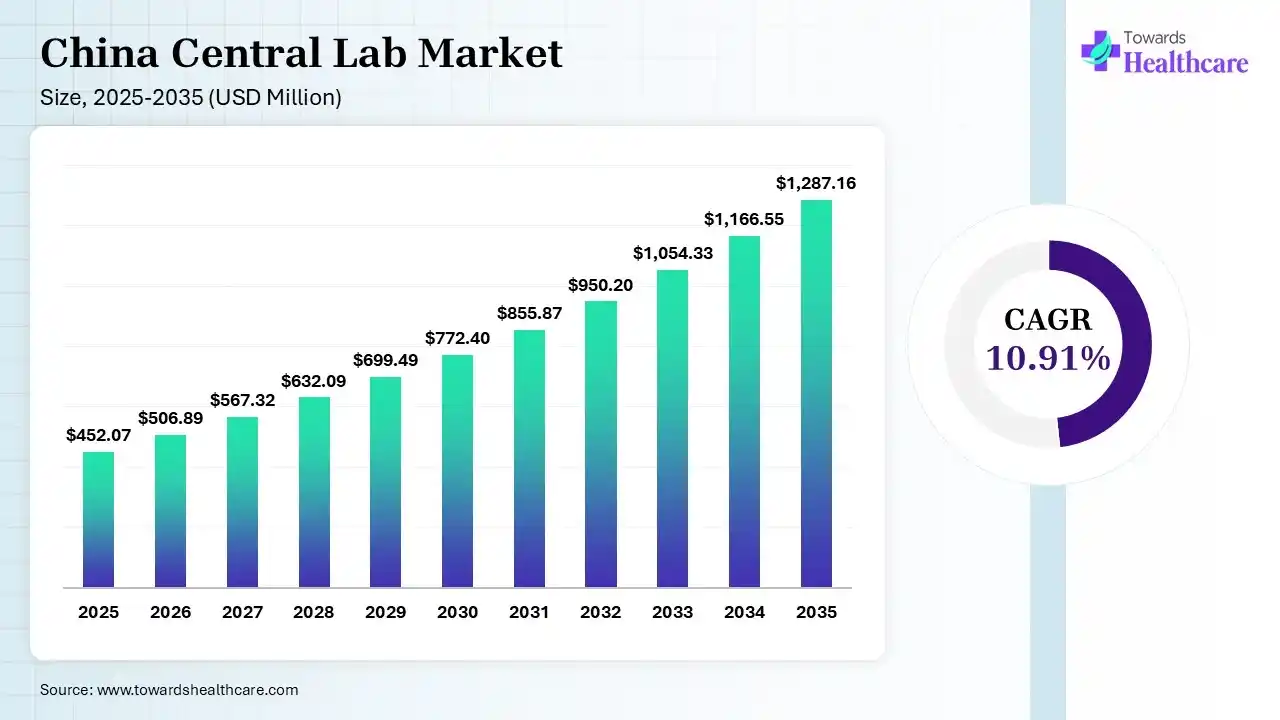

The China central lab market size was estimated at USD 452.07 million in 2025 and is predicted to increase from USD 506.89 million in 2026 to approximately USD 1287.16 million by 2035, expanding at a CAGR of 10.91% from 2026 to 2035. The Chinese central lab market is increasing due to central laboratory service providers playing a significant role in healthcare trial research by offering significant services that maintain the quality of the sample.

")

A central lab is generally a large, dedicated laboratory service that is typically independent of the clinical trial site. It is accountable for handling a noteworthy portion of the laboratory testing needed for the clinical trial. These labs are often equipped with well-developed technology and have wide experience in conducting particular types of tests. They typically process and analyse a massive number of samples composed from many trial sites or locations. The central lab obtains the samples from the trial sites, conducts the testing, and communicates the outputs back to the trial sites. Central labs ensure consistent and reliable testing technology and quality control measures in multiple trial sites, which is specifically significant for multinational or multicenter trials.

AI plays an important role in processing massive datasets in the healthcare laboratory. Data collected from hospital laboratory tests is analysed by AI-based technology and used for disease diagnosis, prediction, and prognosis. Chinese researchers created the world's first AI-driven transmission electron microscope (AI-TEM) technology. Laboratory devices integrate AI-based models, hardware, and software to perform experiments, work with advanced robotic systems, and handle data, completing the predict-make-measure detection cycle.

| Table | Scope |

| Market Size in 2026 | USD 506.89 Million |

| Projected Market Size in 2035 | USD 1287.16 Million |

| CAGR (2026 - 2035) | 10.91% |

| Key Applications | Clinical trials, biomarker testing, companion diagnostics, genomics, pathology, bioanalysis, vaccine studies, cell & gene therapy studies |

| Primary End Users | Pharmaceutical companies, biotechnology firms, CROs, medical device companies, academic research institutions |

| Key Growth Drivers | Expansion of China's biopharma industry, increasing clinical trials, innovative drug development, global multicenter studies, precision medicine adoption |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By End User, By Test Type, By Phase of Clinical Trial, By Technology, By Sample Type |

| Top Key Players | WuXi AppTec, KingMylab, Tigermed, Pharmaron, JOINN Laboratories, Medicilon, SDM CRO, ChemPartner, Frontage Laboratories, KingMed Diagnostics |

The Safety Testing Segment Dominated the Market in 2025

The safety testing segment led with a 35.02% share of the China central lab market in 2025. Prominent drivers are stringent clinical trial regulations, the expedited development of complex biologics, & expanding biotech sector. Alongside, national public health redevelops & plans to bolster biological safety, which has resulted in a major rise in high-level biosafety laboratories & advanced pathogen laboratory equipment in the Centers for Disease Control and Prevention (CDC) networks.

Moreover, the genomic & molecular testing segment captured a 17.60% share in 2025 & is predicted to expand at a 12.97% CAGR. The growth is mainly propelled by a massive rise in the clinical research framework, the growing burden of chronic & rare diseases, coupled with a greater inclination towards tailored medicine. Whereas the Chinese government is boosting awareness & mandating maternal health surveillance & the mitigation of genetic disorders, which spurs the higher adoption of karyotyping & genetic counseling across public hospitals.

The pathology & histology services segment accounted for 15.87% of the China central lab market in 2025. Increasing oncology clinical trials, a severe shortage of pathologists, & heavy government investments in healthcare modernization & AI are fueling the segmental growth. China is a center for the geriatric population, & higher cases of chronic illnesses, like cancer & diabetes, demand advanced routine and specialized tissue testing.

However, the specialty testing & biomarkers segment captured a 14.95% in 2025, due to major movement towards targeted therapies & precision treatments that necessitate the latest genetic & molecular profiling. Besides this, several pharmaceutical & biotech leaders are increasingly emphasizing the development of translation science, which drives the need for biomarker analysis to find patient data & estimate treatment outcomes.

The Oncology Segment Led the Market in 2025

In 2025, the oncology segment held the largest share of 35.34% of the China central lab market. As China is facing nearly 4.8 million cancer cases annually, central labs speed up oncology trials by facilitating investigator sites with modernized strategies for the collection & processing of laboratory samples. Vast promotion of personalized oncology propels central labs to offer highly specific molecular characterization.

The infectious diseases segment held the second-largest share of 18.50% of the market in 2025. Respective expansion is driven by central laboratory solutions that focus on effectiveness, standardization, & affordability for large numbers of samples from different trial sites. Booming closeness to wildlife & human modification of ecosystems is offering genetic reassortment, mutation, & the arrival of pathogens from animals to humans, leading to diverse infectious incidences.

Although the cardiovascular & metabolic diseases (CVMD) segment accounted for a 17.68% share of the China central lab market. A huge & faster rise in the ageing population, increasing sedentary lifestyles, with higher sodium & processed diets, & massive expansion of environmental pollution, resulting in these cases. For this, central labs are fostering sophisticated diagnostic imaging technology, which is substantial for the accurate visualization of the cardiac arteries & compartments.

The rare diseases & genetic disorders segment captured a 5.14% share in 2025 & is estimated to expand at a 15.28% CAGR. Key catalysts are expeditiously declining cost of Next-Generation Sequencing (NGS), bolstering the national newborn screening program, & accelerating investments in biologic & orphan drug trials. China’s labs are widely leveraging bioinformatics & machine learning to speed up diagnostic turnaround times & optimize variant classification.

The Phase III (Late Phase) Segment Dominated the Market in 2025

The Phase III (late phase) segment registered dominance with a 54.73% share of the China central lab market in 2025. Dominance is mainly driven by performing this phase in China, which is majorly affordable, coupled with minimal per-patient operational costs at clinical sites. The emergence of parallel development models, i.e., global sponsors are conducting Phase III trials in China simultaneously to assist simultaneous NDA/BLA filings with the US FDA & NMPA.

On the other hand, the Phase I & II (early phase) segment held the second-largest share of a 29.45% in 2025, due to rapid IND approvals by the NMPA & involvement of international multi-center trial (MRCT) data, joining early-phase Chinese clinical data with global submission standards. Surging progression of new biologics, especially Cell and Gene Therapies (CGTs) & antibody-drug conjugates (ADCs), is driving the respective phase inclusion.

The Phase IV (post-marketing surveillance) segment captured a 15.82% share in 2025 & is anticipated to expand at a 12.21% CAGR in the China central lab market. Eventually, robust China’s adverse drug reaction monitoring agencies have inclined towards proactive PV, developing demand for central labs to manage biomarker, pathology, & safety testing for large-scale patient populations. Post-marketing studies are emphasizing an evaluation of long-term efficiency, affordability, & safety in various Chinese demographics under naturalistic settings, which complements pre-marketing data.

The Biologics (Large Molecules) Segment Was Dominant in the Market in 2025

In 2025, the biologics (large molecules) segment led with 40.27% of the market. The segmental dominance is fueled by the arrival of capital & top-tier talent into biopharma R&D, a rise in local incidence of chronic diseases, & regulatory c hanges that accelerate approval processes for innovative therapies. China is expanding as an industry powerhouse, with a vast focus on biologic therapies, like antibody-drug conjugates (ADCs) & bispecific antibodies.

Moreover, the small molecules segment held a 35.27% share of the China central lab market in 2025, due to the rising strong oncology & neurology pipelines, a well-developed local clinical trial ecosystem, & the faster adoption of Model-Informed Drug Discovery and Development (MIDD). Revolutionary LC-MS/MS & LBA (Ligand Binding Assay) capacities in central labs are fostering complex small molecules, like targeted protein degraders (PROTACs), ADC payloads, & liposomal formulations.

Whereas the advanced therapies (ATMP) segment accounted for a 14.28% share in 2025 & is estimated to expand rapidly at a 15.76% CAGR. This primarily covers various cell therapies, gene therapies, & tissue-engineered products. To manage the growing demand for these therapies, central labs are offering intricate evaluations, such as vector biodistribution, viral shedding, & complex immunogenicity (ADA/NAb) assays.

However, the vaccines segment captured a 10.18% share of the China central lab market in 2025. The segmental growth is propelled by a rise in complex modalities, including mRNA platforms, viral vectors, & recombinant proteins that require sophisticated centralized testing. Escalating the need for standardized, global-standard immunogenicity & safety testing, Chinese labs are assisting specialized platforms, like ELISPOT, flow cytometry, & multi-plex serology assays, to assess complex vaccine efficacy.

The Pharmaceutical & Biotechnology Companies Segment Led the Market in 2025

The pharmaceutical & biotechnology companies segment held a dominant share of a 62.55% of the market in 2025. These companies are bolstering due to a huge untreated patient pool, simplified IND (Investigational New Drug) review processes, and the need for highly standardized biomarker & genomic testing. Alongside, many Chinese biotech players are expanding their independent research & development capabilities, supporting the overall market progression.

The contract research organizations (CROs) segment accounted for a 16.82% share in 2025 & is predicted to expand at a 12.14% CAGR in the China central lab market. CROs enhance the quality and choice of their clinical trials and confirm timely and precise reporting. As advanced central labs are beneficial for CROs, the central lab has a proven track record of supporting successful trials and steps in when a trial needs rescuing.

Moreover, the academic & government research institutes segment held a lucrative share of 13.18% share in 2025. Major drivers include the higher state-led funding for STEM & biomedical research, national support for technological self-sufficiency, and top-down restructuring of the State Key Laboratory system. In addition, government assistance & optimized domestic research infrastructure are appealing to global & US-based scientists to return to or join Chinese institutions.

The clinical diagnostic laboratories segment captured a 7.45% share in 2025, due to rising focus on preventing higher R & D spending & follow China's unique regulatory framework. For this, many institutional buyers & hospitals are widely outsourcing complex pathology, genetic sequencing, & biomarker testing to third-party providers. Also, elevating unification of AI, automation, & molecular diagnostics is enabling labs to control higher sample volumes with higher accuracy & lowered turnaround times.

The Bio-Tech Boom: China’s Central Lab Expansion

China's central lab market is expanding rapidly, fueled by a surge in domestic pharmaceutical research and a rising prevalence of chronic diseases. Robust government investments and favorable regulatory shifts encourage biotechnology companies to outsource complex clinical testing. These developments collectively cement the nation as a global hub for innovative drug development.

Expanding upon this landscape, the sector is experiencing significant capacity upgrades. Seamless integration of artificial intelligence and advanced biomarker or genetic testing allows facilities to handle larger sample volumes with higher accuracy and reduced turnaround times. Local biotechnology and pharmaceutical entities increasingly utilize these specialized central labs to mitigate high R&D costs and navigate evolving National Medical Products Administration regulations.

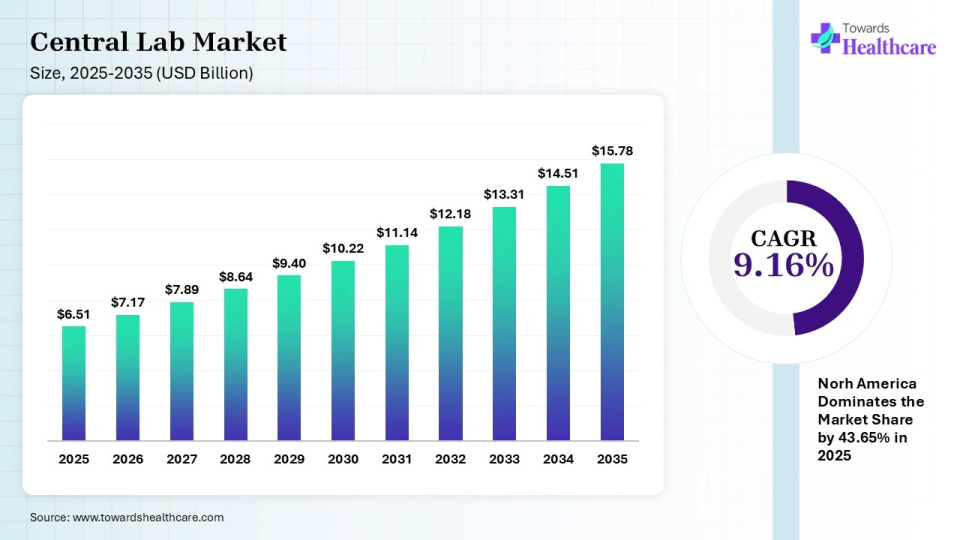

The global central lab market size is calculated at USD 6.51 billion in 2025 and is expected to be worth USD 15.78 billion by 2035, expanding at a CAGR of 9.16% from 2026 to 2035, as a result of rising investment in R&D and rising demand for clinical trials.

")

| Ecosystem Segment | Description | Key Participants |

| Technology Providers | Laboratory automation, LIMS, sample tracking, biomarker platforms | Thermo Fisher Scientific, Roche Diagnostics, Agilent Technologies |

| Product Manufacturers | Clinical testing instruments, reagents, diagnostics platforms | Abbott, Danaher, Siemens Healthineers |

| Central Laboratory Service Providers | Core providers conducting clinical trial laboratory testing | IQVIA Laboratories, Eurofins Central Laboratory, Medpace Central Labs, KingMylab, WuXi AppTec |

| CROs/CDMOs | Clinical development partners utilizing central lab services | ICON, Labcorp Drug Development, Parexel, WuXi AppTec |

| Platform Providers | Data management and clinical trial platforms | Medidata, Oracle Health Sciences, Veeva Systems |

| Software Vendors | Clinical data integration and laboratory informatics | LabVantage, STARLIMS, Thermo Fisher Informatics |

| Research Institutions | Academic and translational research centers | Shanghai Clinical Research Center (SCRC), Peking Union Medical College Hospital |

| End-User Industries | Organizations outsourcing clinical laboratory activities | Pharma, Biotechnology, Medical Devices, Vaccines, Cell & Gene Therapy |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 30% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| IQVIA Laboratories | Durham, North Carolina, USA | USA | Operates major Beijing central laboratory supporting local and global clinical studies | Central lab services, biomarker testing, genomics, pathology, bioanalysis |

| Labcorp Drug Development (Central Laboratories) | Burlington, North Carolina, USA | USA | One of the largest global central lab providers serving multinational trials in China | Central laboratory testing, biomarker services, companion diagnostics |

| Eurofins Central Laboratory | Luxembourg City, Luxembourg | Luxembourg | Extensive clinical trial laboratory network with Shanghai operations | Central laboratory testing, specialty testing, logistics, data management |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| WuXi AppTec | Shanghai, China | China | Leading Chinese CRO offering comprehensive central laboratory services | Central lab testing, logistics, sample management, bioanalysis |

| KingMylab | Guangzhou, Guangdong, China | China | One of China's leading dedicated clinical trial central laboratories | Central lab services, pathology, biomarker testing, data management |

| SGS Life Sciences | Geneva, Switzerland | Switzerland | Active central laboratory services supporting multicenter studies in China | Clinical trial central lab services, logistics, PK/PD testing |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Shanghai Clinical Research Center (SCRC) | Shanghai, China | China | Specialized central laboratory serving pharmaceutical research projects | Clinical testing, pathology, PK/PD services |

| Clinical Service Center (CSC) | Suzhou, Jiangsu, China | China | CRO with dedicated clinical trial central laboratory capabilities | Clinical chemistry, hematology, biomarker testing |

| KingMed Diagnostics | Guangzhou, Guangdong, China | China | Major diagnostics company supporting central lab operations and trials | Central laboratory services, biobanking, logistics |

Strengths

Weakness

Opportunities

Threat

By Service Type

By Therapeutic Area

By End User

By Test Type

By Phase of Clinical Trial

By Technology

By Sample Type

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar