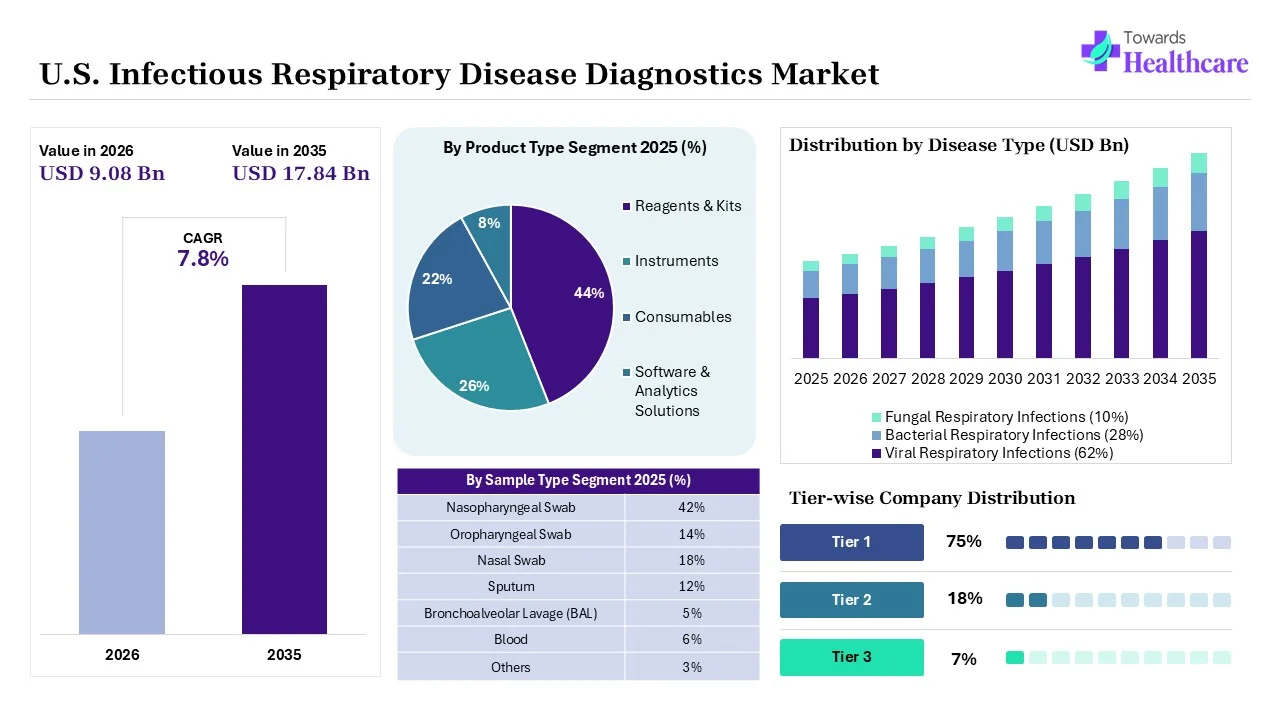

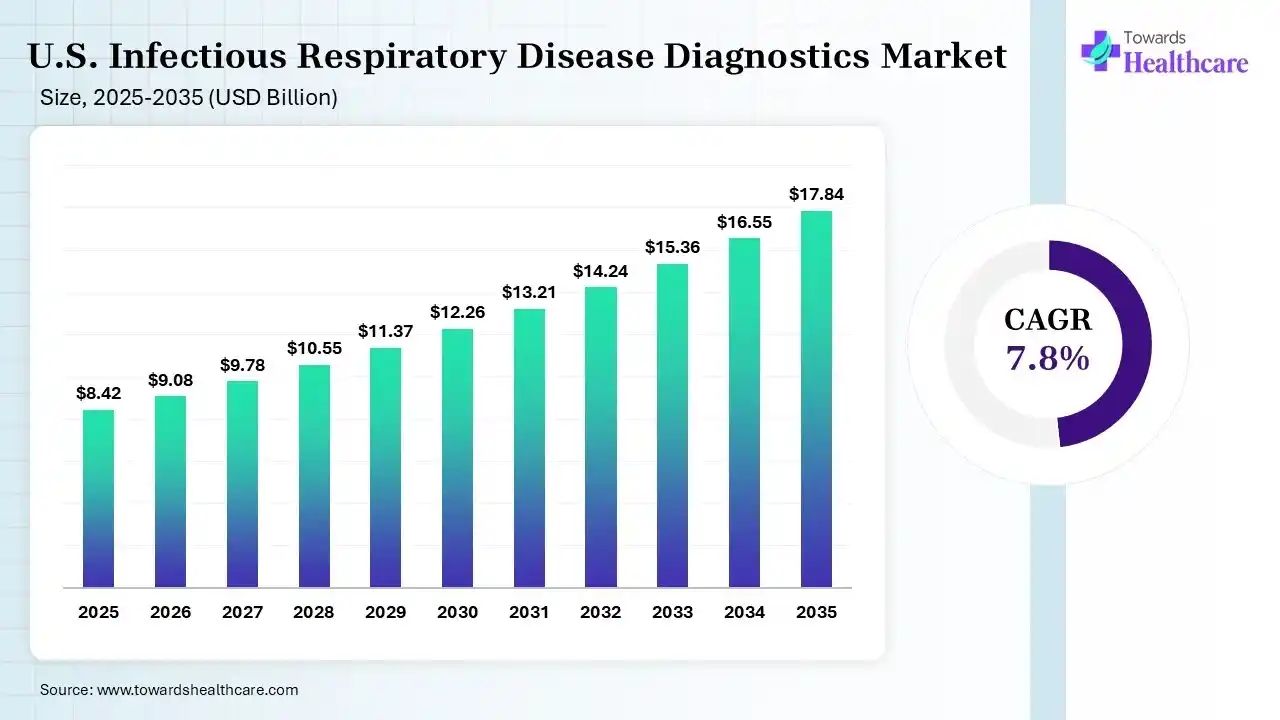

The U.S. infectious respiratory disease diagnostics market size was estimated at USD 8.42 billion in 2025 and is predicted to increase from USD 9.08 billion in 2026 to approximately USD 17.84 billion by 2035, expanding at a CAGR of 7.8% from 2026 to 2035.

")

The U.S. infectious respiratory disease diagnostics market is driven by continuous growth in bacterial infections, a shift towards decentralized healthcare settings, and rapid advancements in multiplex and POC molecular technologies. The U.S. infectious respiratory disease diagnostics encompass tests, products, technologies, and services for the detection, monitoring, and identification of infectious diseases across the U.S. The infectious respiratory diseases refer to the infections caused by viruses, fungi, bacteria, and other microorganisms affecting the respiratory tract. Most commonly found infectious respiratory diseases across the U.S. are COVID-19, RSV, influenza, TB, pneumonia, etc, which drives the demand for their diagnostic solutions.

The growing incidence of these respiratory infectious diseases across the U.S. is driving the demand for various diagnostic solutions for their early and acute detection. Moreover, the U.S. infectious respiratory disease diagnostics also help in reducing their transmission, solidify infection control, support public health surveillance, and strengthen outbreak preparedness. This, in turn, is driving the development and adoption of various molecular diagnostics, immunodiagnostics, multiplex respiratory panels, point-of-care diagnostic testing, and microbiology-based testing solutions. Additionally, growing technological advancements and health awareness are also driving the development of new portable and biosensor-based diagnostic devices.

AI offers a wide range of applications in the U.S. infectious respiratory disease diagnostics market, where it helps enhance diagnostic accuracy and image interpretation. It also helps in accelerating the diagnosis time, analyzing large volumes of diagnostic datasets, and supports real-time surveillance and predicts disease progression. AI also helps in the identification of infection patterns, predicts disease outbreaks, differentiates between viral, bacterial, and fungal infections, and helps in automating laboratory workflow, reducing manual errors.

Growing Public Health Surveillance

Growing government investments across the U.S. are increasing the infectious disease monitoring programs, which are driving the demand for infectious respiratory disease diagnostics. Expanding real-time surveillance and pandemic preparedness are also increasing the adoption of various infectious respiratory disease diagnostics to control respiratory infection outbreaks. This, in turn, is driving the frequent testing of various infectious respiratory diseases, boosting the demand for their reagents, kits, and consumables as well.

Expanding Multiplex Testing

The high efficiency and simultaneous detection of various infectious respiratory diseases are increasing the demand for multiplex testing. They are being utilized to identify influenza, adenovirus, RSV, COVID-19, and multiple other pathogens, and they also help in the selection of appropriate treatment. They also help in reducing diagnostic time, eliminating the need for multiple separate tests, and their increased accuracy and affordability also drive their adoption across various hospitals and laboratories.

Rising Demand for Point-of-Care Testing

Growing health awareness and expanding home healthcare are driving the demand for point-of-care testing solutions. They also support decentralized healthcare, remote patient monitoring, and enhance accessibility and patient convenience, which increases their adoption rates. At the same time, growing advances are also driving the development of new, easy-to-use, portable, rapid antigen testing technologies, creating new opportunities for advanced POC testing solutions. Moreover, growing telemedicine platforms and demand for convenient testing solutions are also increasing their use.

| Table | Scope |

| Market Size in 2026 | USD 9.08 Billion |

| Projected Market Size in 2035 | USD 17.84 Billion |

| CAGR (2026 - 2035) | 7.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Disease Type, By Diagnostic Technology, By Product, By Test Type, By End User, By Sample Type |

| Top Key Players | bioMerieux, QuidelOrtho Corporation, Abbott Laboratories, Becton, Dickinson and Company (BD), F. Hoffmann-La Roche Ltd, QIAGEN, Cepheid |

")

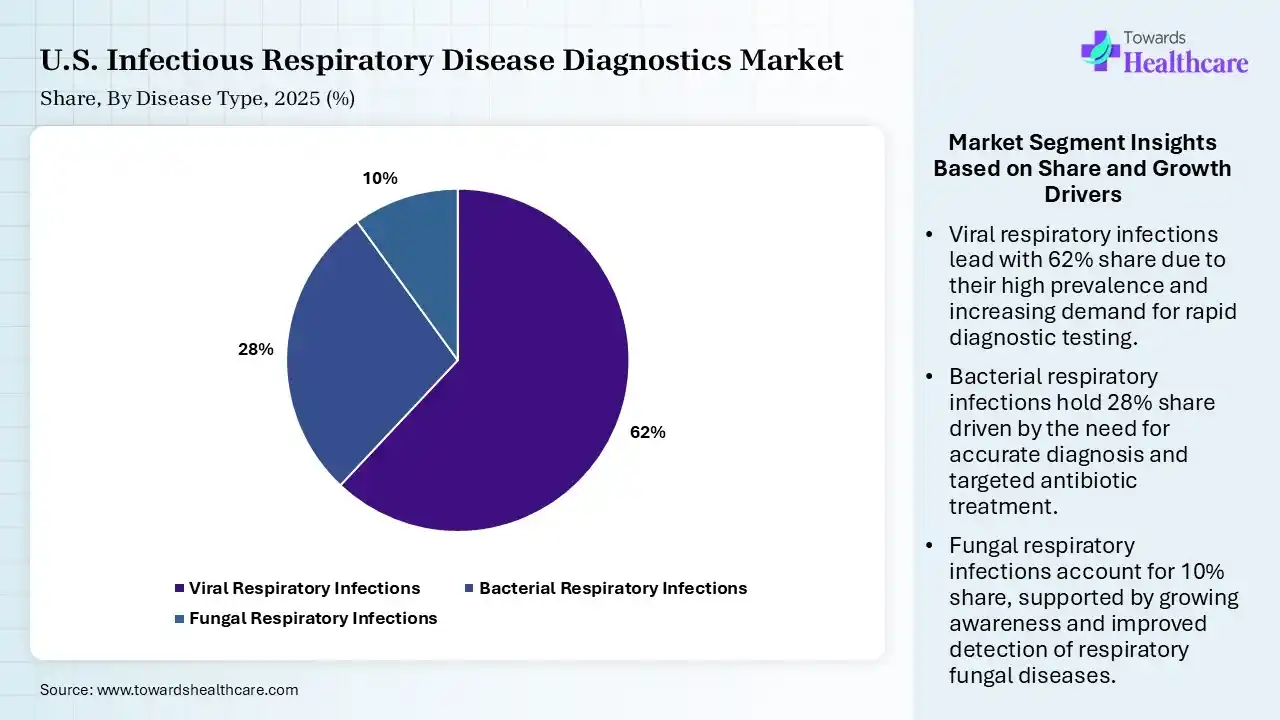

| Segment | Share 2025 (%) |

| Viral Respiratory Infections | 62% |

| Bacterial Respiratory Infections | 28% |

| Fungal Respiratory Infections | 10% |

The Viral Respiratory Infections Segment Dominated the Market With 62% in 2025

The viral respiratory infections segment led the U.S. infectious respiratory disease diagnostics market with a 62% share in 2025, driven by a rise in viral outbreaks, which increased the testing volumes. Multiplex panels improve detection rates, which increases their adoption rates. At the same time, the public health surveillance also promoted their adoption.

The bacterial respiratory infections segment held the second-largest share of 28% of the market in 2025, due to growing antimicrobial resistance, which increases diagnostic demand. Their early detection also supports treatment decisions, which increase the use of various diagnostic solutions. Hospital testing volumes remain strong, which contributes to their increased use.

The fungal respiratory infections segment held 10% of the U.S. infectious respiratory disease diagnostics market share in 2025 and is expected to witness the fastest growth with a CAGR of 9.2% during the forecast period, due to expanding immunocompromised patient populations. Growing advanced fungal assays are also improving the diagnostic accuracy. Awareness of invasive infections continues to rise, which drives their demand.

")

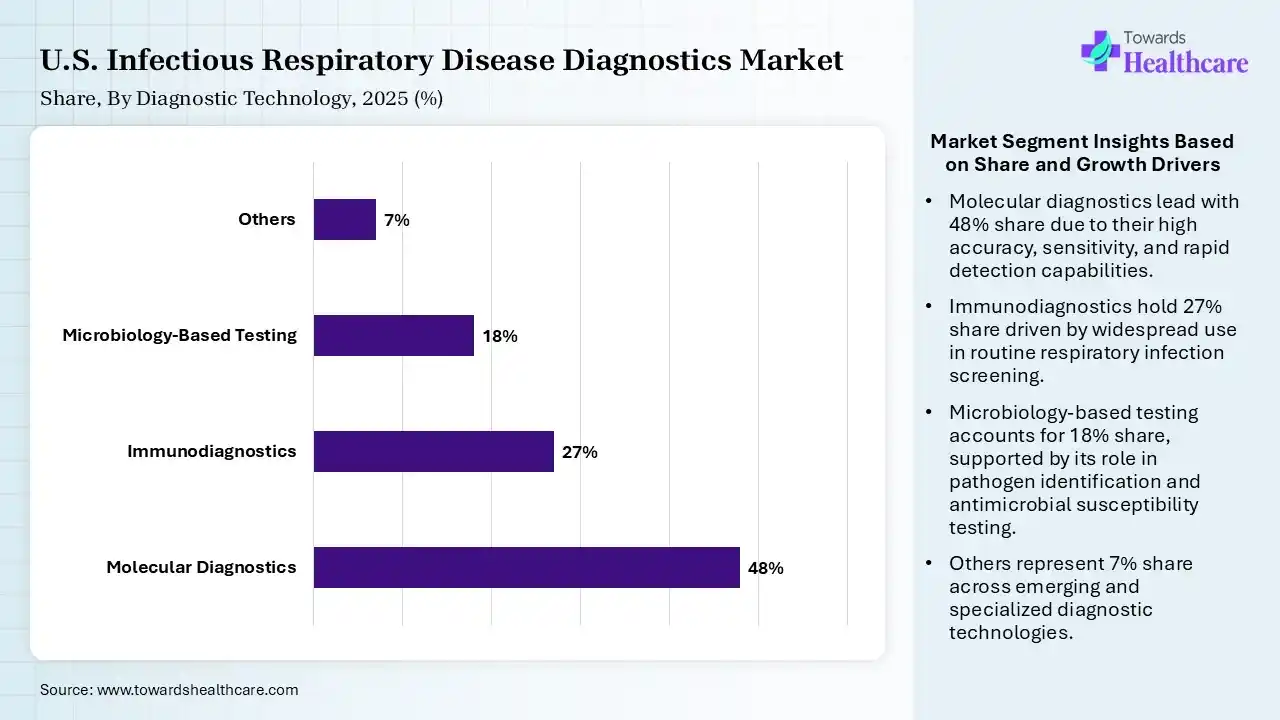

| Segment | Share 2025 (%) |

| Molecular Diagnostics | 48% |

| Immunodiagnostics | 27% |

| Microbiology-Based Testing | 18% |

| Others | 7% |

The Molecular Diagnostics Segment Dominated the Market With 42% in 2025

The molecular diagnostics segment accounted for the highest revenue share of 48% of the U.S. infectious respiratory disease diagnostics market in 2025 and is expected to show the highest growth with a CAGR of 9.3% during the forecast period, due to its high sensitivity, which accelerated clinical adoption. Multiplex testing also improved workflow efficiency. The rise in the demand for rapid pathogen identification has also increased their use.

The immunodiagnostics segment held the second-largest share of 27% of the market in 2025, due to cost-effective testing, which supports its broad utilization. Their rapid assays also enhance accessibility, promoting their use for the detection of a wide range of infectious respiratory diseases. The rise in the screening programs is also sustaining their demand.

The microbiology-based testing segment held 18% of the U.S. infectious respiratory disease diagnostics market share in 2025, due to their increase use for confirmatory testing, which remains clinically important. Laboratories continue culture-based analysis, which drives their demand. At the same time, antibiotic stewardship also supports their usage.

The others segment held 7% of the market share in 2025, driven by emerging biosensors that improve turnaround time. Moreover, growing innovations are also supporting the adoption of various infectious respiratory disease diagnostics in specialized settings. Growing automation is also enhancing diagnostic efficiency, driving its adoption rates.

")

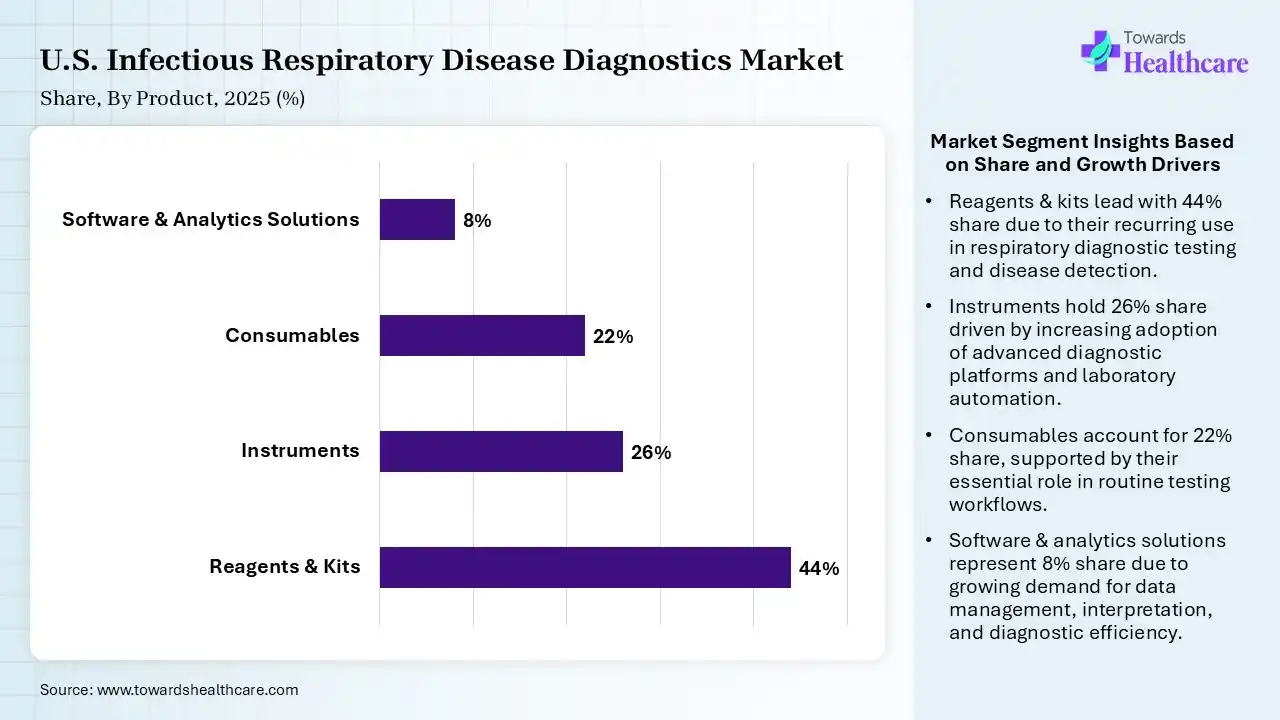

| Segment | Share 2025 (%) |

| Reagents & Kits | 44% |

| Instruments | 26% |

| Consumables | 22% |

| Software & Analytics Solutions | 8% |

The Reagents & Kits Segment Dominated the Market With 44% in 2025

The reagents & kits segment held a major revenue share of 44% of the U.S. infectious respiratory disease diagnostics market in 2025, driven by recurring testing, which drives repeated purchases. At the same time, expanded respiratory panels also contributed to their increased consumption. Laboratories require continuous replenishment, which increases their adoption rates.

The instruments segment held the second-largest share of 26% of the market in 2025, due to rising automation investments, which are improving laboratory capacity. Advanced analyzers support high-throughput detection, where their improved accuracy and multiplex testing are also increasing their use. Replacement cycles also sustain revenues, and expanding laboratory infrastructure is also promoting their installation.

The consumables segment held 22% of the U.S. infectious respiratory disease diagnostics market share in 2025, due to a continuous rise in sample collection volumes and growing innovations. Routine testing and expansion in point-of-care testing are also supporting their consistent demand. Well-established distribution networks also enhance their availability.

The software & analytics solutions segment held 8% of the market share in 2025 and is expected to expand rapidly with a CAGR of 10.2% during the forecast period, driven by digital workflows, which improve laboratory productivity. AI-enabled analytics also enhance interpretation, driving their demand. Their high connectivity also supports surveillance initiatives, promoting their use.

")

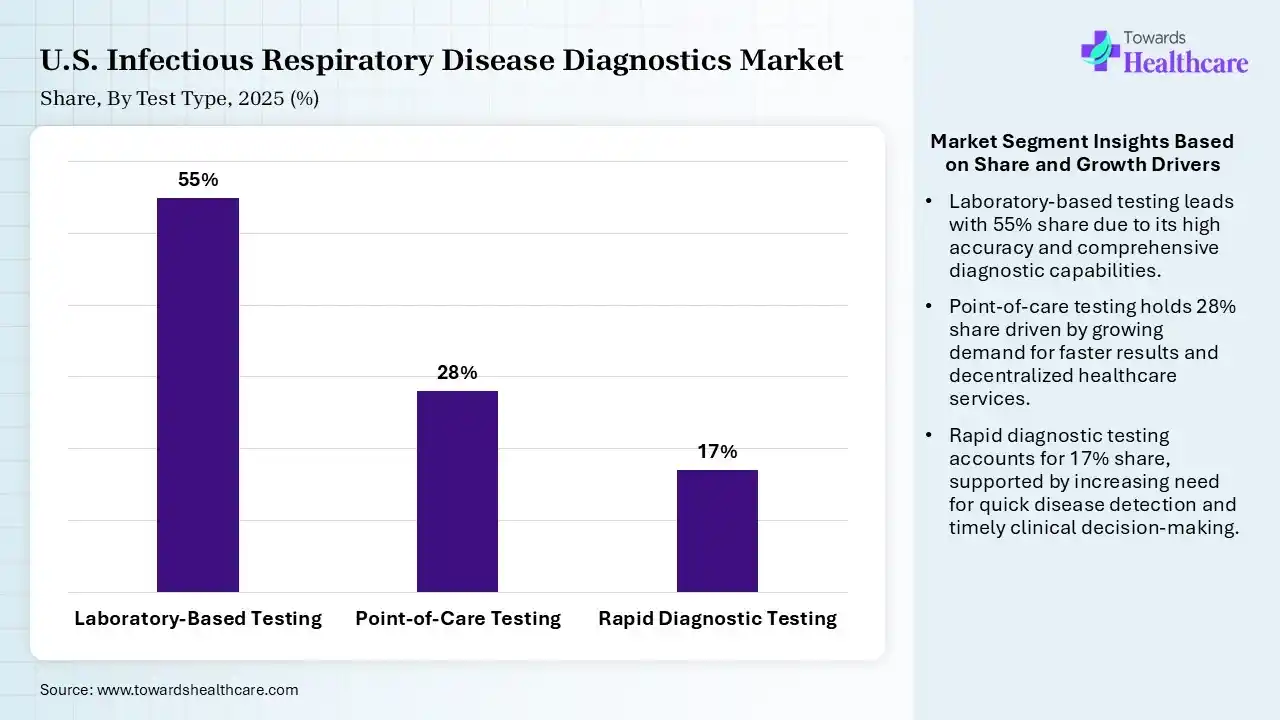

| Segment | Share 2025 (%) |

| Laboratory-Based Testing | 55% |

| Point-of-Care Testing | 28% |

| Rapid Diagnostic Testing | 17% |

The Laboratory-Based Testing Segment Dominated the Market With 55% in 2025

The laboratory-based testing segment contributed the biggest revenue share of 55% of the U.S. infectious respiratory disease diagnostics market in 2025, due to high testing volumes handled by the centralized laboratories. The growth in their advanced platforms also improved accuracy, which increased their use. Reimbursement support also promoted their adoption and accessibility.

The point-of-care testing segment held the second-largest share of 28% of the market in 2025 and is expected to gain the highest share with a CAGR of 9.4% during the forecast period, driven by rapid decision-making, which improves patient management. Their decentralized testing also expands their accessibility. Technological improvements increase reliability, promoting their use.

The rapid diagnostic testing segment held 17% of the U.S. infectious respiratory disease diagnostics market share in 2025, as it drives short turnaround times, which support its widespread use. A rise in the community screening programs also increases their demand. Additionally, they offer enhanced convenience, which drives their adoption rates.

")

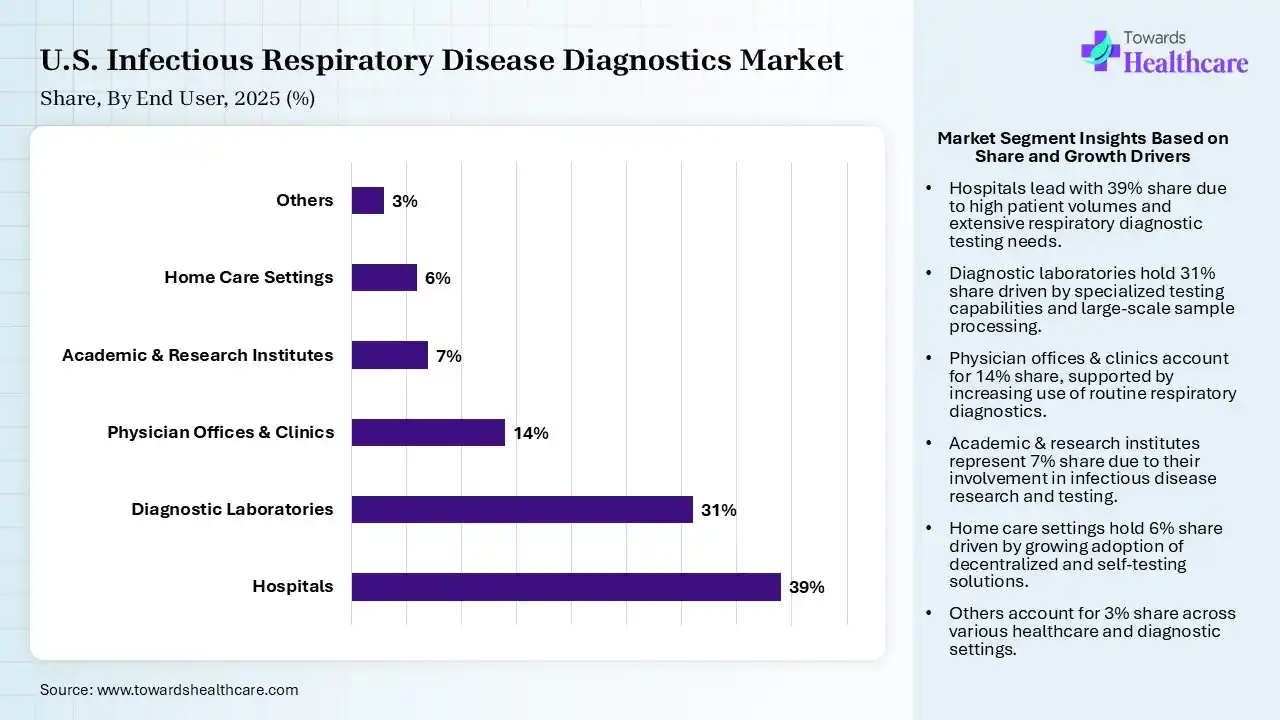

| Segment | Share 2025 (%) |

| Hospitals | 39% |

| Diagnostic Laboratories | 31% |

| Physician Offices & Clinics | 14% |

| Academic & Research Institutes | 7% |

| Home Care Settings | 6% |

| Others | 3% |

The Hospitals Segment Dominated the Market With 39% in 2025

The hospitals segment held the largest revenue share of 39% of the U.S. infectious respiratory disease diagnostics market in 2025, due to high patient inflow, which supported the testing demand. The presence of advanced laboratories enables comprehensive diagnostics, which attracts patients. Growth in infection control programs also promoted infectious respiratory disease diagnostics utilization.

The diagnostic laboratories segment held the second-largest share of 31% of the market in 2025, driven by growing outsourcing trends, which increase volumes. The presence of high-throughput systems also improves diagnostic efficiency, which increases their use. At the same time, the presence of expanded test menus also supports their growth.

The physician offices & clinics segment held 14% of the U.S. infectious respiratory disease diagnostics market share in 2025, driven by increasing point-of-care adoption, which enhances accessibility. Their early diagnosis also improves treatment decisions. Moreover, the high volume of outpatient visits and the expansion of community clinics are also driving their demand.

The home care settings segment held 6% of the market share in 2025 and is expected to grow with the fastest CAGR of 10.5% during the forecast period, due to the continuous rise in self-testing solution adoption. Increasing consumer awareness is also supporting the infectious respiratory disease diagnostics utilization. Convenient diagnostic options are also expanding their availability.

The U.S. infectious respiratory disease diagnostics market is expected to experience significant growth during the forecast period, due to the presence of well-established healthcare infrastructure and favourable reimbursement policies, which are enhancing accessibility to various diagnostic technologies. Growth in respiratory infections and health awareness is also increasing their demand, and the expansion in government initiatives is also increasing their use for infectious disease surveillance. A rise in investments and collaborations is also promoting the development of new molecular, POC tests, and home-based diagnostic tests, enhancing the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | U.S. Infectious Respiratory Disease Diagnostics |

| bioMerieux | Durham, U.S. | BIOFIRE Respiratory Panel 2.1 and BIOFIRE SPOTFIRE Respiratory Panel |

| QuidelOrtho Corporation | San Diego, U.S. | Sofia 2 Flu=SARS-CoV-2 FIA and Solana Respiratory Viral Panel |

| Abbott Laboratories | Abbott Park, U.S. | ID NOW Influenza A&B/COVID-19/RSV and Alinity m Resp 4-Plex |

| Becton, Dickinson and Company (BD) | Franklin Lakes, U.S. | BD Veritor Plus System and BD MAX Respiratory Viral Panel |

| F. Hoffmann-La Roche Ltd | Basel, Switzerland | Cobas Respiratory 4-flex and Cobas Liat Influenza A/B & COVID-19 |

| QIAGEN | Venlo, Netherlands | QIAstat-Dx Respiratory Panel Plus |

| Cepheid | Sunnyvale, California | Xpert Xpress MVP and Xpert Xpress CoV-2/Flu/RSV plus |

In October 2025, after the submission of Simplicity Dx Respiratory Panel for simultaneous detection of SARS-CoV-2 (COVID-19), Respiratory Syncytial Virus (RSV), Influenza A, Influenza B, the CEO of Molecular Designs Michael Clark expressed that, "Submitting our IVD product to the FDA is an important milestone," "It reflects our commitment to giving labs tools that are not only clinically sound, but also practical and efficient to use. Our goal is to help labs streamline testing workflows without sacrificing accuracy or flexibility."

By Disease Type

By Diagnostic Technology

By Product

By Test Type

By End User

By Sample Type

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar