")

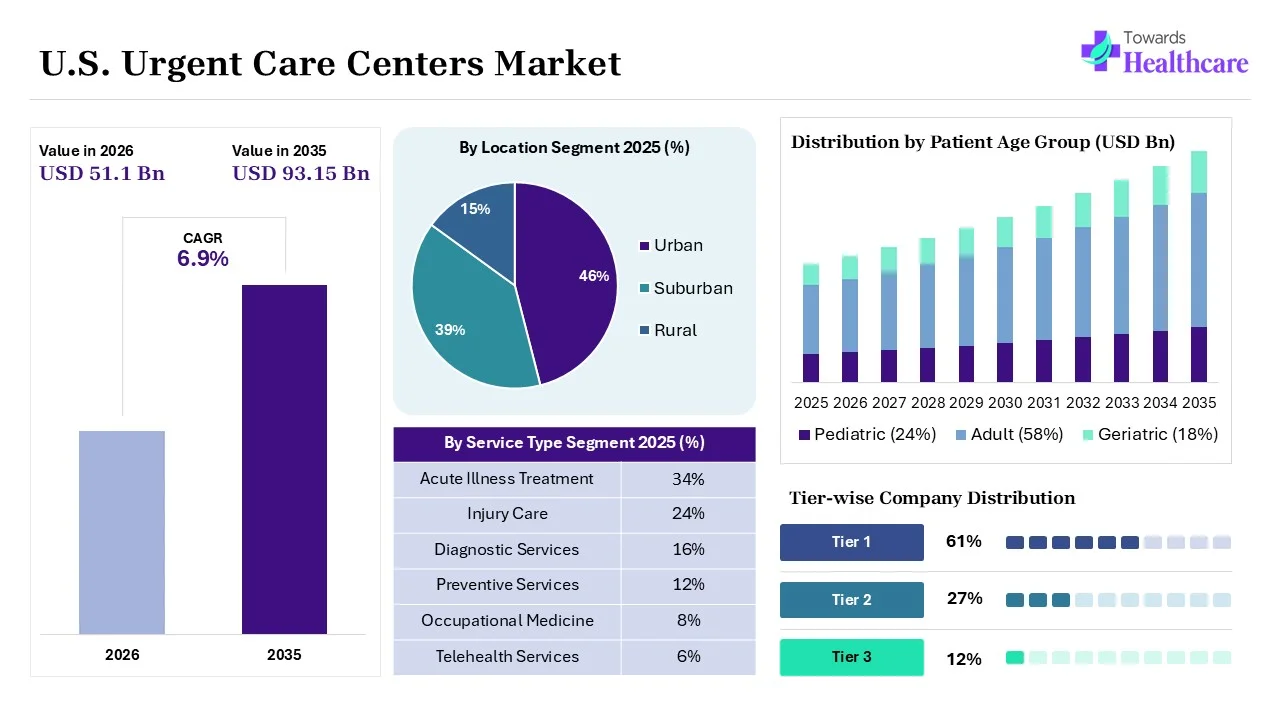

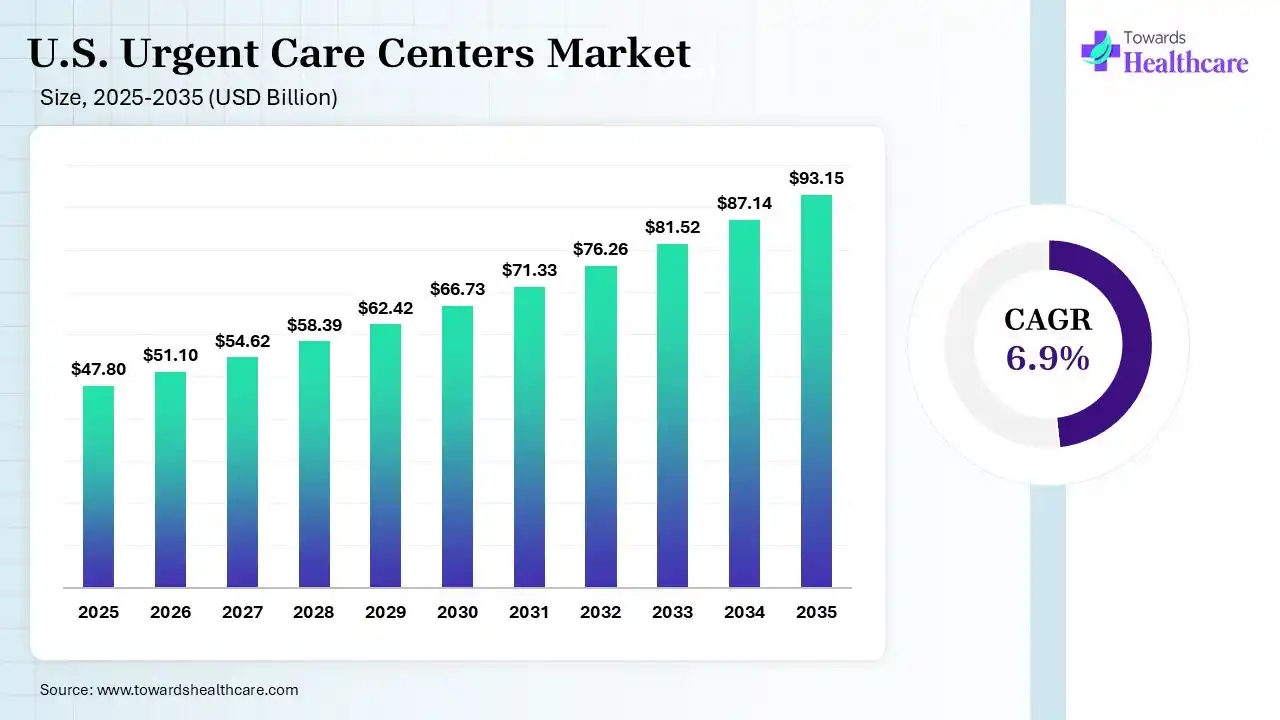

The U.S. urgent care centers market size was estimated at USD 47.8 billion in 2025 and is predicted to increase from USD 51.1 billion in 2026 to approximately USD 93.15 billion by 2035, expanding at a CAGR of 6.9% from 2026 to 2035.

")

Macro Factors

Micro Factors

Artificial intelligence is transforming the market by enhancing clinical triage, streamlining patient scheduling, and supporting faster diagnosis of common conditions. AI-powered tools improve operational efficiency, reduce wait times, and optimize resource allocation. Integration of predictive analytics and virtual health assistants enables more personalized care, while automated administrative workflows help lower costs and improve the overall patient experience across urgent care networks.

Telehealth and Hybrid Care Integration

Urgent care centers are increasingly combining in-person consultations with virtual care services to improve accessibility and convenience. Hybrid care models enable faster triage, remote follow-ups, and expanded patient reach, helping providers deliver efficient and cost-effective healthcare while enhancing patient satisfaction and continuity of care.

Expansion of Retail and Community-Based Care Networks

Urgent care providers are expanding through retail clinics and community-based facilities to meet growing demand for accessible healthcare. This trend is increasing healthcare availability in underserved areas while reducing pressure on hospital emergency departments. Continued network expansion is expected to strengthen outpatient care delivery across the United States.

| Table | Scope |

| Market Size in 2026 | USD 93.15 Billion |

| Projected Market Size in 2035 | USD 51.1 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Ownership, By Service Type, By Patient Age Group, By Payer Type, By Facility Type, By Visit Type, By Location |

| Top Key Players | Concentra, American Family Care, FastMed Urgent Care, CityMD, CareNow, GoHealth Urgent Care, NextCare Urgent Care |

")

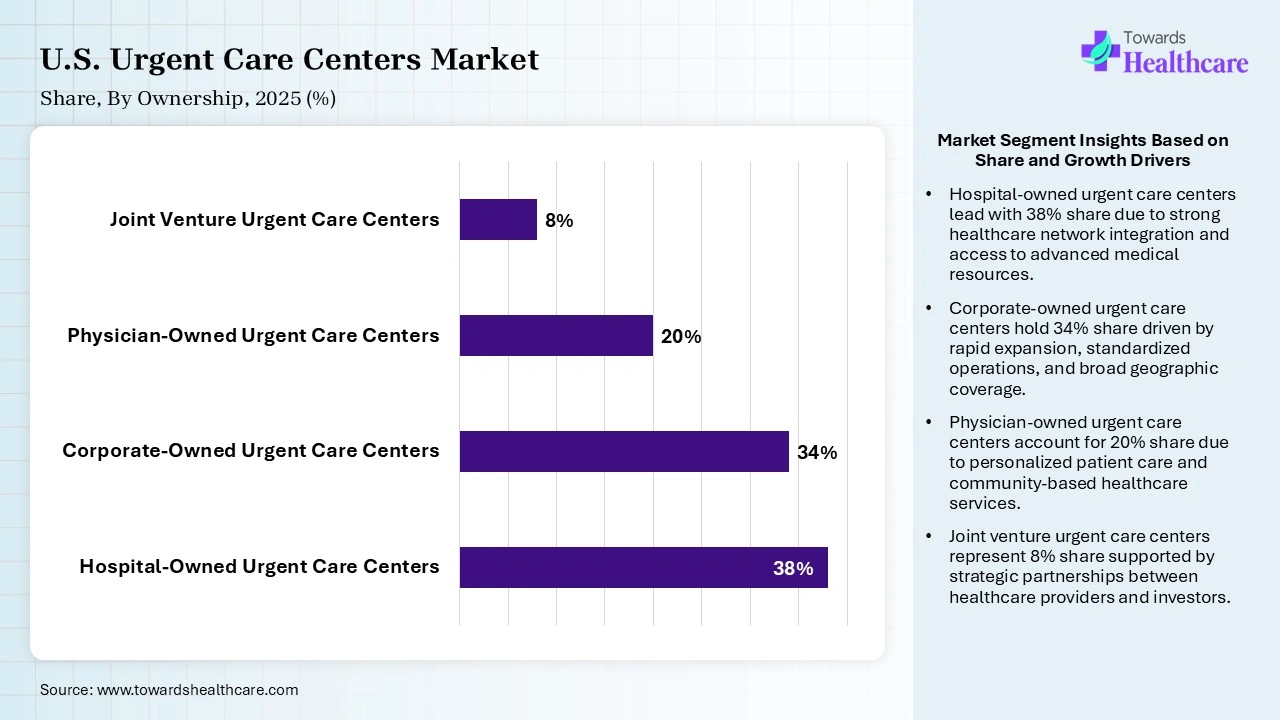

| Segment | Share 2025 (%) |

| Hospital-Owned Urgent Care Centers | 38% |

| Corporate-Owned Urgent Care Centers | 34% |

| Physician-Owned Urgent Care Centers | 20% |

| Joint Venture Urgent Care Centers | 8% |

The Hospital-owned Urgent Care Centers Segment Dominated the U.S. Urgent Care Centers Market in 2025.

The hospital-owned urgent care centers segment held a dominant share of 38% in 2025 due to strong healthcare network integration, established brand trust, and access to advanced medical resources. These centers offer seamless referrals to specialized and hosptials, ensuring continuity of care. Their broader geographic presence, enhanced insurance partnerships, and ability to manage higher patient volumes further strengthened their market leadership.

The corporate-owned urgent care centers segment held the second-largest share of 34% in 2025 and is expected to grow at the fastest CAGR of 8.2% in the market during the forecast period due to aggressive network expansion, standardized service delivery, and strong operational efficiency. These centers emphasize convenient locations, extended operating hours, and rapid patient access. Strategic investments in digital health technologies, branding, and consumer-focused care models have further strengthened their market presence and patient volume growth.

The physician-owned urgent care centers segment held a 20% U.S. urgent care centers market share due to its focus on personalized patient care, clinical autonomy, and strong community relationships. These centers often provide flexible, patient-centric services with shorter decision-making processes and enhanced care quality. Rising demand for accessible healthcare, coupled with physicians’ ability to tailor services to local needs, is supporting the expansion and competitiveness of physician-owned urgent care facilities.

The joint venture urgent care centers segment held an 8% market share due to increasing collaboration between hospitals, health systems, and private healthcare operators. These partnerships combine clinical expertise, financial resources, and an established patient network to improve service delivery and market reach. Joint ventures enable cost sharing, operational efficiencies, and accelerated expansion into underserved areas, while providing patients with seamless access to integrated and high-quality healthcare services.

")

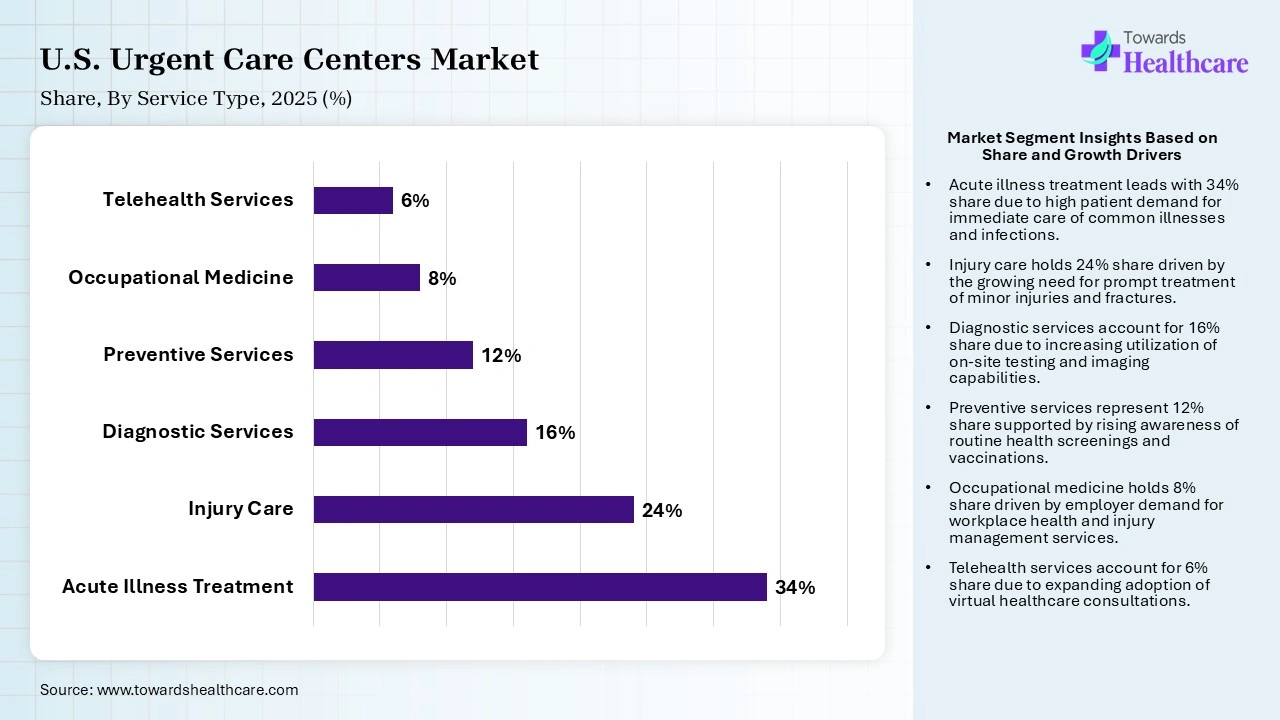

| Segment | Share 2025 (%) |

| Acute Illness Treatment | 34% |

| Injury Care | 24% |

| Diagnostic Services | 16% |

| Preventive Services | 12% |

| Occupational Medicine | 8% |

| Telehealth Services | 6% |

The Acute Illness Treatment Segment Led the Market in 2025 with the Largest Share

The acute illness treatment segment dominated the U.S. urgent care centers market with a share of 34% in 2025 due to the high prevalence of common conditions such as respiratory infections, influenza, fever, sore throat, and urinary tract infections. Patients increasingly prefer urgent care centers for quick, affordable treatment of non-life-threatening illnesses. Convenient access, shorter wait times, and growing demand for same-day care further contributed to the segment’s market leadership.

The injury care segment held the second-largest share of 24% in 2025 due to the high incidence of minor fractures, sprains, cuts, burns, and sport-related injuries. Urgent care centers provide timely treatment, diagnostic imaging, and wound management at a lower cost than emergency departments. Growing participation in physical activities and demand for immediate, convenient care further supported segment growth.

The diagnostic services segment held a 16% market share due to growing demand for rapid and accurate disease detection in urgent care settings. Increased availability of point-of-care testing, laboratory services, and diagnostic imaging enables faster clinical decision-making and treatment initiation. Rising prevalence of infectious diseases and chronic conditions, along with the need for convenient same-day testing, is driving the adoption of diagnostic services across urgent care centers.

The telehealth services segment held a 6% share in 2025 and is expected to grow at the fastest CAGR of 11.5% in the U.S. urgent care centers market during the forecast period due to increasing demand for convenient, remote healthcare access. Rising adoption of digital health platforms, expanding internet connectivity, and growing patient preference for virtual consultations are accelerating market growth. Telehealth reduces travel and wait times, improves access in underserved areas, and supports efficient management of non-emergency medical conditions.

")

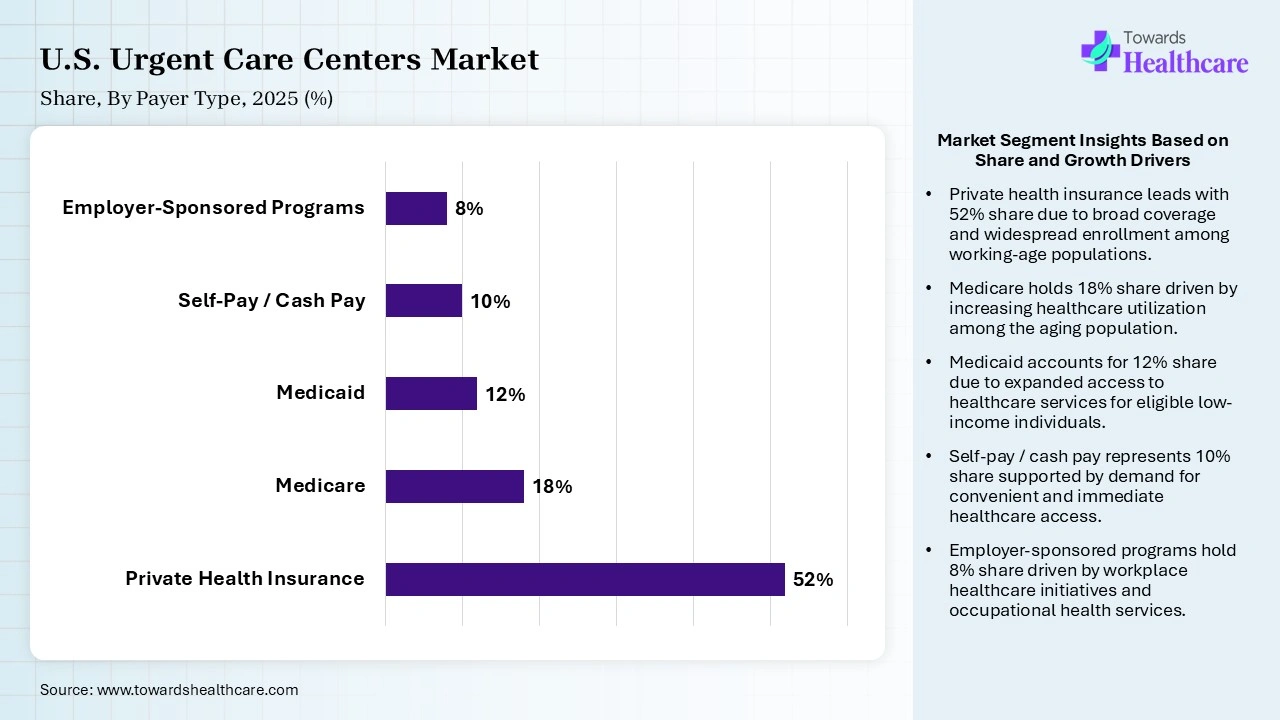

| Segment | Share 2025 (%) |

| Private Health Insurance | 52% |

| Medicare | 18% |

| Medicaid | 12% |

| Self-Pay / Cash Pay | 10% |

| Employer-Sponsored Programs | 8% |

The Private Health Insurance Segment Led the U.S. Urgent Care Centers Market in 2025 with the Largest Share

The private health insurance segment led the market with a share of 52% in 2025 due to widespread employer-sponsored health plans and extensive coverage for outpatient medical services. Patients with private insurance are more likely to utilize urgent care centers because of lower out-of-pocket costs and convenient access to care. Strong insurance-provider partnerships and growing healthcare utilization further contributed to the segment’s dominant market position.

The Medicare segment held the second-largest share of 18% in 2025 due to the growing elderly population and increasing prevalence of age-related health conditions. Medicare beneficiaries frequently utilize urgent care centers for timely treatment of non-emergency illnesses and injuries. Expanded Medicare coverage, rising healthcare utilization among seniors, and the need for convenient outpatient services further supported the segment’s substantial market share.

The Medicaid segment held a 12% market share due to increasing enrollment in government-sponsored healthcare programs and improved access to outpatient medical services. Urgent care centers offer Medicaid beneficiaries a convenient and cost-effective alternative to alternative to emeregency department for non-emergency conditions. Growing healthcare utilization among the low-income population, coupled with expanding providers’ participation in Medicaid networks, is further supporting segment growth.

The self-pay/cash pay segment held a 10% share in 2025 and is expected to grow at the fastest CAGR of 8.5% in the U.S. urgent care centers market during the forecast period due to increasing numbers of uninsured and underinsured individuals seeking affordable and convenient walk-in services, making urgent care centers attractive to self-paying patients. Growing healthcare attractive to self-paying patients. Growing healthcare consumerism and demand for cost-effective outpatient care are further driving rapid segment expansion.

")

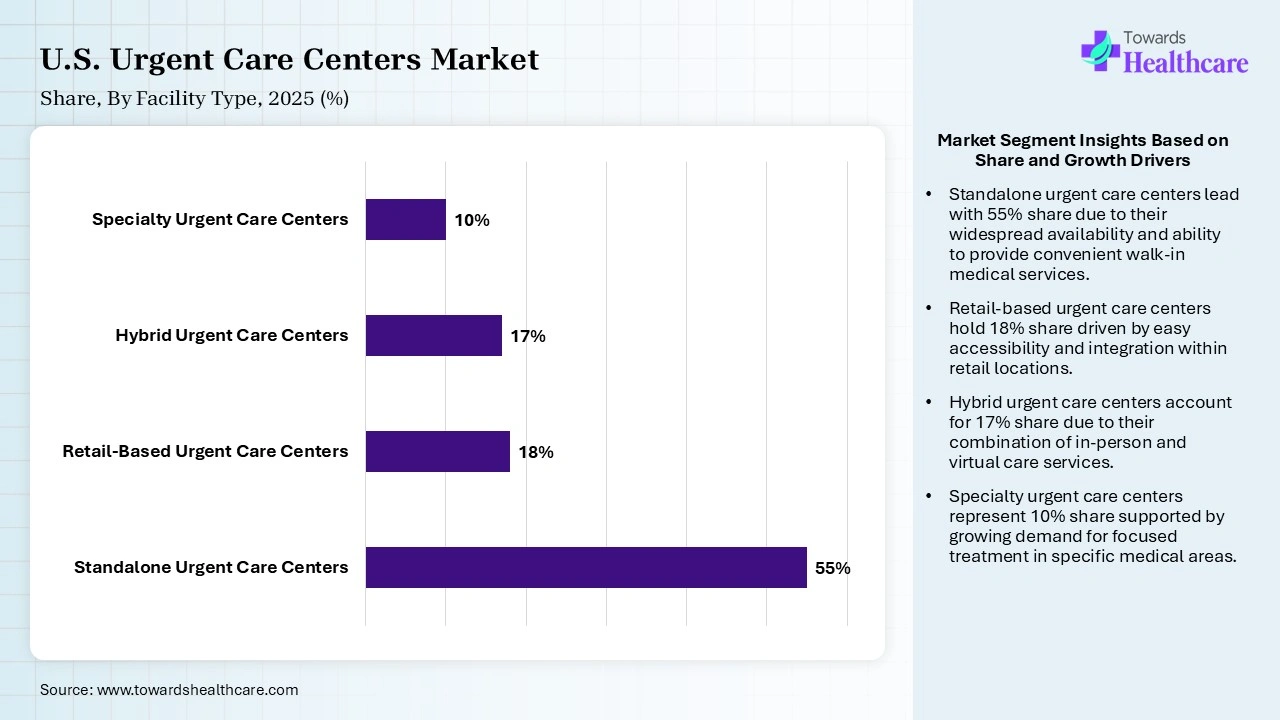

| Segment | Share 2025 (%) |

| Standalone Urgent Care Centers | 55% |

| Retail-Based Urgent Care Centers | 18% |

| Hybrid Urgent Care Centers | 17% |

| Specialty Urgent Care Centers | 10% |

The Standalone Urgent Care Centers Segment Led the U.S. Urgent Care Centers Market in 2025 with the Largest Share

The standalone urgent care centers segment held a dominant share of 55% in 2025 due to its widespread availability, convenient locations, and ability to provide rapid treatment without hospital affiliation. These facilities offer extended operating hours, shorter wait times, and cost-effective care for non-emergency conditions. Their strong community presence, operational flexibility, and growing patient preference for accessible outpatient services contributed significantly to market leadership.

The retail-based urgent care centers segment held the second-largest share of 18% in 2025 due to its strategic locations within pharmacies, supermarkets, and retail stores. These centers offer convenient access, extended hours, and quick treatment for minor illnesses and injuries. Growing consumer preference for easily accessible healthcare services, combined with lower costs and efficient care delivery, has strengthened the segment’s position in the U.S. urgent care centers market.

The hybrid urgent care centers segment held a 17% share in 2025 and is expected to grow at the fastest CAGR of 9.4% in the market during the forecast period due to increasing adoption of combined in-person and virtual care models. These centers offer greater convenience, improved access to healthcare, and enhanced patient engagement through telehealth integration. Rising demand for flexible care options, technological advancements, and the need for cost-effective healthcare delivery are accelerating segment growth.

The specialty urgent care centers segment held a 10% market share due to growing demand for focused medical services such as pediatric care, orthopedic treatment, occupational health, and women’s healthcare. These centers provide specialized expertise, faster diagnosis, and tailored treatment for specific patient needs. The increasing prevalence of condition-specific healthcare requirements, coupled with rising patient preference for specialized outpatient services, is driving the growth of this segment.

The U.S. urgent care centers market leads due to well-established healthcare infrastructure, high healthcare spending, and widespread adoption of convenient outpatient care services. A large network of urgent care facilities, strong insurance coverage, and increasing demand for cost-effective alternatives to emergency departments support market growth. Continuous investments in digital health technologies and expanding patient access further strengthened the country’s market leadership.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| Concentra | Addison, Texas, USA | Urgent care, occupational health, physical therapy, employer health services |

| American Family Care | Birmingham, Alabama, USA | Urgent care, primary care, telemedicine, laboratory testing, and vaccinations |

| FastMed Urgent Care | Raleigh, North Carolina, USA | Urgent care, telehealth, occupational medicine, and preventive healthcare services |

| CityMD | New York, New York, USA | Walk-in urgent care, diagnostic imaging, laboratory services, virtual care |

| CareNow | Brentwood, Tennessee, USA | Urgent care, injury treatment, occupational health, diagnostic testing |

| GoHealth Urgent Care | Atlanta, Georgia, USA | Urgent care, virtual visits, integrated health system partnerships, diagnostic services |

| NextCare Urgent Care | Tempe, Arizona, USA | Urgent care, telemedicine, pediatric care, laboratory, and imaging services |

In July 2025, “We are excited to partner with GoHealth. Their proven consumer-focused model will allow Community Health Network to deliver even more exceptional, convenient care to Hoosiers throughout Central Indiana,” said Patrick McGill, MD, EVP and chief transformation officer for Community Health Network.

In January 2026, Sutter Health expanded its Placer County footprint with a new 5,010-square-foot urgent care in West Roseville. Located at 4001 Woodcreek Oaks Blvd., the two-provider facility features on-site imaging and online check-ins to increase access to same-day care for the growing greater Sacramento region.

In August 2025, UPMC and GoHealth Urgent Care launched a massive joint venture to unveil 81 rebranded urgent care centers across Pennsylvania and West Virginia. The collaborative network expands seamless, on-demand medical access while directly integrating the clinics with UPMC’s broader network of expert physicians and specialists.

By Ownership

By Service Type

By Patient Age Group

By Payer Type

By Facility Type

By Visit Type

By Location

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar