")

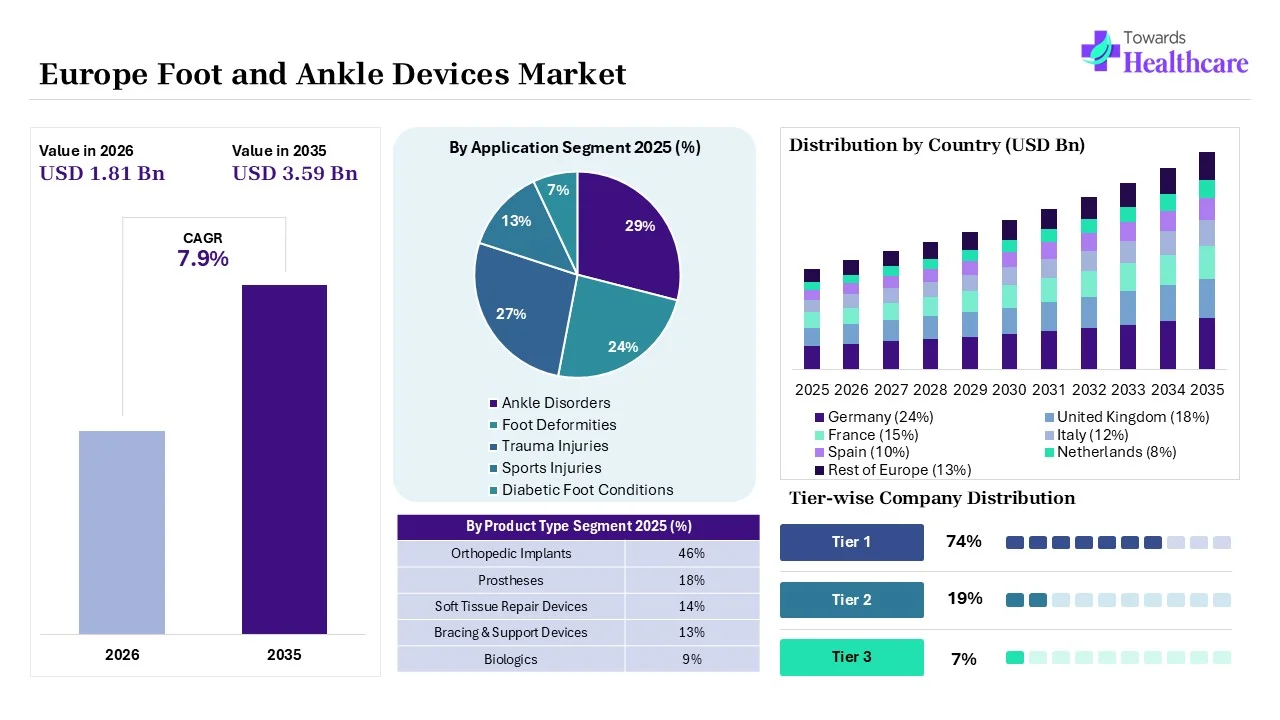

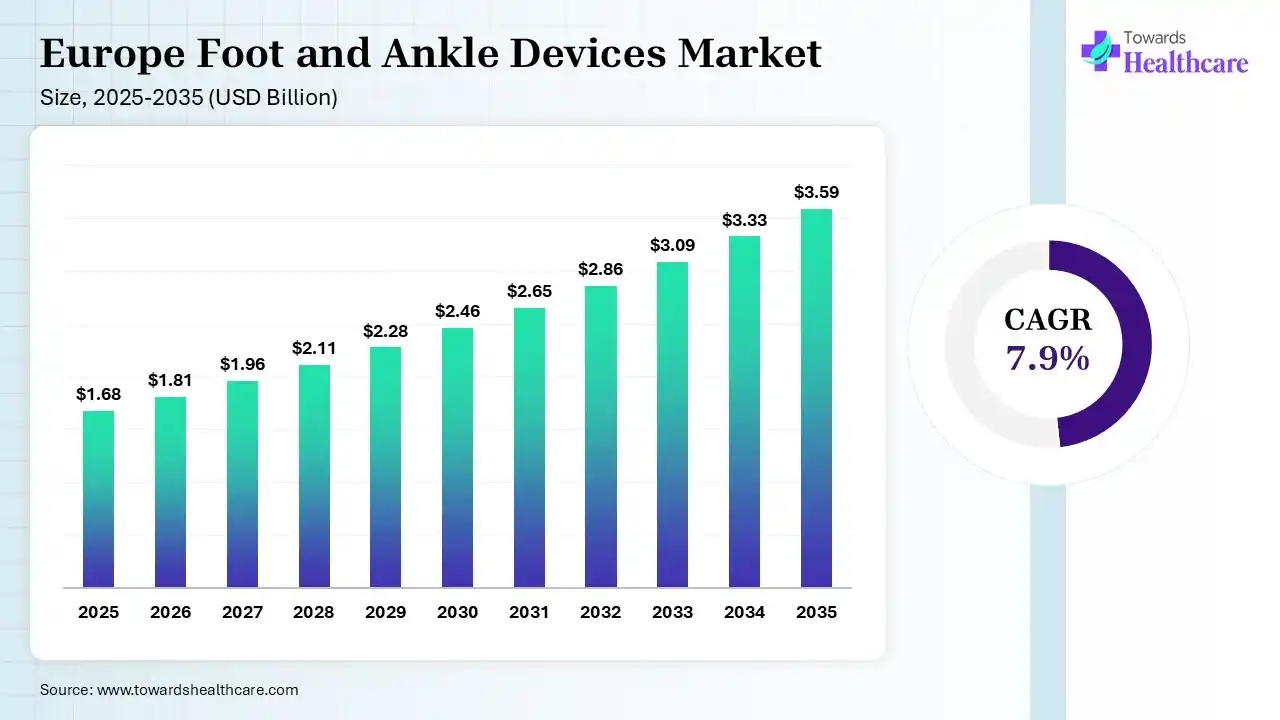

The Europe foot and ankle devices market size reached US$ 1.68 billion in 2025 and is anticipate to increase to US$ 1.81 billion in 2026. By 2035, the market is forecasted to achieve a value of around US$ 3.59 billion, growing at a CAGR of 7.9%.

")

Foot and ankle devices are being developed as a process of preventing people with sensory perception loss from sustaining a fall. This tool is designed to relieve pain related to different foot and ankle conditions. They comprise everything from shoe inserts and ankle braces to custom tools. A foot and ankle specialist recommends trying an over-the-counter orthotic device for patients who have mild symptoms related to their condition. Orthotics support, prevent, or delay the requirement for more invasive treatment, such as surgery.

Foot and ankle strategies are less edge-supportive apparel that offers soft tissue protection, bone or joint stability, and control of body gesture. Orthotics play a significant role in the nonoperative management of foot and ankle pathology. The type of orthotic requirement should be specific for the underlying bony or ligamentous pathology to offer appropriate functional support. Knee measures lead the European joint replacement industry, as the continent's high and increasing prevalence of knee osteoarthritis is linked to aging.

AI-driven technology is increasingly used for interpreting healthcare imaging and making healthcare predictions. AI-based technology remains relatively advanced in foot and ankle surgery as compared to other orthopaedic regions, such as the hip and knee. These AI-driven models are significant for progressing foot and ankle technology, as they support surgeons in accurately predicting long-term results for patients with foot and ankle conditions. AI-based tools have the potential to enhance rehabilitation technology and support detailed anthropometric studies. Furthermore, AI-driven algorithms improve hospital and clinic management, enhance electronic healthcare databases, monitor patient results, and support safety events. AI-based models are advanced in nearly all orthopaedic subspecialties, involving arthroplasty, arthroscopy, cancer treatment, spinal surgery, and paediatric surgery.

Increasing Sports Injuries:

Increasing sports injuries due to overtraining, falls, and running in the wrong direction are common causes. These injuries are common muscle, bone, or soft tissue injuries that occur during physical activities. They involve sprains, strains, and cracked injuries that typically heal within weeks or months. Ankle and foot tools support the foot and ankle; they help maintain appropriate alignment and distribute weight, lessening stress on the injured parts.

Patient-Specific 3D Printing:

Recent advancement in 3D-printed PSI indicates its use in SMO that improves surgical precision and alignment and reduces surgical challenges. This technology has the potential to improve patient results and make operations more effective, accurate, and modified. 3D-printed implants in foot and ankle renovation are at the level of customization.

Next-Generation Arthroplasty:

Next-generation arthroplasty implants and healthcare tools provide many advantages, such as preserving the stability and flexibility of the joint and achieving rapid recovery, as well as potential progress in gait rehabilitation, gait assistance, and strength for consumers. Patients experience a faster rehabilitation period because of these minimally invasive techniques and well-developed materials.

| Table | Scope |

| Market Size in 2026 | USD 1.81 Billion |

| Projected Market Size in 2035 | USD 3.59 Billion |

| CAGR (2026 - 2035) | 7.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Procedures, By Application, By End User, By Material, By Region |

| Top Key Players | Enovis, DePuy Synthes, Zimmer Biomet, Smith+Nephew, Arthrex |

")

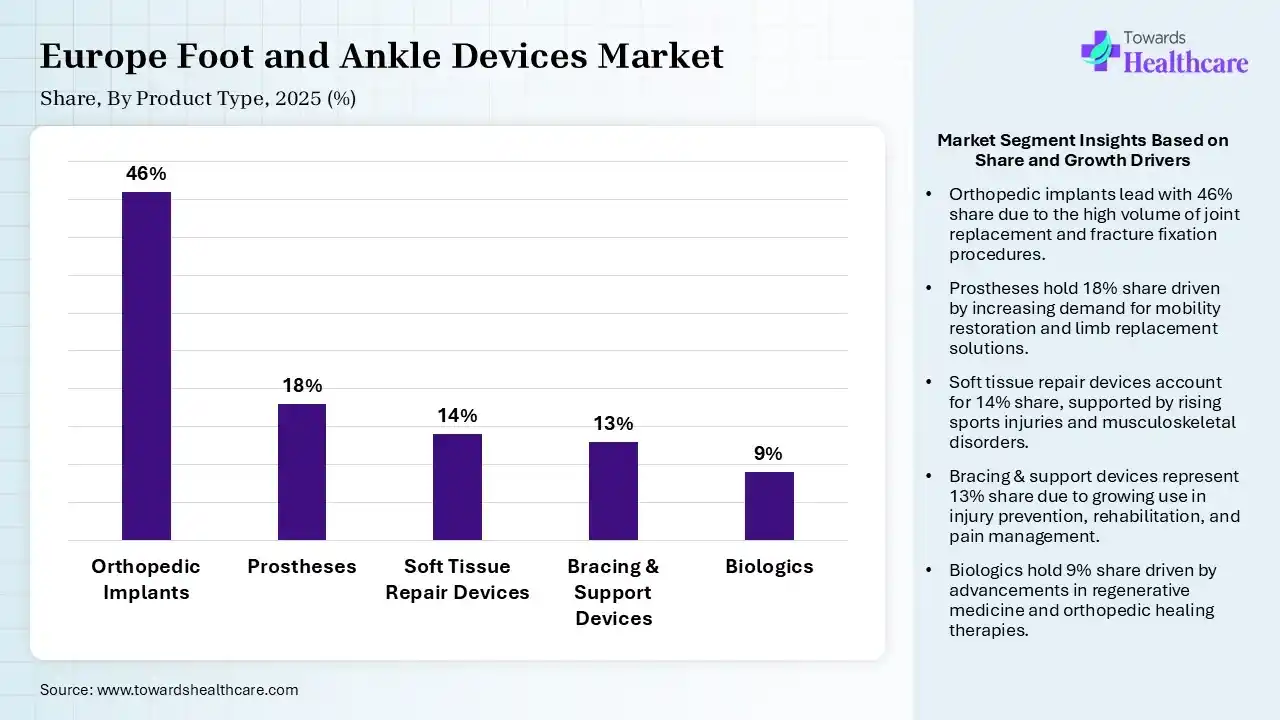

| Segment | Share 2025 (%) |

| Orthopedic Implants | 46% |

| Prostheses | 18% |

| Soft Tissue Repair Devices | 14% |

| Bracing & Support Devices | 13% |

| Biologics | 9% |

The Orthopedic Implants Segment Led the Europe Foot and Ankle Devices Market in 2025

The orthopaedic implants segment contributed the largest market share of 46% in 2025, as these types of implants and instruments are tools used in orthopaedic surgeries to restore, replace, or support damaged or injured bones, joints, and soft tissues. These implants and instruments are intended to restore function, lessen pain, and enhance the quality of life for patients with musculoskeletal conditions.

The prostheses segment held a significant share of 18% and is expected to grow at the fastest CAGR of 9.2% during the forecast period in the market, as prosthetic feet restore mobility, freedom, and quality of life after a foot amputation. A prosthetic foot supports walking more safely and comfortably for the body and helps to avoid injuries. Various types of prosthetic feet cause different complications, such as balance issues, muscle strains, or mechanical failures.

The soft tissue repair devices segment held a significant share of 14% in the Europe foot and ankle devices market, as these devices preserve a neutral hindfoot arrangement and restrict forefoot abduction. These devices are a convenient, negligibly invasive treatment that increases healing and pain relief in the technology. Soft tissue mobilisation helps to lower pain and enhance movement in the foot.

The bracing & support devices segment held a significant share of 13% in the market, as it provides proprioceptive response from the ground via the dynamic footplate and helps support calf muscles. The goal is to offer support and, at the same time, permit a normal range of motion.

")

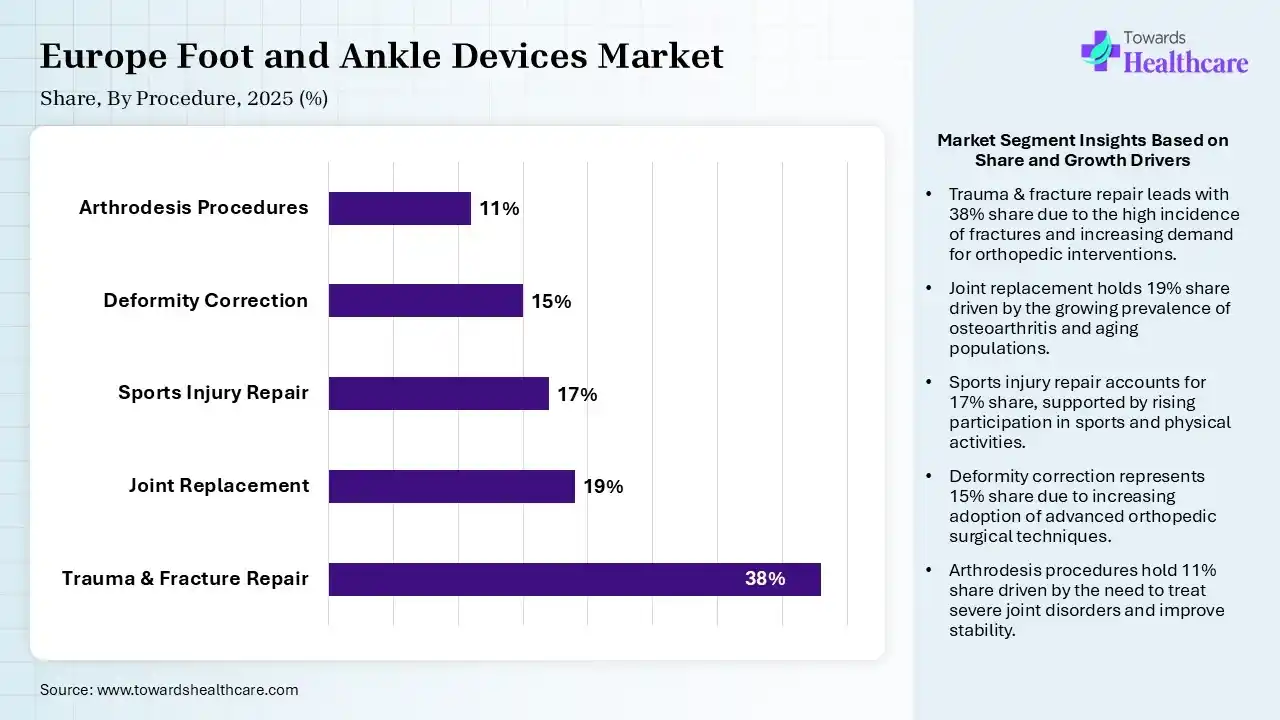

| Segment | Share 2025 (%) |

| Trauma & Fracture Repair | 38% |

| Joint Replacement | 19% |

| Sports Injury Repair | 17% |

| Deformity Correction | 15% |

| Arthrodesis Procedures | 11% |

Trauma & Fracture Repair Segment Led the Europe Foot and Ankle Devices Market in 2025

The trauma & fracture repair segment contributed the largest market share of 38%. Trauma fixation devices of orthopaedic care support millions of patients to regain their strength, mobility, and freedom after serious injuries. Trauma stabilization devices are special implants and tools to stabilize broken bones and help them heal properly. The requirement for these devices has been rising consistently over the last decade because of factors like an older population.

The joint replacement segment held a significant share of 19% of the market and is expected to grow at the fastest CAGR of 9.5 % during the forecast period. These devices significantly improved the performance of standard joint replacements in terms of precision, earlier recoveries, and better long-term outcomes. Joint replacement surgery, whether traditional or robotic, aims to restore mobility by eliminating pain and enhancing the function of the joint.

The sports injury repair segment held a significant share of 17% of the Europe foot and ankle devices market, as robotic devices ensure improved support for lower-extremity rehabilitation and aid in the recovery of physical capabilities after sports injuries. Sports therapeutic innovation provides significant advantages for patients, involving reduced pain, smaller incisions, and quicker recovery times.

The deformity correction segment held a significant share of 15% of the market. The segment maintains its significant share due to rising incidences of congenital anomalies, sports-related injuries, and age-related conditions like hallux valgus, which demand specialized surgical implants and minimally invasive osteotomy procedures.

")

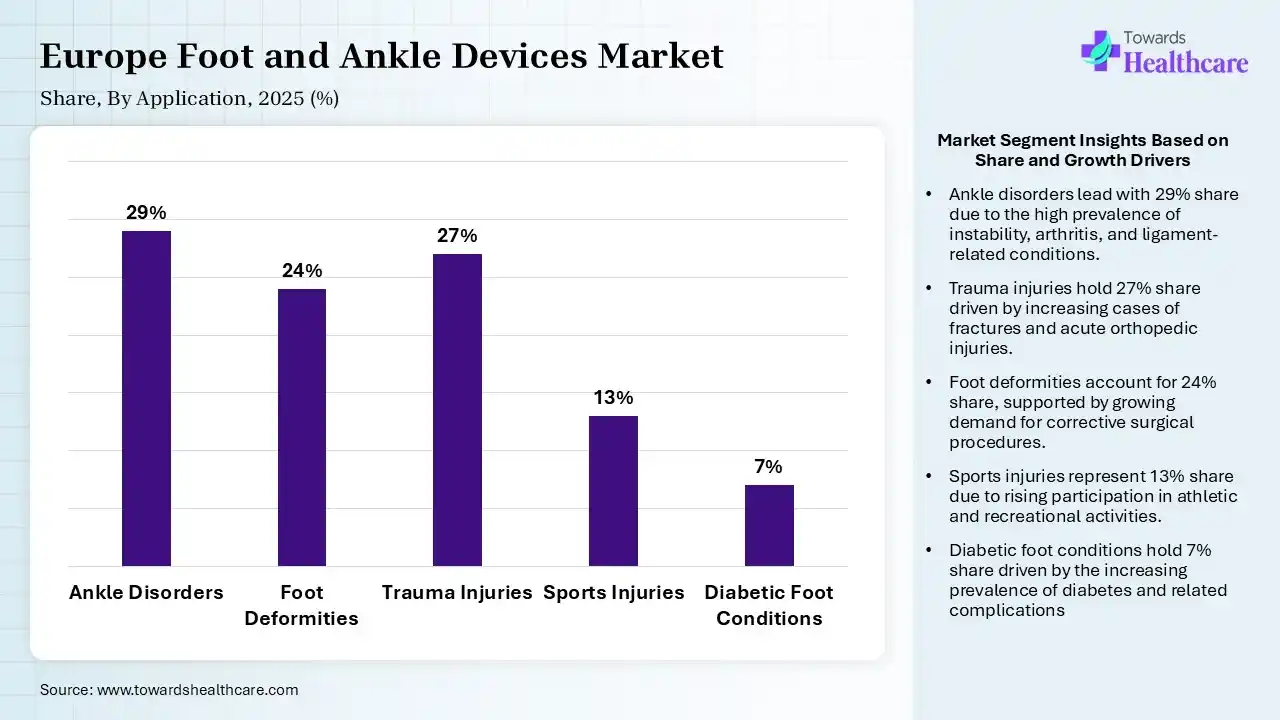

| Segment | Share 2025 (%) |

| Ankle Disorders | 29% |

| Foot Deformities | 24% |

| Trauma Injuries | 27% |

| Sports Injuries | 13% |

| Diabetic Foot Conditions | 7% |

The Ankle Disorders Segment Led the Market in 2025

The ankle disorders segment captured the dominant share of 29% of the Europe foot and ankle devices market in 2025. The high prevalence of ankle osteoarthritis, ligament injuries, chronic instability, and degenerative conditions significantly contributed to segment growth. Increasing adoption of advanced fixation systems, ankle replacement procedures, and minimally invasive surgical techniques across European healthcare facilities further supported demand. Growing awareness of early diagnosis and treatment also strengthened market expansion.

The trauma injuries segment captured 27% market share in 2025. The segment's growth was driven by the rising incidence of fractures, dislocations, and accident-related foot and ankle injuries across Europe. Increasing participation in physical activities, road traffic accidents, and an aging population prone to falls generated substantial demand for trauma fixation devices. Continuous advancements in surgical implants and improved healthcare infrastructure further supported segment development.

The foot deformities segment captured 24% market share in 2025. The growing prevalence of conditions such as bunions, hammertoes, flat feet, and congenital deformities has significantly increased the demand for corrective procedures and specialized devices. Rising awareness regarding mobility improvement and quality of life encouraged patients to seek treatment. Technological advancements in orthopedic implants and personalized treatment approaches further accelerated segment growth across the region.

The sports injuries segment held a market share of 13% in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. Increasing participation in recreational and professional sports activities is driving the occurrence of sprains, ligament tears, tendon injuries, and fractures. Growing demand for rapid recovery solutions, advanced rehabilitation programs, and innovative orthopedic devices is supporting market growth. Enhanced sports medicine facilities and greater investment in athlete healthcare are expected to further boost the segment.

")

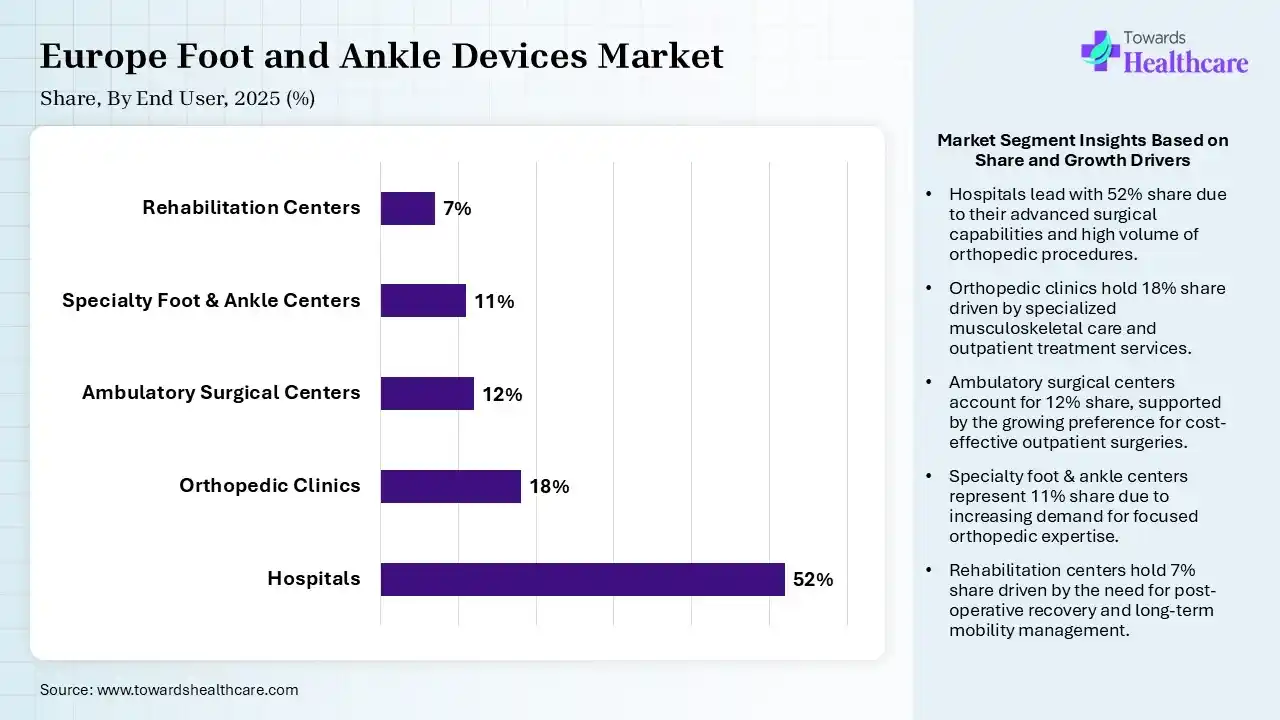

| Segment | Share 2025 (%) |

| Hospitals | 52% |

| Orthopedic Clinics | 18% |

| Ambulatory Surgical Centers | 12% |

| Specialty Foot & Ankle Centers | 11% |

| Rehabilitation Centers | 7% |

The Hospitals Segment led the Europe Foot and Ankle Devices Market in 2025

The hospitals segment held a significant share of 52% in the market. Foot and ankle devices lowered post-operative pain, negligible scarring, reduced infection rates, and a much faster return to weight-bearing. It supports refining the posture of the feet and lessens the chance of injuries.

The orthopaedic clinics segment contributed a market share of 18% in 2025, as orthotics support, align, and help feet and ankles. They support the prevention and treatment of foot deformities and other conditions involving the feet. The healthcare provider recommends giving it some time to allow the feet to adjust to this modification.

The ambulatory surgical centers segment held a significant 12% share of the Europe foot and ankle devices market, and is expected to grow at the fastest CAGR of 9.4% during the forecast period, as this center outpatient foot and ankle surgeries, providing rapid recovery, lower expenses, and lower infection challenges compared to hospital stays. Lower costs, reduced infection risks, targeted attention, and faster recovery are the advantages that draw patients and physicians to these facilities.

The specialty foot & ankle centers segment held a significant share of 11% in the market, as orthopedic foot & ankle centers treat the most multifaceted foot and ankle challenges and serve as a reliable source for surgery. Orthopedic foot and ankle physicians are able to treat patients of all ages.

")

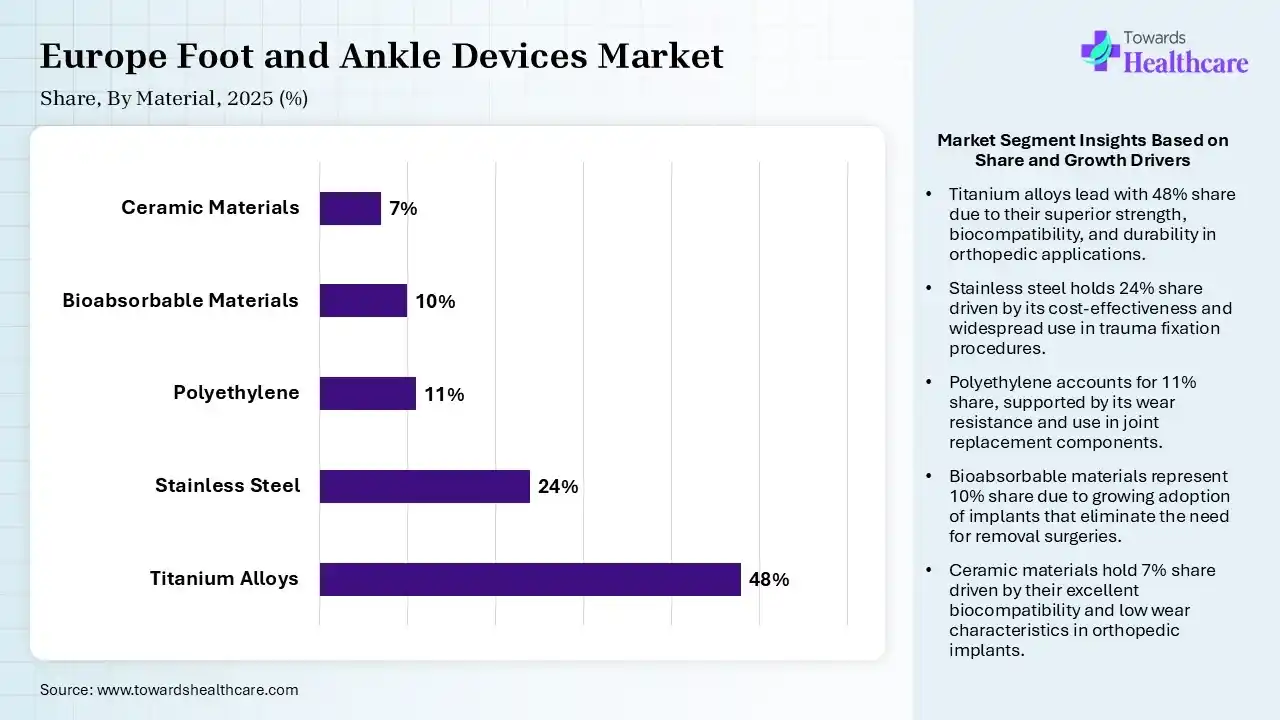

| Segment | Share 2025 (%) |

| Titanium Alloys | 48% |

| Stainless Steel | 24% |

| Polyethylene | 11% |

| Bioabsorbable Materials | 10% |

| Ceramic Materials | 7% |

The Titanium Alloys Segment led the Europe Foot and Ankle Devices Market in 2025

The titanium alloys segment contributed the largest market share of 48%, as these alloys have the highest corrosion resistance of the generally used metals, such as stainless-steel alloys and cobalt-chromium alloys for implantation. Its alloys are favoured for biomedical implants because of their massive strength, corrosion resistance, and biocompatibility. It lowers the chances of rejection and lessens challenges after surgery.

The stainless steel segment held a significant share of 24% in the market. Stainless steel orthopedic devices bear substantial loads, which is significant in trauma cases. Stainless steel is an affordable engineering material with advanced corrosion resistance.

The polyethylene segment held a significant share of 11% in the Europe foot and ankle devices market, as polyethylene has good biocompatibility, reduced wear, and easy workability. It is a type of polymer broadly used in healthcare applications, known for its variable characteristics, including wear resistance, which improves via cross-linking to potentially lessen wear rates compared to conventional polyethylene.

The bioabsorbable materials segment held a significant share of 10% in the market and is expected to grow at the fastest CAGR of 9.6% during the forecast period, as bioabsorbable materials allow the gradual transmission of stresses to the healing muscle. These devices provide the benefits of regular load transfer to the healing tissue, lessen the requirement for hardware removal, and provide radiolucency.

The Europe foot and ankle devices market is rapidly expanding, propelled by a growing elderly population and a higher prevalence of musculoskeletal disorders. Advancements in minimally invasive surgeries, personalized 3D-printed implants, and advanced biomaterials are boosting adoption across clinics. As sports-related injuries and diabetes-induced foot complications rise, demand for specialized implants, prosthetics, and fixation hardware continues climbing. This ensures faster recoveries and better patient mobility across the region.

Germany Market Trends

Germany contributed the largest market share of 24%, as this region has a progressively aging population that is extremely susceptible to deteriorating bone conditions, osteoarthritis, and various musculoskeletal disorders. Increasing rates of recreational sports participation and ordinary trauma incidents, which increase the demand for advanced foot and ankle devices.

United Kingdom Market Trends

The United Kingdom held a significant share of 18% in the Europe foot and ankle devices market, as the National Health Service (NHS) has prioritized reducing orthopaedic waiting lists, prompting an increased volume of foot and ankle technology performed yearly. This has led to massive spending on effective surgical tools and streamlined modular technology.

France Market Trends

France held a significant share of 15% in the market due to an increasing aging population, which led to a higher prevalence of degenerative diseases, osteoporosis, and joint uncertainty. High contribution of athletics and rise in trauma, road accidents, and breakages have required more robust orthopaedic fixation tools.

Netherlands Market Trends

The Netherlands held a significant share of 8% in the market and is expected to grow at the fastest CAGR of 8.2% during the forecast period, as physicians and hospitals are shifting toward less invasive technology. Significant technology, like 3D-printed, patient-driven implants and progressive fixation hardware, provides greater precision, shorter hospital stays, and rapid recovery times. Increasing revolutions like smart, IoT-enabled pneumatic walking boots are gaining traction, enabling real-time health monitoring.

R&D:

Manufacturing Processes:

Patient Services:

| Company | Headquarters | Latest Update |

| Enovis | Germany | In March 2025, Enovis, a global medical technology innovator, will feature its expanding portfolio of foot and ankle solutions. |

| DePuy Synthes | Switzerland | Johnson & Johnson is significantly making moves to separate its orthopaedics business, potentially valued at $20 billion. |

| Zimmer Biomet | Switzerland | In October 2025, Zimmer Biomet Holdings, Inc., a worldwide medical technology leader, and Paragon 28, a wholly owned subsidiary, announced the commercial launch of two innovative services for challenging foot and ankle trauma to provide surgeons with advanced tools to address challenging pilon fractures. |

| Smith+Nephew | Netherlands | In February 2026, Smith+Nephew, the worldwide medical technology company, announced it had signed an exclusive US distribution agreement with RMR Ortho to add the A’TOMIC Nitinol Fixation Scheme to the Smith+Nephew Trauma, Foot & Ankle, and Hand & Wrist portfolio. |

| Arthrex | Germany | The Arthrex MIS product portfolio continues to grow with the introduction of the minimally invasive bunionectomy system. |

In July 2025, “collaboration with Ulrich Medical marks a significant addition to our spine portfolio,” said Dean Stockwell, Osteotec Sales and Marketing Director. Ulrich’s focus on restoring spinal function through engineering excellence perfectly aligns with our commitment to offering UK surgeons high-performance, thoughtfully designed implant systems.

By Product Type

By Procedures

By Application

By End User

By Material

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar