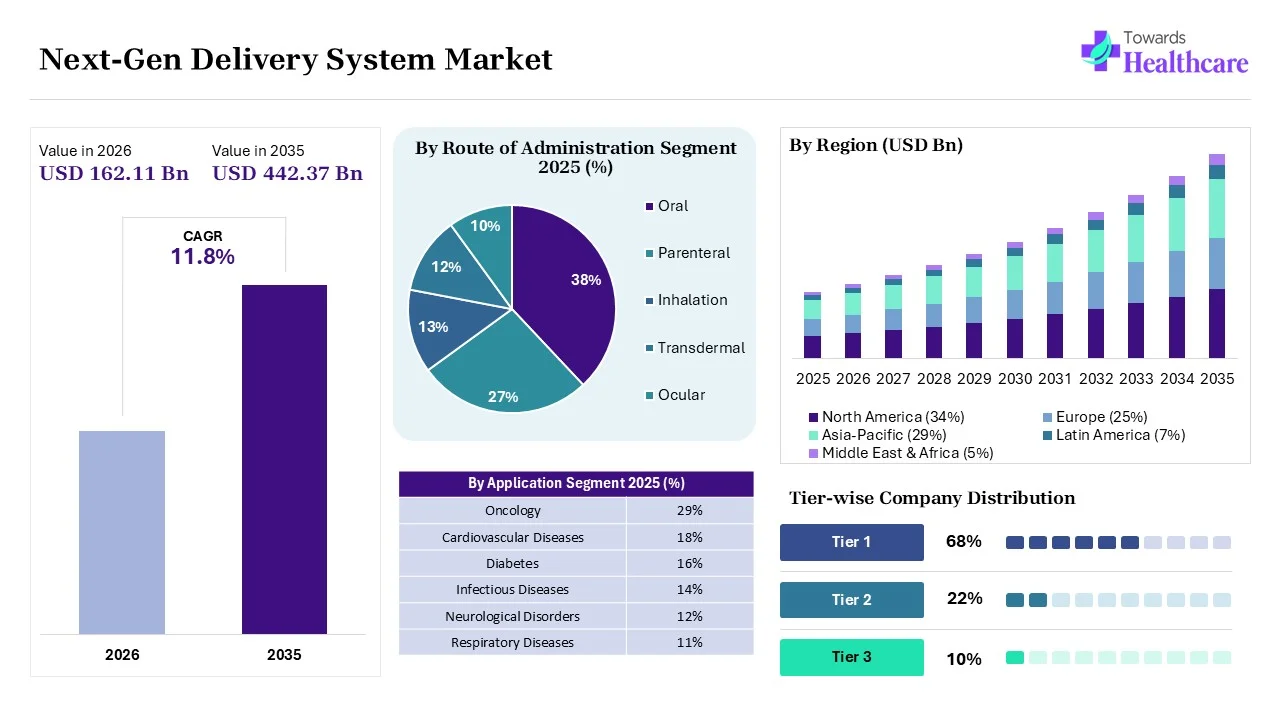

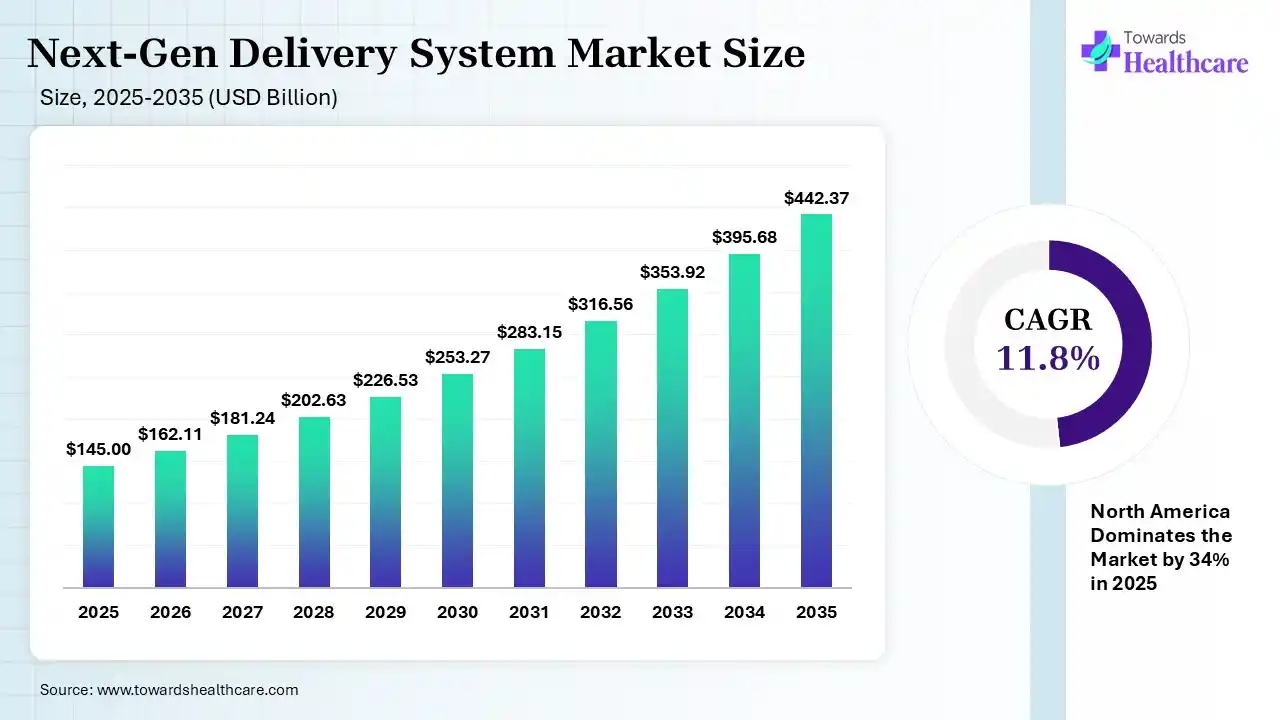

The global next-gen delivery system market size was estimated at USD 145 billion in 2025 and is predicted to increase from USD 162.11 billion in 2026 to approximately USD 442.37 billion by 2035, expanding at a CAGR of 11.80% from 2026 to 2035.

")

The growing incidence of diseases is increasing the use of novel treatment approaches, which in turn, is increasing the demand for next-gen delivery systems. The growing collaborations between the companies are also increasing their development and launches. Moreover, the use of AI is contributing by enhancing its properties, increasing its acceptance rates. This, in turn, is also enhancing the use of various next-gen delivery systems in the biologics and gene therapies. Additionally, their demand in different regions is also increasing, due to growing use of biologics, advancing healthcare, or even due to their rising demand. Thus, all these developments are promoting the next-gen delivery system market growth.

The next generation drug delivery systems provide controlled as well as sustained release of the drugs. At the same time, their use in target-specific action is also growing, which in turn, helps to minimize the side effects. Furthermore, the use of nanocarrier systems and liposomal drug delivery systems is also increasing as they are being used in the delivery of various drugs with poor solubility or instability. Thus, their use in the treatment of cancer, CNS diseases, as well as gene therapies, is increasing.

Driver

To improve the safety, efficacy, as well as bioavailability of drugs, various innovations are being developed. At the same time, research and development to formulate a nanocarrier system for site-specific action are also increasing. Similarly, to enhance the stability of various formulations, the use of liposomal or hydrogel delivery systems is also being considered. Furthermore, the use as well as demand for transdermal drug delivery systems with the help of patches is also increasing. Thus, all these innovations are driving the next-gen delivery system market.

Restraint

For the formulation and development of these next-generation delivery systems, the equipment as well as the infrastructure required are sophisticated. At the same time, the procedure or the methods for their development or complex, which requires expertise. Furthermore, the stability issues as well as unwanted interactions can also affect their development, restraining the market growth.

Opportunity

There is a rise in the incidence rate of various diseases, such as cancer, autoimmune disease, diabetes, and rare diseases etc. These diseases increase the demand for new treatment approaches, leading to the growth of next-gen delivery system options. Hence, with the help of these next-gen delivery systems, drugs with enhanced stability, bioavailability, efficacy, and targeted action can be delivered. Additionally, they can also show prolonged release patterns, reducing the dosing frequency and increasing patient compliance with the treatment. Thus, this promotes the next-gen delivery system market growth.

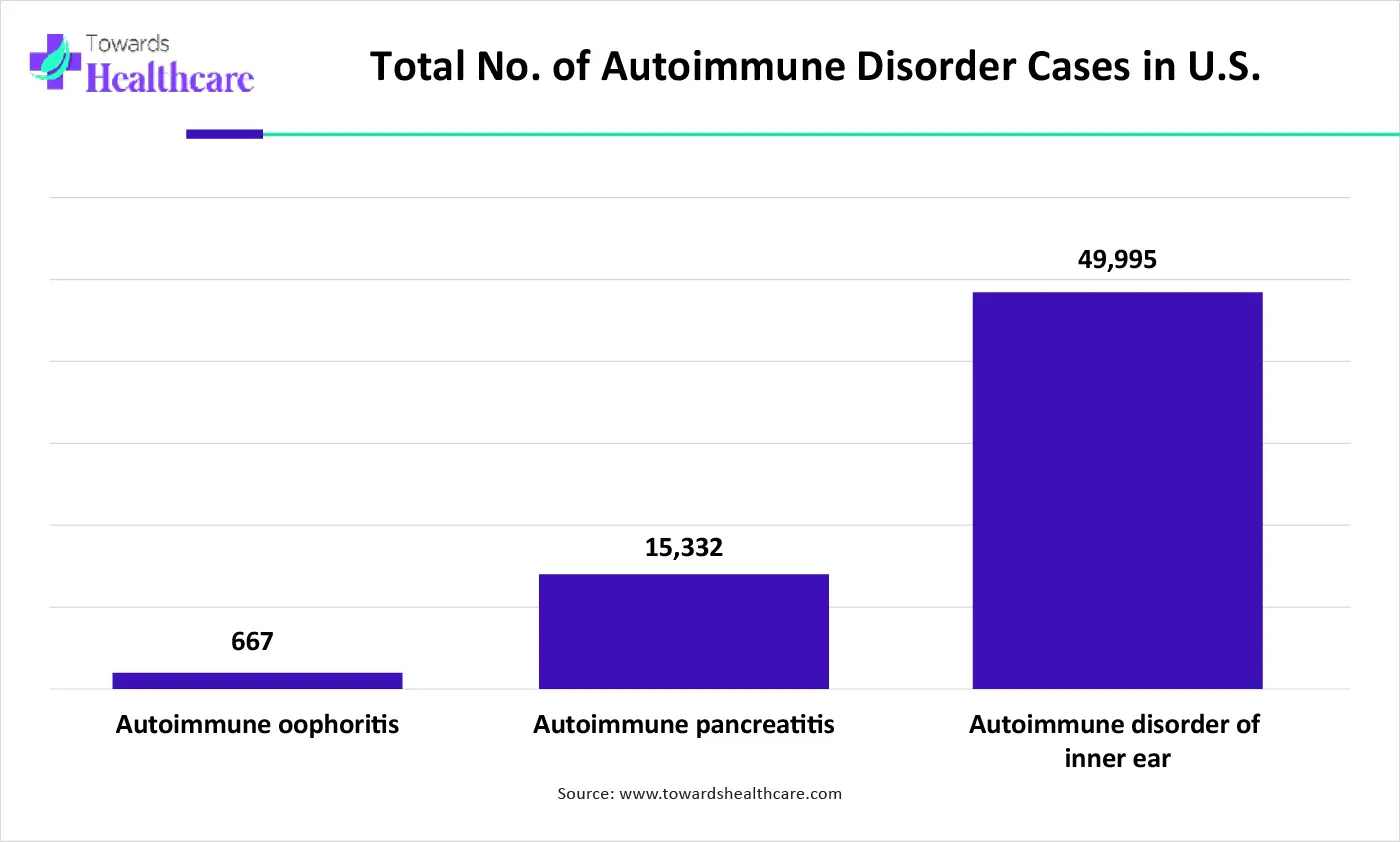

The graph represents the total number of autoimmune disorder cases observed in the U.S. It indicates that there will be a rise in cases of autoimmune disorders. Hence, it increases the demand for next-gen delivery systems to enhance the properties of the treatment options for the effective management of these rising disorders. Thus, this in turn will ultimately promote the market growth.

Increased Focus on Patient-Centric Therapies: In order to enhance patient experience by offering minimally invasive, easy-to-use, and painless solutions, the use of next-gen delivery systems is increasing, where they offer personalized dosing and improve patient compliance and convenience.

Growing Use of Biologics: The growing acceptance rates of the biologics are increasing their development to offer targeted and controlled drug release, which is increasing the demand for next-gen delivery systems, where the growing use of proteins and antibodies is also increasing their use to maintain their stability and effectiveness.

Technological Advancements: The growing technological advancements are driving the development of new next-gen delivery systems, such as smart pumps, implants, and microneedles, along with the integration of advanced technologies to offer real-time monitoring and personalized dosing.

The use of AI in the next-gen delivery systems is increasing. With the help of AI, smart drug delivery systems are being developed that help to transport drugs to the specific tissues and cells, minimizing the side effects. Moreover, with the use of genetic algorithms, the biological processes and drug activity can be predicted and optimized. Additionally, to merge the novel diagnostic tools with targeted therapies, AI in drug design is being integrated with biotechnology to develop personalized medicine, known as theragnostics.

| Table | Scope |

| Market Size in 2026 | USD 162.11 Billion |

| Projected Market Size in 2035 | USD 442.37 Billion |

| CAGR (2026 - 2035) | 11.80 % |

| Leading Region | North America by 34% |

| Key Applications | Oncology drug delivery, vaccine delivery, gene & RNA therapeutics (mRNA/siRNA), controlled-release formulations, insulin delivery systems, CNS drug delivery, long-acting injectables |

| Primary End Users | Pharmaceutical companies, biotechnology firms, hospitals, specialty clinics, research institutes, CDMOs |

| Key Challenges | High R&D costs, complex regulatory pathways, scalability issues, stability & formulation challenges, IP barriers, manufacturing complexity |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Technology, By Route of Administration, By End User, By Region |

| Top Key Players | F. Hoffmann-La Roche Ltd, Johnson & Johnson Services, Inc., Pfizer Inc., Novartis AG, Merck & Co., Inc., Becton, Dickinson and Company, Genmab A/S, Sanofi, GlaxoSmithKline plc, AbbVie Inc., Bayer AG, AstraZeneca, Gilead Sciences, Inc., Amgen, Inc., Boehringer Ingelheim |

| Segments | Shares % |

| Oral Drug Delivery Systems | 32% |

| Injectable Drug Delivery Systems | 26% |

| Pulmonary Drug Delivery Systems | 14% |

| Transdermal Drug Delivery Systems | 12% |

| Implantable Drug Delivery Systems | 9% |

| Ocular Drug Delivery Systems | 7% |

The Oral Drug Delivery Systems Segment Led the Market in 2025

| Segments | Shares % |

| Nanotechnology-Based Delivery | 28% |

| Targeted Drug Delivery | 24% |

| Controlled & Sustained Release | 30% |

| Smart Drug Delivery Systems | 18% |

The Controlled & Sustained Release Segment Led the Market in 2025

| Segments | Shares % |

| Oral | 38% |

| Parenteral | 27% |

| Inhalation | 13% |

| Transdermal | 12% |

| Ocular | 10% |

The Oral Segment Dominated the Market in 2025

| Segments | Shares % |

| Oncology | 29% |

| Cardiovascular Diseases | 18% |

| Diabetes | 16% |

| Infectious Diseases | 14% |

| Neurological Disorders | 12% |

| Respiratory Diseases | 11% |

The Oncology Segment Dominated the Market in 2025

| Segments | Shares % |

| Hospitals | 42% |

| Home Care Settings | 26% |

| Specialty Clinics | 18% |

| Ambulatory Surgical Centers | 14% |

The Hospitals Segment Dominated the Market in 2025

")

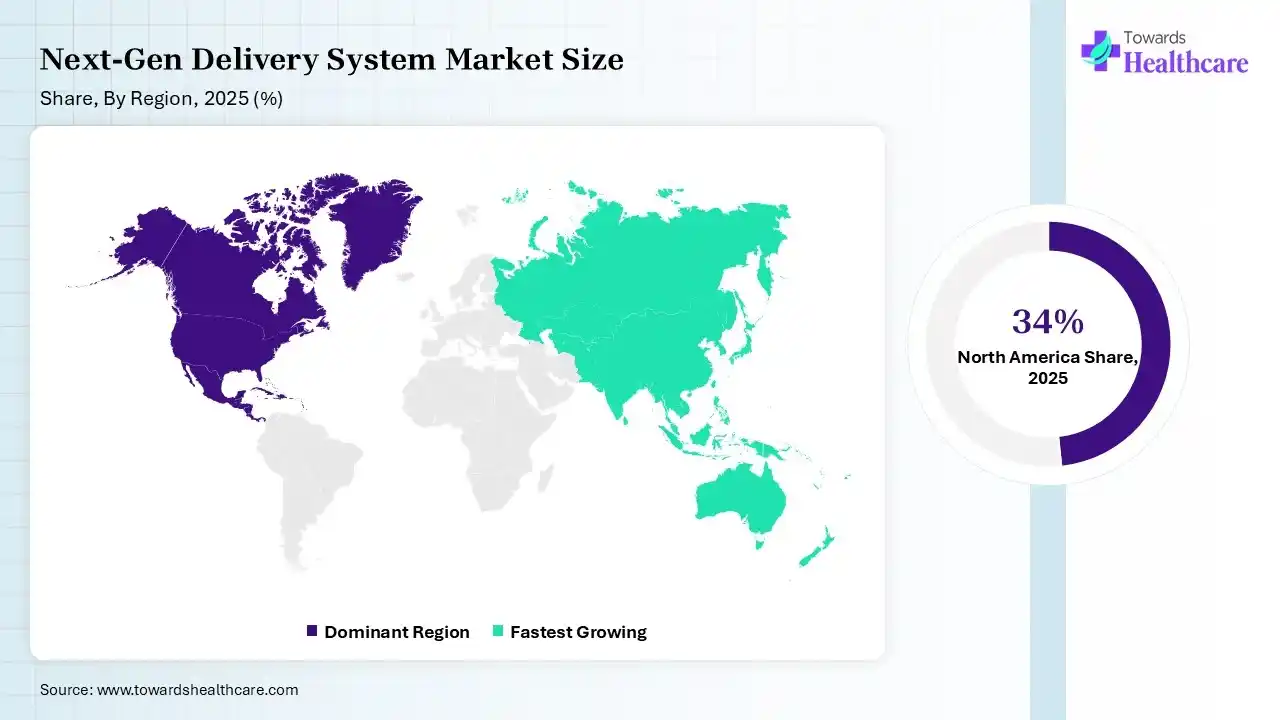

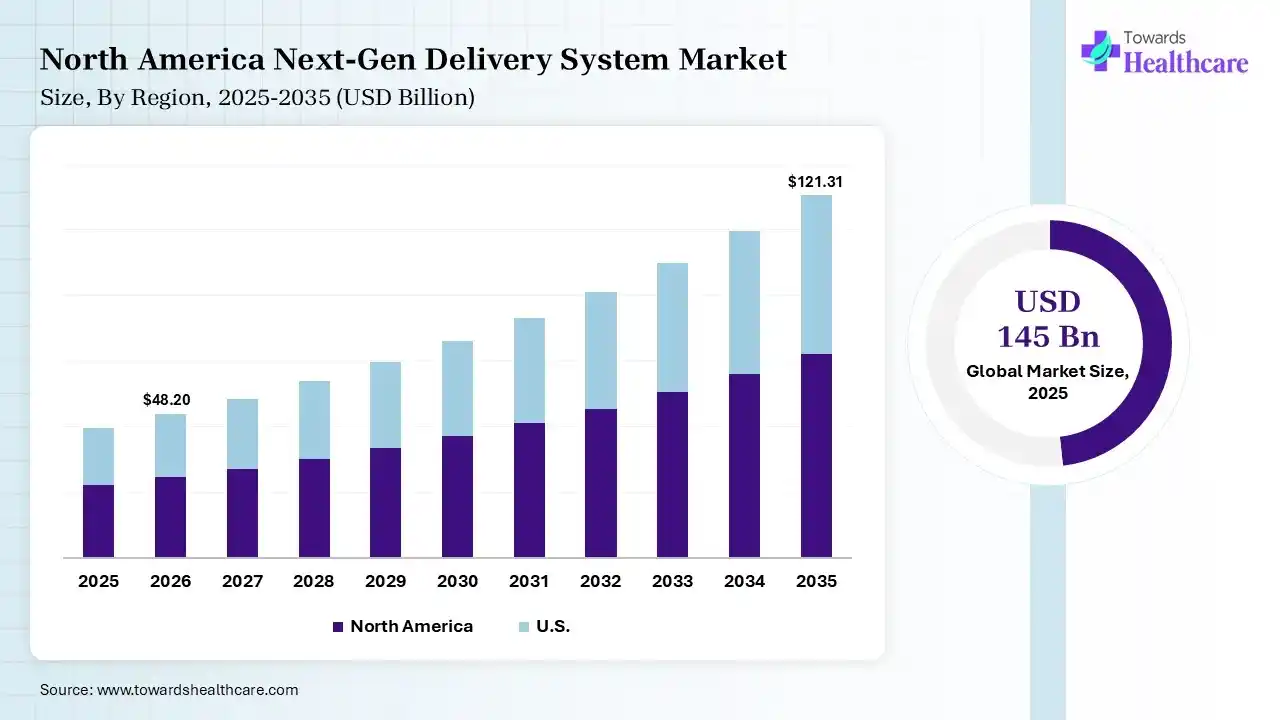

North America dominated the next-gen delivery system market in 2025, with a revenue share of 34%. The growing use of biologics in the treatment of various diseases in North America is increasing the demand for next-gen delivery systems. This contributes to the market growth. The region is also growing due to the strong presence of key market players. These key players collaborate and contribute to the growing demand for therapeutics and other needs for healthcare needs.

The U.S. Next-Gen Delivery System Market Trends

The U.S. dominated the market in North America with 27% of the North American market share in 2025. The industries in the U.S. are focusing on the development of various next-gen delivery systems. At the same time, the use of advanced technologies is enhancing the developmental process as well as their safety and efficacy. The U.S. is the largest economy in the North American region with advanced healthcare systems and a highly developed pharma and biotechnology sector.

The Canada Next-Gen Delivery System Market Trends

Of the 34%, Canada held 7% of the market share in 2025. The industries as well as institutes are developing various next-gen delivery systems for drugs with stability issues. This, in turn, enhances the collaborations between them, which are further supported by the funding provided by the government. The government of Canada is collaborating with other countries to enhance healthcare services and products.

Asia Pacific held 29% of the market share in 2025 and is expected to host the fastest-growing next-gen delivery system market with 13.1% CAGR during the forecast period. The healthcare sector in the Asia Pacific is expanding due to the growing use of various treatment approaches, as well as research and development. This, in turn, is enhancing the market growth. Asia Pacific has the largest population, which demands a large number of products and services from the healthcare industry. Due to this, the countries in this region, like China, Japan, India, Thailand, etc, are taking efforts to develop high-end healthcare products.

The China Next-Gen Delivery System Market Trends

China held 11% of the Asia Pacific market in 2025 because China consists of a large population, which in turn increases the risk of diseases. This results in growing adoption of next-gen delivery systems for their effective treatment. Furthermore, they are also developing new minimally invasive next-gen delivery systems. China contributes the largest share because of its innovation and healthcare advancements. After the U.S., China holds second place in the pharmaceutical and biotechnology sectors.

The India Next-Gen Delivery System Market Trends

India held 5% of the Asia Pacific market share in 2025. The growing diseases in India are increasing the demand for next-gen delivery systems. Thus, this increases their research and development, which are further supported by the government to make them affordable and easily accessible. India has the largest population, with a growing demand for medicine in chronic conditions. As the population grows, the government of India has to take various measures to tackle the demand for products.

Europe held the second largest market share of 25% in 2025 and is expected to grow significantly in the next-gen delivery system market during the forecast period. Europe is experiencing a rise in the research and development of next-gen delivery systems for the treatment of various chronic diseases. This promotes the market growth.

The Germany Next-Gen Delivery System Market Trends

Germany captured 7% of the Europe market in 2025. The healthcare sector in Germany is utilizing next-gen delivery systems for the treatment of cancer or autoimmune diseases. At the same time, new targeted drug delivery systems are also being adopted as well as developed by the industries for diabetes and Alzheimer's disease.

The UK Next-Gen Delivery System Market Trends

Out of the 25% Europe market share, the UK held 5% in 2025. The demand for the use of gene therapies or biologics is increasing in the UK. This, in turn, is increasing the development in the next-gen delivery systems for their targeted release, as well as with new injectable systems. These are furthermore supported by the regulatory bodies.

Latin America captured 7% of the market share in 2025 and is expected to grow significantly in the next-gen delivery system market during the forecast period, due to expanding healthcare infrastructure, which increases the demand for advanced drug delivery systems for the management of growing chronic diseases. The growing shift toward self-administration is also increasing their innovations, which is enhancing the market growth.

Brazil Next-Gen Delivery System Market Trends

The growing incidence of chronic diseases and expanding healthcare in Brazil are increasing the demand for effective treatment options, which is driving the development of the next-gen delivery systems. The companies are developing various injectables, implants, pumps, etc, which are being supported by investment from various sources, driving their acceptance rates.

MEA held 5% of the market share in 2025 and is expected to grow significantly in the next-gen delivery system market during the forecast period, due to growth in chronic diseases, which is increasing the demand for advanced delivery systems for target-specific actions. The growing healthcare infrastructure, investments, innovation, and government initiatives are also promoting their advancement, contributing to the market growth.

Saudi Arabia Next-Gen Delivery System Market Trends

The expanding healthcare infrastructure in Saudi Arabia is driving the development of various next-gen delivery systems. The growing chronic disease and government support are encouraging their development. Additionally, the increasing digitalization is also accelerating their innovations along with the development of new drug delivery devices.

| Ecosystem Category | Key Players / Role | Description |

| Technology Providers | Lipid nanoparticle, polymer, and nanoformulation innovators | Develop core delivery technologies enabling targeted and controlled drug release |

| Product Manufacturers | Pharmaceutical & biotech companies | Integrate delivery systems into therapeutic drugs and biologics |

| Service Providers | CDMOs, formulation development firms | Provide formulation design, scaling, and manufacturing support |

| Platform Providers | Delivery platform developers | Offer proprietary drug delivery platforms (e.g., LNP, antibody-drug conjugate platforms) |

| CROs/CDMOs | Catalent, Lonza, WuXi AppTec | Support formulation, clinical manufacturing, and delivery system optimization |

| Software Vendors | Simulation & formulation modeling tools | Enable drug delivery modeling, pharmacokinetics simulation, and formulation design |

| Research Institutions | Universities, biotech research labs | Drive early-stage innovation in nanomedicine and advanced delivery systems |

| End-User Industries | Pharma, biotech, hospitals, vaccine manufacturers | Primary adopters of next-gen delivery technologies |

R&D

Clinical Trials and Regulatory Approvals

Formulation and Final Dosage Preparation

Packaging and Serialization

Patient Support and Services

Strengths

Weaknesses

Opportunities

Threats

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Pfizer | New York City, New York | USA | Major developer of advanced biologics and mRNA-based therapeutics requiring lipid nanoparticle delivery systems | mRNA vaccines, biologics, injectable formulations, advanced drug delivery platforms |

| Roche | Basel | Switzerland | Strong focus on targeted oncology therapies and biologics with sophisticated delivery mechanisms | Antibody therapies, oncology biologics, targeted delivery formulations |

| Novartis | Basel | Switzerland | Leader in gene therapies and long-acting injectables leveraging advanced delivery technologies | Gene therapy platforms, ocular injectables, sustained-release formulations |

| Johnson & Johnson | New Brunswick, New Jersey | USA | Extensive pharmaceutical and medical device integration enabling advanced delivery systems | Injectable drugs, implantable devices, biologics delivery systems |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| AbbVie | North Chicago, Illinois | USA | Strong biologics pipeline using advanced antibody-based delivery systems | Immunology biologics, long-acting injectables |

| GSK | London | United Kingdom | Vaccine innovation and respiratory delivery systems | Vaccine platforms, inhalation drug delivery |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Catalent | Somerset, New Jersey | USA | Leading CDMO specializing in advanced drug delivery formulation and manufacturing | Softgel, controlled-release, biologic delivery systems |

| Lonza | Basel | Switzerland | Major CDMO enabling cell & gene therapy delivery systems | Cell/gene therapy manufacturing platforms |

By Product Type

By Technology

By Route of Administration

By Application

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar