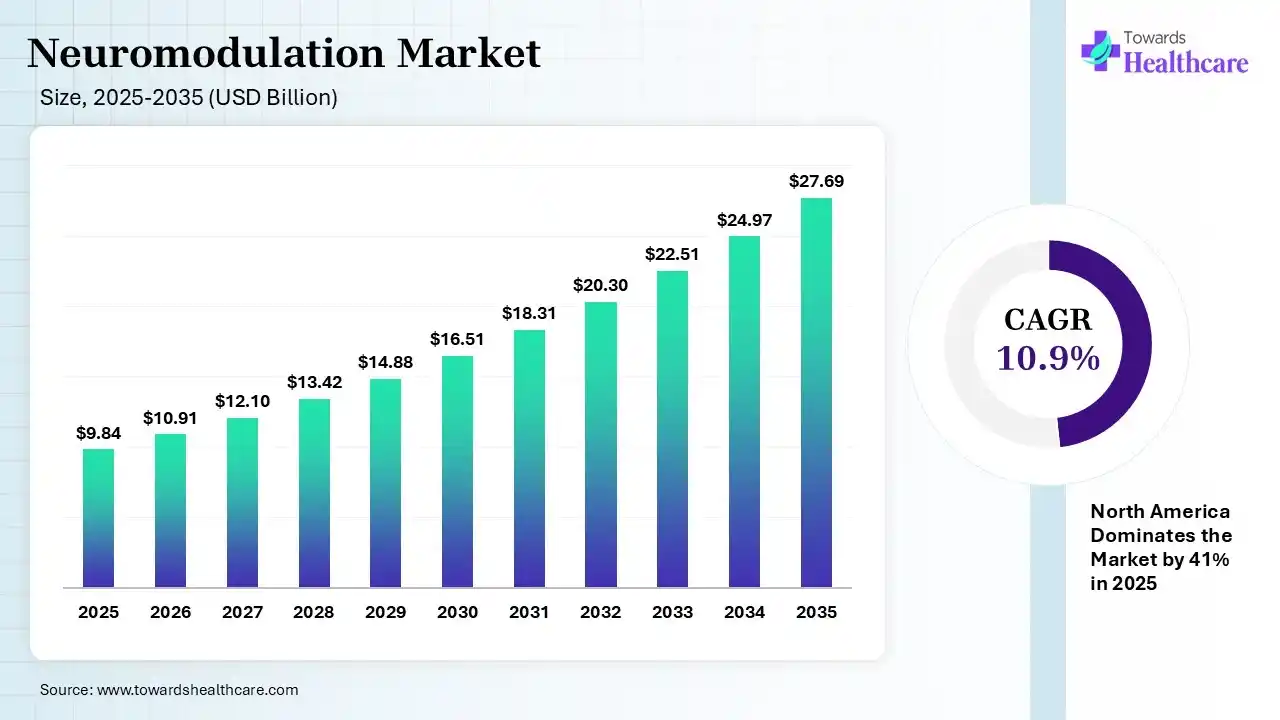

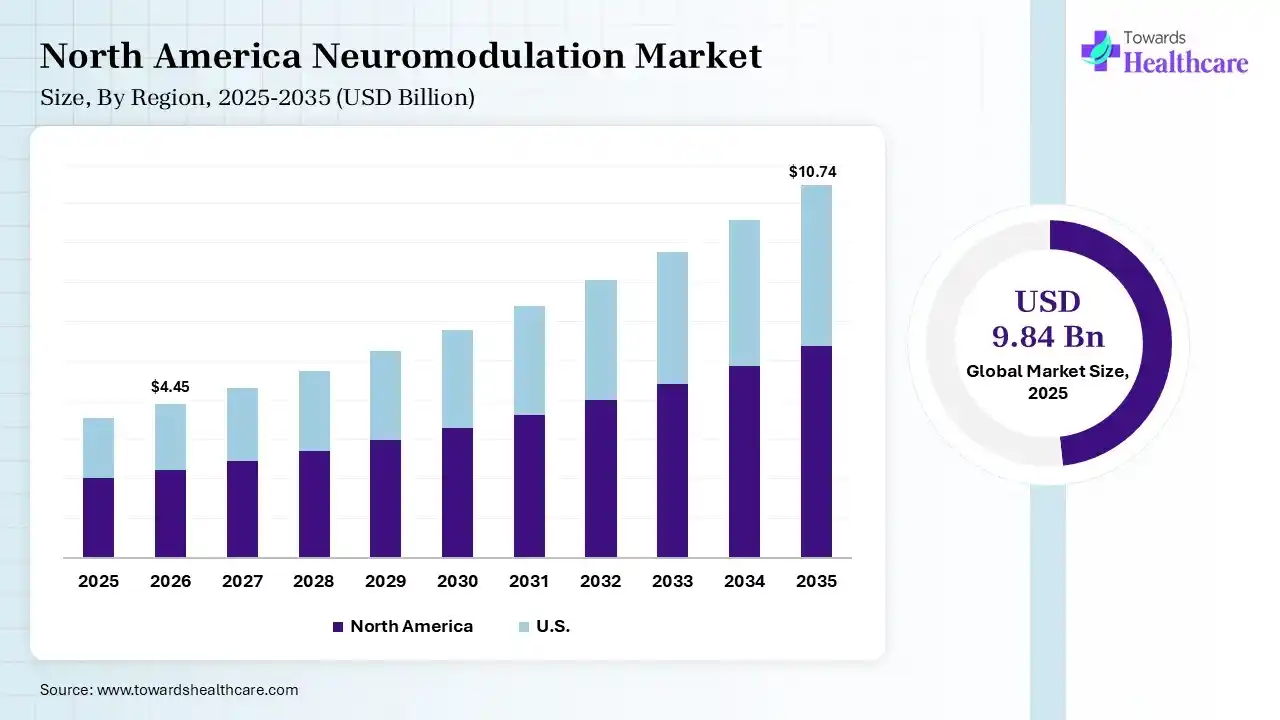

The global neuromodulation market size was estimated at USD 9.84 billion in 2025 and is predicted to increase from USD 10.91 billion in 2026 to approximately USD 27.69 billion by 2035, expanding at a CAGR of 10.9% from 2026 to 2035. The growing chronic disease burden globally is increasing the demand for neuromodulation solutions. A rise in the geriatric population, non-invasive approaches, technological advancements, and new product launches are also enhancing the market growth.

")

The neuromodulation market is driven by growing chronic neurological disorders and advancements in bioelectronic technology. The neuromodulation refers to medical techniques used to change or regulate nerve activity with the help of chemical, electrical, or magnetic stimulation. It is being used in the treatment of chronic pain, Parkinson’s disease, migraine, epilepsy, and depression.

AI plays an important role in the development of neuromodulation devices by providing adaptive learning systems, symptom monitoring, and remote programming support features. It also helps in adjusting stimulation parameters and predicts treatment response, offering personalized neuromodulation therapies. AI also helps in the identification of optimal stimulation sites, reducing overstimulation.

Expanding Applications

Expanding applications of neuromodulation devices beyond patient management is increasing their adoption rates. They are being used for the management of Alzheimer's, cognitive, and psychiatric disorders.

Growing Demand for Minimally Invasive Devices

A rise in the shift towards minimally or non-invasive devices is also driving the adoption of neuromodulation systems. This is increasing the development of transcranial magnetic stimulation (TMS) and transcutaneous electric nerve stimulation (TENS) devices.

Technological Advancements

Growing technological advancements are driving the development of next-generation neuromodulation systems. Closed-loop, miniaturized implants, rechargeable, and wireless devices are being developed by the companies.

| Table | Scope |

| Market Size in 2026 | USD 10.91 Billion |

| Projected Market Size in 2035 | USD 27.69 Billion |

| CAGR (2026 - 2035) | 10.9% |

| Leading Region | North America by 41% |

| Key Applications | Pain management, Parkinson’s disease, epilepsy, depression, essential tremor, urinary/fecal incontinence, sleep disorders, obesity management, hearing loss, and neurorehabilitation |

| Primary End Users | Hospitals, specialty clinics, ambulatory surgical centers, rehabilitation centers, homecare settings |

| Key Challenges | High device costs, complex implantation procedures, reimbursement limitations, regulatory requirements, and need for specialized clinical expertise |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By Technology, By Biomaterial, By End User, By Distribution Channel, By Region |

| Top Key Players | Medtronic plc, NeuroPace, Inc., Abbott Laboratories, Neuronetics, Inc., Boston Scientific Corporation, LivaNova PLC, Inspire Medical Systems, Inc., Nevro Corp, LivaNova/Cyberonics, Saluda Medical Pty Ltd. |

")

| Segment | Share 2025 (%) |

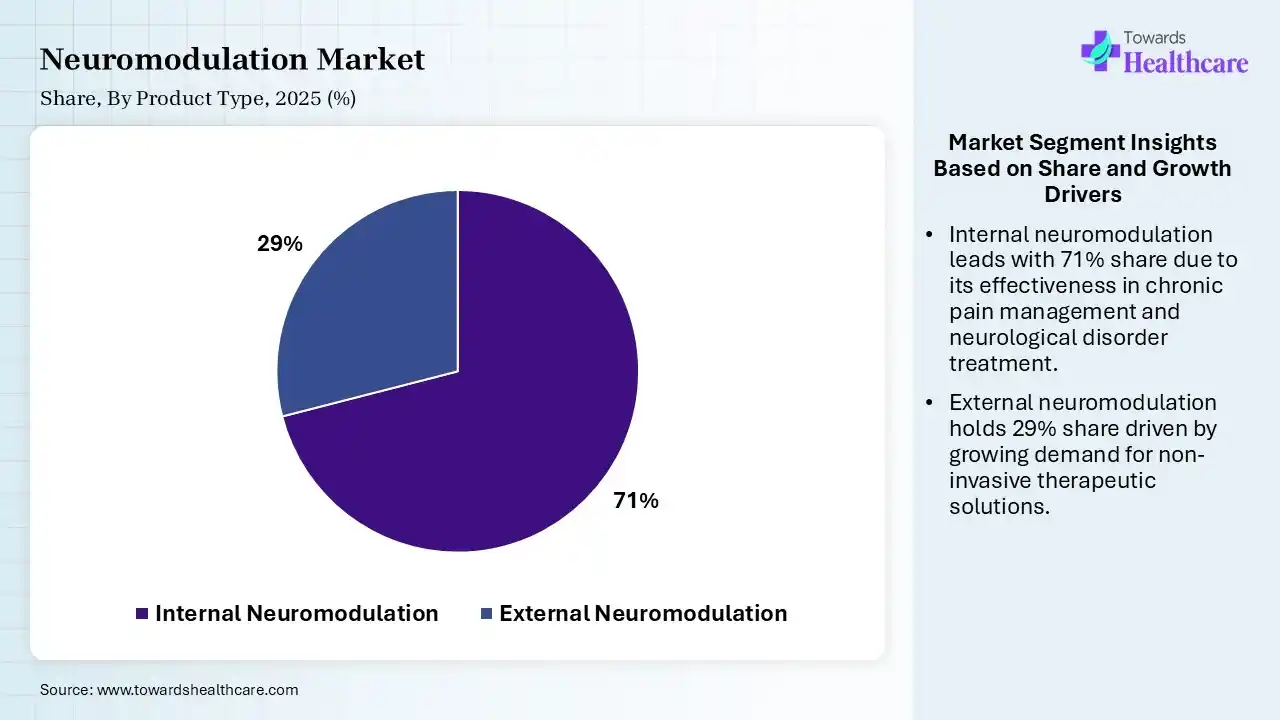

| Internal Neuromodulation | 71% |

| External Neuromodulation | 29% |

The Internal Neuromodulation Segment Dominated the Market With 71% in 2025

The internal neuromodulation segment led the neuromodulation market with 71% share in 2025, due to growth in the implantation procedures for chronic pain and Parkinson’s disease, which continued to expand procedural volumes. Technological advancements in rechargeable implants have also improved patient compliance and long-term therapy outcomes. Favorable reimbursement frameworks in developed countries also accelerated their adoption.

The external neuromodulation segment held the second-largest share of 29% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 12.10% during the forecast period, due to growing preference for non-invasive therapies, which increases demand for wearable and outpatient neuromodulation systems. Expanding mental health treatment applications also support TMS adoption globally. Consumer-focused home-use devices also improve their accessibility and affordability.

")

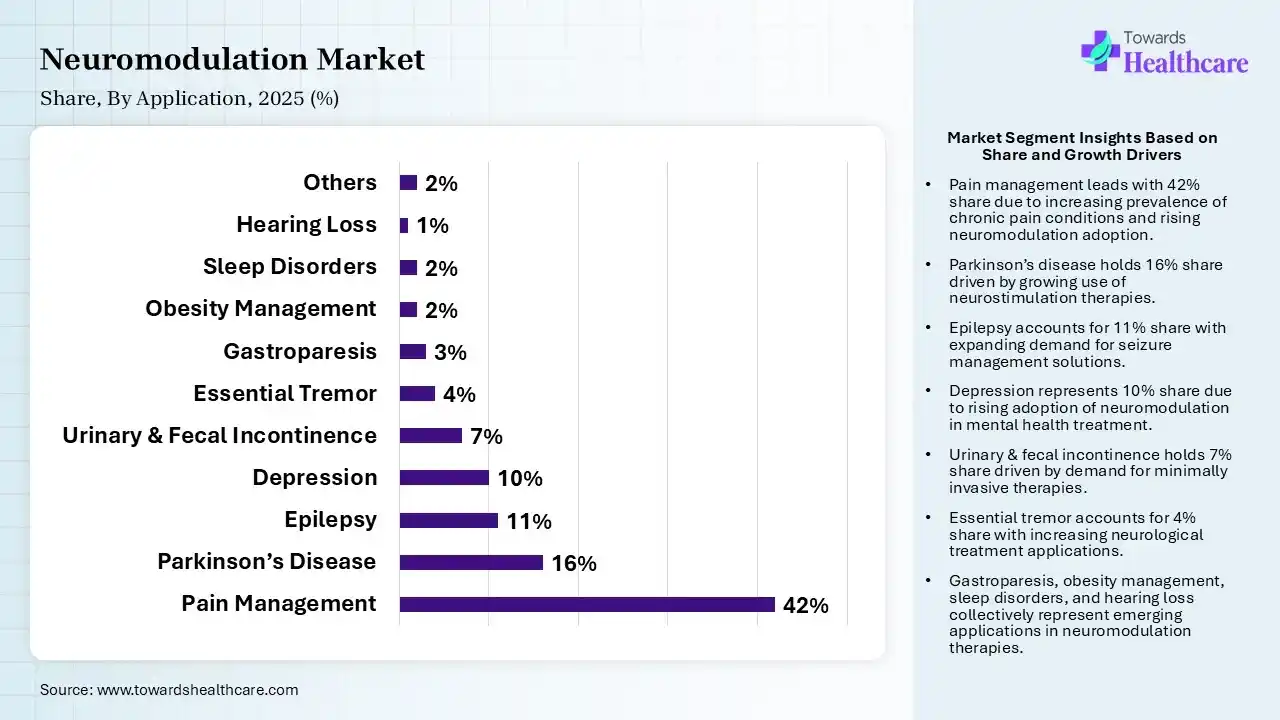

| Segment | Share 2025 (%) |

| Pain Management | 42% |

| Parkinson’s Disease | 16% |

| Epilepsy | 11% |

| Depression | 10% |

| Urinary & Fecal Incontinence | 7% |

| Essential Tremor | 4% |

| Gastroparesis | 3% |

| Obesity Management | 2% |

| Sleep Disorders | 2% |

| Hearing Loss | 1% |

| Others | 2% |

The Pain Management Segment Dominated the Market With 42% in 2025

The pain management segment accounted for the highest revenue share of 42% of the neuromodulation market in 2025, driven by growth in the chronic pain burden, which increased neuromodulation procedure volumes worldwide. Shift towards opioid alternatives among physicians and regulators also increased the use of neuromodulation. Their technological innovations also improved long-term pain control effectiveness.

The Parkinson’s disease segment held the second-largest share of 16% of the market in 2025, due to aging populations contributing to rising neurodegenerative disease prevalence globally. DBS advancements improve motor symptom management outcomes, promoting the use of neurostimulation devices. Neurology centers are also increasingly integrating advanced stimulation therapies.

The epilepsy segment held 11% of the neuromodulation market share in 2025, due to increasing refractory epilepsy incidence, which supports VNS and DBS adoption growth. Improved diagnostic capabilities enable earlier intervention strategies, increasing their use. Expanding pediatric neuromodulation applications also continue their adoption rates.

The depression segment held 10% of the market share in 2025 and is expected to show the highest growth during the forecast period, due to escalating mental health disorders, which boost TMS therapy demand globally. Growing drug-resistant depression cases also encourage alternative therapeutic adoption. Expanding insurance reimbursement also improves treatment accessibility.

")

| Segments | Share 2025 (%) |

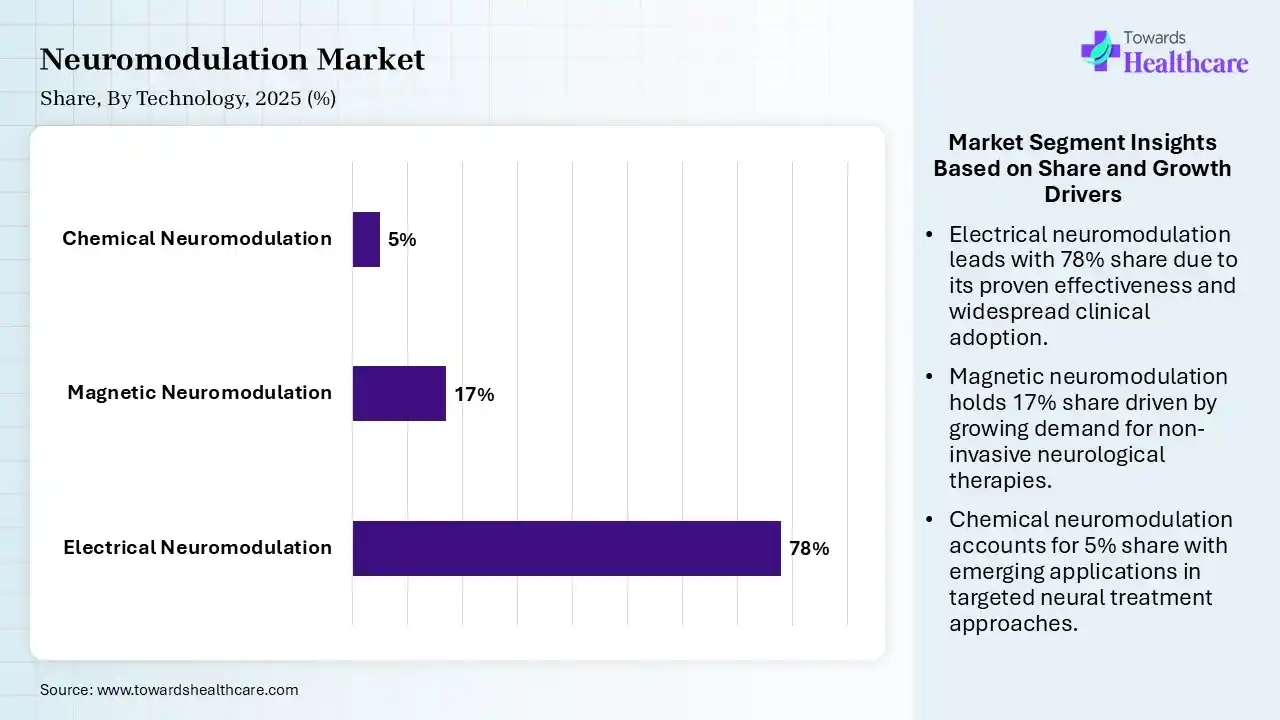

| Electrical Neuromodulation | 78% |

| Magnetic Neuromodulation | 17% |

| Chemical Neuromodulation | 5% |

The Electrical Neuromodulation Segment Dominated the Market With 78% in 2025

The electrical neuromodulation segment held a major revenue share of 78% of the neuromodulation market in 2025, due to its broad clinical applicability across pain, movement, and psychiatric disorders. Implantable stimulation systems also remained the standard therapeutic modality. Continuous technological upgrades also improved therapy precision and battery life.

The magnetic neuromodulation segment held the second-largest share of 17% of the market in 2025 and is expected to expand rapidly during the forecast period, due to the rising TMS utilization for depression treatment, which significantly expands market demand. Their non-invasive procedures also improve patient acceptance and outpatient treatment rates. Clinical approvals for new neurological indications also support rapid expansion.

The chemical neuromodulation segment held 5% of the neuromodulation market share in 2025, driven by increasing research into neurotransmitter-based modulation. Their combination therapies also improve treatment effectiveness in complex neurological disorders. Pharmaceutical-device integration is also expanding future innovation opportunities.

")

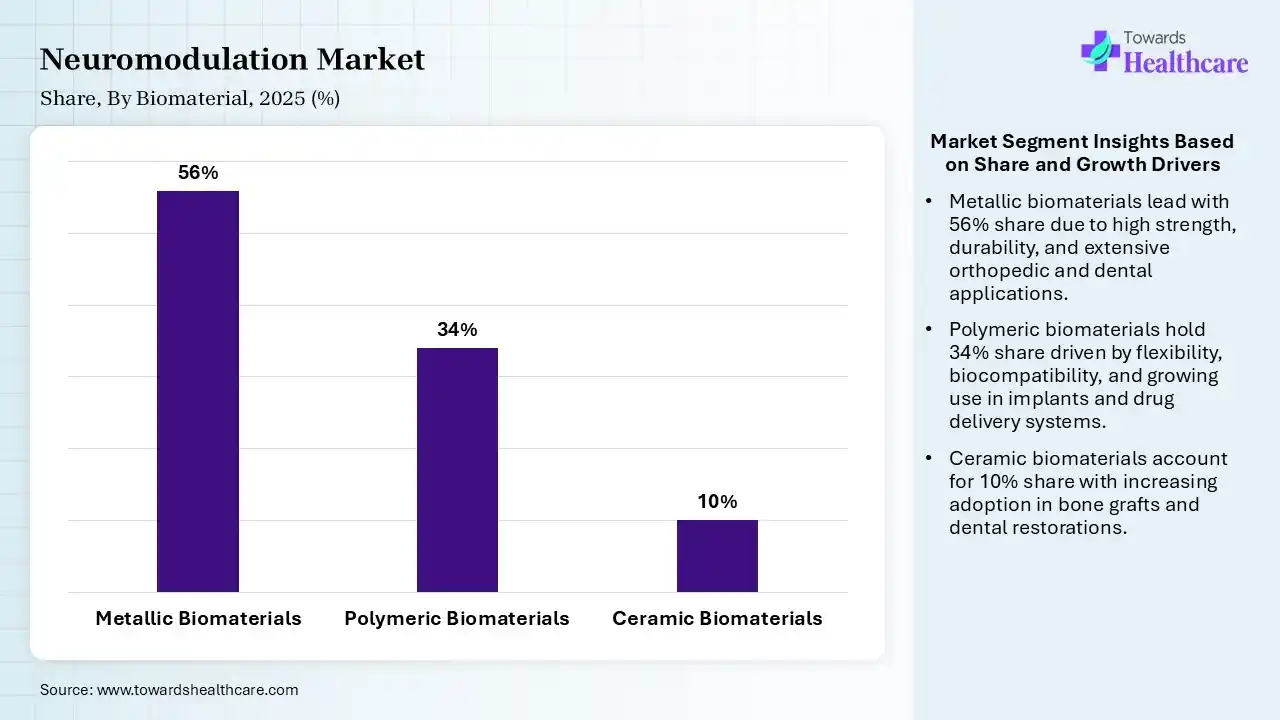

| Segment | Share 2025 (%) |

| Metallic Biomaterials | 56% |

| Polymeric Biomaterials | 34% |

| Ceramic Biomaterials | 10% |

The Metallic Biomaterials Segment Dominated the Market With 56% in 2025

The metallic biomaterials segment contributed the biggest revenue share of 56% of the neuromodulation market in 2025, driven by high durability and conductivity, which made metals essential for implantable electrodes. Titanium-based implants also improved long-term device reliability. Strong biocompatibility also supported extensive clinical utilization.

The polymeric biomaterials segment held the second-largest share of 34% of the market in 2025 and is expected to gain the highest share with a CAGR of 12.30% during the forecast period, due to the use of flexible polymeric materials that enhance patient comfort and implant adaptability. Advances in bioresorbable polymers also support next-generation device development. Miniaturized wearable devices increasingly rely on polymer components, promoting their adoption.

The ceramic biomaterials segment held 10% of the neuromodulation market share in 2025, due to superior insulation properties that improve device safety and electrical performance. Increasing use in high-precision implants also supports stable demand. Growing research into advanced ceramics is also enhancing biocompatibility improvements.

")

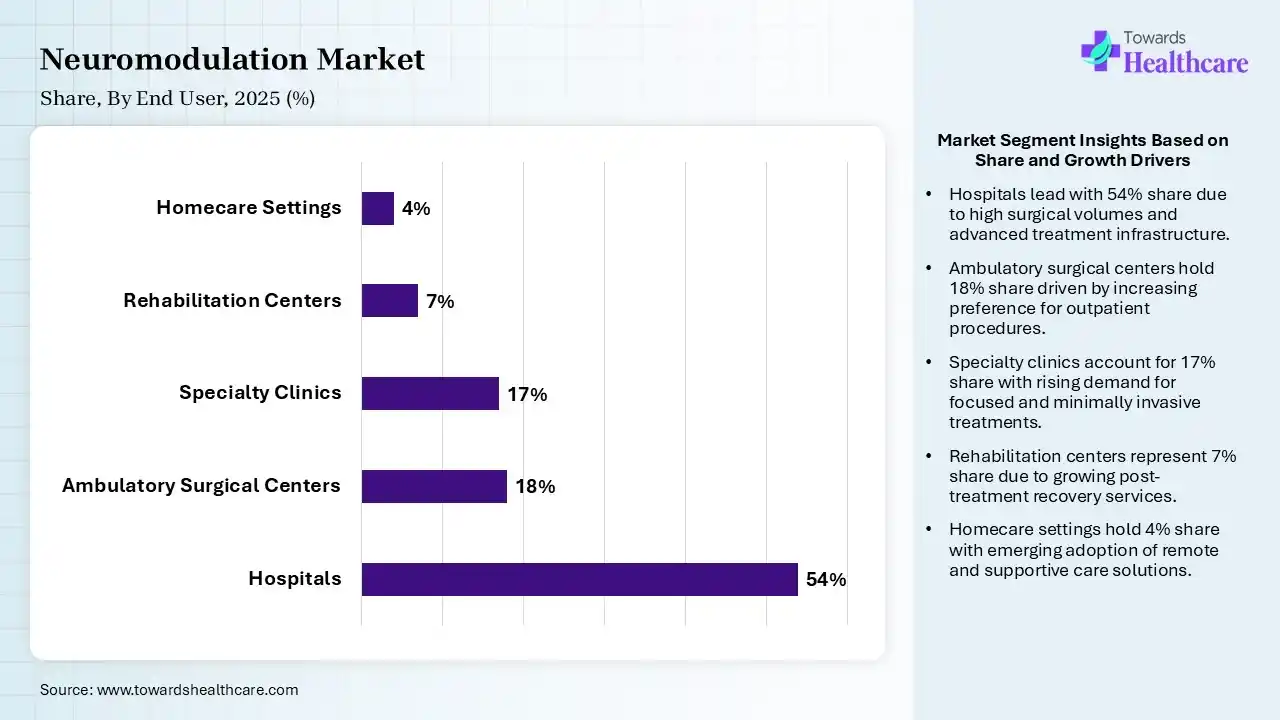

| Segment | Share 2025 (%) |

| Hospitals | 54% |

| Ambulatory Surgical Centers | 18% |

| Specialty Clinics | 17% |

| Rehabilitation Centers | 7% |

| Homecare Settings | 4% |

The Hospitals Segment Dominated the Market With 54% in 2025

The hospitals segment held the largest revenue share of 54% of the neuromodulation market in 2025, due to large surgical infrastructure, which supported high neuromodulation implantation volumes globally. Availability of multidisciplinary specialists also improved treatment adoption. Their continuous investment in advanced neurotechnology platforms also contributed to their growth.

The ambulatory surgical centers segment held the second-largest share of 18% of the market in 2025, due to growing preference for outpatient procedures. Cost-effective surgical settings are also attracting patients and healthcare providers. Minimally invasive implantation technologies also support procedural expansion.

The specialty clinics segment held 17% of the neuromodulation market share in 2025 and is expected to grow with the fastest CAGR of 12.80% during the forecast period, due to the rising demand for focused neurological and psychiatric care, which boosts specialty clinic growth. Growing demand for TMS and pain management therapies is also increasing the shift toward outpatient clinics. Their personalized treatment models are also enhancing patient retention.

The rehabilitation centers segment held 7% of the market share in 2025, due to increasing neurorehabilitation programs supporting neuromodulation integration. Stroke and spinal injury recovery applications also continue their expansion. Advanced stimulation therapies also improve functional rehabilitation outcomes.

")

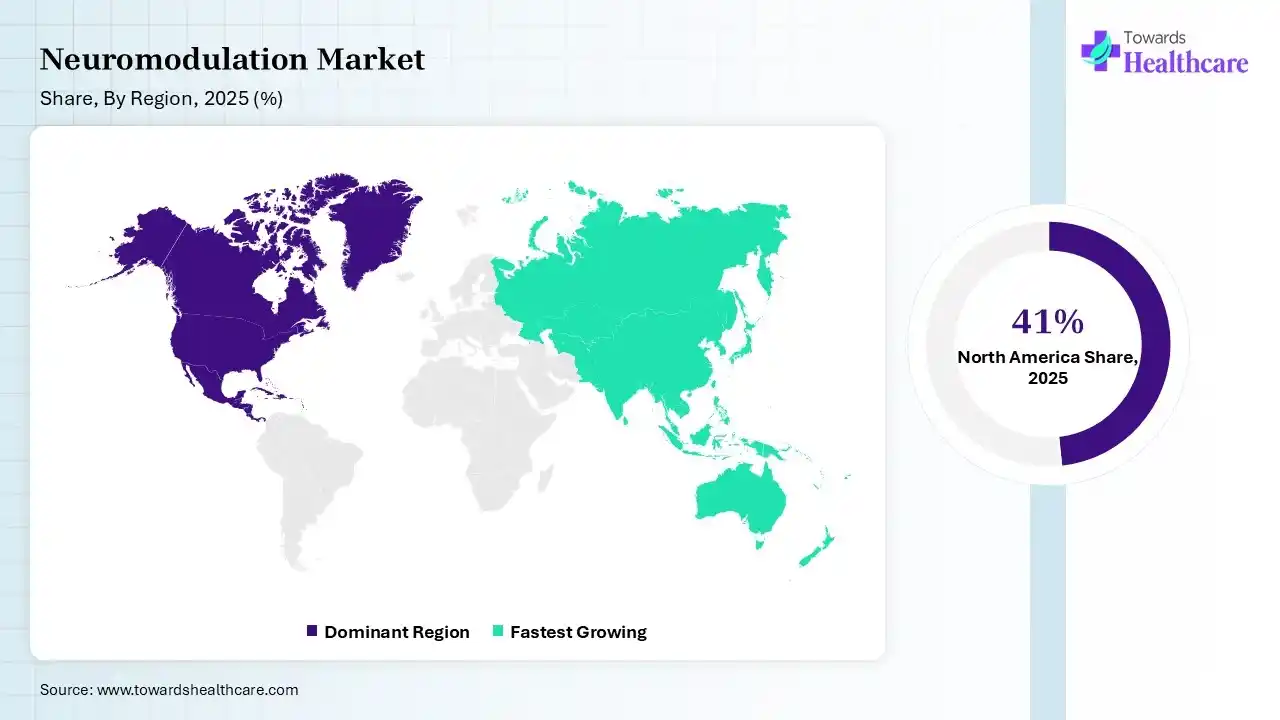

North America dominated the neuromodulation market with 41% in 2025, due to strong reimbursement systems and advanced healthcare infrastructure, which supported high procedural volumes. The presence of major neuromodulation manufacturers also accelerated their innovation adoption. Growth in the prevalence of neurological disorders also sustained the market demand.

U.S. Market Trends

Extensive FDA approvals and high healthcare spending in the U.S. are supporting the market leadership. A strong clinical research ecosystem also accelerates technology commercialization. Increasing chronic pain prevalence also drives implantation procedures.

Asia Pacific held 21% share of the market in 2025 and is expected to grow at the fastest CAGR during the forecast period, due to rapid healthcare infrastructure development, which significantly expands neuromodulation accessibility. A large patient population also drives long-term market potential. Rising investments in neurotechnology research also accelerate commercialization, which enhances the market growth.

India Market Trends

Rising healthcare investments and expanding private hospital networks in India are driving neuromodulation growth. Increasing awareness of neurological treatment options is also supporting their adoption. Growing medical tourism strengthens procedural demand, increasing its use.

| Ecosystem Category | Market Participants / Explanation |

| Technology Providers | Companies developing stimulation technologies including deep brain stimulation (DBS), spinal cord stimulation (SCS), vagus nerve stimulation (VNS), transcranial magnetic stimulation (TMS), and closed-loop systems. |

| Product Manufacturers | Medical device companies manufacturing implantable and non-invasive neuromodulation systems for neurological and pain-related conditions. |

| Service Providers | Clinical service providers, specialty neurology centers, rehabilitation providers, and healthcare organizations delivering neuromodulation therapies. |

| Platform Providers | Companies developing digital monitoring, remote programming, AI-assisted therapy optimization, and adaptive stimulation platforms. |

| CROs / Clinical Research Providers | Organizations supporting clinical trials, regulatory studies, and device validation for neuromodulation technologies. |

| Software Vendors | AI, analytics, and digital health companies supporting personalized stimulation algorithms, patient monitoring, and remote care solutions. |

| Research Institutions | Universities and neuroscience research organizations advancing brain-computer interfaces, neurostimulation, and neural engineering. |

| End-User Industries | Hospitals, neurological clinics, pain management centers, psychiatric care providers, and healthcare systems. |

R&D

Clinical Trials and Regulatory Approvals

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 72% | 21% | 7% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medtronic plc | Dublin, Ireland | Ireland | One of the largest global neuromodulation players with extensive implantable neurostimulation portfolio and global clinical adoption. | Deep Brain Stimulation (DBS), Spinal Cord Stimulation (SCS), Vagus Nerve Stimulation, InterStim systems |

| Abbott Laboratories | Abbott Park, Illinois, United States | USA | Major medical device company with strong presence in neuromodulation through pain management and DBS technologies. | Eterna SCS System, Infinity DBS System, Proclaim XR SCS |

| Boston Scientific Corporation | Marlborough, Massachusetts, United States | USA | Global leader in implantable neuromodulation devices with strong market penetration in pain therapy and neurological care. | WaveWriter Alpha SCS, Vercise DBS systems, spinal cord stimulation solutions |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| NeuroPace, Inc. | Mountain View, California, United States | USA | Specialized epilepsy-focused neuromodulation company with FDA-approved responsive stimulation technology. | RNS System for drug-resistant epilepsy |

| Neuronetics, Inc. | Malvern, Pennsylvania, United States | USA | Leading non-invasive neuromodulation company focused on psychiatric applications. | NeuroStar Advanced Therapy TMS System |

| Inspire Medical Systems, Inc. | Golden Valley, Minnesota, United States | USA | Major player in implantable stimulation technology for sleep apnea management. | Inspire Upper Airway Stimulation therapy |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Nalu Medical, Inc. | Carlsbad, California, United States | USA | Emerging neuromodulation company focused on minimally invasive implantable pain therapy solutions. | Nalu Neurostimulation System |

| BioElectronics Corporation | Frederick, Maryland, United States | USA | Develops wearable microcurrent neuromodulation products for pain management applications. | ActiPatch and wearable neuromodulation devices |

| Magnus Medical, Inc. | San Francisco, California, United States | USA | Emerging company developing next-generation TMS technologies for psychiatric disorders. | SAINT neuromodulation system for depression |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Application

By Technology

By Biomaterial

By End User

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar