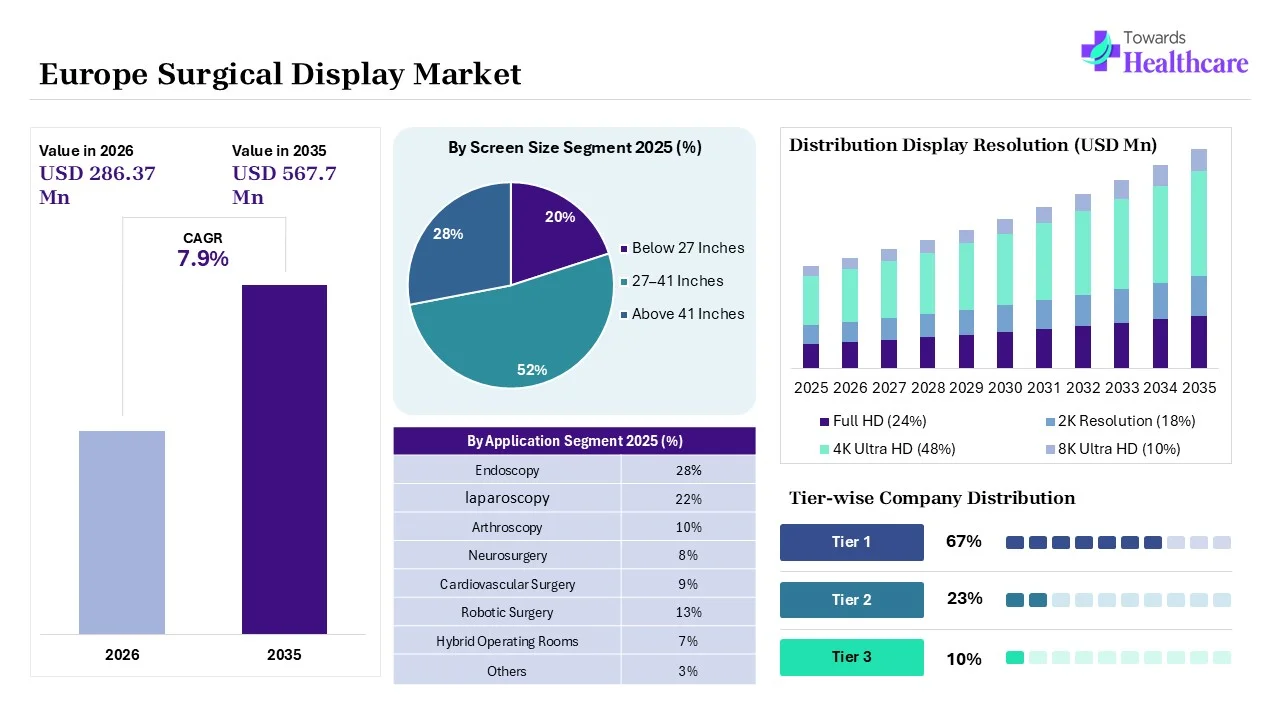

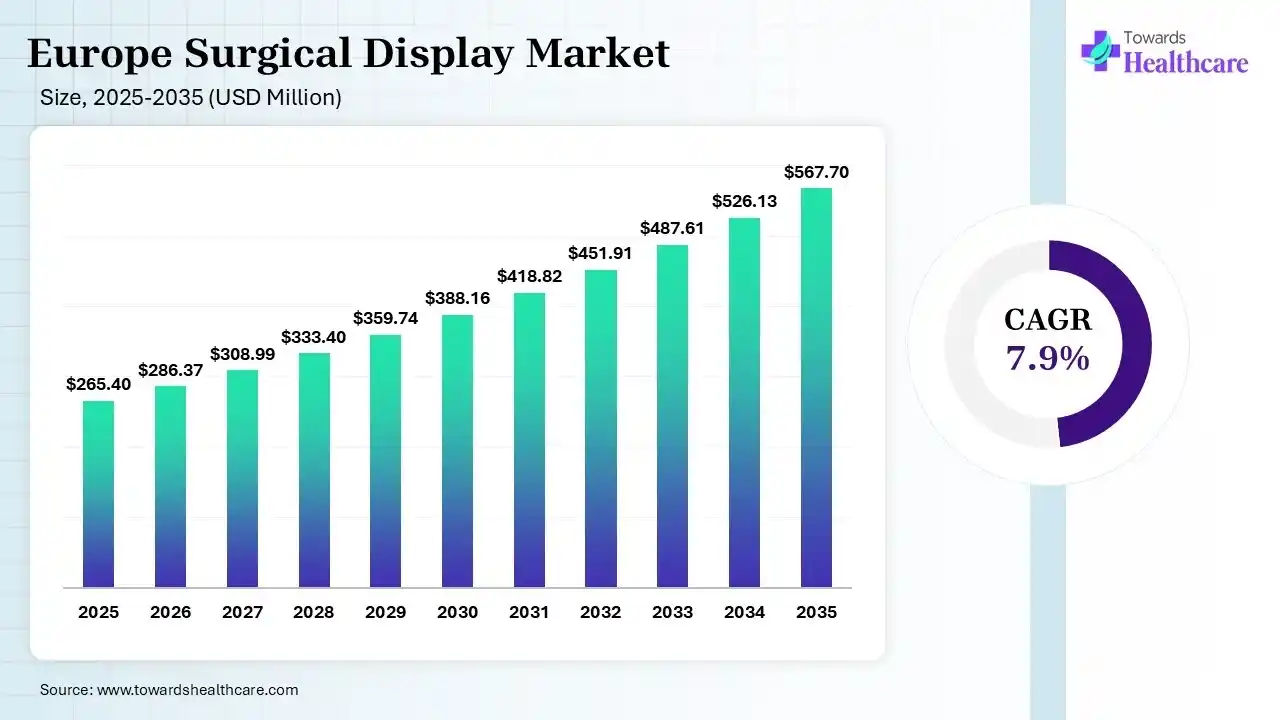

The Europe surgical display market size was estimated at USD 265.4 million in 2025 and is predicted to increase from USD 286.37 million in 2026 to approximately USD 567.7 million by 2035, expanding at a CAGR of 7.9% from 2026 to 2035.

")

")

Surgical displays are medical-grade monitors used in operating rooms to provide high-resolution, real-time visualization during surgical procedures. They are connected to imaging systems such as endoscopes, laparoscopes, and surgical cameras, helping surgeons improve precision and decision-making. Market growth is driven by increasing minimally invasive surgeries, rising demand for advanced imaging technologies, and ongoing hospital modernization initiatives across Europe. Key trends include the adoption of 4K/8K and 3D visualization systems, while opportunities are emerging from the expansion of digital operating rooms and robotic-assisted surgeries. Technological advancements such as HDR imaging, AI-enhanced visualization, and touchscreen medical displays are further improving surgical accuracy and workflow efficiency.

The Europe surgical display market is growing due to the increasing adoption of minimally invasive and image-guided surgeries, rising demand for high-resolution 4K and 3D visualization systems, and continuous modernization of hospital operating rooms. Growing investments in healthcare infrastructure, expansion of robotic-assisted procedures, and advancements in surgical imaging technologies are further supporting market expansion across the region.

AI can significantly impact the market by improving real-time image processing, enhancing tissue and anatomical structure identification, and supporting surgical decision-making. AI-powered visualization systems can reduce errors, optimize workflow efficiency, and improve surgical precision. Increasing integration of AI with robotic-assisted and image-guided surgeries is expected to drive demand for advanced surgical displays across Europe.

Growing Adoption of 4K, 8K, and 3D Displays: European healthcare providers are increasingly investing in ultra-high-definition and 3D surgical displays to enhance visualization during complex procedures. These technologies improve depth perception, image clarity, and surgical precision, supporting the growing demand for minimally invasive and image-guided surgeries across hospitals and specialty surgical centers.

Integration with AI and Robotic Surgery Systems: The market is witnessing greater integration of surgical displays with AI-powered imaging platforms and robotic-assisted surgical systems. Advanced visualization capabilities, real-time image enhancement, and intelligent decision-support tools are helping surgeons improve procedural accuracy, reduce complications, and enhance operating room efficiency.

Expansion of Digital and Smart Operating Rooms: The future outlook remains strong as hospitals continue transitioning toward fully connected digital operating rooms. Surgical displays are becoming central components of integrated surgical ecosystems, enabling seamless data sharing, remote collaboration, and improved workflow management, which is expected to drive sustained market growth across Europe.

| Table | Scope |

| Market Size in 2026 | USD 286.37 Million |

| Projected Market Size in 2035 | USD 567.7 Million |

| CAGR (2026 - 2035) | 7.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Display Resolution, By Screen Size, By Display Type, By Technology, By Application, By End User, By Connectivity, By Region |

| Top Key Players | Barco, Karl Storz SE & Co. KG, Getinge AB, Richard Wolf GmbH, Brainlab AG, NDS Surgical Imaging Europe, Merivaara Corp. |

")

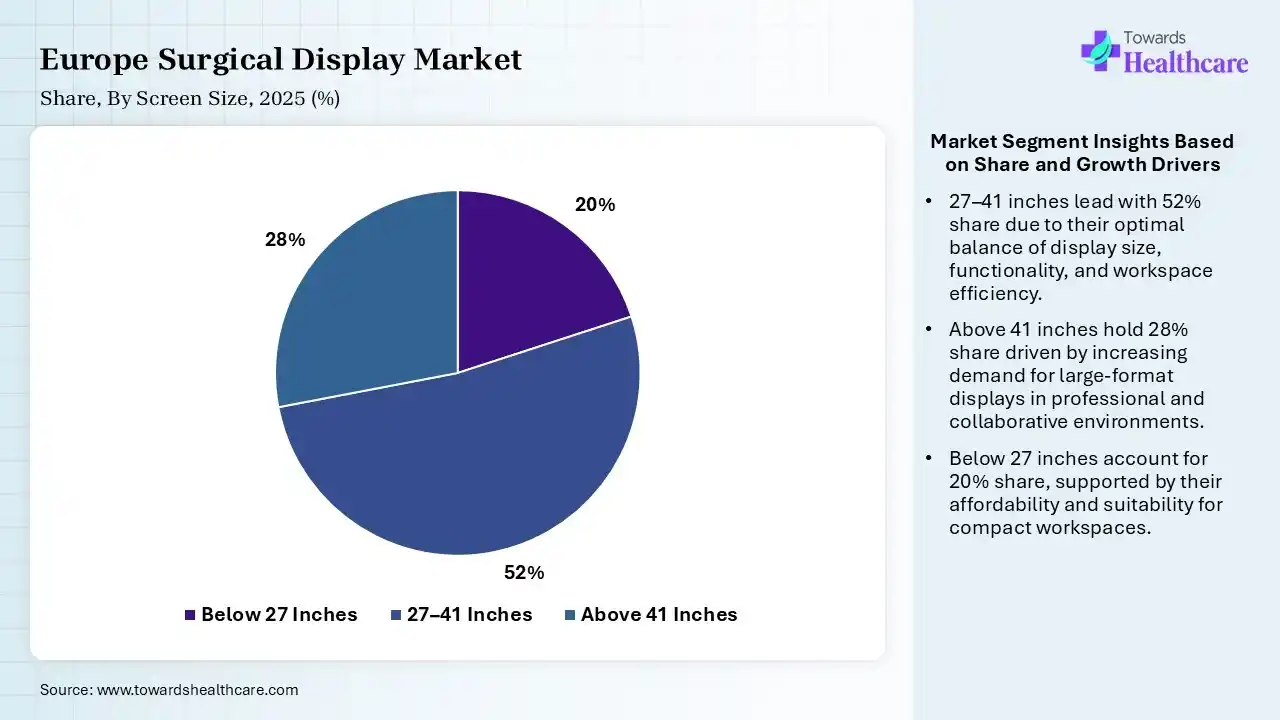

| Segment | Share 2025 (%) |

| Below 27 Inches | 20% |

| 27–41 Inches | 52% |

| Above 41 Inches | 28% |

The 27-41 Inches Segment Dominated the Europe Surgical Display Market in 2025

The 27-41 inches segment held a dominant share of 52% in 2025 due to its ideal balance between large-screen visualization and operating room space efficiency. These displays provide clear, high-resolution images essential for minimally invasive and image-guided procedures while remaining easy to integrate into surgical workstations. This versatility, ergonomic design, and compatibility with advanced imaging systems have made them the preferred choice among hospitals and surgical centers.

The above 41 inches segment held the second-largest share of 28% in 2025 and is expected to grow at the fastest CAGR of 9.6% in the market during the forecast period due to its ability to provide a larger viewing area and enhanced image visibility during complex surgical procedures. These displays are increasingly used in hybrid operating rooms, robotic-assisted surgeries, and multidisciplinary environments where multiple clinicians require simultaneous access to detailed medical images, improving collaboration and procedural efficiency.

The below 27 inches segment held a 20% share of the Europe surgical display market due to increasing demand for compact and space-efficient display solutions in smaller operating rooms, ambulatory surgical centers, and specialized clinical settings. These displays offer cost-effective visualization while maintaining high image quality for routine procedures. Their ease of installation, portability, and compatibility with modern imaging systems are further support adoption across healthcare facilities in Europe.

")

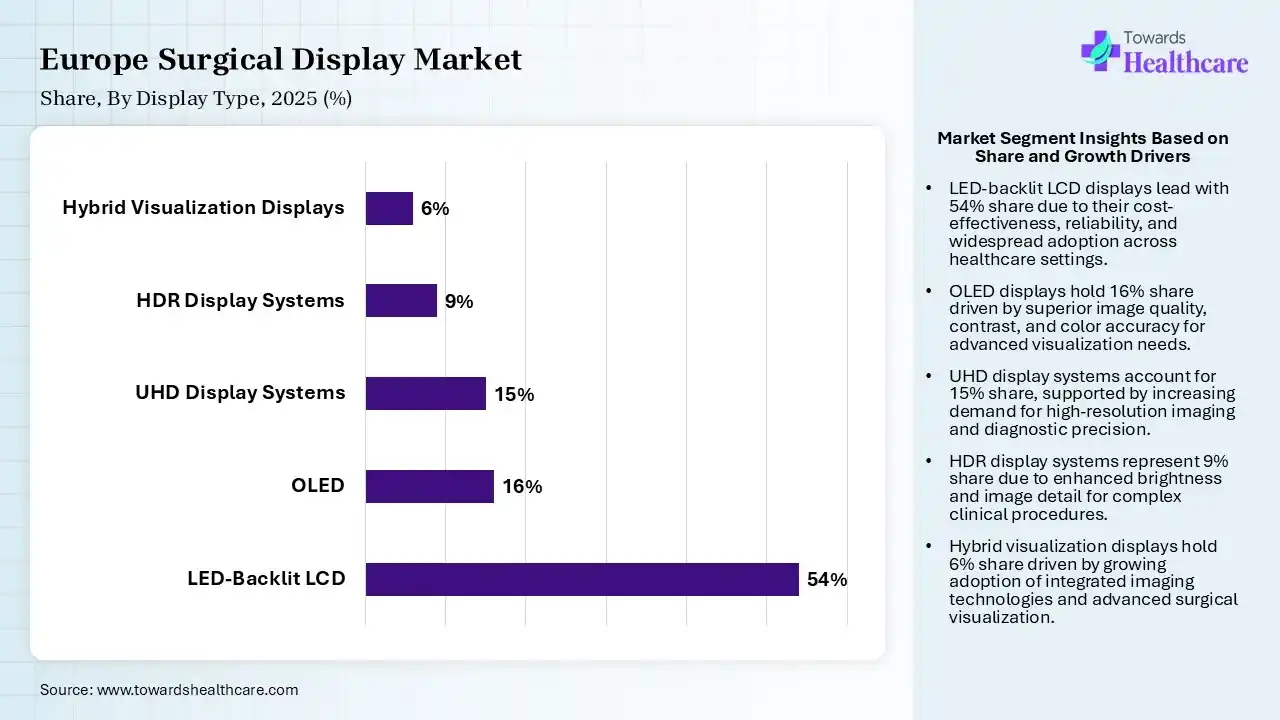

| Segment | Share 2025 (%) |

| LED-Backlit LCD | 54% |

| OLED | 16% |

| UHD Display Systems | 15% |

| HDR Display Systems | 9% |

| Hybrid Visualization Displays | 6% |

The LED-backlit LCD Segment Led the Europe Surgical Display Market in 2025 with the Largest Share

The LED-backlit LCD segment led the market with a share of 54% in 2025 due to its superior image brightness, high contrast ratios, energy efficiency, and cost-effectiveness. These displays provide clear and accurate visualization required for minimally invasive and image-guided procedures while offering long operational life and reliability. Their widespread adoption across hospitals and surgical centers, coupled with compatibility with advanced imaging systems, supported their market dominance.

The OLED segment held the second-largest share of 16% in 2025 and is expected to grow at the fastest CAGR of 11.8% in the market during the forecast period due to its exceptional color accuracy, deep contrast levels, and faster response times. These features enhance the visualization of fine anatomical details during complex surgical procedures. Growing adoption in advanced operating rooms, robotic-assisted surgeries, and high-end healthcare facilities, along with increasing demand for premium imaging performance, supported its strong market position.

The UHD display systems segment held a 15% share of the European surgical display market due to increasing demand for ultra-high-resolution imaging that enhances visualization of anatomical structures and surgical details. UHD displays improve accuracy during minimally invasive and image -guided procedures while supporting advanced technologies such as robotic-assisted surgery and 3D imaging. Rising investment in modern operating rooms and digital healthcare infrastructure is further accelerating adoption.

The HDR display systems segment held a 9% share of the market due to its ability to deliver superior brightness, contrast, and color accuracy compared to conventional displays. HDR technology enables clearer visualization of tissues, blood vessels, and anatomical structures during complex procedures. Increasing demand for enhanced image quality in minimally invasive and robotic-assisted surgeries, along with ongoing operational room modernization, is driving segment growth.

")

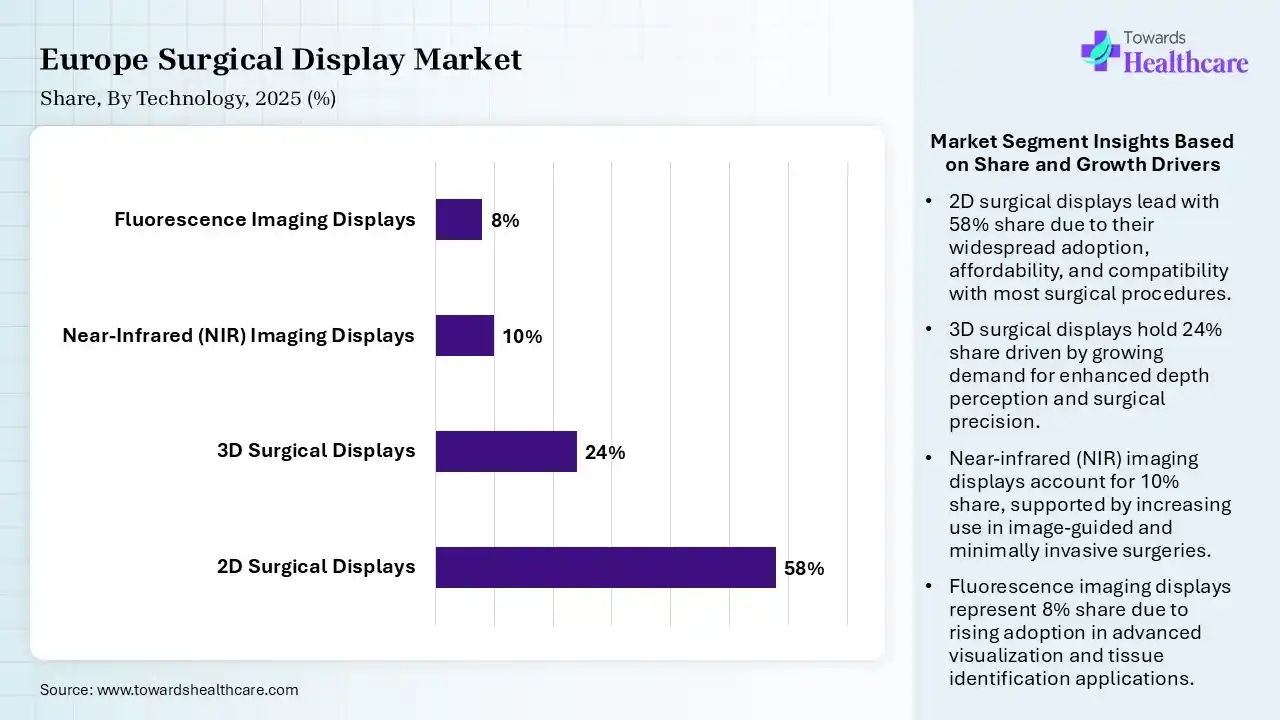

| Segment | Share 2025 (%) |

| 2D Surgical Displays | 58% |

| 3D Surgical Displays | 24% |

| Near-Infrared (NIR) Imaging Displays | 10% |

| Fluorescence Imaging Displays | 8% |

The 2D Surgical Displays Segment Led the Europe Surgical Display Market in 2025 with the Largest Share

The 2D surgical displays segment held a dominant share of 58% in 2025 due to their widespread adoption, cost-effectiveness, and compatibility with a broad range of surgical imaging systems. These displays provide reliable high-resolution visualization for routine and minimally invasive procedures while requiring lower investment than advanced alternatives. Their established presence in hospitals and surgical centers, along with ease of integration into existing operating room infrastructure, supported market dominance.

The 3D surgical displays segment held the second-largest share of 24% in 2025 due to their ability to provide enhanced depth perception and improved visualization of anatomical depth perception and improved visualization of anatomical structure. These displays are increasingly adopted in minimally invasive and robotic-assisted surgeries, where precision is critical. Growing demand for advanced surgical imaging, better hand-eye coordination, and improved clinical outcomes has supported the segment’s strong market position.

The near-infrared (NIR) imaging displays segment held a 10% market share due to its ability to provide enhanced visualization of blood vessel tissue perfusion and anatomical structure during surgery. NIR technology supports greater surgical precision and improved clinical outcomes, particularly in oncology, cardiovascular, and minimally invasive procedures. Growing adoption of image-guided surgeries and advanced fluorescence imaging techniques is further driving segment growth.

The fluorescence imaging displays segment held an 8% share in 2025 and is expected to grow at the fastest CAGR of 11.2% in the Europe surgical display market during the forecast period due to increasing adoption of image-guided surgeries and demand for enhanced tissue visualization. These displays enable real-time identification of blood flow, tumors, and critical anatomical structures, improving surgical precision and patient outcomes. Rising use in oncology, cardiovascular, and minimally invasive procedures is further accelerating segment growth.

")

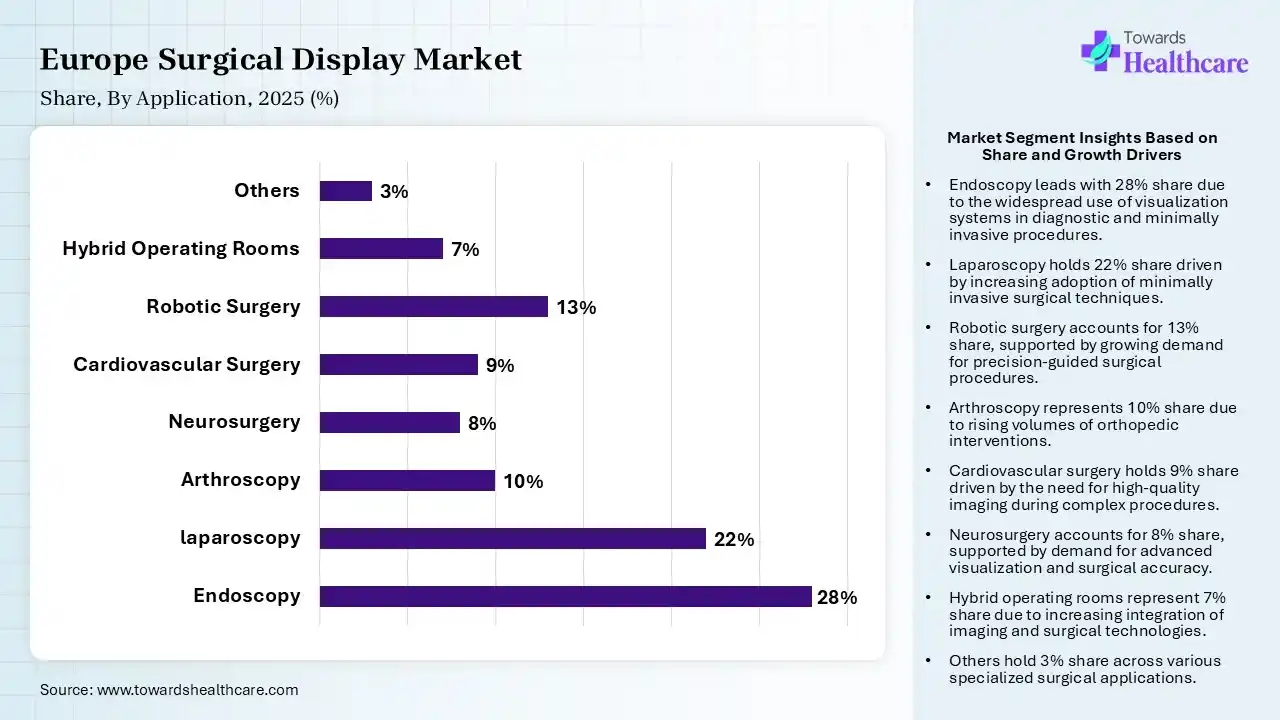

| Segment | Share 2025 (%) |

| Endoscopy | 28% |

| laparoscopy | 22% |

| Arthroscopy | 10% |

| Neurosurgery | 8% |

| Cardiovascular Surgery | 9% |

| Robotic Surgery | 13% |

| Hybrid Operating Rooms | 7% |

| Others | 3% |

The Endoscopy Segment Led the Europe Surgical Display Market in 2025 with the Largest Share

The endoscopy segment dominated the market with a share of 28% in 2025 due to the widespread adoption of minimally invasive procedures across gastroenterology, urology, gynecology, and general surgery. Endoscopic procedures require high-resolution, real-time visualization to ensure accuracy and patient safety. The increasing prevalence of chronic diseases, rising surgical volumes, and growing preference for minimally invasive techniques have significantly boosted demand for advanced surgical displays in endoscopy applications.

The laparoscopy segment held the second-largest share of 22% in 2025 due to the increasing preference for minimally invasive surgical procedures that offer faster recovery times, reduced hospital stays, and lower complication rates. Laparoscopic surgeries rely heavily on high-quality visualization systems for precision and safety. Growing volumes of abdominal, gynecological, and urological procedures, along with advancements in imaging technologies, supported the segment’s strong market position.

The robotic surgery segment held a 13% share in 2025 and is expected to grow at the fastest CAGR of 12.7% in the Europe surgical display market during the forecast period due to increasing adoption of robotic-assisted procedures that require highly advanced visualization systems. Surgical displays play a critical role in delivering real-time, high-definition images that enhance precision and control. Rising investments in robotic surgical platforms, growing demand for minimally invasive procedures, and continuous technological advancements are driving rapid segment growth.

The arthroscopy segment held a 10% market share due to the rising prevalence of sports injuries, orthopedic disorders, and age-related joint conditions. Arthroscopic procedures require high-definition visualization for accurate diagnosis and treatment within confined joint spaces. The growing demand for minimally invasive orthopedic surgeries, faster patient recovery, and advancements in imaging technologies are increasing the adoption of surgical display in arthroscopic applications across Europe.

")

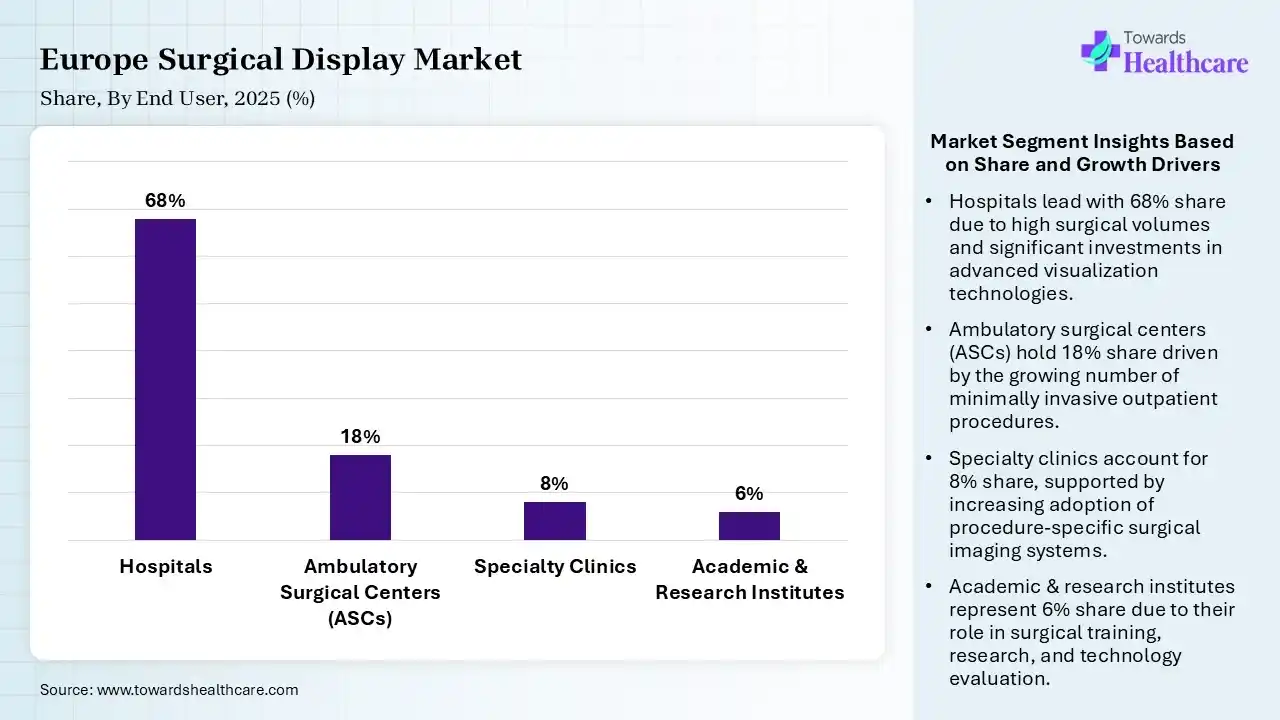

| Segment | Share 2025 (%) |

| Hospitals | 68% |

| Ambulatory Surgical Centers (ASCs) | 18% |

| Specialty Clinics | 8% |

| Academic & Research Institutes | 6% |

The Hospitals Segment Dominance Dominated the Europe Surgical Display Market in 2025

The hospitals segment held a dominant share of 68% in 2025 due to the high volume of surgical procedures performed in hospital settings and the scalability of advanced operating room infrastructure. Hospitals are major adopters of high-resolution surgical visualization systems for minimally invasive, robotic-assisted, and image-guided surgeries. Continuous investments in healthcare modernization, growing patient admissions, and increasing demand for advanced surgical technologies further strengthen the segment’s market leadership.

The ambulatory surgical centers (ASCs) segment held the second-largest share of 18% in 2025 and is expected to grow at the fastest CAGR of 9.8% in the market during the forecast period due to the growing shift towards outpatient surgical procedures that offer lower costs and shorter recovery times. ASCs increasingly adopt advanced visualization systems to support minimally invasive surgeries and improved procedural efficiency. Rising patient preference for same-day surgeries, expanding ASC networks, and continuous technological upgrades have strengthened the segment’s market position.

The specialty clinics segment held an 8% of Europe surgical display market share due to the increasing number of specialized healthcare facilities focused on ophthalmology, orthopedics, gastroenterology, and other surgical disciplines. These clinics are investing in advanced visualization technologies to improve diagnostic and surgical precision. Rising demand for minimally invasive procedures, shorter treatment times, and personalized patient care is further accelerating the adoption of surgical display in specialty clinics.

The academic clinics segment held a 6% market share due to increasing investment in medical education, surgical training, and clinical research. These institutions require advanced surgical displays for teaching. simulation-based learning, and complex surgical procedures. Growing collaborations between universities, hospitals, and medical technology providers, along with rising adoption of innovative imaging systems, are driving demand for displays in academic clinic settings.

The Europe surgical display market is dominated by its well-established healthcare infrastructure, high adoption of minimally invasive and robotic-assisted surgeries, and strong investments in advanced medical imaging technologies. The region benefits from the presence of leading medical device manufacturers, widespread modernization of operating rooms, and favorable healthcare spending. Continuous technological innovation and growing demand for precision-guided surgical procedures further strengthen Europe’s leadership position.

Germany dominated the market with a 24% share in 2025. Germany is experiencing strong growth in the Europe surgical display market due to its advanced healthcare infrastructure, high volume of surgical procedures, and widespread adoption of minimally invasive and robotic -assisted surgeries. The country is home to several leading medical technology manufacturers and research institutions, fostering innovation in surgical imaging. Continuous investments in hospitals’ modernization and digital operating rooms are further accelerating market expansion.

France captured a 15% share of the market in 2025. France is expanding in the Europe surgical display market due to increasing investments in healthcare infrastructure, growing adoption of minimally invasive surgical procedures, and rising demand for medical imaging technologies. The country is actively modernizing hospital operating rooms and integrating digital healthcare solutions to improve surgical outcomes. Strong government support for healthcare innovation and increasing surgical volumes are further driving market growth.

UK held an 18% share in the market and is growing rapidly in the Europe surgical display market due to the growing adoption of advanced surgical imaging technologies, rising demand for minimally invasive procedures, and ongoing modernization of healthcare facilities. Increased investments in digital operating rooms, robotic-assisted surgeries, and high-resolution visualization systems are enhancing surgical precision and efficiency. Strong healthcare spending, expanding surgical volumes, and continuous technological advancements are further supporting market growth across the country.

| Companies | Headquarters | Offerings |

| Barco | Kortrijk, Belgium | Surgical displays, medical imaging monitors, operating room visualization solutions |

| Karl Storz SE & Co. KG | Tuttlingen, Germany | Endoscopic imaging systems, surgical displays, OR integration solutions |

| Getinge AB | Gothenburg, Sweden | Integrated operating room systems, surgical visualization, and display solutions |

| Richard Wolf GmbH | Knittlingen, Germany | Endoscopic imaging equipment, surgical displays, and visualization systems |

| Brainlab AG | Munich, Germany | Surgical navigation systems, medical visualization, and display technologies |

| NDS Surgical Imaging Europe | Amsterdam, Netherland | Medical-grade surgical displays and imaging solutions |

| Merivaara Corp. | Lahti, Finland | Integrated operating room systems, surgical visualization solutions |

In July 2025, Mattias Perjos, President & CEO, said, "In Life Science, we launched a new washer, and in Surgical Workflows, we continue to strengthen our offering in consumables, where we have achieved high growth. Surgical Workflows also entered an exciting partnership with Zimmer Biomet that enhances our presence in the rapidly growing ASC segment in the U.S. market."

By Display Resolution

By Screen Size

By Display Type

By Technology

By Application

By End User

By Connectivity

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar