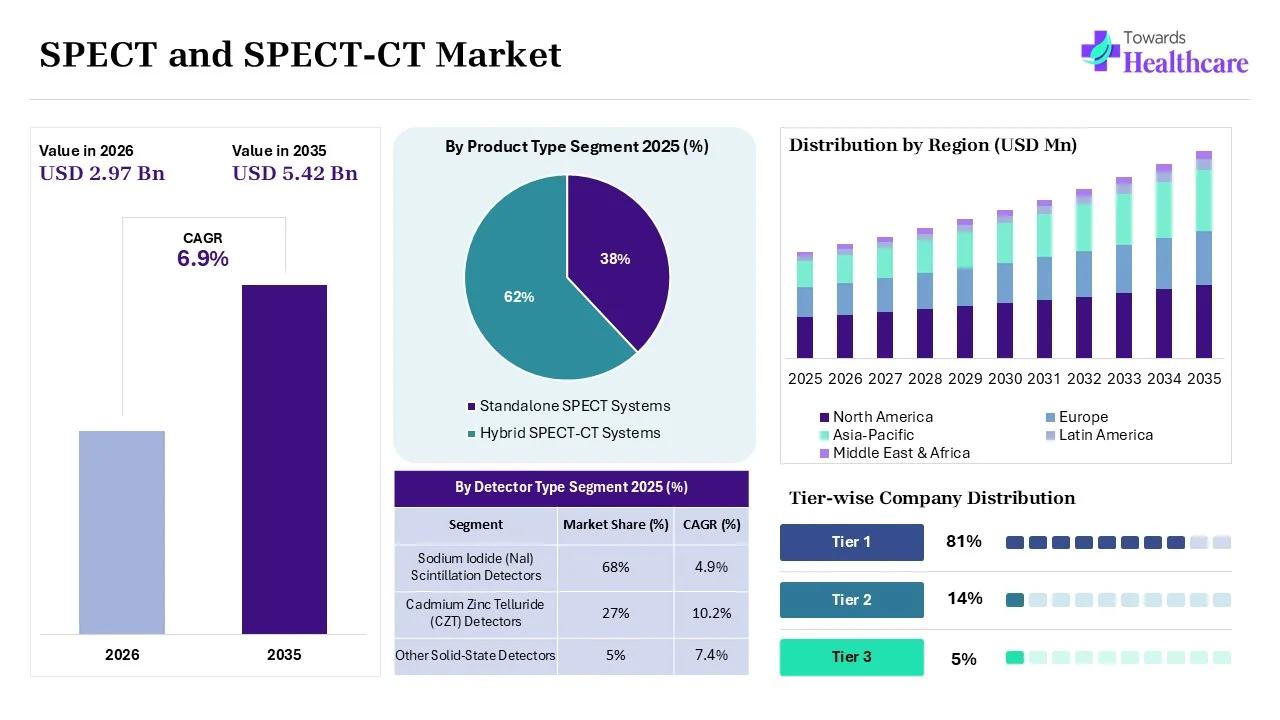

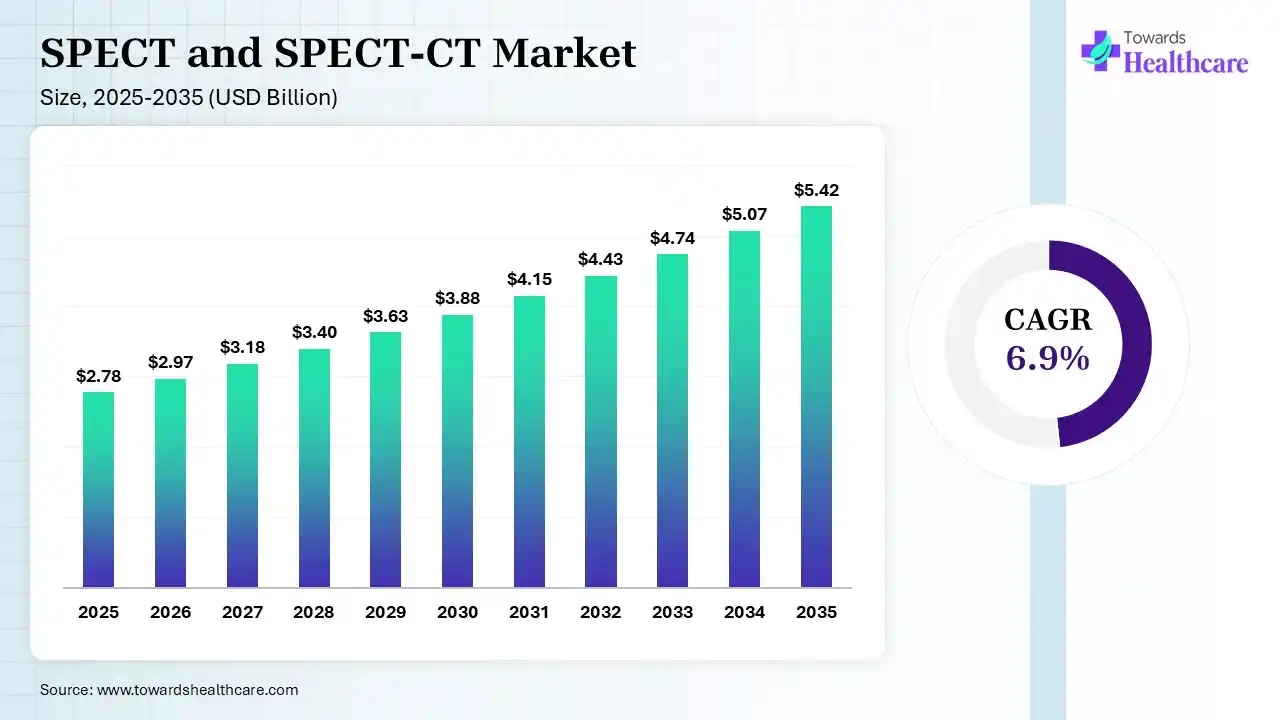

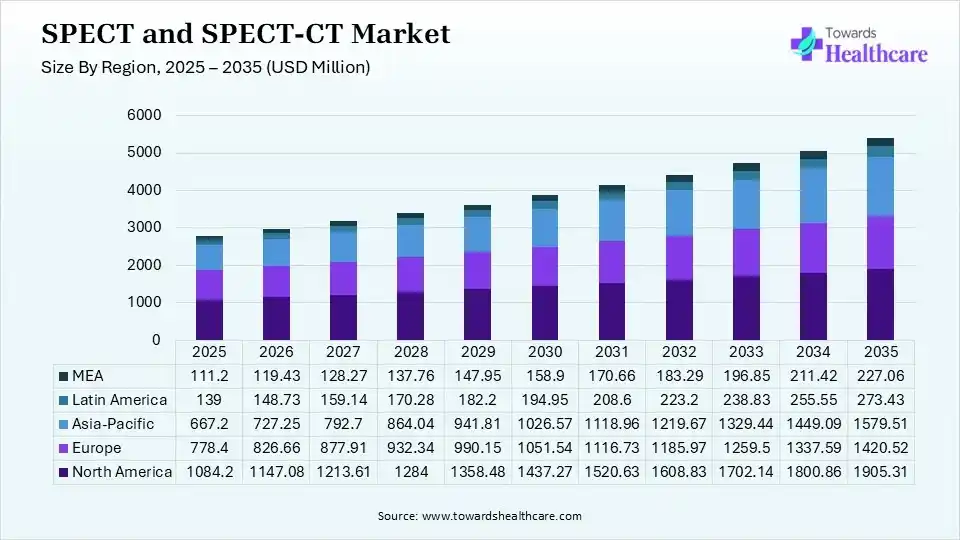

The global SPECT and SPECT-CT market size is calculated at USD 2.78 billion in 2025, driven by growth in chronic disease incidences globally. The market continues to grow USD 2.97 billion in 2026 due to the expansion of the ranostics, increasing health awareness, and AI applications. It is expected to reach USD 5.42 billion by 2035 as rising demand for personalized medicines, radiotracer advancements, expanding applications, and technological advancements accelerate market expansion. North America accounted for 39% of the market in 2025 due to its strong reimbursement systems, continuous technology upgrades, and high chronic disease burden.

")

")

The SPECT and SPECT-CT market is driven by growing chronic diseases, expansion of theranostics, and technological shift from standalone to hybrid systems. The SPECT and SPECT-CT encompass the imaging systems offering functional information and/or CT anatomical imaging of organs and tissues in one scan. SPECT utilizes radioactive tracers and a gamma camera to produce 3D images of organs, tissues, and bones, whereas SPECT-CT combines SPECT and CT technologies, offering functional or molecular and detailed anatomical imaging. This, in turn, drives their use for early and accurate disease diagnosis, monitoring disease progression, organ function assessments, treatment response monitoring, and personalized treatment planning.

With the growing burden of cardiovascular, oncology, neurological, infectious, inflammatory, and skeletal disorders worldwide, the demand for the SPECT and SPECT-CT systems is increasing. Their precise disease diagnoses, improved treatment planning, and reduced risk of false positive results also encourage their adoption rates. The availability of multiple types of SPECT and SPECT-CT scanners, including dedicated SPECT scanners, stand-alone SPECT scanners, SPECT-MRI hybrid scanners, mobile SPECT scanners, and SPECT-CT hybrid scanners, is also increasing their adoption. Furthermore, expanding applications, growing health awareness, expanding government health programs, rising demand for personalized medicines, and increasing technological advancements are also contributing to the market expansion.

The use of AI in the SPECT and SPECT-CT is increasing due to its faster scan process and reduction in noise, offering improved image quality and analysis. It is also used for abnormality detection and qualification, radiation dose optimization, treatment planning, and disease progression monitoring. They also interpret anatomical data, offering decision support and enhancing the workflow. AI also helps in more accurate functional and anatomical information extraction, as well as facilitates the integration of SPECT and SPECT-CT with other imaging modalities.

Increasing Advancements in Radiotracers

To enhance the targeting of diseases, different types of specific radiotracers are being developed, which complement the imaging systems and expand the clinical applications of SPECT and SPECT-CT systems. Their high sensitivity and specificity drive improved diagnostic capabilities and accurate disease detection. Their longer shelf life is also increasing their adoption for targeted molecular imaging and treatment monitoring. At the same time, expanding theranostics are also driving their use for paired diagnostics and personalized medicine development.

Expanding Applications

There is a rise in the demand for SPECT and SPECT-CT systems for cancer and infectious diseases diagnosis and assessment of the therapy response. It is also being used for neurology and bone disorder detection, as well as cardiovascular imaging, where they are also being utilized for therapy monitoring and risk assessment. At the same time, they are also being used for personalized treatment planning, which in turn is expanding their applications.

Growing Technological Innovations

The growing technological advancements are driving the integration of advanced image reconstruction, picture archiving & communication systems (PACS), radiology information systems (RIS), and detector technologies in SPECT and SPECT-CT. This enhances their diagnostic capabilities, image quality, sensitivity, image reconstruction, and workflow efficiency. The companies are also driving the development of low-dose imaging solutions, high-performance, and compact SPECT and SPECT-CT systems, along with software integration to offer improved safety, enhanced accessibility, and automated analysis.

| Table | Scope |

| Market Size in 2026 | USD 2.97 Billion |

| Projected Market Size in 2035 | USD 5.42 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Detector Type, By Application, By Radiopharmaceutical, By End User, By Region |

| Top Key Players | GE HealthCare , Siemens Healthineers, Spectrum Dynamics Medical, Philips Healthcare, Canon Medical Systems, United Imaging Healthcare , Mediso Medical Imaging |

")

| Segment | Share 2025 (%) |

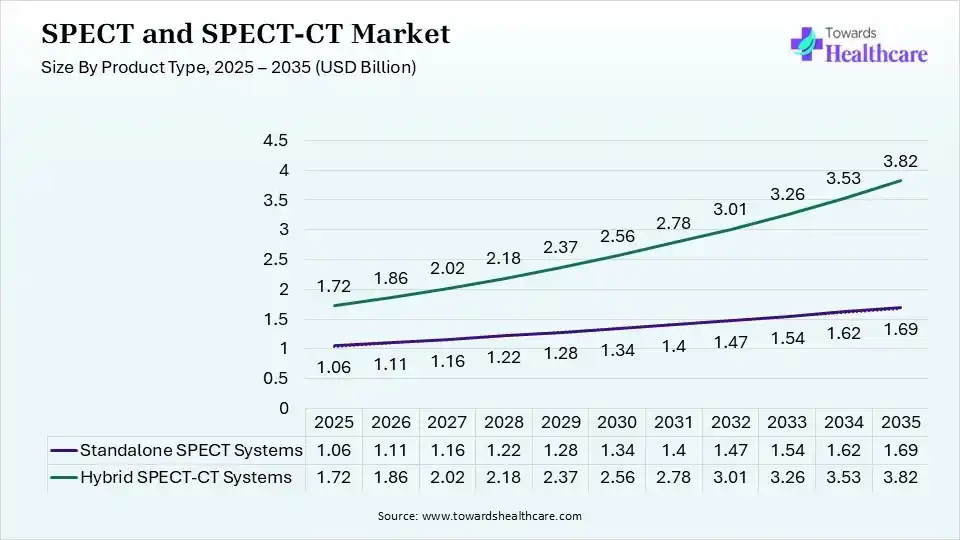

| Standalone SPECT Systems | 38% |

| Hybrid SPECT-CT Systems | 62% |

The Hybrid SPECT-CT Systems Segment Dominated the Market With 62% in 2025

The hybrid SPECT-CT systems segment led the SPECT and SPECT-CT market with a 62% share in 2025 and is expected to witness the fastest growth with a CAGR of 8.3% during the forecast period, as hybrid imaging improved anatomical localization and diagnostic confidence. Increased preference for integrated systems in oncology and cardiology has also increased their installations. Hospitals continued upgrading aging standalone systems to hybrid platforms.

The standalone SPECT systems segment held the second-largest share of 38% of the market in 2025, driven by widespread installation in hospitals with established nuclear medicine infrastructure. Lower acquisition cost also supports continued replacement demand. Emerging economies continue to adopt standalone systems for routine imaging. Their widespread availability, simple operations, and fast deployment also increase their adoption rates.

")

| Segment | Share 2025 (%) |

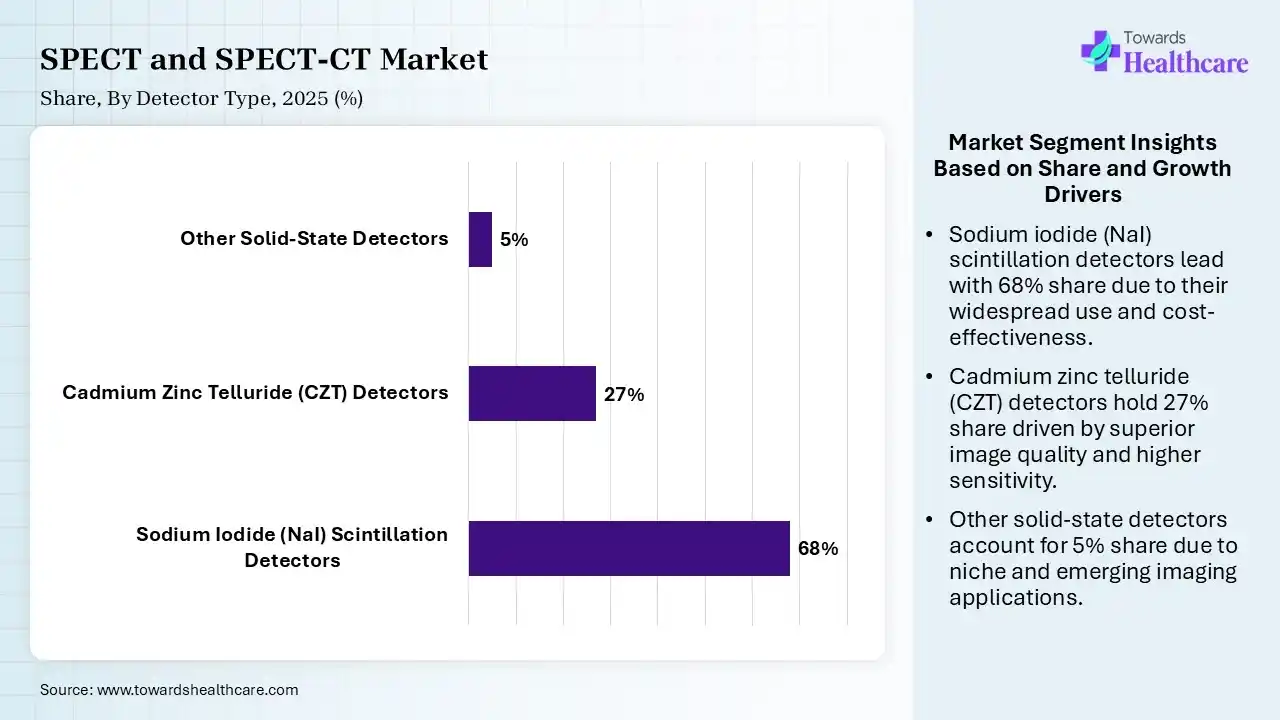

| Sodium Iodide (NaI) Scintillation Detectors | 68% |

| Cadmium Zinc Telluride (CZT) Detectors | 27% |

| Other Solid-State Detectors | 5% |

The Sodium Iodide (NaI) Scintillation Detectors Segment Dominated the Market With 68% in 2025

The sodium iodide (NaI) scintillation detectors segment accounted for the highest revenue share of 68% of the SPECT and SPECT-CT market in 2025, driven by a large installed base and lower equipment cost, which sustained their demand. Healthcare providers continued using proven technology for routine procedures. Replacement cycles remained gradual across mature markets.

The cadmium zinc telluride (CZT) detectors segment held the second-largest share of 27% of the market in 2025 and is expected to show the highest growth with a CAGR of 10.2% during the forecast period, due to superior energy resolution and higher sensitivity, improving scan quality. Growing adoption in cardiac imaging due to shortened scan time and reduced radiation dose. Premium healthcare facilities are increasingly investing in CZT technology.

The other solid-state detectors segment held 5% of the SPECT and SPECT-CT market share in 2025, driven by technological innovation that supports niche applications requiring specialized imaging performance. Research institutions evaluate advanced detector materials, which increases their use. At the same time, commercial adoption is steadily expanding.

")

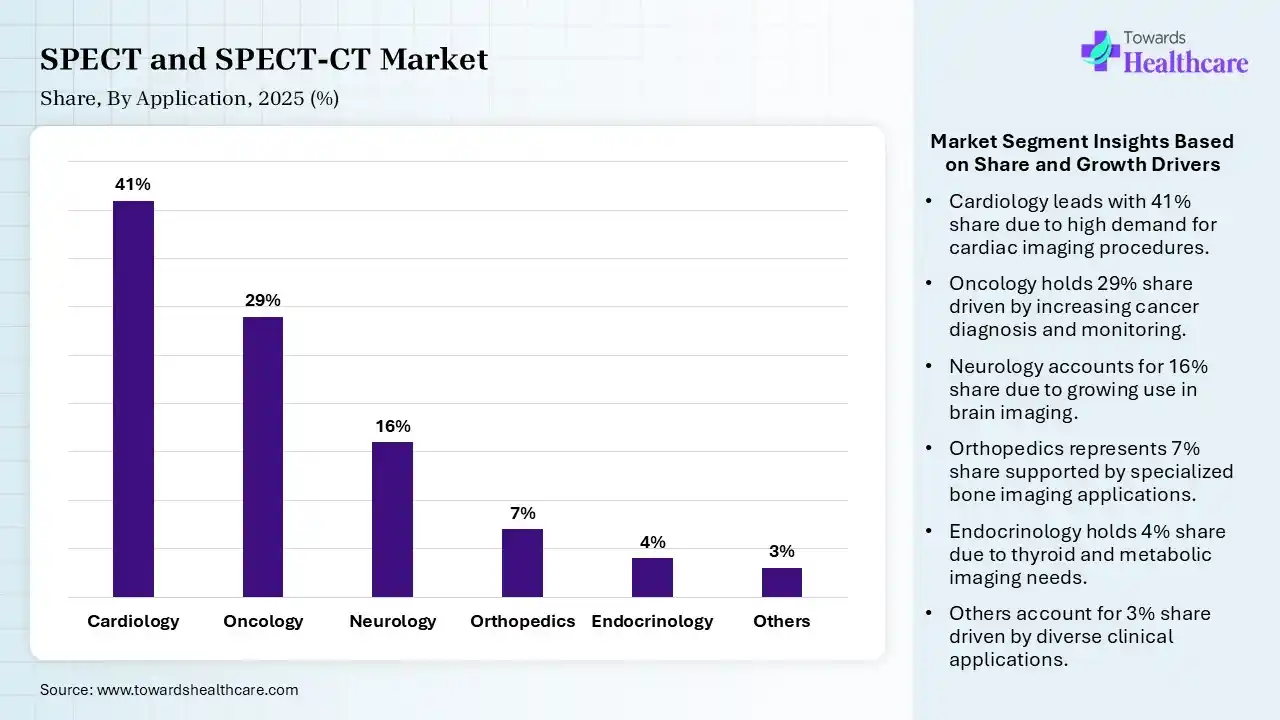

| Segment | Share 2025 (%) |

| Cardiology | 41% |

| Oncology | 29% |

| Neurology | 16% |

| Orthopedics | 7% |

| Endocrinology | 4% |

| Others | 3% |

The Cardiology Segment Dominated the Market With 41% in 2025

The cardiology segment held a major revenue share of 41% of the SPECT and SPECT-CT market in 2025, due to the rise in the burden of cardiovascular diseases, which increased the demand for myocardial perfusion imaging. Additionally, physicians relied on SPECT for functional cardiac assessment. Aging populations continued to support procedure volumes.

The oncology segment held the second-largest share of 29% of the market in 2025 and is expected to expand rapidly with a CAGR of 8.2% during the forecast period, driven by the expanding use of hybrid imaging, which improves cancer staging and treatment planning. Rising cancer prevalence increases diagnostic imaging demand, supporting the use of SPECT and SPECT-CT devices. Growing theranostics adoption supports nuclear medicine procedures.

The neurology segment held 16% of the SPECT and SPECT-CT market share in 2025, driven by increasing diagnoses of dementia and epilepsy, which support functional brain imaging. Advanced neurological evaluations require accurate perfusion assessment, which fuels the adoption of SPECT and SPECT-CT devices. Clinical awareness continues improving their utilization.

The orthopedics segment held 7% of the market share in 2025, due to a rise in bone imaging, which supports the detection of fractures and prosthetic complications. Hybrid imaging improves the localization of musculoskeletal disorders, increasing their adoption rate. Orthopedic referrals continue increasing, which supports the utilization of SPECT and SPECT-CT systems.

")

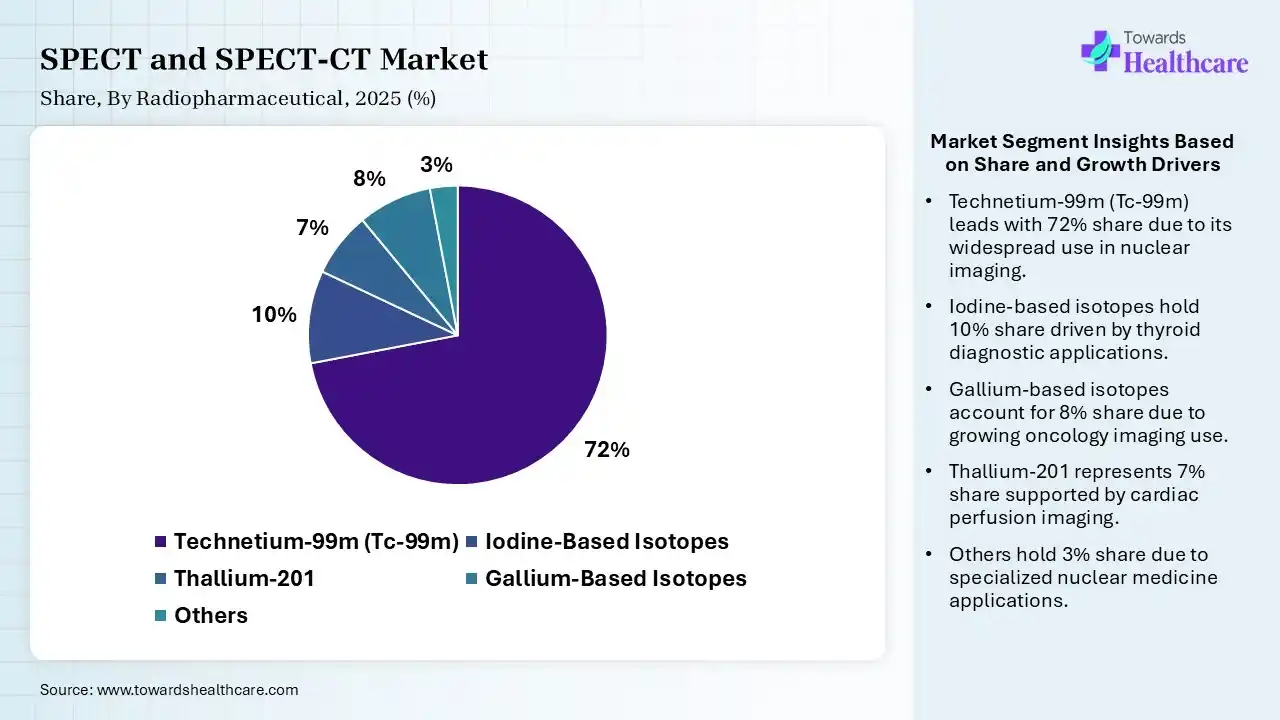

| Segment | Share 2025 (%) |

| Technetium-99m (Tc-99m) | 72% |

| Iodine-Based Isotopes | 10% |

| Thallium-201 | 7% |

| Gallium-Based Isotopes | 8% |

| Others | 3% |

The Technetium-99m (Tc-99m) Segment Dominated the Market With 72% in 2025

The technetium-99m (Tc-99m) segment contributed the biggest revenue share of 72% of the SPECT and SPECT-CT market in 2025, driven by broad clinical utility and favorable imaging characteristics, which sustained its leadership. Reliable diagnostic performance also supported extensive hospital use. Supply chain improvements also enhanced its availability.

The iodine-based isotopes segment held the second-largest share of 10% of the market in 2025, due to thyroid imaging and functional studies continuing to drive their utilization. Clinical demand remains stable across healthcare settings, which supports continued usage. At the same time, their enhanced diagnostic accuracy also supports a rise in their adoption.

The gallium-based isotopes segment held 8% of the SPECT and SPECT-CT market share in 2025 and is expected to gain the highest share with a CAGR of 9.5% during the forecast period, due to expanding oncology imaging applications accelerating adoption. Improved molecular imaging also supports precision medicine, which increases its demand. Hospitals increase access to advanced radiopharmaceuticals.

The thallium-201 segment held 7% of the market share in 2025, driven by selective cardiac imaging applications, which are maintaining consistent demand. Existing clinical protocols continue to support its use. It also helps in offering functional information as well as supports treatment planning, which increases its adoption rates.

")

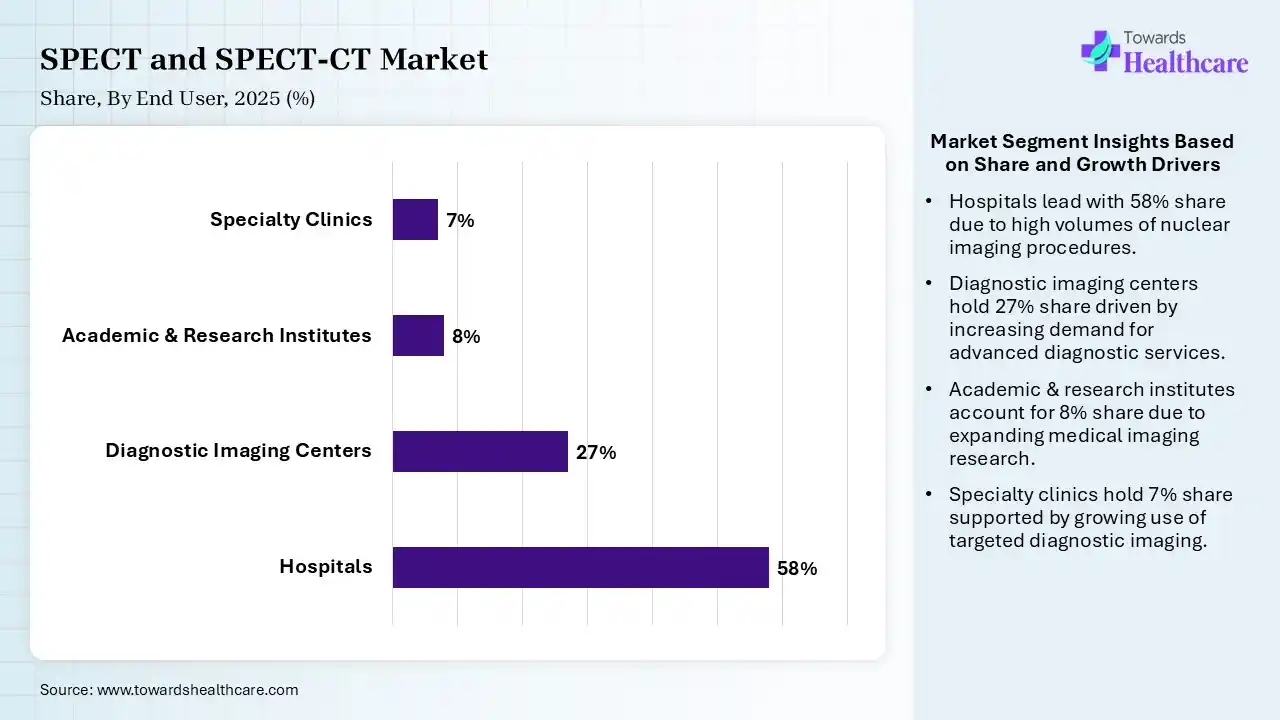

| Segment | Share 2025 (%) |

| Hospitals | 58% |

| Diagnostic Imaging Centers | 27% |

| Academic & Research Institutes | 8% |

| Specialty Clinics | 7% |

The Hospitals Segment Dominated the Market With 58% in 2025

The hospitals segment held the largest revenue share of 58% of the SPECT and SPECT-CT market in 2025, as the large patient volumes and comprehensive diagnostic services helped in sustaining their leadership. Investments in hybrid imaging platforms continued to increase. Multidisciplinary care supported procedure growth, which increased the adoption of SPECT and SPECT-CT devices.

The diagnostic imaging centers segment held the second-largest share of 27% of the market in 2025 and is expected to grow with the fastest CAGR of 8.1% during the forecast period, driven by growing outpatient imaging demand that expands independent diagnostic centers. Faster patient turnaround improves operational efficiency. Healthcare systems are increasingly outsourcing imaging services.

The academic & research institutes segment held 8% of the SPECT and SPECT-CT market share in 2025, driven by growing research funding that supports advanced nuclear medicine studies. Clinical trials require sophisticated imaging technologies, which drives the demand for SPECT and SPECT-CT devices. Universities expand molecular imaging capabilities, driving new opportunities.

The specialty clinics segment held 7% of the market share in 2025, due to specialized cardiology and oncology clinics increasing imaging utilization. Focused patient care drives equipment investments, promoting the adoption of SPECT and SPECT-CT systems. Early disease detection supports procedural growth, encouraging the use of these devices.

")

North America dominated the SPECT and SPECT-CT market with 39% in 2025, due to strong reimbursement systems, which supported nuclear imaging adoption. Continuous technology upgrades also increased equipment replacement, where a high chronic disease burden also sustained their demand. The presence of a well-developed healthcare infrastructure also increased the adoption of SPECT and SPECT-CT, where growth in healthcare spending also increased their use. Additionally, a rise in technological advancements and the presence of skilled medical imaging manufacturers also increased their adoption rates and innovations, which contributed to the market growth.

US Market Trends

The U.S. held a dominant share of 82% of the market in 2025, due to an extensive installed base and strong reimbursement support. Continuous technology replacement also increased the adoption rate of SPECT and SPECT-CT systems, where growth in chronic diseases also sustained imaging volumes across the U.S. A rise in healthcare expenditure also increased their early adoption, where the presence of advanced healthcare infrastructure also enhanced their accessibility. The presence of leading industries and skilled radiologists also increased their innovations and adoption rates. Additionally, technological advancements have also increased their innovations.

Canada Market Trends

Canada held a 12% share of the SPECT and SPECT-CT market in 2025, due to growing public healthcare investments supporting equipment modernization. Growing diagnostic demand is also increasing their installations, where research institutions are expanding nuclear imaging capabilities. Growing incidences of cancer, neurological, and cardiovascular disorders are also increasing the demand for SPECT and SPECT-CT systems, where the growing demand for personalized medicines is also increasing their use. Expanding healthcare organizations, health awareness, and collaborations are also driving the market expansion.

Asia Pacific held a 24% share of the SPECT and SPECT-CT market in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period, due to healthcare infrastructure expansion, which accelerates equipment installations like SPECT and SPECT-CT systems. Rising cancer and cardiovascular disease prevalence also boosts their demand, where government funding supports nuclear medicine growth, driving their adoption. The growing health awareness is also increasing their use, where rising demand for hybrid imaging systems and expanding medical tourism are also enhancing the market growth.

China Market Trends

China held a dominant share of 33% of the market in 2025, due to large healthcare investments accelerating equipment adoption. Expanding hospital networks are increasing imaging capacity, where cancer diagnostics continue growing rapidly, which ultimately drives the adoption of SPECT and SPECT-CT systems. Increasing chronic disease burden, demand for early disease diagnosis, and precision medicine are also promoting the adoption of these systems. Expansion of radiopharmaceutical production, medical services, and nuclear medicine departments is also increasing their use, where growing R&D activities and healthcare investments are also driving their innovation to expand their applications.

India Market Trends

India held a 16% share of the SPECT and SPECT-CT market in 2025 and is expected to grow at the fastest CAGR of 10.8% during the forecast period, due to rapid healthcare expansion, which increases nuclear imaging availability. Private hospitals are also investing in advanced systems, driving the adoption of SPECT and SPECT-CT systems, where rising chronic disease burden also drives their demand. Increasing government initiatives and healthcare expenditures are also enhancing access to advanced imaging systems. At the same time, growing R&D activities, training programs, and health awareness are also increasing their use for early and accurate disease diagnosis.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | SPECT and SPECT-CT Systems |

| GE HealthCare | Chicago, U.S. | NM/CT 800 Series |

| Siemens Healthineers | Erlangen, Germany | Symbia Pro. specta, Symbia Evo, and Symbia Intevo |

| Spectrum Dynamics Medical | Caesarea, Israel | VERITON-CT and D-SPECT |

| Philips Healthcare | Amsterdam, Netherlands | Incisive CT, Vereos, and BrightView XCT |

| Canon Medical Systems | Otawara, Japan | Cartesion Prime, Aquilion integrated hybrid solutions, and GCA-9300R |

| United Imaging Healthcare | Shanghai, China | uMi series, advanced hybrid molecular imaging platforms, and uCT series |

| Mediso Medical Imaging | Budapest, Hungary | AnyScan TRIO and nanoScan |

In May 2025, after receiving U.S. FDA 510(k) clearance for Aurora nuclear medicine system and Clarify DL by GE HealthCare, the MD Chair, Department of Radiology, Radiologist-in-Chief, Donna Plecha, along with MD Chair in Radiology, at University Hospitals Ida and Irwin Haber and Wei-Shen Chin, expressed that, “We are thrilled to be the first in the United States to adopt this incredibly impressive technology,” “Aurora’s seamless integration of SPECT and CT components will allow us to perform comprehensive, high-quality diagnostic exams in a single session, while its support of Clarify DL deep-learning image reconstruction enables enhanced image quality performance.”

By Product Type

By Detector Type

By Application

By Radiopharmaceutical

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar