits the growth of the antiserum market.

Increasing Innovation in Advanced Antiserum Production Technology

Innovations and emerging trends are boosting the effectiveness and expanding the use of therapeutic antibodies. From bispecific antibodies and new engineering strategies to the integration of AI and personalized medicine, the field is changing quickly. Real-time data analysis and cloud-based collaboration are becoming standard, and antibody discovery LIMS and platforms are on track to reach new heights of efficiency and innovation. These developments will help researchers address complex biological challenges, such as designing antibodies for difficult targets or creating multi-specific biologics, thereby opening opportunities for growth in the antiserum market.

Why the Polyvalent Antiserum Segment Dominated the Market?

By product type, the polyvalent antiserum segment led the antiserum market, due to the advantage of this antiserum is the minor cost of production, in that fewer groups of horses are required, compared to the number required to produce numerous monovalent antivenoms. This replaces some monovalent AVs against snakes that cause severe, but low, incidences of envenoming. Conventional polyvalent antiserum is prepared via the immunization of horses with a combination of various basic venoms.

On the other hand, the monovalent antiserum segment is projected to experience the fastest CAGR from 2025 to 2034, as it is a type of antiserum containing one specific antigen. It is used in therapeutic applications. Monovalent antisera are also applied to the detection of specific Salmonella serotypes by reacting with their corresponding flagellar (H) and somatic (O) antigens.

Why the Animal-derived Segment Dominated the Market?

By source, the animal-derived segment is dominant in the antiserum market in 2024, as it is specifically suited to neutralising multiple antigens, toxins, and enzymes that, in humans bitten by snakes, cause coagulopathies. The animal approach is used in the treatment of diphtheria, a possibly deadly respiratory disease caused by a toxin-producing bacterium, Corynebacterium diphtheriae. The process, which harvests antibody-rich serum after injecting the diphtheria toxin in the horses, may appear antiquated, but it nonetheless saves lives.

The equine subsegment is dominated in the animal-derived segment as it is an active, wide coverage, affordable, and scalable COVID-19 treatment. It also requires shorter production time as compared to monoclonal antibody procedures. Equine serum is applied for diagnostic assays, supplementation throughout mycoplasma growth, or for the cultivation of hematopoietic stem cells and neuronal cells.

The recombinant/engineered antiserum segment is projected to grow at the fastest CAGR from 2025 to 2034, as it is characterized the rapid production and high quality. Due to the in vitro method, the production is simply scalable and takes place without animals. A significant advantage of recombinant antibodies is that they are open to rational engineering strategies to confer desired useful benefits. Current development in the sector of antibody engineering has allowed for the production of highly specific recombinant antibodies with different modifications and formats.

Why is the Envenomation Segment Dominant in the Market in 2024?

By indication, the envenomation segment led the market in 2024 due to antisera is a particular treatment for envenomation. It is composed of antibodies and used to treat certain venomous bites and stings. Antivenoms are suggested only if there is massive toxicity or a huge challenge of toxicity. The treatment is composed of immunoglobulins or immunoglobulin fragments obtained from the plasma of animals hyperimmunized with one (monospecific) or several (polyspecific) venoms.

The snakebite subsegment is dominated in the envenomation segment as antiserum boosts the immunity of the patients, and produces powerful antibodies that bind to snake venom components, allowing their immune defences to eradicate these toxins.

The infectious diseases segment is projected to experience the fastest CAGR from 2025 to 2034, as antiserums have some advantages over monoclonal antibodies, like minimum product development time and reduced costs in development and production. Antiserums are a standard option for the treatment of developing infectious diseases when other drugs are inaccessible. Antisera are significant tools to analyse the disease-causing agents. They are applied for diagnostic purposes and to cure diseases.

The rabies subsegment is the fastest growing in the infectious diseases segment as anti-rabies serum is used for post-exposure prophylaxis of rabies infection in patients after exposure to scratches, bites, or other injuries, containing mucous membrane contamination with infectious tissue, like saliva, caused by a confirmed or suspected rabid animal.

Why is the Hospitals Segment Dominant in the Market in 2024?

By end user, the hospitals segment led the market in 2024 due to it is specific treatment for envenomation, as antisera is useful in the identification of ETEC in hospital laboratories, which are capable of performing toxin testing and should be assessed in other geographical areas. An antiserum is a clear liquid serum fraction involving antibodies obtained from an immunized patient or someone exposed to a foreign substance. It is tested for its titer, which designates the relative concentration of antigen-specific antibodies existing.

On the other hand, the emergency medical services segment is projected to experience the fastest CAGR from 2025 to 2034, as antiserum has proven to be advantageous for different types of acute infections and is still generally used as emergency treatment against life-threatening diseases. For instance, human IgG preparations are the ideal standard for rabies and tetanus post-exposure prophylaxis, and are accessible as emergency treatment for anthrax.

Why is the Hospital Pharmacies Segment Dominant in the Market?

By distribution channel, the hospital pharmacies segment led the market in 2024 due to its assisting doctors and other health professionals to make drug-based decisions. Compounding medications for use in the hospital. Supporting patients to understand their drug dose and how to take it. It is a special type of health care service, which includes the art, practice, and profession of selecting, storing, preparing, compounding, and dispensing medicines and medical devices, advising patients on their safe, effective, and efficient application.

On the other hand, the online pharmacies segment is projected to experience the fastest CAGR from 2025 to 2034, as this pharmacy connects patients and essential medications, particularly for those living in remote or underserved areas. In regions where access to traditional pharmacies may be restricted, online platforms ensure that patients obtain the medications they require without having to travel long distances. This accessibility is predominantly beneficial for aging people, persons with disabilities, or those who reside in rural areas where medical resources are rare. Unlike traditional pharmacies inadequate by physical space, online pharmacies also offer a more extensive selection of medications and products.

")

Asia Pacific was dominant in the antiserum market share bby 34% in 2024, as increasing biotech investment in the APAC region, driven by a combination of influences, including high spending, targeted medicine, and development in technology. With the increasing artificial intelligence, machine learning, and advanced data analytics, scientists can analyze massive amounts of data to detect novel drug targets and develop efficient therapies, which increases the demand for antiserum, driving the growth of the market.

The China Antiserum Market Trends

China has recently increased funding in life sciences R&D, leading to more clinical trials than the other countries and approving novel discoveries by Chinese companies, which drives the growth of the market. China involves 23% of the worldwide innovative drug pipeline and leads several developments in biologics, precision medicine, and synthetic biology, increasing the demand for antiserum.

India Antiserum Market Trends

The demand for antiserum production in India is increasing due to several factors, including the increasing prevalence of chronic diseases, recent progress in biotechnology, and government initiatives encouraging medical care and research. Particularly, the rising incidence of cancer, autoimmune disorders, and cardiovascular diseases is driving the requirement for personalized therapies like monoclonal antibodies, which are a type of antiserum.

Middle East & Africa is expected to grow at the fastest CAGR in the antiserum market during the forecast period as increasing advancements of the biotech sector, driven by invention and government support, provide leadership in vaccines, bio-pharma, which drives manufacturing of improved and recombinant antiserum products. Increasing awareness of a disease and its symptoms, people are more likely to take preventive action, and go for screenings, check-ups, and tests, which leads to early diagnosis and the rising use of therapeutic solutions like antiserum.

The Saudi Arabia Antiserum Market Trends

In Saudi Arabia, increasing government funding in vaccine revolution and the huge spending of money during OWS have benefited the whole biopharmaceutical and scientific community, which increases rapid approval and adoption of advanced serum-based treatment, which drives the growth of the market.

The Iran Antiserum Market Trends

In Iran, with growing access to highly skilled talent, industry proficiency, a huge R&D culture, and biotech ecosystems in major cities. Also strong emphasis on research, development, and practical applications, Iranian institutions provide the best programs in biotechnology. These programs not only offer a solid academic foundation but also create opportunities for a broad range of career scenarios in industries like pharmaceuticals, environmental science, and agriculture, which drives the growth of the market.

Europe is estimated to be notably growing in the antiserum market during the forecast period, as increasing government support, such as novel European Biotech Act goal to ensure that the EU makes the most of the biotechnology innovation for the help society, the environment, and the economy, while making it easier to advancement and bring to market products in the all biotechnology sectors in the EU.

The German Antiserum Market Trends

Biotechnology is one of the significant economic drivers in Germany. Around 4,100 organizations are in the biotech industry, including many small and midsize companies. The dominant health tech sectors are supply and engineering (27%), research and development (19%), and professional services and consulting (12.5%), which contribute to the growth of the market.

The UK Antiserum Market Trends

In the UK, increasingly strong scientific research tradition and prestigious universities. The strong presence of advanced Institutions like the University of Oxford, the University of Cambridge, and Imperial College London is widely recognized for their noteworthy contributions to biotechnology research. The UK has the largest biotech pipeline of any biotech cluster in other region. It has an exciting tranche of companies at entirely stages of development, an enabling environment for start-up companies to develop, and is the standard place in Europe for increasing healthcare innovation.

North America is expected to grow significantly in the antiserum market during the forecast period, due to the presence of advanced healthcare infrastructure. The growing R&D activities and healthcare investments are also increasing the advancements of the antiserum innovations. Additionally, the growing government initiatives and increasing infectious diseases are enhancing the market growth.

U.S. Antiserum Market Trends

The growing healthcare investments in the U.S. are increasing the development and innovations of the antiserum products. Their growing applications in the research, treatment, and diagnostic is also increasing their use. At the same time, the increasing incidence of infectious diseases is also increasing their demand.

South America is expected to grow significantly in the antiserum market during the forecast period, due to expanding healthcare infrastructure. The growing incidence of snake bites is also increasing the demand for antiserums. Moreover, the growing R&D activities and development of new diagnostic techniques are also increasing its use, which is promoting the market growth.

Brazil Antiserum Market Trends

The growing incidence of venomous bites across Brazil is increasing the use of antiserums, which is driving their production rates. At the same time, increasing government health initiatives are also increasing their use. Furthermore, the growing health awareness, healthcare investments, and R&D activities are also encouraging their innovations.

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

In July 2025, Dr. Cyrus S. Poonawalla, Chairman, Serum Institute of India, stated, “Providing advanced healthcare and support to children with special requirements is a cause very close to my heart. I feel deeply gratified to inaugurate this novel school dedicated to children with hearing impairments. As an organization, we aim to effectively utilize our resources to offer the standard preventive solutions to the population, including children. This advanced building encompassing advanced infrastructure and modern facilities for the hearing-impaired children is a step towards the same direction."

By Product Type

By Source

By Indication

By End User

By Distribution Channel

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar