Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

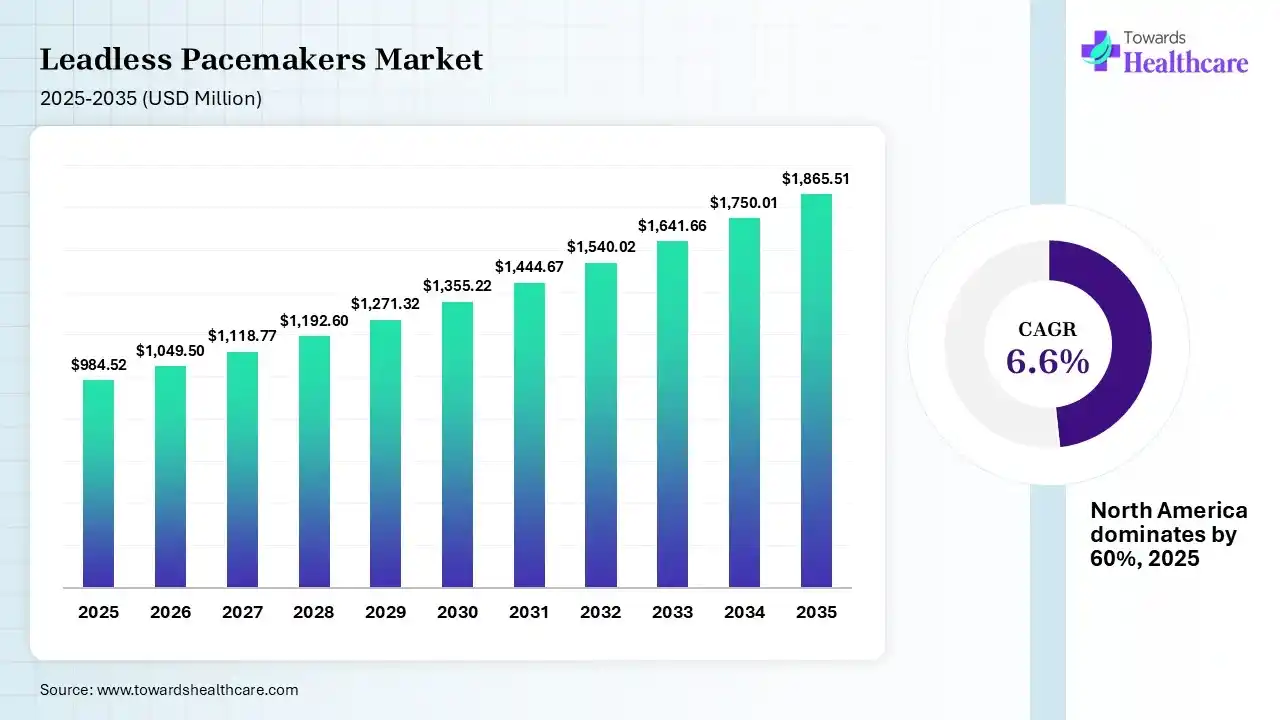

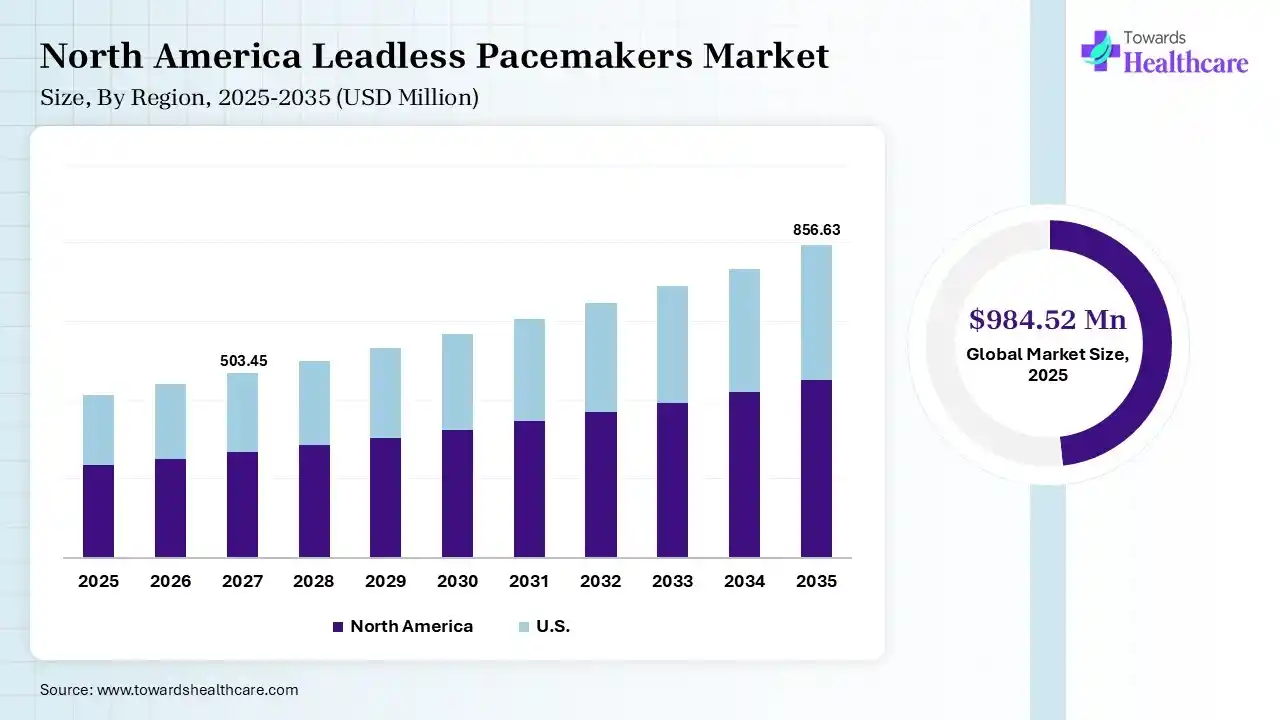

The global leadless pacemakers market size was estimated at USD 984.52 million in 2025 and is predicted to increase from USD 1049.5 million in 2026 to approximately USD 1865.51 million by 2035, expanding at a CAGR of 6.6% from 2026 to 2035.

")

The leadless pacemakers market is growing due to its increased frequency, improvements in the technologies, and the recognition of the considerable advantages over traditional transvenous tools.

The leadless pacemakers market is growing as it is a standard way to bypass these areas of weakness. Recent advancements in battery technology and deep miniaturisation of electronics provide the capability to implant the whole system into the right ventricle (RV). LPPM constitutes an outstanding substitute epicardial approach in case of particular comorbidities. These tools are implanted percutaneously via femoral venous access and offer self-contained, intracardiac single-chamber RV pacing. Leadless pacemakers are increasingly being considered for adults and children to manage congenital cardiac disease.

A leadless pacemaker is a miniaturized, self-contained cardiac pacing device implanted directly into the heart through minimally invasive catheter-based procedures, eliminating the need for traditional leads and surgical pockets. The leadless pacemakers market is growing due to increasing prevalence of cardiac arrhythmias, rising preferences for minimally invasive procedures, and expanding adoption of advanced cardiac rhythm management technologies. Technological advancements in miniaturization, MRI-compatible design, longer battery life, remote patient monitoring, and AI-enabled rhythm analysis are enhancing device safety and clinical outcomes. Emerging trends include next-generation dual-chamber leadless pacemakers, connected digital cardiology platforms, and personalized cardiac care solutions. Future opportunitites lie in expanding use across broader patient populations, improving long-term disease management, integrating predictive analytics, and advancing wireless cardiac technologies that enhance procedural efficiency, patient comfort, and overall cardiovascular care.

Integration of AI-driven technology in leadless pacemakers drives market growth, as artificial intelligence technology in pacemakers is transforming heart care, offering targeted treatment plans and real-time monitoring. This novelty is improving patient results and lowering the need for frequent medical interventions. Artificial intelligence (AI) techniques are increasingly being applied to enhance the management of these devices and the patients who rely on them. Recent developments demonstrate that machine learning (ML) and deep learning (DL) enhance diagnostic abilities, rationalize remote monitoring workflows, and optimise device-driven therapies. Artificial intelligence (AI) is altering the way pacemakers operate, enabling real-time adaptation to a patient's unique needs. AI-driven pacemakers help with remote monitoring, allowing physicians to access patient data via cloud-connected systems.

| Table | Scope |

| Market Size in 2026 | USD 1049.5 Million |

| Projected Market Size in 2035 | USD 1865.51 Million |

| CAGR (2026 - 2035) | 6.6% |

| Leading Region | North America by 60% |

| Key Applications | Bradycardia treatment, atrioventricular block management, cardiac rhythm management, dual-chamber pacing, cardiac resynchronization therapies |

| Primary End Users | Hospitals, Cardiac Centers, Electrophysiology Labs, Ambulatory Surgical Centers |

| Key Growth Drivers | Rising cardiovascular disease burden, preference for minimally invasive procedures, lower infection risks, technological advancements, growing elderly population |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Chambers, By Brands, By End Use, Regional Outlook |

| Top Key Players | Abbott, Medtronic, EBR Systems, Inc., Boston Scientific Corporation, MicroPort Scientific Corporation |

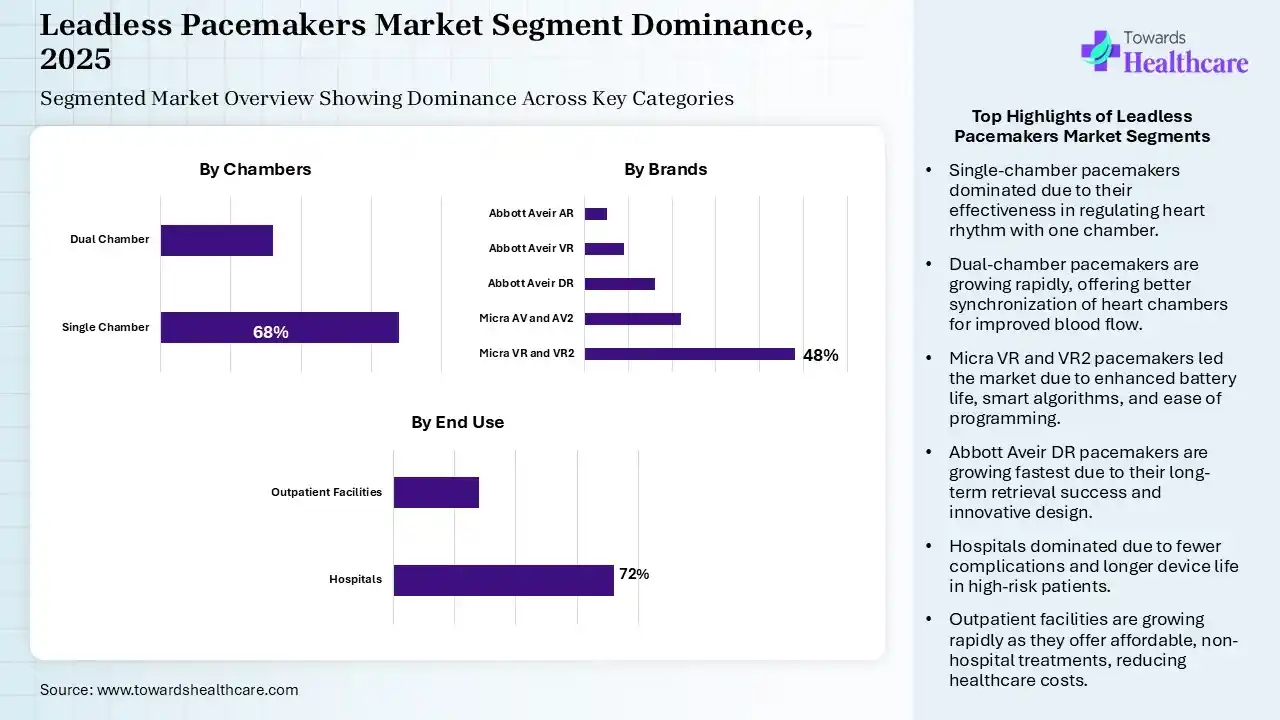

Which Chambers Segment Led the Leadless Pacemakers Market in 2025?

The single-chamber segment held the dominant market by 68% share in 2025, due to its use of a single wire that attaches to one chamber of the heart. Single-chamber atrial or ventricular stimulation has resulted in survival rates of 93% in the first year and 66% in the fifth year. This type of support regulates the heartbeat of one chamber, either the atrium or the ventricle, to continue a steady heart rhythm.

Dual Chamber

Whereas the dual chamber segment is the fastest-growing in the market, as this tool coordinates the upper and lower chambers of the heart, ensuring they beat in harmony for effective blood flow. A dual-chamber pacemaker is believed to allow more physiological pacing, largely attributable to the maintenance of AV synchrony. Dual-chamber pacemakers are often recommended for patients with more challenging heart rhythm disorders, as they offer better long-term results and enhanced quality of life.

Why did the Micra VR and VR2 Segment Dominate the Market in 2025?

The Micra VR and VR2 segment was dominant in the leadless pacemakers market by 48% share in 2025, as it offers enhanced battery longevity and smarter algorithms, and major patients only require one tool for life. It is easier to program than the previous Micra pacemakers. The Micra AV2 involves advanced algorithms that robotically program AV synchrony, therefore coordinating the heart’s upper and lower chambers.

Abbott Aveir DR

Whereas the Abbott Aveir DR segment is estimated to grow at the fastest CAGR during the forecast period, as AVEIR VR ventricular leadless pacemaker predecessor, has a long-term retrieval achievement rate of 88% with helix fixation through 9 years regardless of implant periods. Designed to support reducing the number of relocation attempts in the atrium and ventricle, AVEIR Leadless Pacemakers assess the Current of Injury through Commanded EGM.

Why did the Hospitals Segment Dominate the Market in 2025?

The hospitals segment was dominant in the leadless pacemakers market by 72% share in 2025, as leadless pacemakers significantly lower device-associated complications compared to traditional systems, particularly in elderly or high-risk patients. These tools are engineered for durability and generally last 10-15 years. Some hospitals have features that mechanically adjust pacing based on the patient’s movement level. Leadless pacemakers eliminate major complications related to transvenous pacemakers and leads, like pocket infections, hematoma, lead displacement, and lead fracture.

Outpatient Facilities

Whereas the outpatient facilities segment is the fastest-growing in the market, as outpatient care removes the requirement for hospital stays, it significantly reduces healthcare expenses. Major insurance plans cover outpatient solutions. Outpatient care is more affordable than inpatient solutions. Outpatient care enables patients to receive treatment for minor illnesses or wounds without the requirement for hospitalisation, therefore freeing up hospital resources for more pressing cases.

")

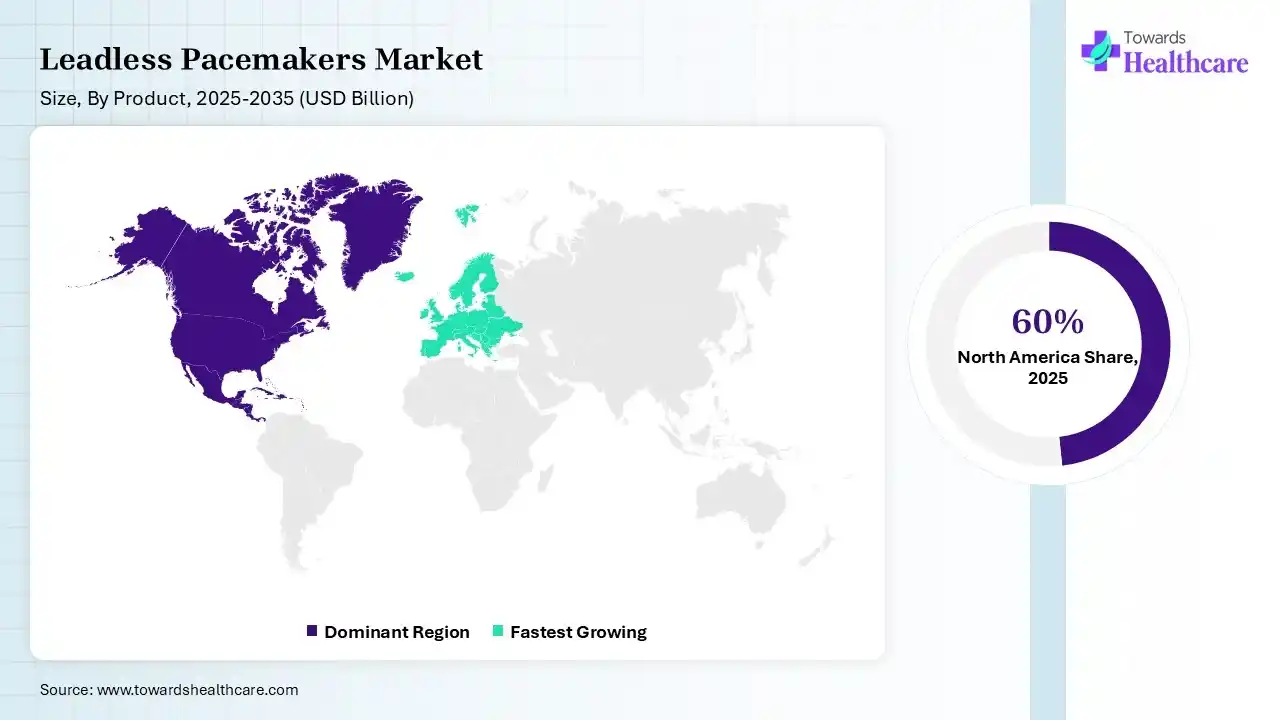

In 2025, North America dominated the leadless pacemakers market by 60% share because the medical care infrastructure in this region is a complex network of public and private healthcare settings, clinics, health centers, laboratories, pharmacies, and alternative solutions. It is supported by a highly specialized workforce and an array of healthcare technologies. Growing cardiovascular risk factors like diabetes, hypertension, obesity, cholesterol, and cigarette smoking remain predominant in adults, which increases the demand for leadless pacemakers, driving the growth of the market.

U.S. Market Trends

In the U.S., increasing cases of chronic diseases such as diabetes, stroke, heart disease, and cancer are among the major causes of mortality and morbidity in the United States. The technological innovation has played a significant role in the alteration of the medical care sector by offering tools that enhance the effectiveness of information management, treatments, and interaction between doctors and patients.

Canada Leadless Pacemakers Market Growth Through Advanced Cardiac Care

The Canada leadless pacemakers market is growing due to increasing prevalence of cardiac arrhythmias, rising demand for minimally invasive procedures, and expanding adoption of advanced cardiac rhythm management technologies. Strong healthcare infrastructure, favorable reimbursement policies, and growing investments in digital cardiology and remote patient monitoring are accelerating market growth. Continuous advancement in miniaturized, MRI-compatible, and long-lasting leadless pacemakers is further supporting widespread adoption.

Asia Pacific is expected to see rapid growth in the leadless pacemakers market, driven by rising technological advancements, which have improved the effectiveness of social support services, enabling health professionals to focus more on direct care and less on administrative tasks. The fast-aging population in the Asia-Pacific region has the strength to create severe health issues. Increased spending in neurosurgical ability and an early shift by payers to evaluate reimbursement, which contributes to the growth of the market.

India Market Trends

The development of leadless pacemakers in India has marked a decisive shift toward safer and smarter cardiac rhythm management. With increasing adoption in hospitals and better affordability of technology, this revolution is set to redefine the standard of care. With healthcare excellence, compassionate care, and transparent medical care delivery, India is creating the opportunity for a healthier future driven by technology and its access.

China Leadless Pacemakers Marekt Expands Through Cardiac Innovation

The China Leadless market is expanding due to the rising prevalence of cardiovascular disease, increasing adoption of minimally invasive cardiac procedures, and rapid modernization of healthcare infrastructure. Growing investments in cardiac care and strong government support for medical technology innovation are driving demand. Continuous advancement in miniaturized wireless and AI-enabled cardiac are further accelerating market growth.

Europe is increasing significantly in the leadless pacemakers market, as its massive population diversity, well-developed healthcare infrastructure, and stringent government standards offer an ideal ecosystem for the execution of clinical trials. Cardiovascular diseases (CVDs) are the major cause of disability and premature death in the European Region, causing over 42.5% of all deaths per year, which increases the demand for leadless pacemakers.

| Ecosystem Segment | Key Participants | Explanation |

| Technology Providers | Medtronic, Abbott, BIOTRONIK, EBR Systems | Develop leadless pacing technologies, communication systems, battery innovations, and catheter delivery platforms |

| Product Manufacturers | Medtronic, Abbott, EBR Systems, MicroPort, Lepu Medical | Design, manufacture, and commercialize leadless pacemakers and related devices |

| Service Providers | Mayo Clinic, Cleveland Clinic, Apollo Hospitals, NHS Cardiac Centers | Implantation, monitoring, and patient management services |

| Platform Providers | Abbott Merlin Platform, Medtronic CareLink | Remote monitoring and device management platforms |

| CROs/CDMOs | NAMSA, ICON plc, IQVIA, Charles River Laboratories | Clinical trials, regulatory support, device validation |

| Software Vendors | Medtronic, Abbott, GE HealthCare, Philips | Cardiac monitoring and device analytics software |

| Research Institutions | Mayo Clinic, Cleveland Clinic, Stanford University, Harvard Medical School | Clinical studies and technology validation |

| End-User Industries | Hospitals, Cardiac Specialty Centers, Ambulatory Surgery Centers | Primary users and purchasers of leadless pacemaker systems |

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 88% | 9% | 3% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medtronic | Galway | Ireland | Global market leader and pioneer in leadless pacing | Micra VR, Micra AV, Micra VR2, Micra AV2 |

| Abbott | Abbott Park, Illinois | USA | Second major commercial player with dual-chamber technology | AVEIR VR, AVEIR DR |

| Boston Scientific | Marlborough, Massachusetts | USA | Strong CRM portfolio and advanced leadless pacing pipeline | Empower Modular Pacing System |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| EBR Systems | Sunnyvale, California | USA | FDA-approved wireless leadless pacing for CRT applications | WiSE CRT System |

| Lepu Medical Technology | Beijing | China | Active cardiovascular implantable device developer | Leadless pacing R&D |

| LivaNova | London | United Kingdom | Cardiac rhythm management expertise and technology base | Cardiac pacing technologies |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| CAIRDAC | Paris | France | Developing autonomous leadless pacemaker technologies | Next-generation leadless pacemakers |

| Celtro GmbH | Munich | Germany | Focused on innovative pacing technologies | Leadless pacing development |

| Oscor | Palm Harbor, Florida | USA | Electrophysiology and pacing technology specialist | Cardiac rhythm management products |

In June 2026, “We designed LivIQ to address critical gaps in current leadless technologies: a single-device leadless solution that combines intuitive catheter handling with AV synchrony, particularly when an elevated heart rate and higher cardiac output is required,” said Dr. David Hayes, chief medical officer, Biotronik.

Strengths

Weaknesses

Opportunities

Threats

By Chambers

By Brands

By End Use

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar