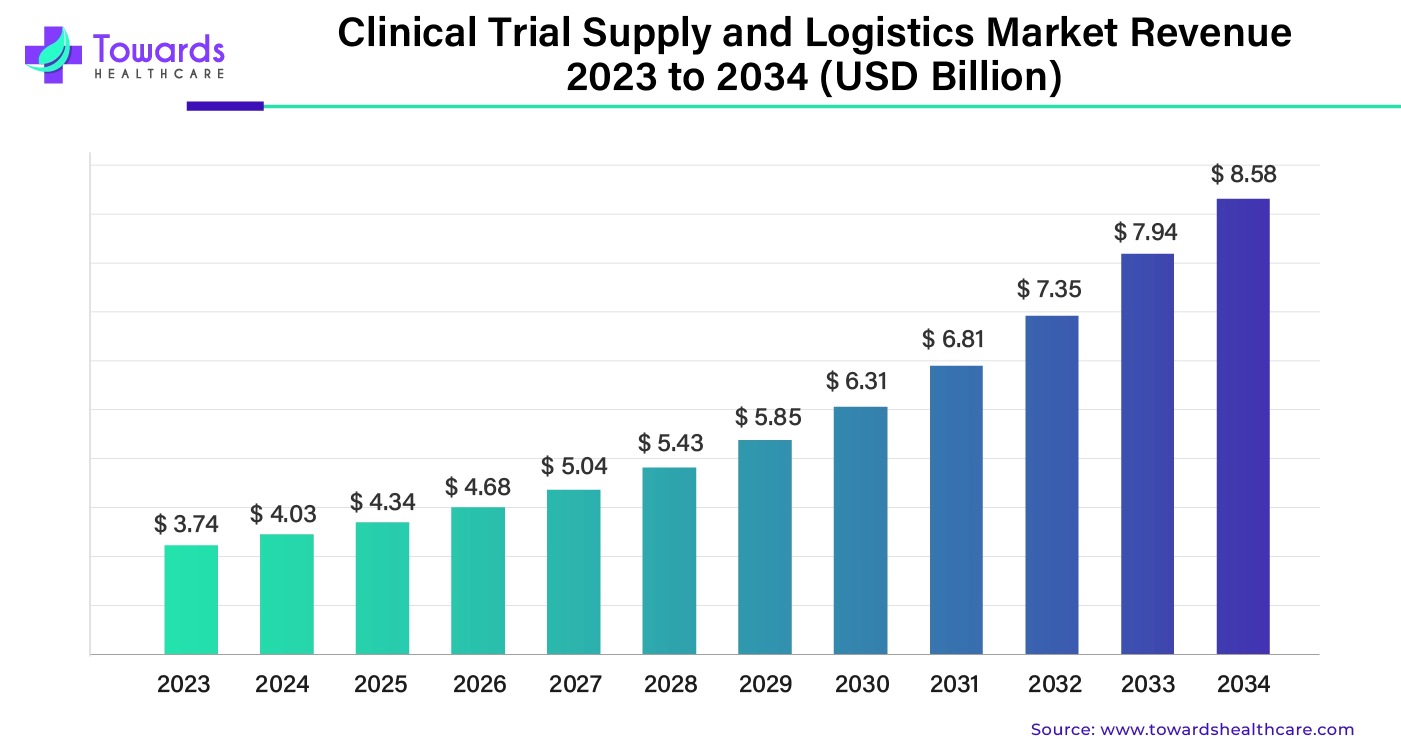

The clinical trial supply and logistics market was estimated at US$ 3.74 billion in 2023 and is projected to grow to US$ 8.58 billion by 2034, rising at a compound annual growth rate (CAGR) of 7.63% from 2024 to 2034.

The clinical trial supply and logistics include sourcing, packaging, labeling, storing, and distributing pharmaceutical and biotechnological products, medical devices, and related materials required for a clinical trial. Clinical trials require ancillary supplies like medical equipment, centrifuges, disposable products, case report forms (CRF), and investigator literature. The clinical trial supply and logistics company provides these services along with regulatory requirements for timely delivery. A clinical trial supply chain involves all steps from storage to distribution of clinical trial products, while clinical trial logistics involve planning, managing, and executing the supply of products. This type of service overcomes several challenges of a clinical trial, such as regulatory specifications for the import and export of products, geographical challenges for conducting trials at multiple locations, and compliance management for maintaining consistency and integrity in the storage and supply of products.

The integration of AI in various sectors has provided numerous benefits, includIng the healthcare sector. AI can optimize and simplify several processes in biopharmaceutical & biotechnology companies. The supply chain and logistics can be automated with recent advancements in machine learning (ML) and the Internet of Things (IoT). It includes everything from automated inventory management systems to sophisticated tracking and monitoring tools. AI can be used to analyze problems in the supply chains related to inventory, production bottlenecks, and other areas. Additionally, AI can be used to find the best logistics route based on the particular needs of a shipment and can adjust in real-time to changing conditions.

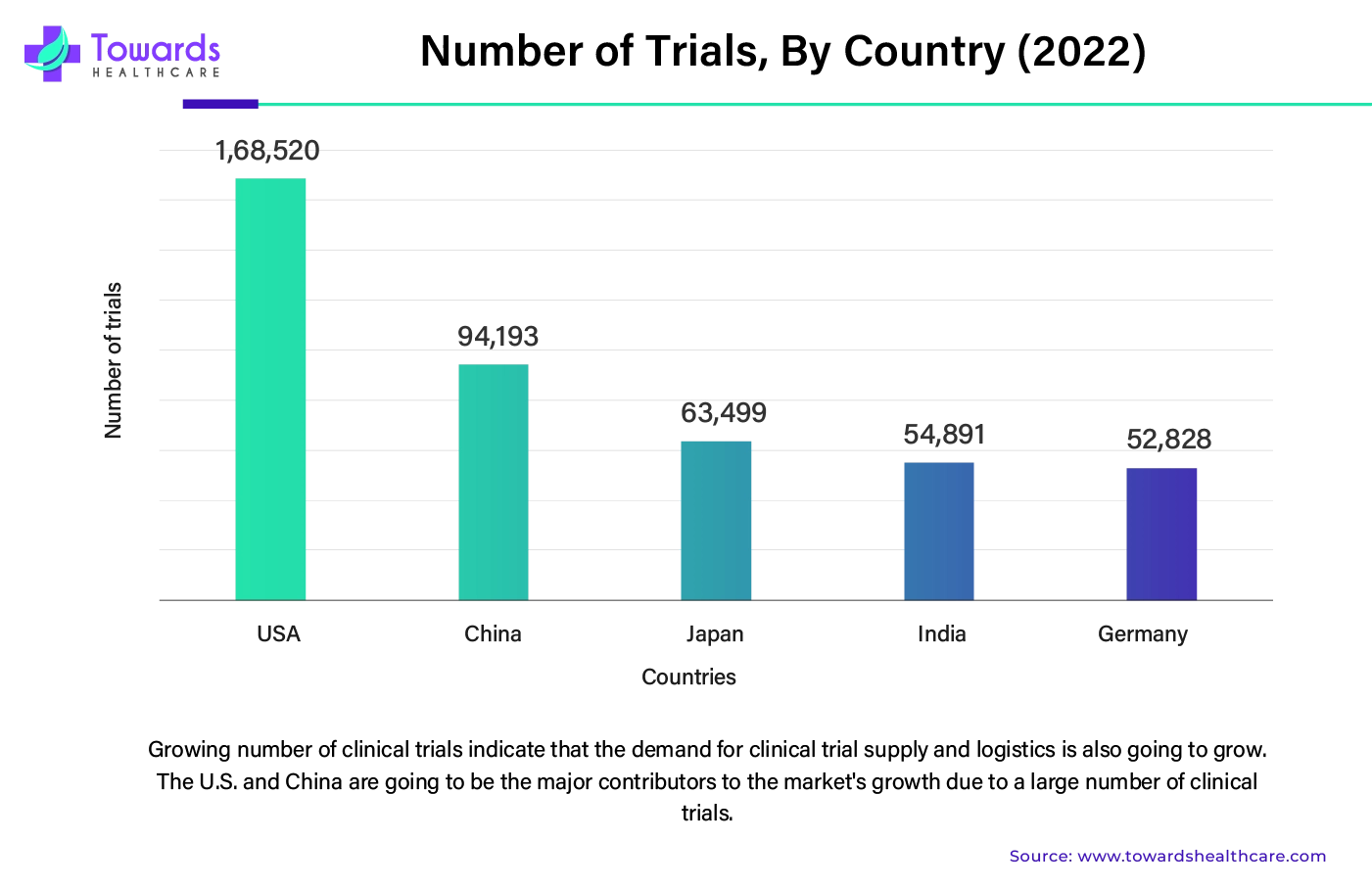

The rising incidences of chronic disorders, autoimmune disorders, infectious diseases, and genetic disorders necessitate the development of new drugs, vaccines, and cell and gene therapy products. Several research firms and institutions are investigating the development of these products to treat several disorders. Clinical trial data are also required for novel use of an existing drug or combination therapies. Clinical trials provide safety, tolerability, pharmacokinetics, pharmacodynamics, and toxicity data of products in humans. Hence, drug approval agencies require preclinical and clinical trial data to successfully approve these products for human use. The growing research and development and rising incidences of chronic disorders drive the market. The US, China, Japan, India, and Germany are the top five countries conducting the highest number of clinical trials. The other countries include the UK, France, Iran, Canada, and Spain.

")

The clinical trial supply chain and logistics face several challenges. The major challenge is the increased transportation and logistics costs due to the rise in petrochemical prices and the Russia-Ukraine conflict. Another challenge is the inconsistency in tracking, which decreases efficiency and workforce productivity. The lack of communication and tracking orders also pose a challenge to the consumers. This leads to unnecessary delays in deliveries and reduced operational efficiencies.

A clinical trial supply chain assists in logistics and transportation, effective inventory management, warehousing and storage solutions, and accurate demand planning and forecasting. The increasing demand for cell and gene therapy products and the increasing number of trials testing cell and gene therapy products boost the market. The supply chain and logistics for cell and gene therapy need to meet several criteria for a high-touch and customized supply chain. Additionally, the increasing investments and collaborations and technological advancements like automation and digitization further promote market growth. According to the IQVIA report, the global investment in cell and gene therapy products was around $5.9 billion in 2023. Also, in 2023, a total of 76 cell and gene therapy products were launched globally.

")

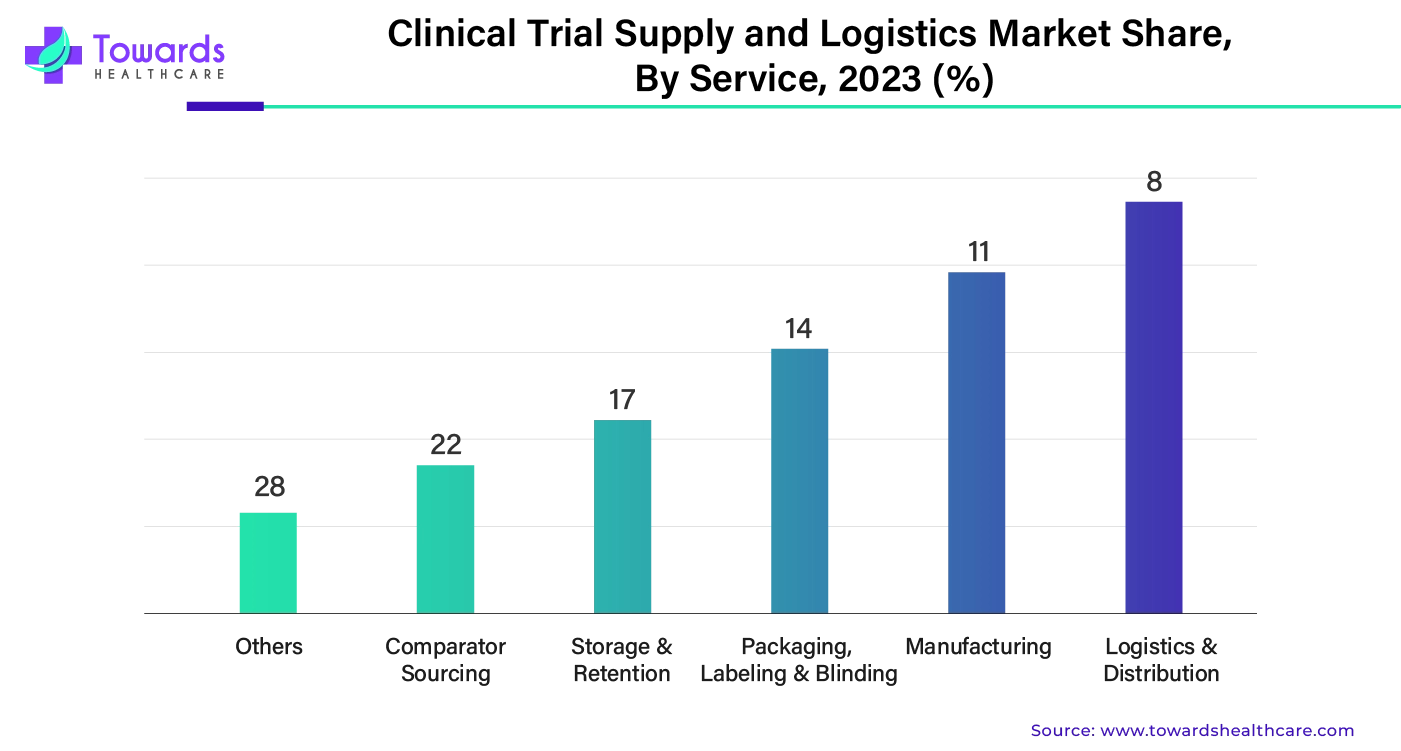

By service, the logistics & distribution segment led the global clinical trial supply and logistics market by 28% in 2023. Clinical trial logistics involve managing and coordinating resources, materials, and procedures for moving, storing, and distributing products for clinical trials. The logistics and distribution service cater to client requirements by providing specialized transportation options. Biologics like vaccines require stringent conditions like cold storage to avoid degradation. Logistics and distribution services provide multi-temperature storage facilities to support a secure and successful clinical trial supply chain service. The rising development of biologics and advancements in technologies drive the market.

By service, the manufacturing segment is expected to grow significantly in the clinical trial supply and logistics market holding 22% shares in 2023. Many pharmaceutical & biotechnology companies give contracts for the manufacturing of clinical trial products to the Contract Development & Manufacturing Organizations (CDMO). CDMOs contain the desired facilities like a sterile environment, chambers to conduct stability testing, and analytical method development and quality control testing services. Hence, CDMOs provide the expertise and all the in-house facilities that some companies do not have. The increasing clinical trials, demand for quality products, and technological advancements boost the market.

For instance,

")

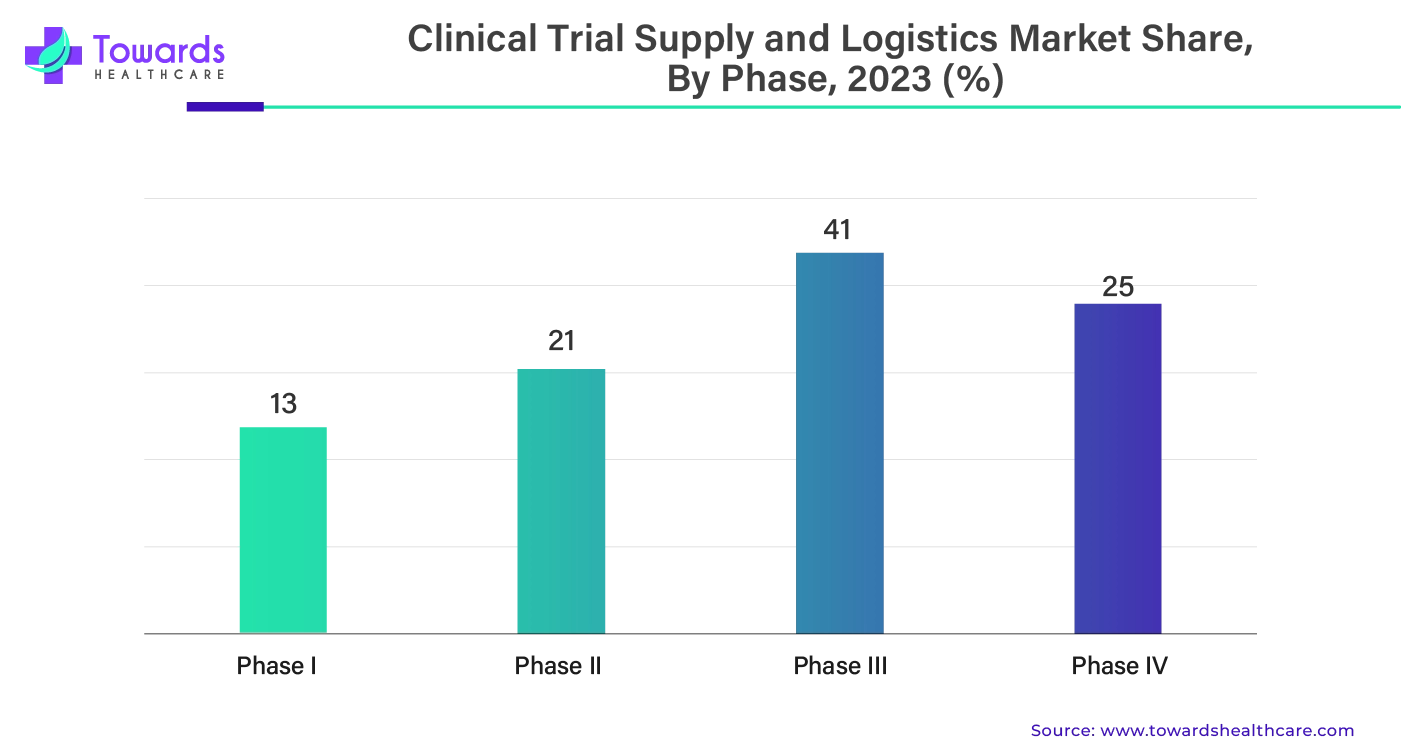

By phase, the phase III segment held a dominant presence in the clinical trial supply and logistics market by 41% in 2023. Phase III clinical trials are conducted to determine a drug’s safety and efficacy and monitor side effects in a diseased population. Phase III trials are conducted at multiple centers in different geographical locations with several hundred or thousand patients. Phase III trials are performed on 300 to 3000 participants. Since phase III trials are conducted at a large scale, they require regulatory approvals and an efficient supply chain for the timely delivery of products.

By phase, the phase II segment is projected to expand at the fastest rate in the clinical trial supply and logistics market in the coming years holding 21% shares in 2023. Phase II trials are conducted to determine the effectiveness of a drug. Phase II trials are conducted with 100 to 300 participants and may last from several months to two years. Approximately 70% of the drugs reach phase II trials after passing the phase I trials. Hence, more drugs reaching clinical trials require supply chain and logistics services.

")

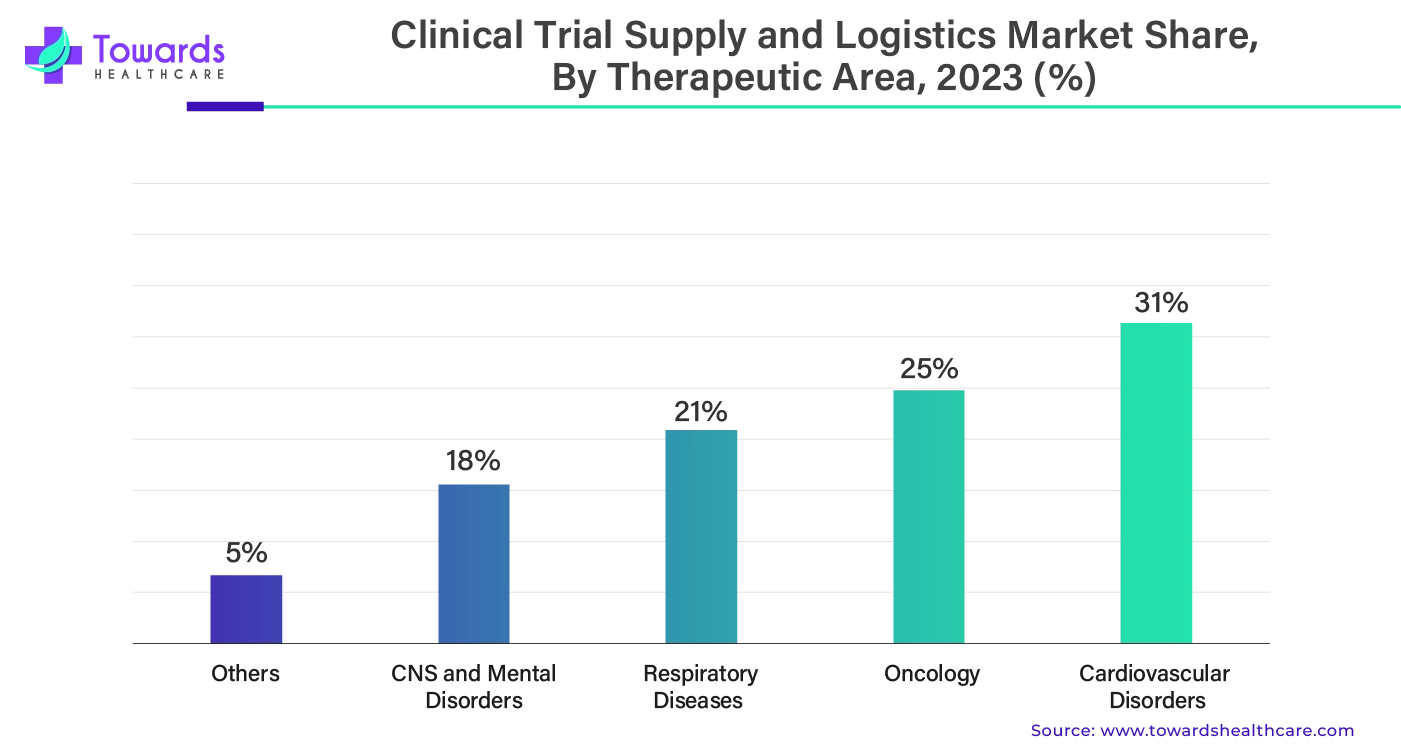

By therapeutic area, the cardiovascular disorders segment registered its dominance over the global clinical trial supply and logistics market share by 31% in 2023. Cardiovascular disorders like coronary heart disease, cerebrovascular disease, rheumatic heart disease, etc., are the leading cause of death globally. According to the WHO, an estimated 17.9 million people die from cardiovascular disorders each year globally. The rising geriatric population and sedentary lifestyle increase the risk of these disorders. At present, 2,419 clinical trials are performed for various cardiovascular disorders. The rising prevalence of cardiovascular disorders and new drug development augment the market.

By therapeutic area, the oncology segment is predicted to witness significant growth in the clinical trial supply and logistics market over the forecast period holding 25% market shares in 2023. The increasing incidences of cancer cases, novel cancer therapeutic research, and increasing number of clinical trials drive the market. According to the GLOBOCAN report, approximately 20 million cancer cases were reported in 2022, with 9.7 million deaths. Cancer research is the most prominent research topic among researchers globally. Currently, there are 7,666 ongoing clinical trials for cancer.

")

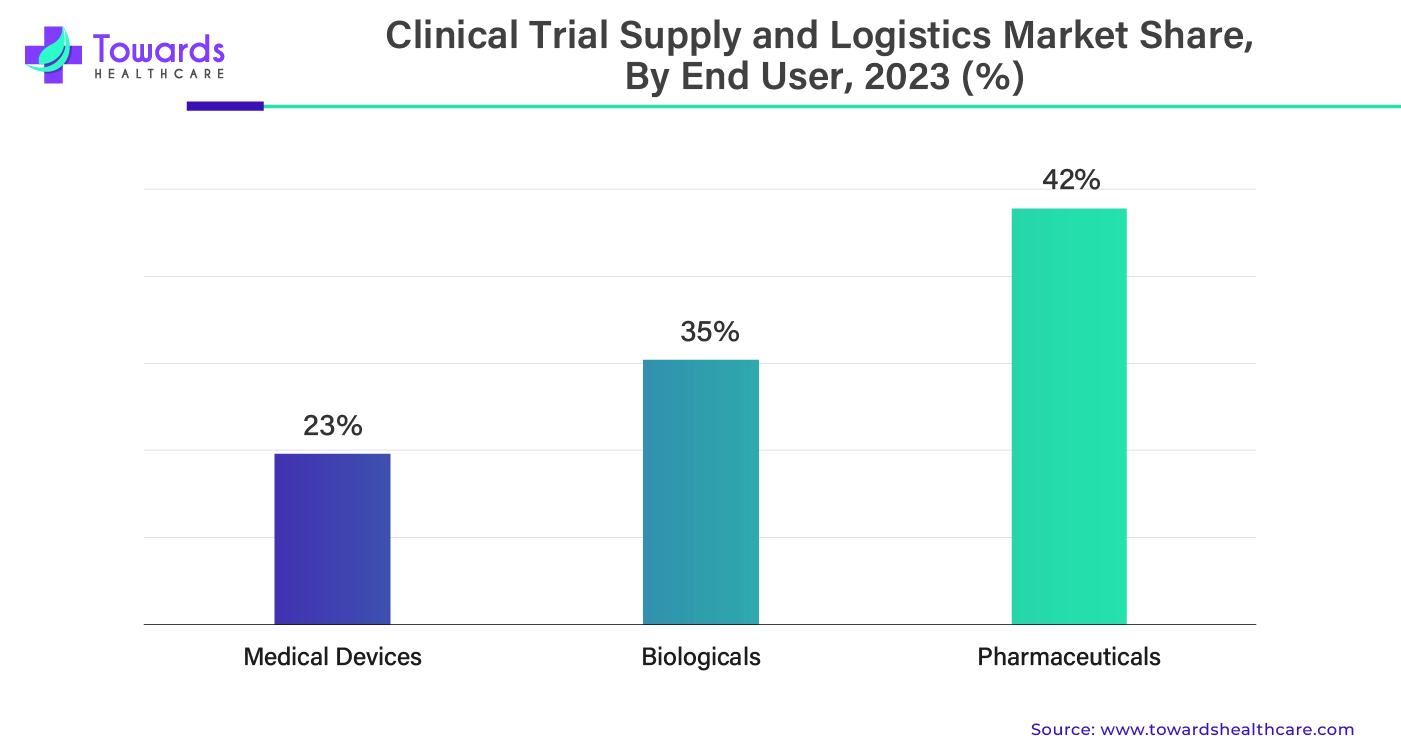

By end-use, the pharmaceuticals segment dominated the global clinical trial supply and logistics market share by 42% in 2023. Clinical trials for small molecules are the most prevalent for treating several disorders. The increasing R&D activities, patent filings, demand for personalized medicines, and drug repurposing drive the market. The traditional drug discovery and development process takes around 13-14 years for a drug to be marketed. Hence, the clinical trial supply chain and logistics assist in a faster supply of drugs to the patients, which, in turn, improves the speed to market. This further makes the process cost-effective from improved supply chain planning.

By end-use, the biologicals segment will grow at a significant rate in the clinical trial supply and logistics market over the studied period of 2024 to 2034 holding 35% shares in 2023. The rising incidences of infectious diseases and growing research on biologicals drive the market. Biologicals require stringent conditions for storage and transportation, such as multi-temperature requirements.

")

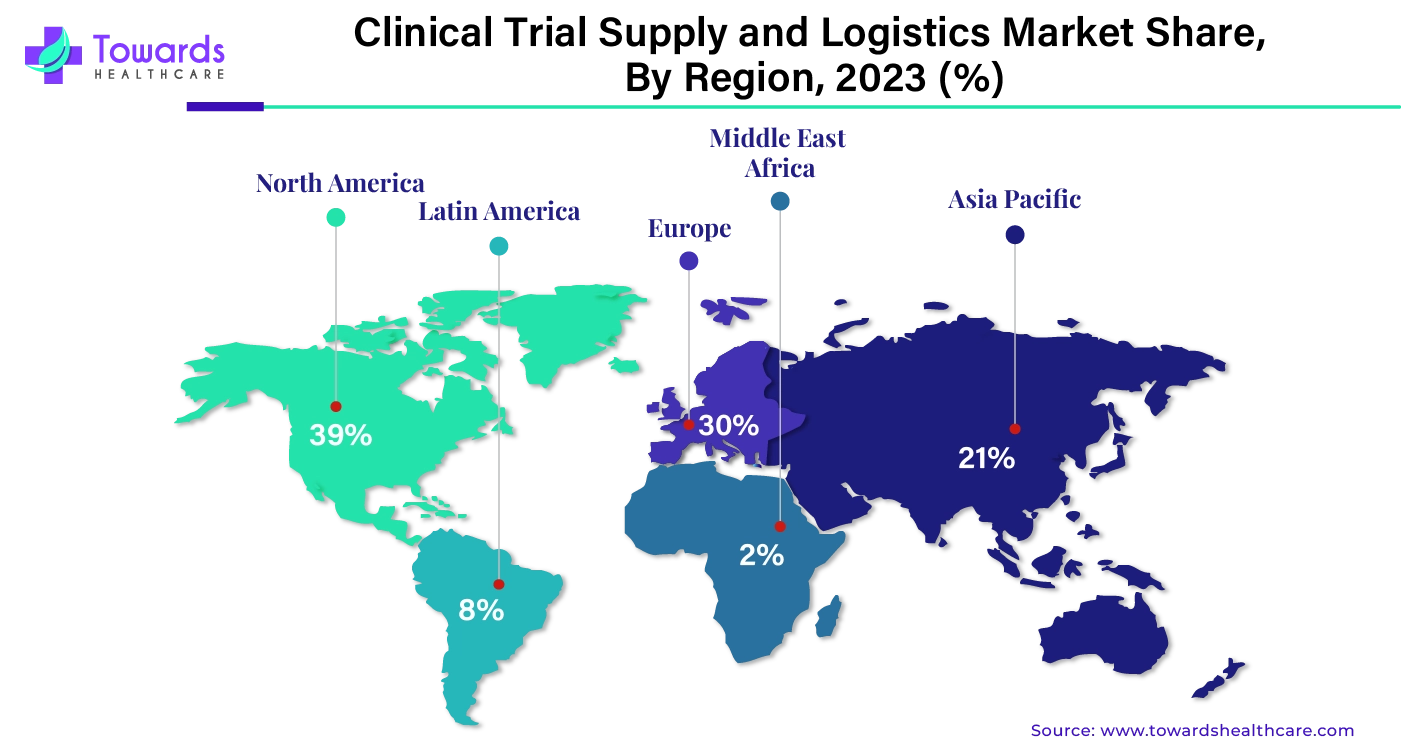

North America held a significant share of the clinical trial supply and logistics market by 39% in 2023. The state-of-the-art research and development facilities, advanced healthcare infrastructure, higher number of ongoing clinical trials, and technological advancements augment the market. According to the WHO International Clinical Trials Registry Platform (ICTRP), the number of trials conducted in the US from 1999 to 2022 was found to be 168,520, whereas that in Canada was found to be 34,041. The number of trials in 2022 in the North American region was around 11,935. Additionally, the rising investments in pharmaceutical and biopharmaceutical R&D boost the market in North America. Countries like the US and Canada are at the forefront of driving the clinical trials supply chain and logistics market in North America.

For instance,

Asia-Pacific is anticipated to grow fastest in the market during the forecast period. The rising number of trials, chronic disorders, growing research and development activities, and the increasing number of pharmaceutical companies boost the clinical trial supply and logistics market. China, India, and Japan are among the top five nations globally, with the highest number of clinical trials between 1999 and 2022. Apart from these countries, clinical trials are also widely conducted in Australia, South Korea, Singapore, Thailand, Vietnam, and the Philippines. Additionally, the presence of key players like Credevo, Catalent, and FedEx further augment the market. Furthermore, access to a diverse patient population, lower recruitment costs, and favorable policies promote market growth

For Instance,

Europe is anticipated to grow at a notable rate in the foreseeable future. The increasing number of clinical trials and the growing research and development activities are the major growth factors of the market in Europe. The presence of key players and favorable regulatory frameworks boosts the market. The availability of suitable logistics and the burgeoning healthcare sector contribute to market growth. The increasing number of CDMOs and CMOs, and the growing focus on product marketing and regulations, foster the need for clinical trial supply and logistics.

Germany has registered 26,694 clinical trials on the clinicaltrials.gov website as of May 2025. The German government’s National Pharma Strategy aims to reverse the declining trend of clinical trial participation by facilitating faster trial approvals, improving market access, and reducing regulatory barriers. The strategy focuses on accelerating clinical research and enhancing Germany’s appeal to pharmaceutical companies.

| Company Name | Thermo Fisher Scientific, Inc. |

| Headquarters | Waltham, Massachusetts, United States |

| Recent Development | In June 2024, Thermo Fisher Scientific opened a new ultra-cold facility in Europe to expand its clinical trial network in Europe to help accelerate the development of advanced therapies. The new facility was opened in Bleiswijk, Netherlands, to provide tailored, end-to-end support throughout the clinical supply chain for high-value therapies. |

| Company Name | Experic |

| Headquarters | Cranbury, New Jersey |

| Recent Development | In February 2024, Experic announced the launch of its new facility in Dublin, Ireland, to support global clinical trials. The new facility was opened to expand the company’s global footprint, increase the efficiency of its worldwide clinical trial supply services, and facilitate future growth. |

By Service

By Phase

By Therapeutic Area

By End-Use

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar