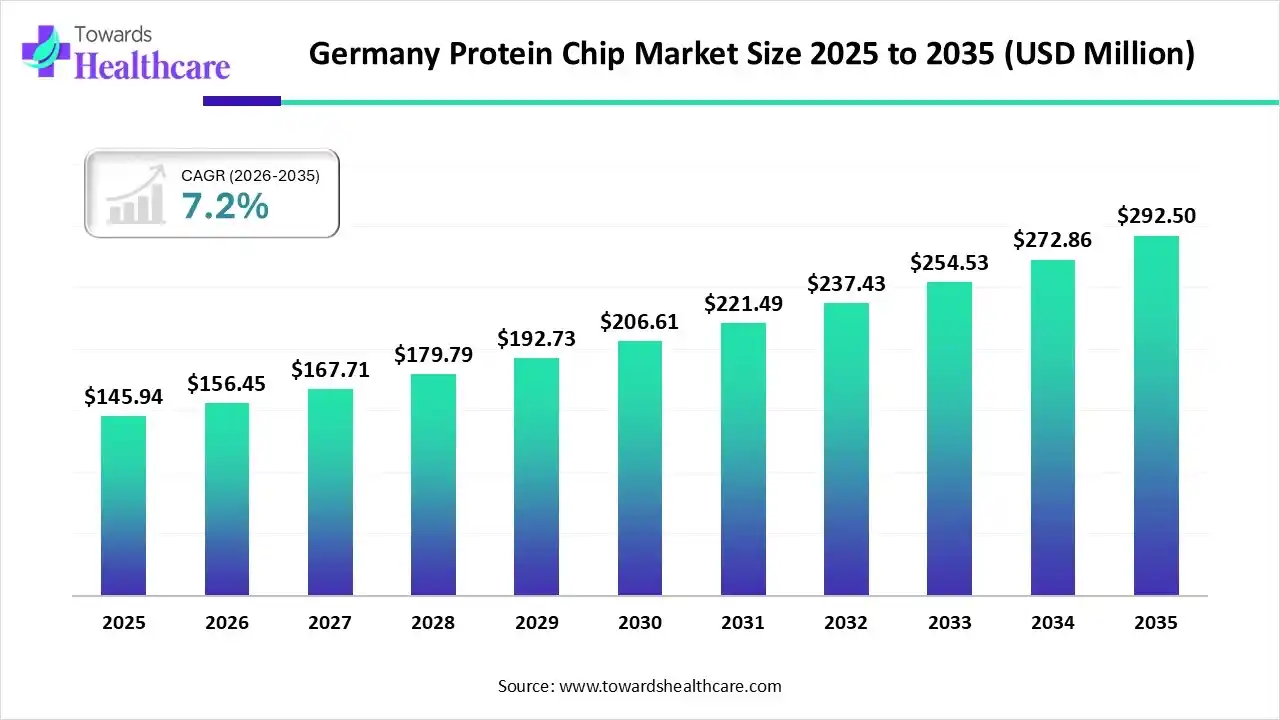

The germany protein chip market is expected to increase from USD 145.94 million in 2025 to USD 292.50 million by 2035, growing at a CAGR of 7.20% throughout the forecast period from 2025 to 2035.

Germany is a major contributor to the European protein chip market due to its strong biotechnology and pharmaceutical sectors, extensive research infrastructure, and high investment in life sciences innovation. The country’s focus on proteomics, personalized medicine, and advanced diagnostics, supported by government and academic collaborations, drives significant demand for protein chip technologies. Additionally, the presence of leading research institutions and biotech companies fosters continuous innovation and market growth.

The growth of the market in Europe is primarily driven by increasing investments in proteomics research, rising adoption of personalized and precision medicine, and a strong focus on early disease detection. Supportive government initiatives and funding for biomarker discovery and clinical diagnostics further boost market expansion. Additionally, the presence of advanced research infrastructure, collaborations between academic institutions and biotechnology companies, and growing demand for efficient diagnostic tools contribute to the region’s market growth.

| Segments | Shares 2025 (%) |

| Planar Protein Microarrays | 38% |

| Bead-Based / Suspension Arrays | 20% |

| Reverse-Phase Protein Arrays (RPPA) | 10% |

| Label-Free & Biosensor Arrays | 18% (highest growth) |

| Peptide Arrays & Epitope Mapping Chips | 7% |

| Other Custom / Specialty Arrays | 7% |

| Segments | Shares 2025 (%) |

| Biomarker Discovery & Validation | 30% |

| Drug Target Identification & Pharmacodynamics | 20% |

| Clinical Diagnostics & Companion Diagnostics | 25% (highest growth) |

| Immune Profiling & Vaccine Research | 10% |

| Protein–Protein Interaction & Pathway Analysis | 5% |

| Quality Control / Bioprocess Monitoring | 5% |

| Others | 5% |

| Segments | Shares 2025 (%) |

| Pharmaceutical & Biotech Companies | 34% |

| Academic & Research Institutes | 15% |

| Clinical & Diagnostic Laboratories | 20% (highest growth) |

| Contract Research Organizations (CROs) | 10% |

| Industrial / Bioprocess QC Users | 10% |

| Other | 11% |

| Segments | Shares 2025 (%) |

| Label-based Fluorescence / Chemiluminescence Assays | 45% |

| Enzyme-Linked / Colorimetric Assays | 10% |

| Label-free (SPR, interferometry, photonic) Detection | 25% (highest growth) |

| Antibody/Antigen Capture Sandwich Assays | 5% |

| Affinity / Binding Kinetics Assays | 10% |

| Other | 5% |

| Segments | Shares 2025 (%) |

| Protein Chip Kits & Reagents | 36% |

| Array Substrates & Slides | 15% |

| Detection Instruments & Scanners | 10% |

| Consumables | 7% |

| Software & Data Analysis Tools | 20% (highest growth) |

| Contract Services / Assay Development | 12% |

By Platform Type

By Application

By End User

By Detection Chemistry / Assay Type

By Product / Offering

| Key Elements | Scope |

| Market revenue in 2026 | USD 156.45 Million |

| Market revenue in 2035 | USD 292.50 Million |

| Growth Rate (2025 - 2035) | 7.20% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Platform Type, By Application, By End User, By Detection Chemistry / Assay Type, By Product / Offering |

| Key Players | PerkinElmer Inc., BioRad Laboratories, Illumina, Inc., RayBiotech Life, Inc., Arrayit Corporation, Danaher Corporation |

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar