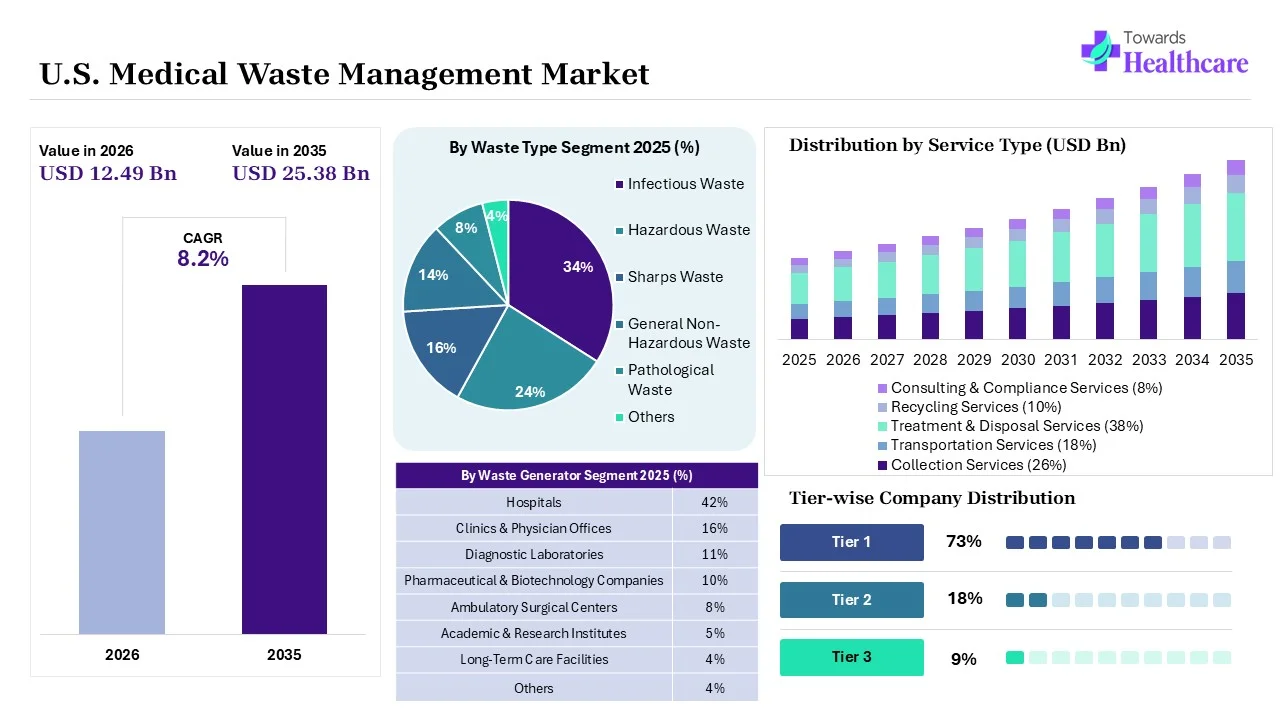

The U.S. medical waste management market size was estimated at USD 11.54 billion in 2025 and is predicted to increase from USD 12.49 billion in 2026 to approximately USD 25.38 billion by 2035, expanding at a CAGR of 8.20% from 2026 to 2035.

")

The U.S. medical waste management market is driven by a growing chronic disease burden, stringent regulations, and a shift towards sustainable technologies. The U.S. medical waste management encompasses the systematic collection, segregation, treatment, transportation, disposal, and recycling of the medical waste generated in healthcare facilities. The hospitals, clinics, research centres, laboratories, pharmacies, and nursing homes generate a wide range of infectious, pharmaceutical, pathological, and sharp waste, which increases their demand for proper, efficient, and safe medical waste management solutions. Expanding stringent regulatory requirements are also driving the adoption of these solutions to reduce environmental impact, infectious disease transmission, and protect public health.

The medical waste management solutions across the U.S. are used for the disposal of used medical supplies, handling and treatment of chemical and biological waste, and management of expired and unused waste. They also help in the treatment of biohazardous waste, the disposal of blood-contaminated materials, and the management of sharp and surgical waste. They employ various techniques such as incineration, autoclaving, thermal treatment, microwave treatment, chemical treatments, and landfilling to destroy, sterilize, or neutralize various medical wastes. At the same time, the companies are developing various AI-based waste segregation, IoT-based smart waste monitoring, digital tracking, and advanced sterilization systems to improve and automate waste transportation, handling, and tracking, along with regulatory compliance and minimized environmental impact.

The use of AI in the U.S. medical waste management market is increasing as it helps in the automatic identification of different types of waste categories, promoting their sorting and segregation. It also helps in optimization of waste capacity planning, collection, real-time tracking, waste bins management, and treatment processes, as well as promotes sustainability enhancements. AI also helps in safety management, disposal supply maintenance, development of smart containers, and supports regulatory compliance monitoring.

Sustainable Waste Management on the Rise

The growing shift towards environmentally friendly waste management procedures is promoting sustainable waste management practices across the U.S. healthcare sector. This, in turn, is increasing the demand for non-incineration technologies such as microwave treatment, advanced sterilization systems, and autoclaving to reduce the environmental impact. Additionally, growing investments and resource recovery programs are also driving the use of various waste segregation, recycling, and other eco-friendly solutions to reduce landfill usage and lower carbon emissions.

Growing Regulatory Compliance Requirements

With the rising healthcare waste generation in the U.S., the demand for safe and effective waste management solutions is also increasing, and the regulatory agencies are also introducing new regulations. They are focusing on strengthening the medical waste handling, disposal, transportation, and treatment, as well as reducing emissions and implementing sustainable waste management methods. This is driving the adoption of advanced technologies, disposal solutions, and digital solutions for regulatory auditing, documentation, and compliance-focused waste management.

Technological Advancement

The growing investments and collaborations are driving the development of new technologies to enhance the waste segregation, treatment, transportation, and tracking efficiencies. They are also focusing on enhancing sterilization efficiency, waste category identification, reducing contamination risks, and regulatory compliance. This, in turn, is driving the development of smart waste containers, advanced tracking technologies, digital tracking platforms, and automated reporting systems.

| Table | Scope |

| Market Size in 2026 | USD 12.49 Billion |

| Projected Market Size in 2035 | USD 25.38 Billion |

| CAGR (2026 - 2035) | 8.20% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Waste Type, By Treatment Method, By Service Type, By Waste Generator, By Treatment Site |

| Top Key Players | Waste Management Inc. (WM), Daniels Health, Clean Harbors, Inc., Sharps Compliance, Inc., Republic Services, Inc., Veolia North America, Triumvirate Environmental |

")

| Segments | Shares % |

| Infectious Waste | 34% |

| Hazardous Waste | 24% |

| Sharps Waste | 16% |

| General Non-Hazardous Waste | 14% |

| Pathological Waste | 8% |

| Others | 4% |

The Infectious Waste Segment Dominated the Market With 34% in 2025

The infectious waste segment led the U.S. medical waste management market with a 34% share in 2025, due to growth in hospital admissions, which increased infectious waste volumes. Infection control regulations also increased segregation requirements. A rise in healthcare utilization also supported the sustained generation of infectious waste, which promoted the demand for proper waste management.

The hazardous waste segment held the second-largest share of 24% of the market in 2025, as pharmaceutical and chemical waste volumes continue rising due to increasing R&D activities. Strict EPA compliance requirements also increase treatment demand for hazardous waste. Advanced disposal technologies are also improving management efficiency.

The sharps waste segment held 16% of the U.S. medical waste management market share in 2025, as higher injection-based therapies are increasing sharps waste generation. Safety regulations and expanding healthcare infrastructure also require specialized containment. Home healthcare and rising chronic diseases also expand disposal requirements.

The pathological waste segment held 8% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 8.8% during the forecast period, due to surgical procedures continuing to increase nationwide. Advanced pathology testing is also driving tissue disposal needs. Regulatory oversight also supports specialized treatment demand.

")

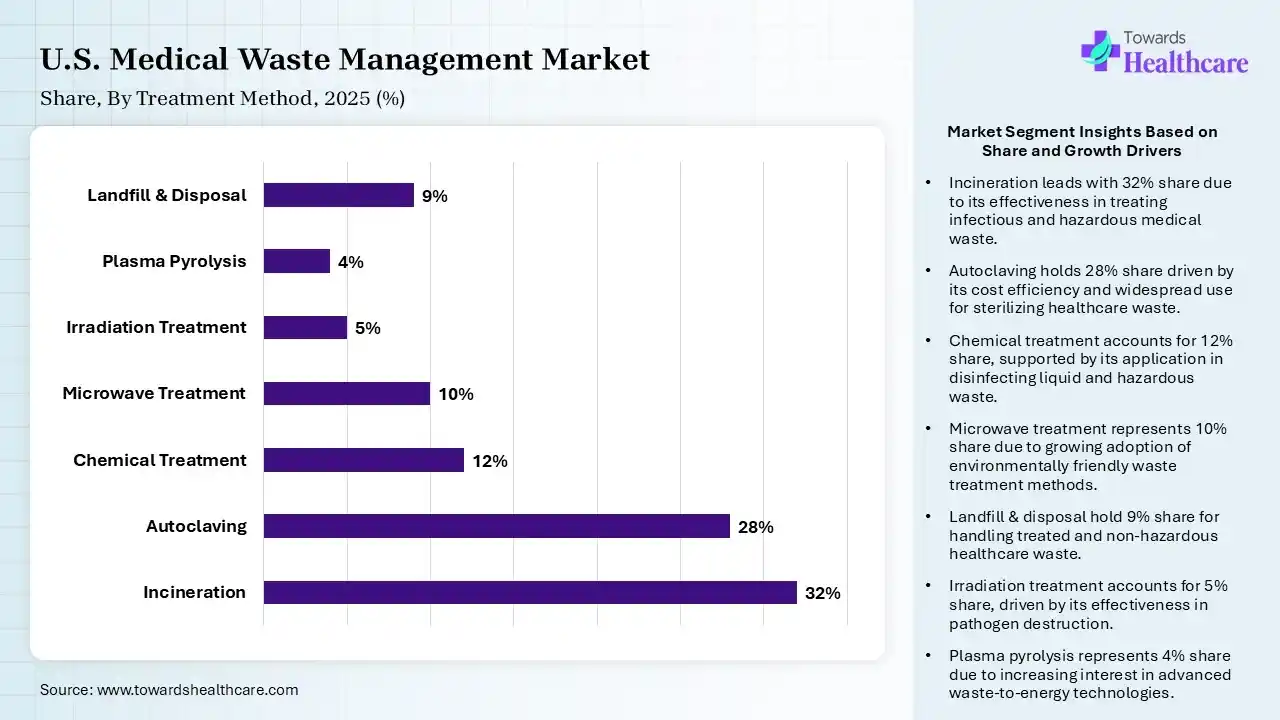

| Segments | Shares % |

| Incineration | 32% |

| Autoclaving | 28% |

| Chemical Treatment | 12% |

| Microwave Treatment | 10% |

| Irradiation Treatment | 5% |

| Plasma Pyrolysis | 4% |

| Landfill & Disposal | 9% |

The Incineration Segment Dominated the Market With 32% in 2025

The incineration segment accounted for the highest revenue share of 32% of the U.S. medical waste management market in 2025, as it handles high-risk medical waste effectively. Established infrastructure also supported large treatment volumes, which increased the demand for the incineration method. Regulatory acceptance also helped in maintaining its utilization.

The autoclaving segment held the second-largest share of 28% of the market in 2025, as it is an environmentally preferable treatment option that is gaining adoption for a wide range of medical waste management. Hospitals seek lower-emission alternatives, which also fuel their adoption rates. Cost efficiency also improves their market penetration.

The chemical treatment segment held 12% of the U.S. medical waste management market share in 2025, as they are effective for liquid and pharmaceutical waste streams, which increases its use across various laboratories and institutions. Compliance requirements also encourage chemical neutralization, which drives their demand. Growing technological improvements also expand their applications.

The plasma pyrolysis segment held 4% of the market share in 2025 and is expected to show the highest growth with a CAGR of 10.8% during the forecast period, due to the increasing investment in sustainable treatment technologies. Emission reduction goals also encourage their deployment. Advanced waste-to-energy capabilities are also attracting the operators.

")

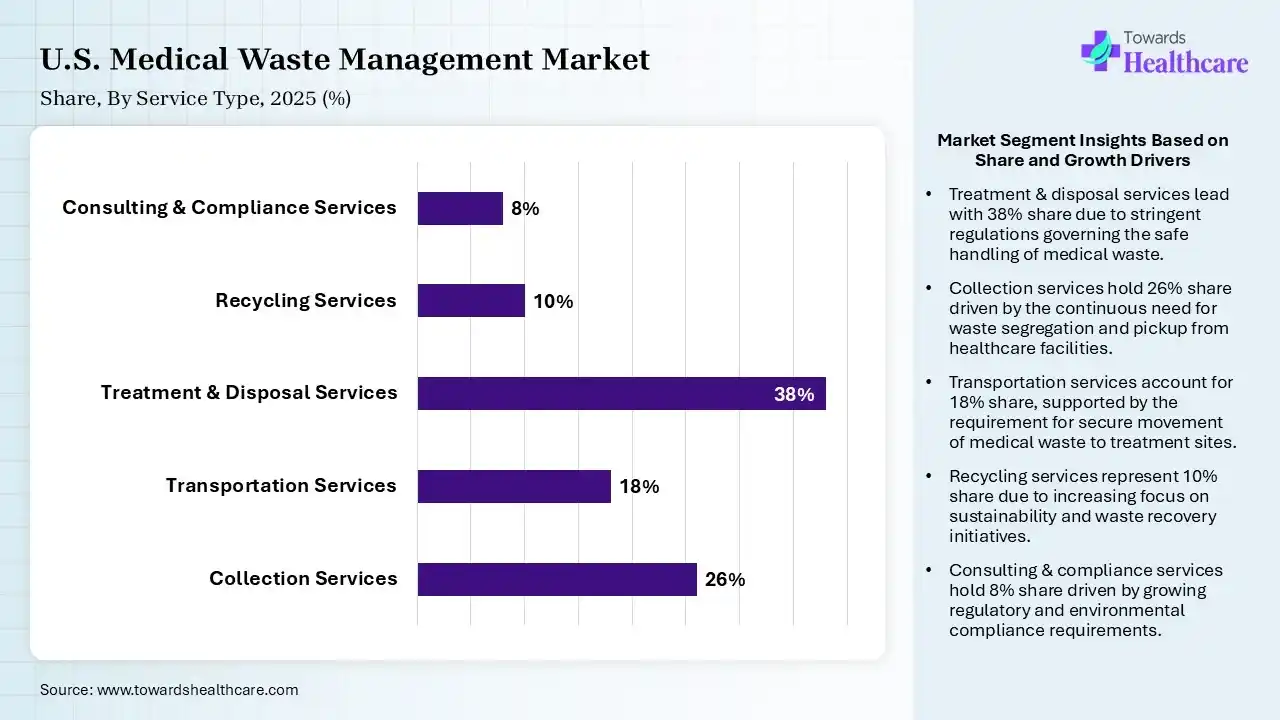

| Segments | Shares % |

| Collection Services | 26% |

| Transportation Services | 18% |

| Treatment & Disposal Services | 38% |

| Recycling Services | 10% |

| Consulting & Compliance Services | 8% |

The Treatment & Disposal Services Segment Dominated the Market With 38% in 2025

The treatment & disposal services segment held a major revenue share of 38% of the U.S. medical waste management market in 2025, as it was the core medical waste processing that promoted revenue generation. Increased regulatory requirements also supported the outsourcing trends, which increased the adoption of various treatment and disposal services. Advanced treatment investments also improved their capacity.

The collection services segment held the second-largest share of 26% of the market in 2025, due to expanding healthcare facilities, which require regular pickups. Outsourcing trends also support service demand for medical waste management. Compliance mandates also increase collection frequency for the safe handling of a wide range of medical waste.

The transportation services segment held 18% of the U.S. medical waste management market share in 2025, due to specialized logistics that ensure regulatory compliance. Growing waste volumes also increase transportation needs, promoting their use. Regional treatment networks also support their growth.

The recycling services segment held 10% of the market share in 2025 and is expected to expand rapidly with a CAGR of 10.1% during the forecast period, due to sustainability initiatives, which encourage material recovery. Healthcare organizations also pursue ESG goals. Recycling technologies also improve economic viability, driving their demand.

")

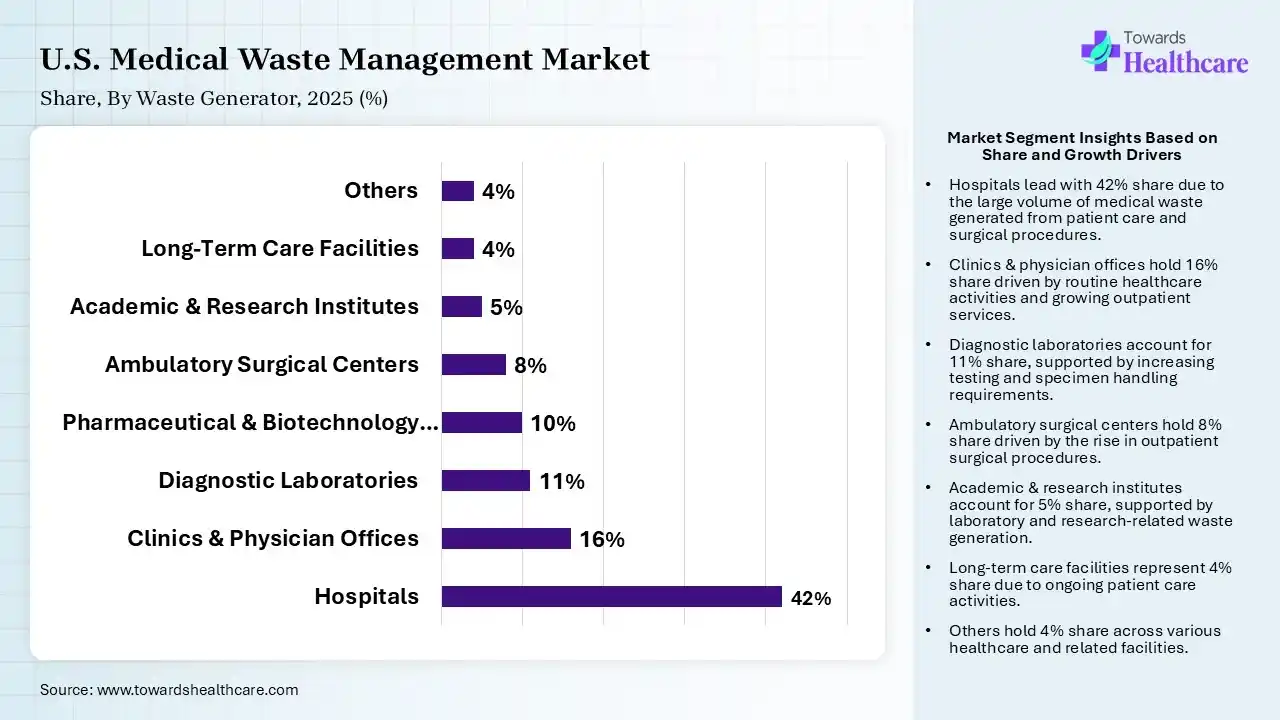

| Segments | Shares % |

| Hospitals | 42% |

| Clinics & Physician Offices | 16% |

| Diagnostic Laboratories | 11% |

| Pharmaceutical & Biotechnology Companies | 10% |

| Ambulatory Surgical Centers | 8% |

| Academic & Research Institutes | 5% |

| Long-Term Care Facilities | 4% |

| Others | 4% |

The Hospitals Segment Dominated the Market With 42% in 2025

The hospitals segment contributed the biggest revenue share of 42% of the U.S. medical waste management market in 2025, as it is the largest generator of infectious and pathological waste, which increased the demand for medical waste management services. A rise in inpatient procedures also increased waste output. Compliance requirements also supported specialized management.

The clinics & physician offices segment held the second-largest share of 16% of the market in 2025, due to growing outpatient care, which increases waste generation. Expansion of specialty clinics also supports high volumes, driving the demand for medical waste management. At the same time, regulatory oversight also drives service adoption.

The diagnostic laboratories segment held 11% of the U.S. medical waste management market share in 2025, driven by rising diagnostic testing, which boosts hazardous waste production. Molecular testing expansion also increases the waste generation, which drives the demand for its proper management. Biohazard disposal requirements also remain stringent.

The others segment held 4% of the market share in 2025 and is expected to gain the highest share with a CAGR of 10.2% during the forecast period, due to the expansion of veterinary and blood bank activities. Specialized waste streams also increase the demand for professional handling. Regulatory oversight also strengthens market demand.

")

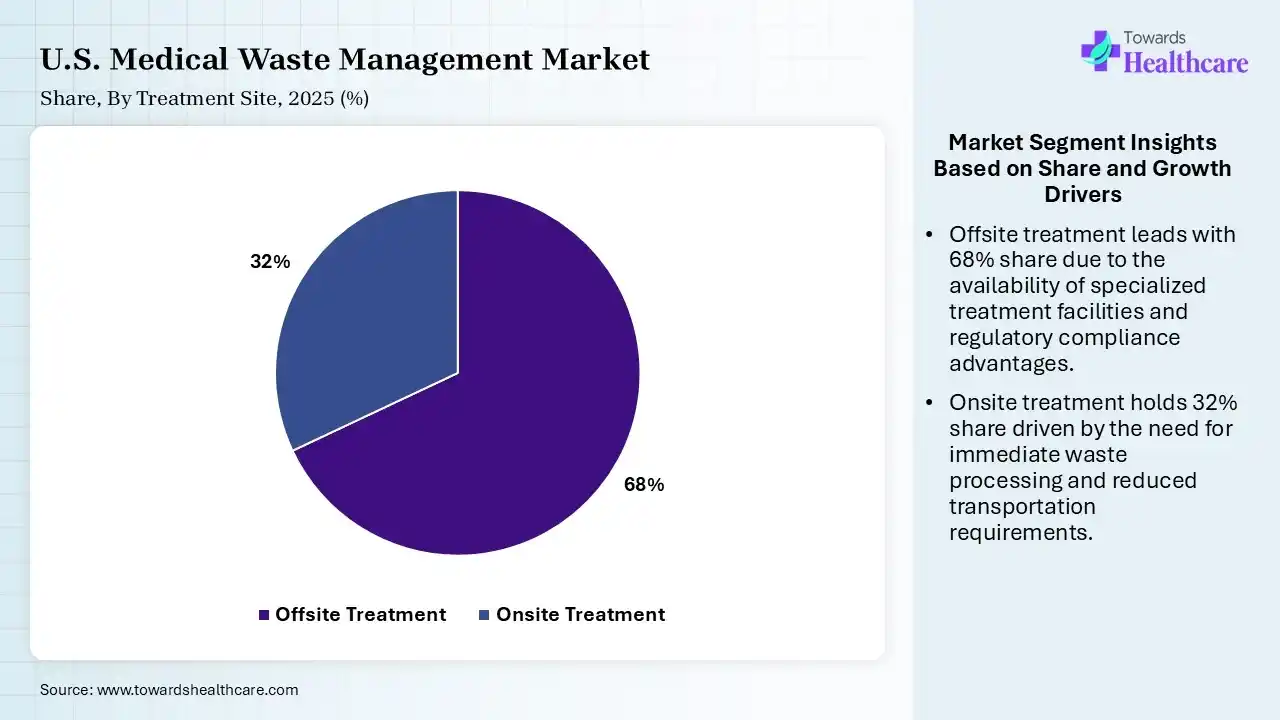

| Segments | Shares % |

| Offsite Treatment | 68% |

| Onsite Treatment | 32% |

The Offsite Treatment Segment Dominated the Market With 68% in 2025

The offsite treatment segment held the largest revenue share of 68% of the U.S. medical waste management market in 2025 and is expected to grow with the fastest CAGR of 8.40% during the forecast period, due to centralized facilities that provide economies of scale. Healthcare providers also outsourced waste management. Advanced treatment technologies also supported their adoption.

The onsite treatment segment held the second-largest share of 32% of the market in 2025, due to large hospitals seeking operational control. They also offer immediate treatment, which reduces transportation needs as well as the risk of contamination. Technology improvements also enhance feasibility and operational efficiency, which increases their use.

The U.S. medical waste management market is expected to show notable growth during the forecast period, due to the well-established healthcare infrastructure and rise in the chronic disease burden. This increased the patient volumes, which increased the generation of a wide range of medical waste, driving the demand for safe and effective management services. Stringent regulations, focused on environmental sustainability, also increased the adoption of advanced waste management technologies. Expanding home healthcare, the medical device industry, and investments are also increasing their adoption rates, enhancing the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

, Daniels Health, Clean Harbors, Inc., Sharps Compliance, Inc., Republic Services, Inc., Veolia North America, Triumvirate Environmental")

| Companies | Headquarters | U.S. Medical Waste Management Solutions |

| Waste Management Inc. (WM) | Houston, Texas | Shred-it, SafeShield, and Stericycle |

| Daniels Health | Chicago, Illinois | Sharpsmart, Clinismart, and Medismart |

| Clean Harbors, Inc. | Norwell, Massachusetts | Clean Harbors Medical Waste Management, Apollo & Pyrochem Incineration Systems, One-Source Healthcare Waste Options, and Chemical & Lab Pack Services |

| Sharps Compliance, Inc. | Houston, Texas | Sharps Recovery System, MedSafe, and TakeAway Medication Recovery System |

| Republic Services, Inc. | Phoenix, Arizona | Republic Sharps & Medical Waste Disposal, Sustainable Waste-to-Energy, and Mail-Back Sharps Solutions |

| Veolia North America | Boston, Massachusetts | Clean Earth Pharmaceutical & DEA Solutions and Veolia Clinical Waste Recovery Systems |

| Triumvirate Environmental | Somerville, Massachusetts | Regulated Medical Waste (RMW) Recycling, EHS Compliance & Training Programs, and Red Bag Waste Disposal Solutions |

In March 2025, after announcing the initiation of an important new research project, that is, State of Practice: Hospital, Medical & Infectious Waste (HMIW), EREF President & CEO Bryan Staley stated that “Our goal is to deliver a clear, data-driven understanding of how modern HMIW practices impact the environment”. “This research is vital to correct potential misconceptions resulting from outdated information and support informed decision-making in the healthcare and waste management industries.”

By Waste Type

By Treatment Method

By Service Type

By Waste Generator

By Treatment Site

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar