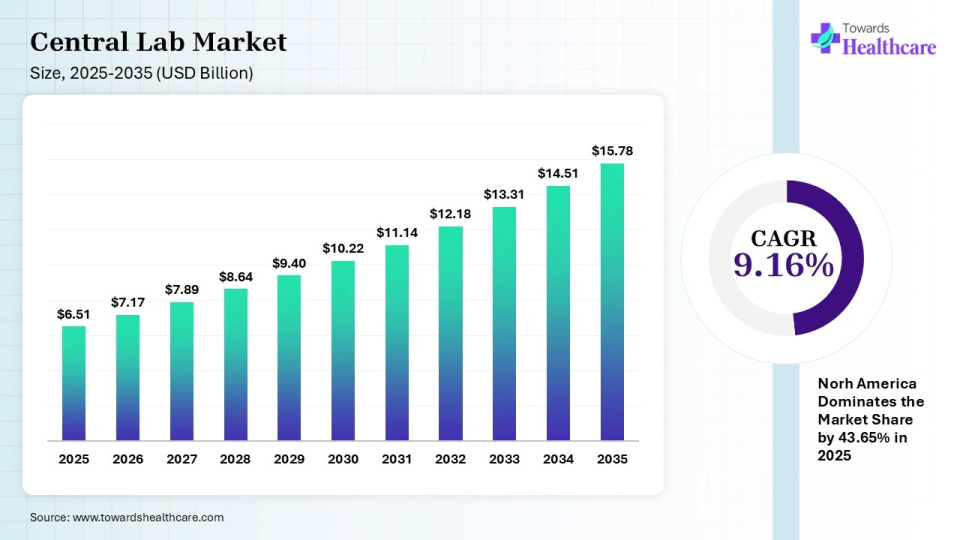

The global central lab market size is calculated at USD 6.51 billion in 2025 and is expected to be worth USD 15.78 billion by 2035, expanding at a CAGR of 9.16% from 2026 to 2035, as a result of rising investment in R&D and rising demand for clinical trials.

")

A central lab, also known as a central laboratory, is a specialized facility for conducting various laboratory tests and analyses. These labs are typically used in clinical trials, where they are responsible for performing a range of analyses on samples of blood, urine, tissue, and other materials collected from study participants. The goal of central labs is to provide consistent and reliable data across multiple study sites, which can then be used to evaluate the safety and effectiveness of new drugs, medical devices, or other healthcare interventions.

Central labs typically use advanced laboratory equipment and technologies, such as automated sample processing systems, high-throughput screening systems, and sophisticated analytical instruments. They are staffed by trained technicians and scientists who are responsible for conducting the tests and interpreting the results.

In addition to clinical trials, central labs may also be used for other types of laboratory testing, such as diagnostic testing for infectious diseases or genetic testing for inherited conditions. These labs may be operated by private companies, academic institutions, or government agencies, and they may be located in a variety of settings, including hospitals, research centers, and specialized laboratory facilities.

| Key Elements | Scope |

| Market Size in 2026 | USD 7.17 Billion |

| Projected Market Size in 2035 | USD 15.78 Billion |

| CAGR (2026 - 2035) | 9.16% |

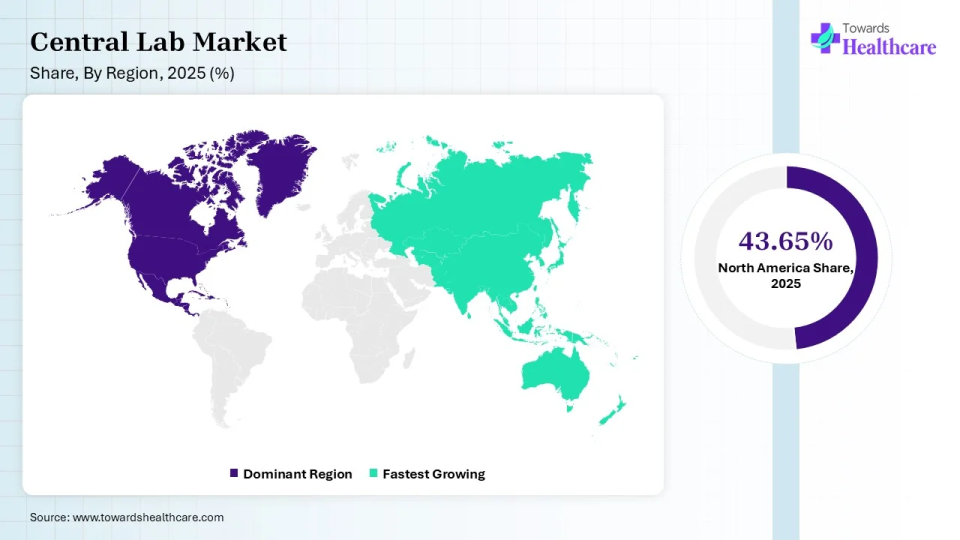

| Leading Region | North America by 43.65 |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Clinical Trial Phase, By Modality, By End-User |

| Top Key Players | ACM Global Laboratories, CIRION BioPharma Research, Eurofins Scientific, ICON plc, Intermountain Health, IQVIA, LabConnect, Labcorp, Medpace, Reprocell, SGS S.A., Thermo Fisher Scientific |

Which Product Type Segment Dominated the Central Lab Market?

Biomarker services play a crucial role in advancing precision medicine, a medical approach that tailors treatments to individual patients based on their genetic makeup, lifestyle, and other factors. Biomarkers are biological indicators that can be used to predict, diagnose, and monitor diseases, as well as to measure the effectiveness of treatments.

Central labs, which provide clinical trial testing services, have been increasingly incorporating biomarker services into their offerings. These services can include the development of biomarker assays, sample analysis, and data interpretation. By providing these services, central labs can help pharmaceutical and biotech companies identify the right patient populations for clinical trials and better understand the efficacy and safety of their drugs.

Biomarker services have also been instrumental in the development of new treatments for diseases, including cancer. For example, biomarkers can help identify which patients are most likely to respond to certain cancer treatments, allowing for more targeted therapies and better patient outcomes. Thus, the incorporation of biomarker services into central labs' offerings has helped drive growth in the central lab market by increasing the demand for more advanced and personalized clinical trial testing services.

How the Pharmaceutical Companies Dominated the Central Lab Market?

Pharmaceutical dominance has fueled the expansion of central lab services in recent years. With the increasing number of clinical trials and research activities conducted by pharmaceutical companies, the demand for central lab services has grown significantly.

Central labs play a crucial role in clinical trials, providing accurate and reliable testing services for the evaluation of drug efficacy and safety. As the pharmaceutical industry continues to grow, so does the demand for central lab services, driving market expansion.

Pharmaceutical companies accounted for the largest revenue shareholder by end-user, in 2022 with around 45.8% market share in the central lab market. And are projected to register the highest growth over the forecast period with a CAGR of 6.1% (2022-2032).

In addition, the rising trend of personalized medicine has also contributed to the growth of central lab services. Personalized medicine relies on the use of biomarkers to identify patients who are likely to respond to a particular treatment. Central labs provide biomarker testing services that enable clinicians to make more informed treatment decisions, leading to better patient outcomes.

Furthermore, the increasing prevalence of chronic diseases such as cancer and cardiovascular diseases has also driven the demand for central lab services. These diseases require continuous monitoring of biomarkers and other laboratory parameters, which can be provided by central labs. The pharmaceutical industry's dominance, the rising trend of personalized medicine, and the increasing prevalence of chronic diseases are the key drivers fueling the expansion of central lab services.

")

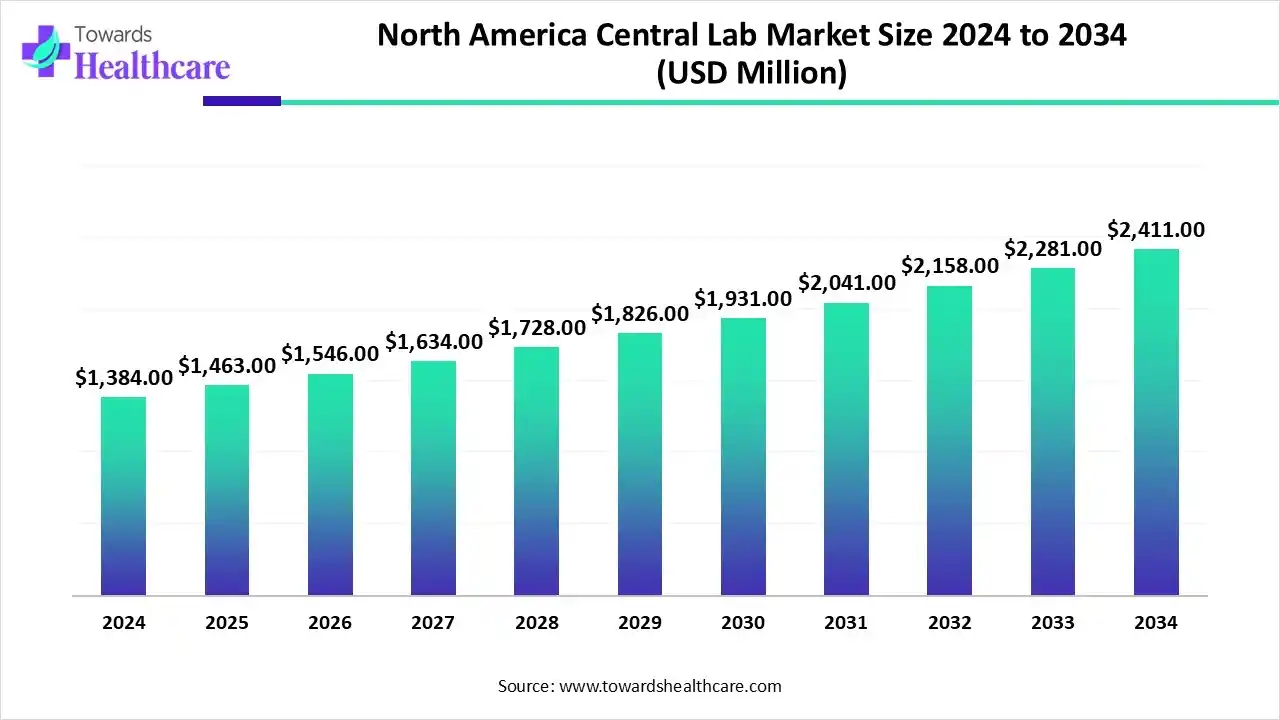

The North America central lab market size is calculated at USD 2.84 billion in 2025, grew to USD 3.11 billion in 2026, and is projected to reach around USD 6.37 billion by 2035. The market is expanding at a CAGR of 8.31% between 2026 and 2035.

")

The central lab market is witnessing growth globally, with North America leading the market by 43.65% share in 2025, followed by Europe and the Asia Pacific. The North American market is driven by factors such as the increasing number of clinical trials, the presence of key players, and a favorable regulatory environment. The presence of leading pharmaceutical and biotechnology companies in the region is also contributing to market growth. The U.S. conducts the highest number of clinical trials globally. According to the WHO International Clinical Trials Registry Platform (ICTRP), the number of trials conducted in the US from 1999 to 2022 was 168,520, whereas that in Canada was 34,041. While the total number of clinical trials in the entire North American region was around 11,935 in 2022.

U.S. Market Trends

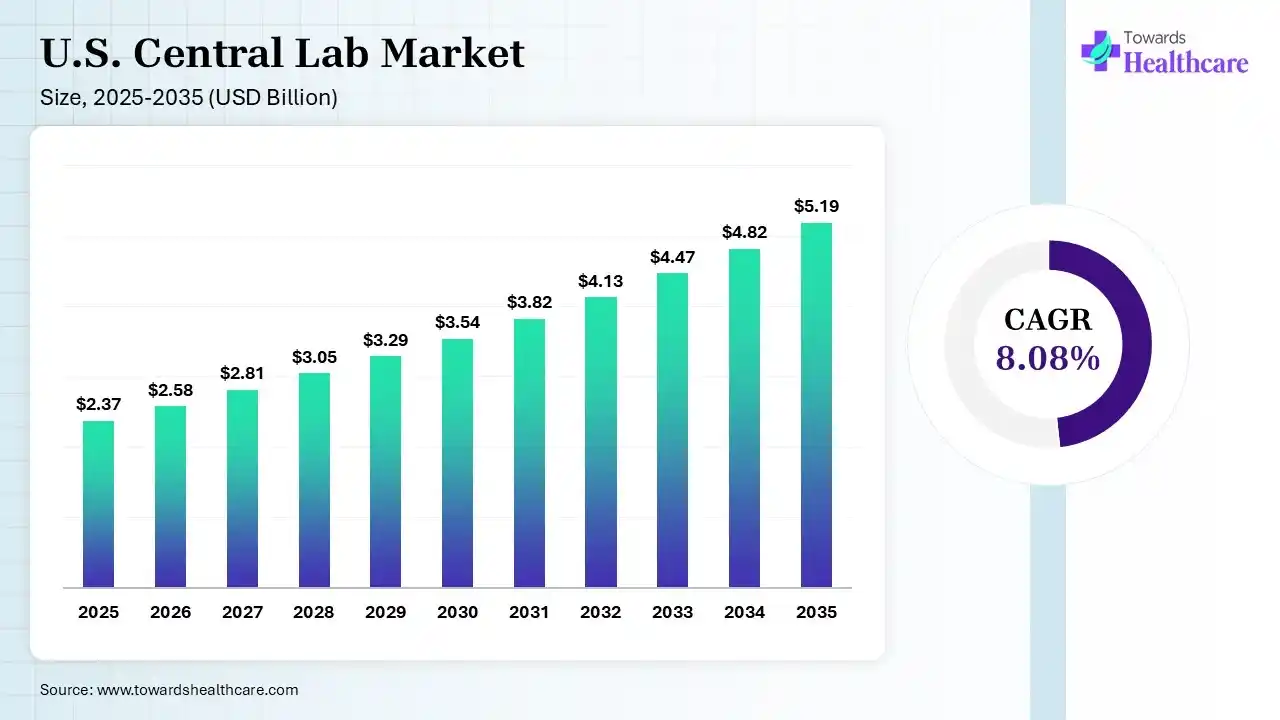

The U.S. central lab market size was estimated at USD 2.37 billion in 2025 and is predicted to increase from USD 2.58 billion in 2026 to approximately USD 5.19 billion by 2035, expanding at a CAGR of 8.08% from 2026 to 2035.

")

U.S. boasts a dominant position in the global central lab market, and this dominance is attributed to the strong healthcare infrastructure comprising a well-developed network of laboratories, research institutions, and academic medical centers. Being a major hub for clinical research, the U.S. not only offers high-quality central lab services but also enhances its operational efficiency and capabilities. The high investment in research and development in the pharmaceutical and biotechnology sectors led to the adoption of innovative laboratory technologies and testing methods

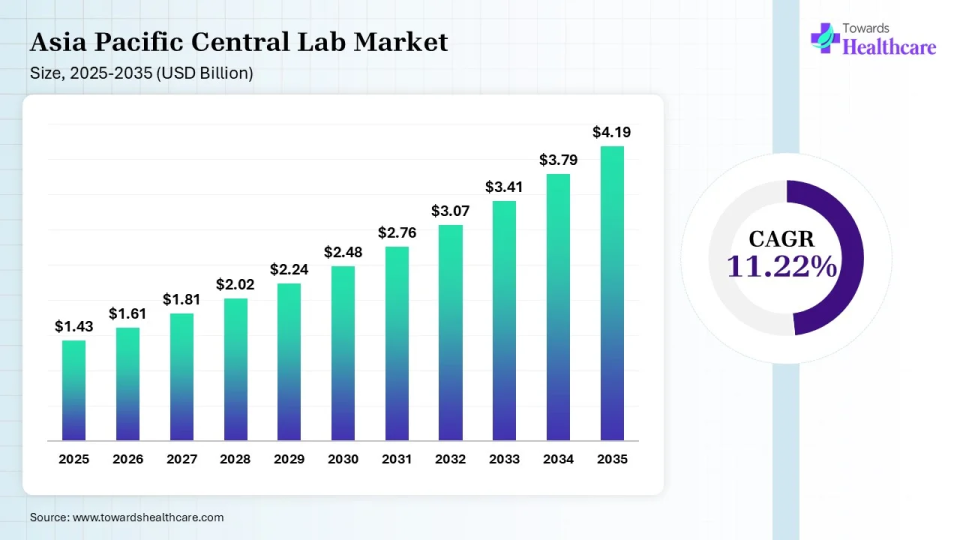

The APAC central lab market size was estimated at US$ 1.43 billion in 2025, projected to increase to US$ 1.61 billion in 2025 and reach US$ 4.19 billion by 2035, showing a healthy CAGR of 11.22% across the forecast years.

")

On the other hand, the Asia Pacific region is expected to emerge as a significant market for central lab services, owing to the increasing number of clinical trials in the region, growing healthcare infrastructure, and rising investments by pharmaceutical and biotechnology companies. The Asia Pacific market is expected to witness significant growth in countries such as China, India, and Japan, major clinical research hubs. Singapore has emerged as a hub for central labs in the Asia-Pacific region. The number of clinical trials in China, Japan, and India is rapidly rising. China conducted 94,193 clinical trials, whereas Japan and India conducted 63,499 and 54,891 clinical trials, respectively, from 1999 to 2022.

Furthermore, the increasing prevalence of chronic diseases, the growing geriatric population, and the rising demand for personalized medicine are expected to drive market growth in the region. The market is also expected to witness growth in emerging economies such as Brazil and South Africa, owing to the increasing number of clinical trials and the growing focus on healthcare infrastructure development.

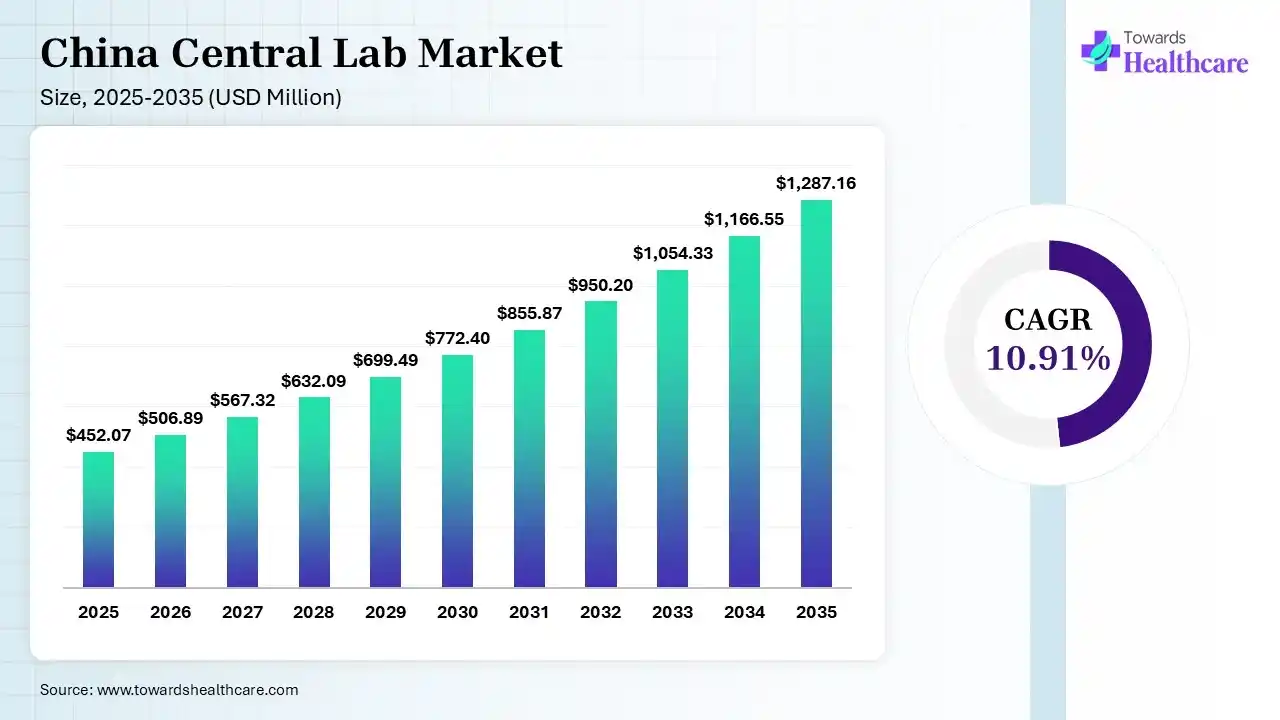

The China central lab market size was estimated at USD 452.07 million in 2025 and is predicted to increase from USD 506.89 million in 2026 to approximately USD 1287.16 million by 2035, expanding at a CAGR of 10.91% from 2026 to 2035.

")

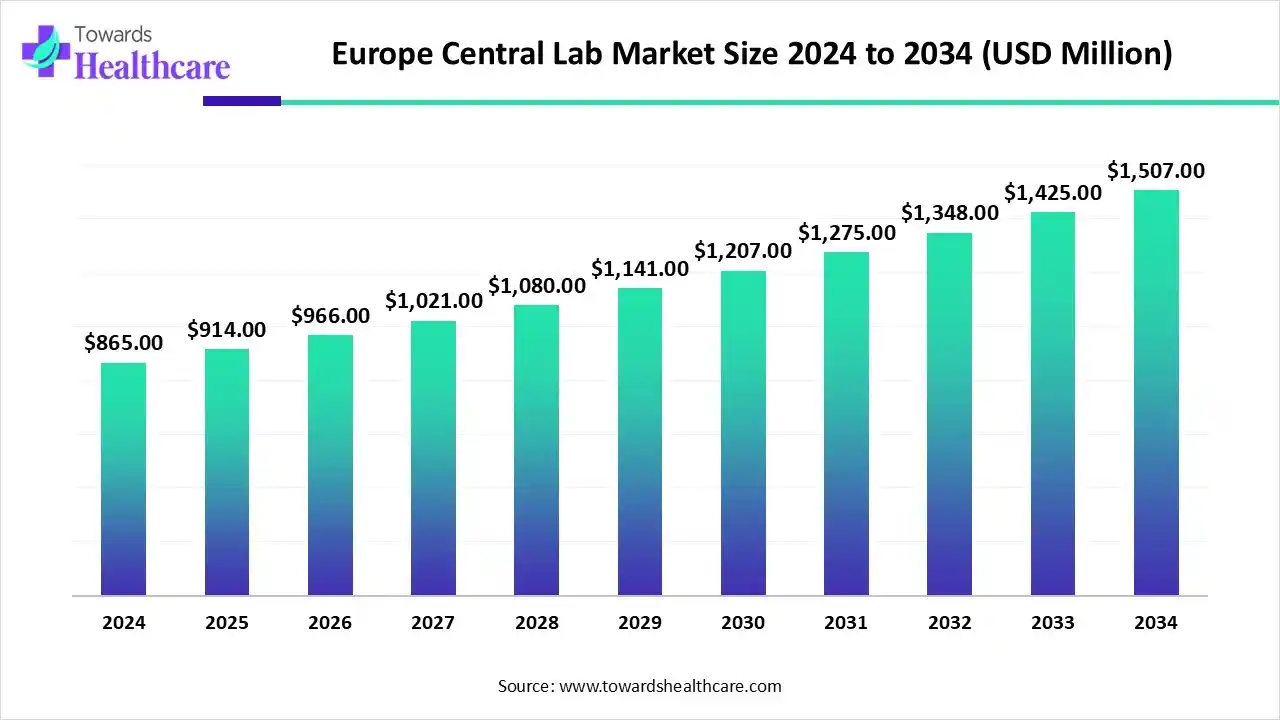

The Europe central lab market size was reported at US$ 1.77 billion in 2025 and is expected to rise to US$ 1.93 billion in 2026. According to forecasts, it will grow at a CAGR of 8.34% to reach US$ 3.98 billion by 2035.

")

Europe is considered the fastest-growing market for central lab services. The European market is driven by a strong life sciences ecosystem, which boasts a long history of pharmaceutical discovery and the life sciences industry. The adoption of electronic lab notebooks and lab automation in Europe is rising, and it is propelled by investments by prominent firms like LabWare and Merck. The significant investments by the region in the pharmaceutical industry for research and development also create a demand for central lab services, especially since the German market is experiencing rapid growth, fueled by increasing R&D investments and the development of new life sciences research centers.

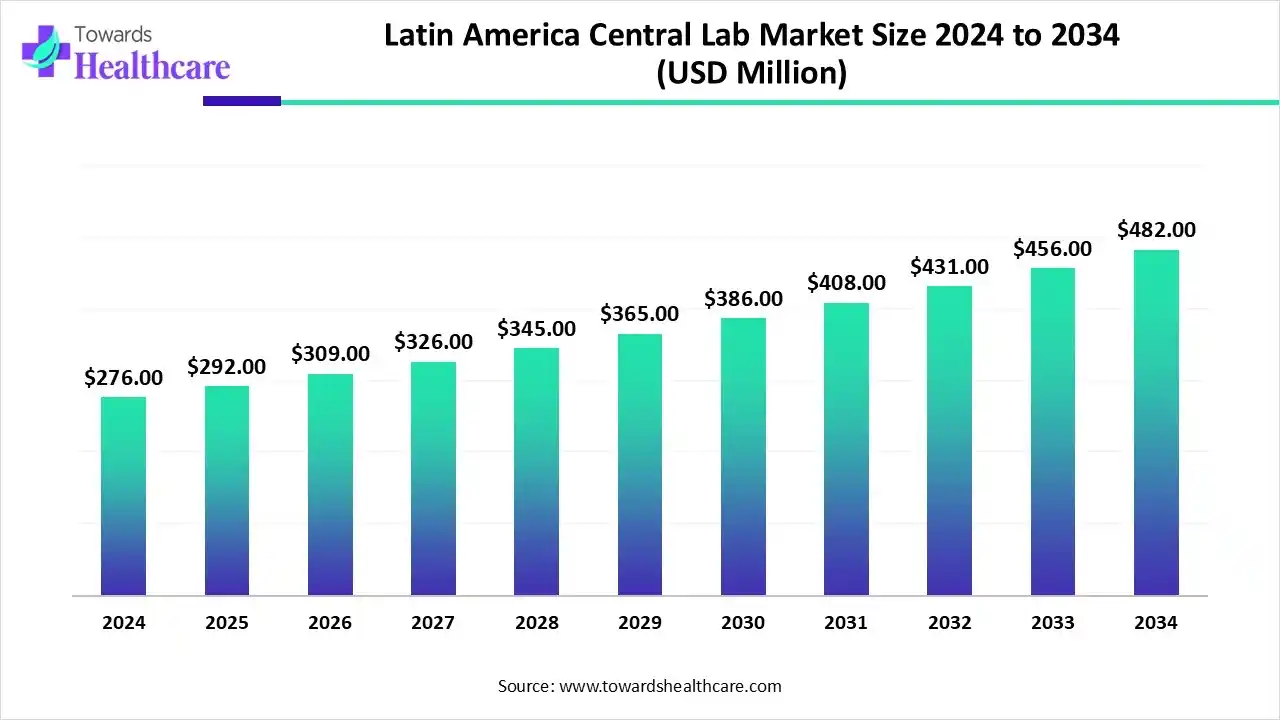

The Latin America central lab market size reached US$ 289.89 million in 2025 and is anticipate to increase to US$ 322.51 million in 2026. By 2035, the market is forecasted to achieve a value of around US$ 773.25 million, growing at a CAGR of 10.20%.

")

The Latin America central lab market is experiencing steady growth, driven by the rising number of clinical trials, expanding pharmaceutical and biotechnology sectors, and improved regulatory frameworks. Growing demand for high-quality diagnostic services and standardized testing supports this trend. Among regional countries, Brazil dominates the market due to its advanced healthcare infrastructure, skilled workforce, and strong government initiatives to promote clinical research and innovation.

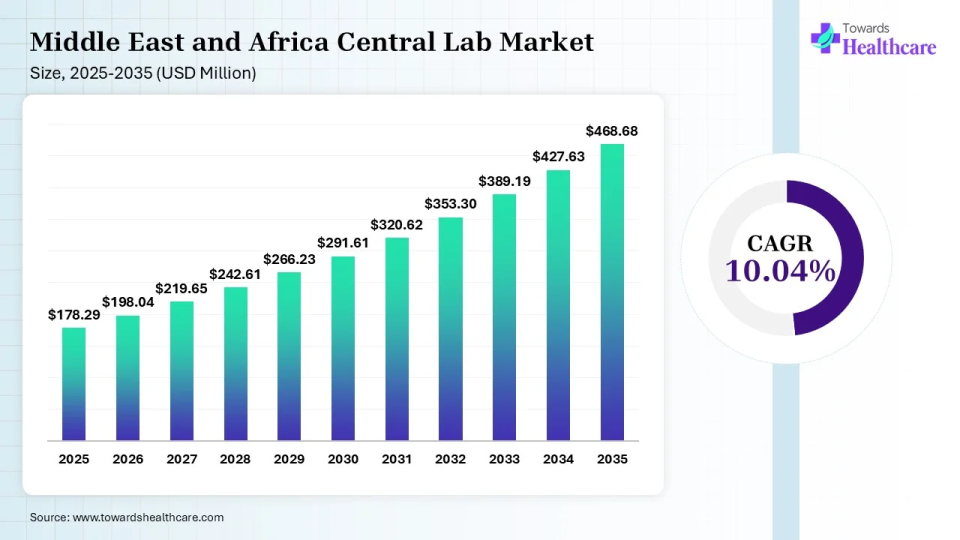

The Middle East & Africa central lab market size reached US$ 178.29 million in 2025 and is expected to increase to US$ 198.04 million in 2026. By 2035, the market is forecasted to achieve a value of around US$ 468.68 million, growing at a CAGR of 10.04%.

")

The Middle East & Africa are considered to be a significantly growing area, due to the increasing number of clinical trials and favorable government support. The growing awareness of decentralized trials and the burgeoning pharma and biotech sectors augment the market. The rising demand for personalized medicines encourages companies to develop innovative biologics and conduct clinical trials, potentiating the demand for central lab services.

The Dubai Central Laboratory (DCL) Department in Dubai Municipality and the Abu Dhabi Quality and Conformity Council are some central labs in the UAE. These labs ensure the quality of materials and products and preserve the environment and public health. The increasing public-private partnerships also facilitate clinical trials and sample testing & analysis.

The central lab market has been growing steadily in recent years, driven by a range of factors such as increasing demand for clinical research, advancements in technology, and the need for better patient outcomes. In particular, the growing number of clinical trials has been a major driving force behind the expansion of the central lab market. As the pharmaceutical industry continues to develop new drugs and therapies, the demand for clinical trials is expected to increase further. Central labs play a critical role in supporting these trials by providing a range of testing and analysis services, including sample testing, biomarker analysis, and data management.

In addition, advancements in technology have made it easier and more efficient for central labs to handle large volumes of data and samples. This has led to increased productivity and faster turnaround times, which are important factors in the success of clinical trials. Thus, the growth of the central lab market is closely linked to the pharmaceutical industry and the demand for clinical research. As the industry continues to innovate and develop new treatments, the importance of central labs in supporting clinical trials is only expected to increase.

The central labs market is experiencing significant growth, with one of the driving factors being the increase in R&D investment. As pharmaceutical companies seek to develop more effective drugs and therapies, they are investing more in clinical trials, which require the services of central labs. For instance, IQVIA spent around $160 billion on outsourced R&D in biopharmaceutical expenditure on drug development, in 2022.

The growing investment in R&D is not limited to pharmaceutical companies, as academic institutions, government organizations, and biotech startups are also increasing their research budgets. This trend is expected to continue, driving demand for central lab services in the coming years. To meet the growing demand for central lab services, many companies are expanding their central lab facilities.

Additionally, the rise of precision medicine and personalized healthcare is fueling the need for advanced diagnostics and biomarker testing, which are often conducted by central labs. These factors are further driving the growth of the central lab market.

The increasing demand for precision medicine and personalized healthcare is a major driving force behind the growth of the central lab market. With the aim of developing targeted treatments that cater to the specific needs of individual patients, more sophisticated diagnostics and biomarker testing are needed, which in turn require the expertise of clinical trials. This has resulted in the increased use of biomarkers to identify specific diseases and to stratify patient populations for clinical trials.

Central labs are time-consuming because they involve multiple steps in the process of sample collection, transportation, analysis, and reporting. The market is also experiencing challenges due to the lack of skilled professionals. There are several ways to overcome these obstacles.

Automation can significantly reduce the time and effort required for laboratory testing, allowing central labs to process more samples in a shorter amount of time. This can help reduce turnaround times and improve overall efficiency, boosting customer satisfaction and driving market growth.

In addition, to ensure that central lab staff are equipped with the necessary skills and knowledge, it is essential to invest in training and education programs. By expanding these programs, central labs can improve the quality of their services and gain a competitive edge in the market.

Furthermore, emerging markets such as Asia Pacific and Latin America offer significant growth opportunities for the central lab market. By expanding into these regions, central labs can tap into new customer bases and drive market growth. Adopting innovative technologies such as digital pathology and next-generation sequencing can help central labs improve the accuracy and speed of their testing processes. This can help boost customer confidence and drive market growth.

Moreover, by offering value-added services such as consulting, data analysis, and clinical trial management, central labs can differentiate themselves from competitors and provide additional value to customers. This can help boost customer retention and drive market growth.

Central laboratory logistics can present several challenges in the context of clinical trials. These challenges can arise due to several factors, including the need to handle a large volume of patient samples, the requirement for a standardized sample collection process across multiple study sites, and the need for timely and accurate delivery of samples to the central laboratory. One of the main challenges in central lab logistics is ensuring the quality and integrity of samples during transportation. Samples must be transported under appropriate conditions to prevent degradation and maintain their stability. This requires specialized packaging, temperature monitoring, and transportation protocols to ensure that samples are delivered to the central laboratory in optimal condition.

Another challenge is ensuring the timely delivery of samples to the central laboratory. Delayed or lost shipments can result in compromised sample quality, inaccurate test results, and delays in the clinical trial timeline. This requires careful coordination between the study sites, clinical research organizations (CROs), and logistics providers to ensure that samples are collected, shipped, and received in a timely and efficient manner.

Additionally, there can be challenges related to data management and communication between study sites and the central laboratory. This requires a robust information technology infrastructure and effective communication channels to ensure that data and results are transmitted accurately and securely. Thus, successful navigation of central lab logistics requires a combination of specialized expertise, effective communication, and careful planning and execution to ensure that clinical trial timelines and objectives are met.

The virtual reporting revolution is transforming the clinical research industry by providing more efficient, accurate, and cost-effective solutions. Automation is driving revenue opportunities for clinical research by streamlining data management, reducing turnaround time, and increasing productivity. Virtual reporting solutions leverage artificial intelligence, machine learning, and natural language processing to automate data extraction, processing, and analysis. This eliminates the need for manual data entry, reduces errors, and improves the accuracy and speed of data reporting. Virtual reporting solutions also enable real-time data analysis, making it easier to identify trends, outliers, and potential issues, thereby improving decision-making.

In addition, the adoption of virtual reporting solutions is expected to drive revenue opportunities for the clinical research industry, as it allows companies to manage large data volumes more efficiently and effectively. It also improves the accuracy and speed of data processing and reporting, which can help companies bring products to market faster and with greater confidence.

Furthermore, virtual reporting solutions can be integrated with other systems, such as electronic data capture (EDC) and clinical trial management systems (CTMS), further streamlining the clinical trial process. This integration can improve data quality, reduce costs, and enhance collaboration among stakeholders. Moreover, the adoption of virtual reporting solutions is expected to drive revenue opportunities for the clinical research industry by improving the efficiency, accuracy, and speed of data reporting, enabling real-time data analysis, and integrating with other systems to streamline the clinical trial process.

Leon Wyszkowski, President, Analytical Services, Clinical Research, Thermo Fisher Scientific, commented on its expansion in Europe that they can use the most technologically advanced systems to develop assays supporting early discovery and then apply them for testing of clinical trial samples. Their new facility in Sweden will provide accurate and timely data and empower their customers to make informed decisions.

By Service Type

By Therapeutic Area

By Clinical Trial Phase

By Modality

By End-User

By Geography

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar