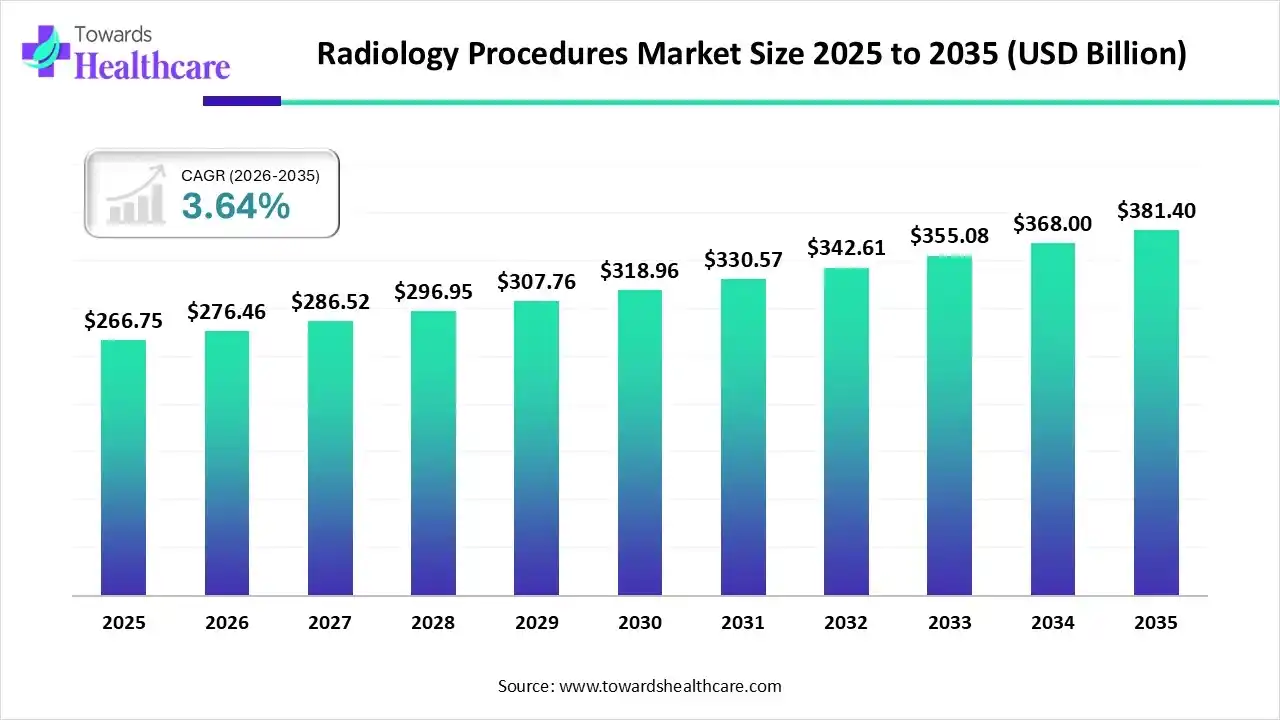

The global radiology procedures market size was estimated at USD 266.75 billion in 2025 and is predicted to increase from USD 276.46 billion in 2026 to approximately USD 381.4 billion by 2035, expanding at a CAGR of 3.64% from 2026 to 2035.

")

The growing disease burden globally is increasing the demand for various radiology procedures. Additionally, expanding innovations, AI integration, screening programs, health awareness, and launches are also promoting the market growth.

The radiology procedures market is fuelled by growing chronic diseases and the integration of AI into the diagnostic workflow. The radiology procedures encompass the medical imaging techniques used for diagnosis, monitoring, and treatment planning. These procedures help in the detection of fractures, tumors, injuries, and other organ abnormalities, which is increasing their use in preventive care and personalized treatment planning.

The use of AI in radiology procedures is increasing as it helps in detecting tumors, lesions, and fractures, along with their quantification. Its enhanced diagnostic accuracy and predictive analytics help in assessing disease progression with reduced errors. Its integration with radiology systems enhances the imaging quality, scan times, and quantitative assessment, where it also helps in personalized treatment planning.

The growing demand for preventive care and increasing chronic disease burden is driving the shift from inpatient to outpatient settings for faster and more affordable services, which is increasing the use of diagnostic centers for various radiology procedures.

The growing shift towards remote healthcare is increasing the adoption of teleradiology and cloud solutions, which are enhancing access to expertise, advanced diagnostics, and overcoming specialist shortages.

In order to offer superior resolution, point-of-care imaging, enhanced workflow automation, and improve radiologist productive, the companies are developing portable, advanced imaging solutions and hybrid systems.

| Table | Scope |

| Market Size in 2026 | USD 276.46 Billion |

| Projected Market Size in 2035 | USD 381.4 Billion |

| CAGR (2026 - 2035) | 3.64% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Modality, By End Use, By Region |

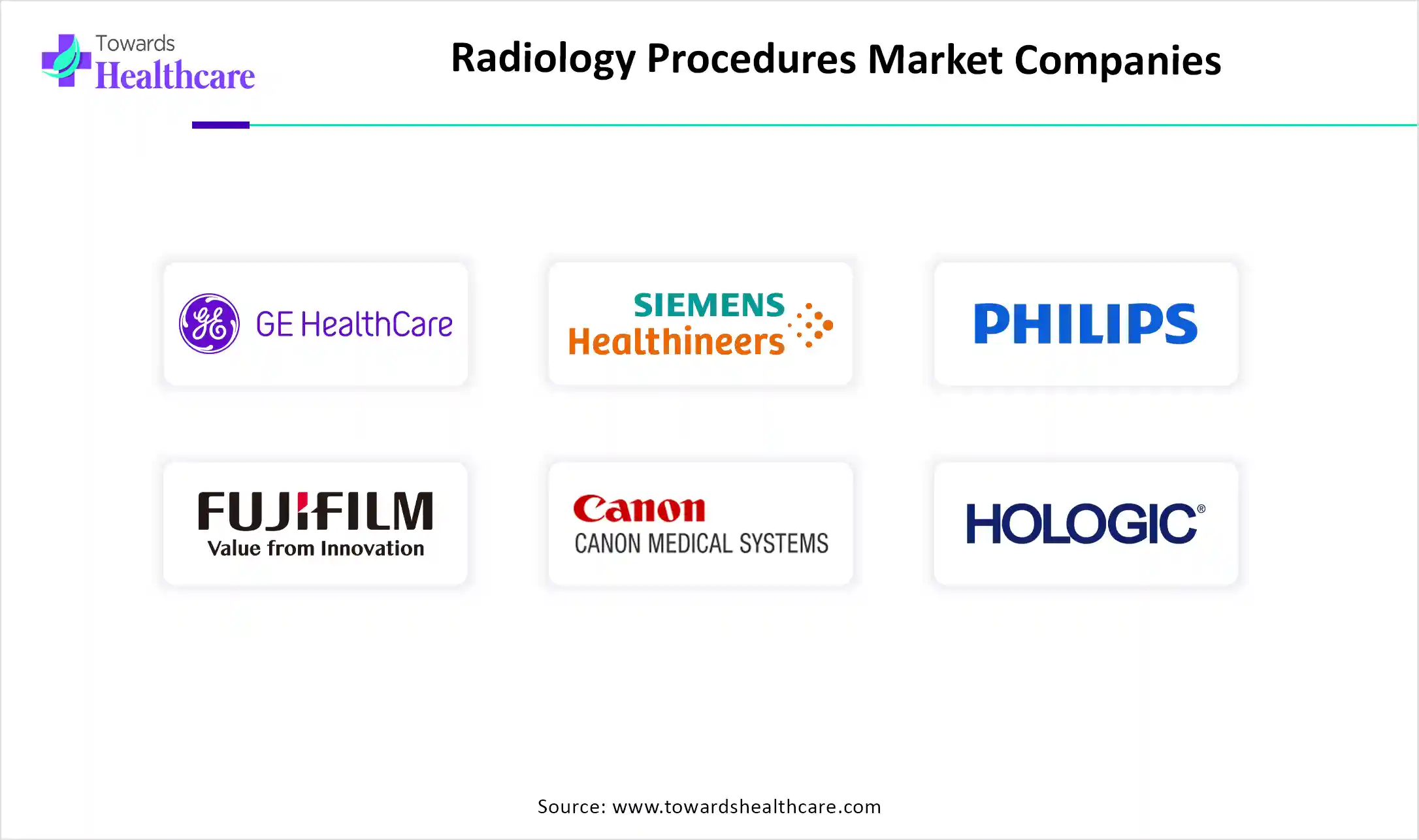

| Top Key Players | GE HealthCare, Siemens Healthineers, Koninklijke Philips N.V., Fujifilm Holdings, Canon Medical Systems, Hologic, Inc., Apollo Hospitals Radiology Network, RadNet, Inc. |

Which Modality Type Segment Held the Dominating Share of the Radiology Procedures Market in 2025?

The X-ray segment held the dominating share of the market in 2025, due to affordability and widespread availability. They also provided faster imaging, which increased their use in emergency situations. They were also utilized for routine checkups for effective detection of fractures and dental imaging, where the growth in the screening programs also increased their use for chest x-rays.

Computed Tomography

The computed tomography segment is expected to show the highest growth during the upcoming years, due to growing chronic diseases like cancer, neurological disorders, and cardiovascular diseases. Their rapid diagnosis is increasing their use in the detection of strokes, traumatic injuries, tumors, and internal bleeding. Additionally, increasing technological advancements are also driving their innovations.

What Made Hospitals the Dominant Segment in the Radiology Procedures Market in 2025?

The hospitals segment registered its dominance over the market in 2025, due to growth in the patient volume. The growth in chronic disease burden also increased the use of various radiology procedures to handle the inpatients, outpatients, and emergency cases. The presence of multiple departments and well-developed infrastructures, along with reimbursement policies, also attracted the patients.

Diagnostic Imaging Centers

The diagnostic imaging centers segment is expected to witness the fastest growth during the predicted time, due to the growing number of outpatients. Their affordable imaging services and short waiting time are also increasing their acceptance rates. Moreover, the presence of advanced technologies and expanding disease screening programs is also increasing their use to leverage various radiology procedures.

North America dominated the radiology procedures market in 2025, due to the presence of a well-developed healthcare infrastructure, which increased the use of radiological procedures to deal with the growing chronic diseases. Growth in healthcare investments also increased the early adoption of new technologies, which encouraged their innovations, which further contributed to the market growth.

U.S. Market Trends

The U.S. consists of a wide range of radiology systems due to the presence of advanced healthcare infrastructure, where the growing electronic investment and screening programs are also increasing their adoption rates. Increasing lifestyle changes, chronic diseases, and technological innovations are also encouraging their use.

Asia Pacific is expected to host the fastest-growing radiology procedures market during the forecast period, due to growing healthcare investments, which are increasing the adoption of various advanced technologies. The growing disease burden and geriatric population are also increasing the use of radiology procedures, where the expanding medical tourism and health awareness are also increasing their demand, enhancing the market growth.

China Market Trends

The prevalence of a large population in China is increasing the incidence of chronic disease, which is driving the demand for radiology procedures. Rapid healthcare expansion is also increasing the adoption of advanced radiology systems, where the growing government initiatives and medical tourism are also increasing their innovations and adoption rates.

Europe is expected to grow significantly in the radiology procedures market during the forecast period, due to the growing geriatric population and advanced healthcare infrastructure, which are encouraging the use of radiology procedures. Increasing focus on preventive care and government support is also increasing their adoption and innovation, promoting market growth.

UK Market Trends

The growing geriatric population in the UK is increasing the use of radiology procedures for the detection of various diseases. Additionally, increasing screening programs, government funding, and technological advancements are also increasing their use and innovations. They are also being preferred as a preventive care option for early disease diagnosis.

| Companies | Headquarters | Solutions |

| GE HealthCare | Chicago, U.S. | MRI, CT, PET/CT, interventional image-guided surgery, and 3D mammography |

| Siemens Healthineers | Forchheim, Germany | Advanced neuro and vascular interventions, digital radiography, PET/CT, oncology-focused imaging, and MRI |

| Koninklijke Philips N.V. | Amsterdam, Netherlands | Image-guided therapy, cloud-based AI-integrated diagnostics, cardiology and peripheral vascular interventions, and ultrasound |

| Fujifilm Holdings | Tokyo, Japan | Digital radiography, ultrasound, AI-powered image enhancement systems, digital mammography, and ultrasound |

| Canon Medical Systems | Otawara, Japan | High-resolution CT, MRI, interventional angiography systems, and diagnostic ultrasound |

| Hologic, Inc. | Marlborough, U.S. | Specialized women’s health imaging, like bone densitometry and digital breast tomosynthesis |

| Apollo Hospitals Radiology Network | Chennai, India | Tertiary-care imaging, including cardiac CT angiography, nuclear medicine, PET-CT, and functional MRI |

| Vijaya Diagnostic Centre | Hyderabad, India | 3T MRI, oncology-oriented PET-CT, multi-slice CT scans, and high-field cardiology imaging |

| Krsnaa Diagnostics | Pune, India | High volume public-private partnership (PPP) imaging, including MRI, large-scale teleradiology reporting, and CT |

| RadNet, Inc. | Los Angeles, U.S. | Comprehensive outpatient diagnostic imaging, including PET, X-ray, MRI, and CT |

By Modality

By End Use

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar