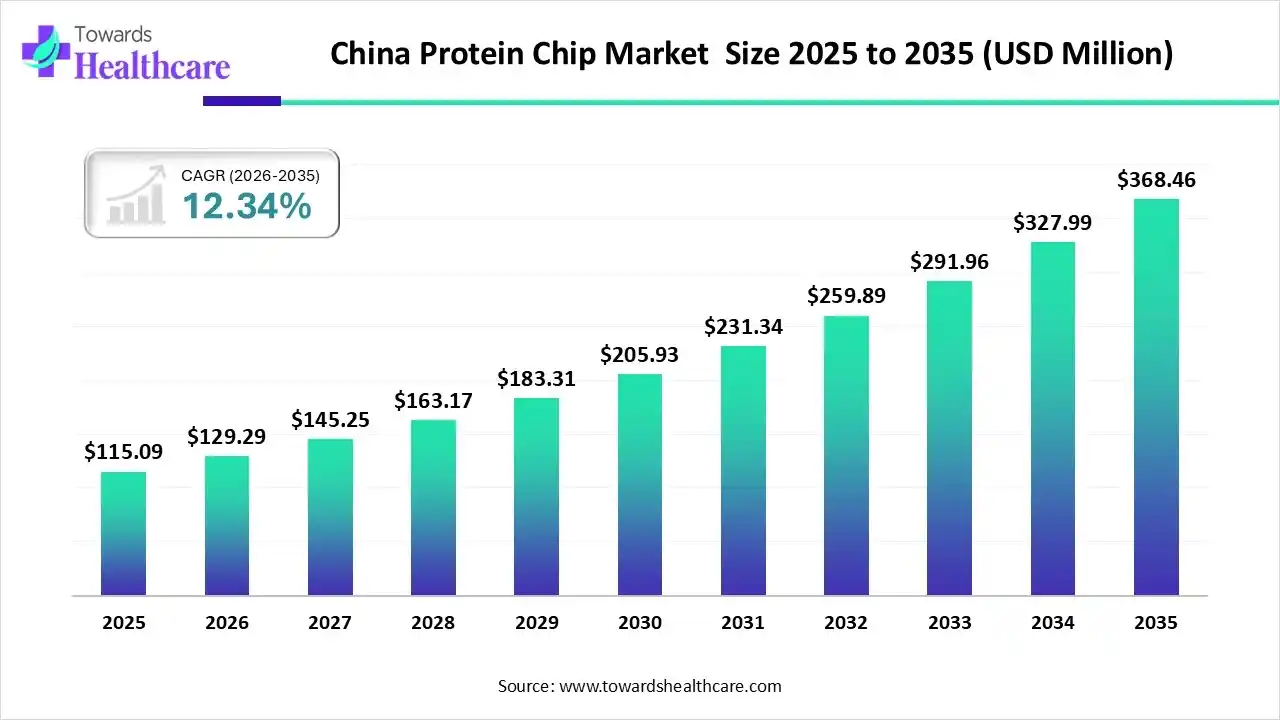

Revenue, 2025

USD 115.09 million

Forecast, 2035

USD 368.46 Million

China Protein Chip Market Trends for 2026

The china protein chip market is projected to reach USD 368.46 million by 2035, growing from USD 115.09 million in 2025, at a CAGR of 12.34% during the forecast period from 2025 to 2035.

")

China leads the Asia-Pacific protein chip market due to strong government support for biotechnology, expanding research infrastructure, and increasing investments in proteomics and personalized medicine. The presence of leading academic institutions, local biotech firms, and collaborations with global pharmaceutical companies further enhances innovation, production capacity, and adoption of protein chip technologies.

Asia Pacific is the fastest-growing region in the protein chip market, driven by increasing investments in biotechnology research, expanding healthcare infrastructure, and rising adoption of advanced diagnostic technologies. Growing government funding, academic collaborations, and the presence of emerging biotech startups further drive innovation and market expansion across the region.

Key Takeways

- The Protein Chip Market is set to grow from US$ 2.36 billion in 2025 to US$ 4.98 billion by 2035, at a CAGR of 7.78%.

- China is a major contributor to the North America protein chip market by 4.8%.

- Planar Protein Microarrays lead the platform type segment with 38% market share in 2024.

- Biomarker Discovery & Validation holds the largest application share at 30%, with Clinical Diagnostics at 25%.

- Pharmaceutical & Biotech Companies dominate the end-user segment with 34%, followed by Clinical & Diagnostic Laboratories at 18%.

- Label-based Fluorescence / Chemiluminescence Assays capture 45% of the detection chemistry market.

- Protein Chip Kits & Reagents lead the product offering segment with 36%, while Software & Data Analysis Tools grow at 18%.

- Label-Free & Biosensor Arrays and Clinical Diagnostics & Companion Diagnostics are expected to grow the fastest.

- Bead-Based / Suspension Arrays and Reverse-Phase Protein Arrays capture 10% and 8% market share, respectively.

Segments

By Platform Type

| Segments |

Shares 2025 (%) |

| Planar Protein Microarrays (glass slides, printed arrays) |

38% |

| Bead-Based / Suspension Arrays (Luminex-style, flow-based) |

10% |

| Reverse-Phase Protein Arrays (RPPA) |

8% |

| Label-Free & Biosensor Arrays (SPR, photonic crystal, nanoplasmonic) |

14% |

| Peptide Arrays & Epitope Mapping Chips |

6% |

| Other Custom / Specialty Arrays (cell-based arrays, glycan-protein arrays) |

4% |

- Planar Protein Microarrays (glass slides, printed arrays) – Dominating the market with a 38% share, these are widely used for protein analysis on solid surfaces.

- Bead-Based / Suspension Arrays (Luminex-style, flow-based) – Holding 10% of the market, these arrays use beads in suspension to detect multiple proteins simultaneously.

- Reverse-Phase Protein Arrays (RPPA) – This segment has 8% market share, using a reverse-phase method to profile proteins.

- Label-Free & Biosensor Arrays (SPR, photonic crystal, nanoplasmonic) – Growing fast, this segment captures 14% of the market by detecting proteins without labels, ideal for real-time analysis.

- Peptide Arrays & Epitope Mapping Chips – Representing 6% of the market, this segment focuses on mapping peptide interactions for understanding diseases.

- Other Custom / Specialty Arrays (cell-based arrays, glycan-protein arrays) – Taking up 4% of the market, these arrays are designed for specific research needs like cell signaling or glycan-protein studies.

By Application

| Segments |

Shares 2025 (%) |

| Biomarker Discovery & Validation |

30% |

| Drug Target Identification & Pharmacodynamics |

10% |

| Clinical Diagnostics & Companion Diagnostics |

25% |

| Immune Profiling & Vaccine Research |

8% |

| Protein–Protein Interaction & Pathway Analysis |

7% |

| Quality Control / Bioprocess Monitoring (biomanufacturing) |

5% |

| Others (agriand environmental proteomics) |

5% |

- Biomarker Discovery & Validation – Holding the largest share of 30%, this application focuses on identifying biomarkers for diseases.

- Drug Target Identification & Pharmacodynamics – With a 10% share, this application helps in discovering drug targets and studying their effects.

- Clinical Diagnostics & Companion Diagnostics – This segment holds 25%, focusing on diagnosing diseases and supporting personalized medicine.

- Immune Profiling & Vaccine Research – Representing 8%, it helps understand immune responses and assists in vaccine development.

- Protein–Protein Interaction & Pathway Analysis – With a 7% share, this application focuses on understanding protein interactions in cellular processes.

- Quality Control / Bioprocess Monitoring (biomanufacturing) – Holding 5%, it is critical for maintaining quality and consistency in biomanufacturing processes.

- Others (agri- and environmental proteomics) – Contributing 5%, this segment includes research related to agriculture and environmental proteomics.

By End User

| Segments |

Shares 2025 (%) |

| Pharmaceutical & Biotech Companies |

34% |

| Academic & Research Institutes |

12% |

| Clinical & Diagnostic Laboratories |

18% |

| Contract Research Organizations (CROs) |

15% |

| Industrial / Bioprocess QC Users |

10% |

| Other (agriculture, food safety labs) |

11% |

- Pharmaceutical & Biotech Companies – Dominating with 34%, these companies are the largest users of protein chips for drug discovery and development.

- Academic & Research Institutes – Holding 12%, these institutions use protein chips for research in various biological fields.

- Clinical & Diagnostic Laboratories – With 18%, this segment applies protein chips for clinical diagnostics and patient testing.

- Contract Research Organizations (CROs) – Having 15% market share, these organizations conduct outsourced research services for pharma and biotech companies.

- Industrial / Bioprocess QC Users – With a 10% share, these users focus on quality control in industrial and biomanufacturing processes.

- Other (agriculture, food safety labs) – Contributing 11%, this segment includes agricultural research and food safety testing.

By Detection Chemistry / Assay Type

| Segments |

Shares 2025 (%) |

| Label-based Fluorescence / Chemiluminescence Assays |

45% |

| Enzyme-Linked / Colorimetric Assays |

12% |

| Label-free (SPR, interferometry, photonic) Detection |

15% |

| Antibody/Antigen Capture Sandwich Assays |

10% |

| Affinity / Binding Kinetics Assays |

8% |

| Other (lectin-binding, glycoprotein-specific assays) |

10% |

- Label-based Fluorescence / Chemiluminescence Assays – Holding 45%, this is the dominant detection method using labeled molecules to emit signals for protein detection.

- Enzyme-Linked / Colorimetric Assays – With a 12% share, these assays use color changes to detect proteins, often in simpler setups.

- Label-free (SPR, interferometry, photonic) Detection – Growing at a fast rate with 15%, this label-free detection allows real-time monitoring of protein interactions.

- Antibody/Antigen Capture Sandwich Assays – This method, holding 10% of the market, uses antibodies to capture proteins for detection.

- Affinity / Binding Kinetics Assays – With 8% share, this assay type measures the strength and duration of protein bindings.

- Other (lectin-binding, glycoprotein-specific assays) – Contributing 10%, this segment covers specialized assays for glycoprotein and lectin interactions.

By Product / Offering

| Segments |

Shares 2025 (%) |

| Protein Chip Kits & Reagents |

36% |

| Array Substrates & Slides |

15% |

| Detection Instruments & Scanners |

10% |

| Consumables (antibodies, buffers, blocking reagents) |

12% |

| Software & Data Analysis Tools |

18% |

| Contract Services / Assay Development |

9% |

- Protein Chip Kits & Reagents – Dominating with 36%, these kits and reagents are essential for conducting protein chip experiments.

- Array Substrates & Slides – Holding 15%, these provide the surface where proteins are arrayed for analysis.

- Detection Instruments & Scanners – With a 10% share, these instruments are used to read protein chip results.

- Consumables (antibodies, buffers, blocking reagents) – Contributing 12%, these are the supporting materials used in protein chip testing.

- Software & Data Analysis Tools – Growing rapidly with 18%, these tools help analyze complex data generated from protein chip experiments.

- Contract Services / Assay Development – Holding 9%, this segment offers outsourced services for assay development and protein chip applications.

Key Players

- PerkinElmer Inc.

- BioRad Laboratories

- Illumina, Inc.

- RayBiotech Life, Inc.

- Arrayit Corporation

- Danaher Corporation

Segments Covered in the Report

By Platform Type

- Planar Protein Microarrays (glass slides, printed arrays)

- Bead-Based / Suspension Arrays (Luminex-style, flow-based)

- Reverse-Phase Protein Arrays (RPPA)

- Label-Free & Biosensor Arrays (SPR, photonic crystal, nanoplasmonic)

- Peptide Arrays & Epitope Mapping Chips

- Other Custom / Specialty Arrays (cell-based arrays, glycan-protein arrays)

By Application

- Biomarker Discovery & Validation

- Drug Target Identification & Pharmacodynamics

- Clinical Diagnostics & Companion Diagnostics

- Immune Profiling & Vaccine Research

- Protein–Protein Interaction & Pathway Analysis

- Quality Control / Bioprocess Monitoring (biomanufacturing)

- Others (agri- and environmental proteomics)

By End User

- Pharmaceutical & Biotech Companies

- Academic & Research Institutes

- Clinical & Diagnostic Laboratories

- Contract Research Organizations (CROs)

- Industrial / Bioprocess QC Users

- Other (agriculture, food safety labs)

By Detection Chemistry / Assay Type

- Label-based Fluorescence / Chemiluminescence Assays

- Enzyme-Linked / Colorimetric Assays

- Label-free (SPR, interferometry, photonic) Detection

- Antibody/Antigen Capture Sandwich Assays

- Affinity / Binding Kinetics Assays

- Other (lectin-binding, glycoprotein-specific assays)

By Product / Offering

- Protein Chip Kits & Reagents

- Array Substrates & Slides

- Detection Instruments & Scanners

- Consumables (antibodies, buffers, blocking reagents)

- Software & Data Analysis Tools

- Contract Services / Assay Development

Protein Chip Market Quick Stats and Facts

| Key Elements |

Scope |

| Market revenue in 2026 |

USD 129.29 Million |

| Market revenue in 2035 |

USD 368.46 Million |

| Growth Rate (2025 - 2035) |

12.34% |

| Historical Data |

2020 - 2023 |

| Base Year |

2025 |

| Forecast Period |

2026 - 2035 |

| measurable Values |

USD Millions/Units/Volume |

| Market Segmentation |

By Platform Type, By Application, By End User, By Detection Chemistry / Assay Type, By Product / Offering |

| Key Players |

PerkinElmer Inc., BioRad Laboratories, Illumina, Inc., RayBiotech Life, Inc., Arrayit Corporation, Danaher Corporation |