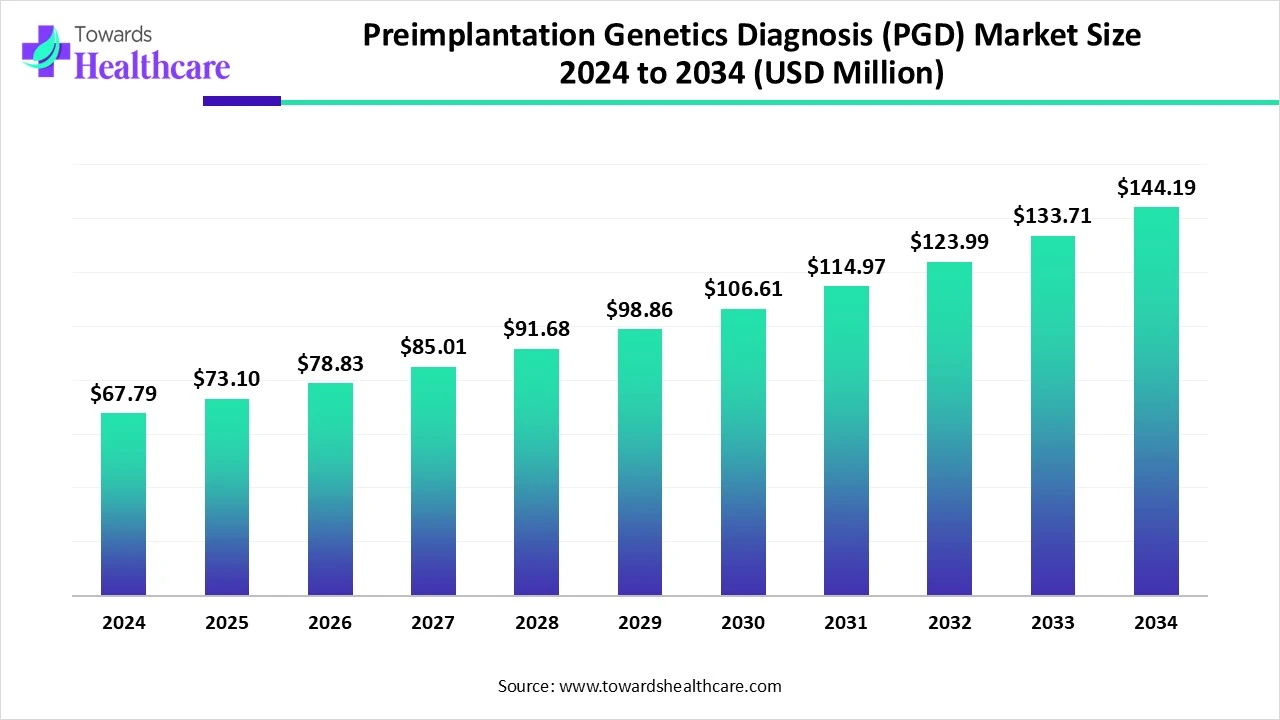

The global preimplantation genetics diagnosis (PGD) market size is calculated at US$ 67.79 Million in 2024, grew to US$ 73.1 million in 2025, and is projected to reach around US$ 144.19 million by 2034. The market is expanding at a CAGR of 7.84% between 2025 and 2034.

Market Trends and Growth (2025)")

The demand for PGD is increasing globally due to growing cases of infertility. The growing awareness and demands for non-invasive testing are also increasing their adoption rates. AI is also being used to enhance its accuracy, speed, quality, and applications. Additionally, the presence of the advanced healthcare sector, growing IVF procedures, and increasing genetic disorders are also increasing their utilization in various regions. Moreover, the companies are launching or adopting these platforms. Thus, all these developments are promoting the market growth.

| Table | Scope |

| Market Size in 2025 | USD 73.1 Million |

| Projected Market Size in 2034 | USD 144.19 Million |

| CAGR (2025 - 2034) | 7.84% |

| Leading Region | North America |

| Market Segmentation | By Clinical Purpose/Test Indication, By Biopsy Stage/Sample Type, By Testing Technology/Laboratory Method, By Service Model/Delivery, By End-User/Buyer Type, By Region |

| Top Key Players | IGENOMIX, Natera/PGT solutions, CooperSurgical/Reprogenetics, BGI/BGI Genomics, Invitae, Genea Biomedx, Illumina, Thermo Fisher Scientific, Agilent Technologies, PerkinElmer, MGI/Complete Genomics, Sage Labs/CooperGenomics, Academic/clinic networks offering high-volume in-house PGT, Specialized niche providers of niPGT and embryo analytics, Consumables & biopsy instrument suppliers |

The preimplantation genetics diagnosis (PGD) market encompasses in-vitro fertilization (IVF)-linked genetic testing performed before embryo transfer to detect chromosomal (aneuploidy, structural) abnormalities and single-gene disorders. It involves the preimplantation genetic testing for aneuploidy (PGT-A), monogenic/single-gene (PGT-M) and structural rearrangements (PGT-SR), plus associated biopsy workflows (polar body, cleavage-stage, trophectoderm), laboratory testing methods (NGS, aCGH, PCR/SNP), counselling, cryopreservation and reporting services used by IVF clinics, reference labs and public-health programs.

The use of AI in the preimplantation genetics diagnosis (PGD) market is increasing to enhance its accuracy as well as to evaluate the quality of the embryo. AI models are also being used to predict the viability of the embryo to promote successful implantation. It also helps in detecting the mutations, mosaicism, and chromosomal abnormalities, which in turn reduces the chances of errors. The PGT results are also rapidly interpreted with the use of AI. At the same time, it also helps in detecting the patient's data and predicting the appropriate time for embryo transfer.

Growing Awareness

There is a growth in awareness about genetic disorders and infertility. This, in turn, is increasing the demand for PGD. These are being used to reduce the risk of passing the genetic diseases to their children. It also helps in reducing the chances of miscarriages, ensuring healthy embryos. At the same time, various programs and campaigns are also being conducted to enhance its use to tackle the growing genetic diseases and infertility. Thus, this is driving the preimplantation genetics diagnosis (PGD) market growth.

High Cost

The cost of PGD is high. At the same time, the IVF procedures are also expensive. Moreover, the lack of insurance policies also makes them costly. Thus, this increases the total treatment cost. Additionally, this limits the use and adoption of PGD.

Growing IVF Usage

Due to increasing IVF usage, there is a rise in the use of PGD to decrease the infertility cases. They help in enhancing the pregnancy success rates by selecting the genetically normal embryo. This, in turn, minimizes the rates of miscarriages. They also help in minimizing chromosomal abnormalities during delayed pregnancies with the use of PGT-A. At the same time, different types of innovations are also being made to enhance its accuracy and speed. Thus, this is promoting the preimplantation genetics diagnosis (PGD) market growth.

For instance,

By clinical purpose/test indication type, the PGT-A segment held the largest share of the preimplantation genetics diagnosis (PGD) market in 2024, due to elective aneuploidy screening. This, in turn, helped in minimizing the risk of miscarriages. Moreover, it also helps in detecting chromosomal abnormalities, increasing the pregnancy success rates.

By clinical purpose/test indication type, the PGT-M segment is expected to show the highest growth during the predicted time. The growing carrier screening and family planning is increasing its demand. Additionally, the growing fertility disorders is also increasing their use. Moreover, their growing awareness is also contributing to the same.

By biopsy stage/sample type, the trophectoderm (TE) biopsy of blastocyst segment led the preimplantation genetics diagnosis (PGD) market in 2024, as they provided DNA for testing, which enhanced the accuracy of the test. This decreased the misdiagnosis, which increased its use in various clinics. Thus, this enhanced the market growth.

By biopsy stage/sample type, the non-invasive embryo testing segment is expected to show the highest growth during the upcoming years. They help in maintaining the viability of the embryo, which makes them a safer alternative. This is increasing their adoption rates. Additionally, the growing research and development are also increasing their use.

By testing technology/laboratory method type, the next-generation sequencing (NGS)-based workflows segment held the dominating share of the preimplantation genetics diagnosis (PGD) market in 2024, due to its high sensitivity and accuracy. It also enhanced the efficiency due to its high throughput and resolution. Moreover, its affordability also enhanced its use.

By testing technology/laboratory method type, the digital PCR & droplet-based assays segment is expected to show the fastest growth rate during the predicted time. They provided low-pass WGS with improved bioinformatics and digital/ultra-sensitive PCR for mosaics. Additionally, they are able to detect any abnormalities or mutations due to their high sensitivity.

By service model/delivery type, the centralized/reference genetic testing labs segment held the largest share of the preimplantation genetics diagnosis (PGD) market in 2024, driven by their high volume of testing. They also provided prise results under strict quality control. Moreover, different types of PGDs were also used for testing.

By service model/delivery type, the hybrid networks segment is expected to show the highest growth during the forthcoming years. They help in offering accurate and fast testing services. They also consist of advanced technologies, which are attracting the population. Moreover, their digital platforms are enhancing their accessibility and reliability.

By end user/buyer type, the private IVF clinics & hospital fertility centers segment led the global preimplantation genetics diagnosis (PGD) market in 2024, due to growing patient demands for PGD. They are also preferring a large volume of IVF cycles, which has increased its use. They were also used to provide personalized treatment plans.

By end user/buyer type, the consumers/patients segment is expected to show the fastest growth rate during the upcoming years. Due to growing personalized fertility treatment plans, their use by patients is increasing. The growing at-home testing is also contributing to the same. Similarly, the growing fertility awareness is also increasing their use.

North America dominated the preimplantation genetics diagnosis (PGD) market in 2024. North America consisted of well-developed fertility clinics, which increased the use of PGD during the IVF cycles. The presence of advanced technologies also increased their accuracy, increasing their use. Thus, this contributed to the market growth.

A large volume of IVF procedures is conducted in the U.S., which is increasing the use and adoption of PGD. They are also increasing the use of non-invasive embryo testing and digital PCR platforms. The companies are also increasing their innovations. Moreover, the growing awareness is also increasing their adoption rates.

There is a rise in the adoption of PGD in Canada due to growing IVF procedures. They are also being supported by the government. At the same time, funding is also provided to promote their development and adoption. Additionally, the fertility clinics are also increasingly utilizing such advanced platforms.

Asia Pacific is expected to host the fastest-growing preimplantation genetics diagnosis (PGD) market during the forecast period. Asia Pacific is experiencing a rise in infertility cases, which is increasing the use of IVF procedures and growing the demand for PGD. The advancing fertility clinics are also increasing their adoption along with their new innovations. Additionally, the growing awareness is also increasing their demand to avoid hereditary diseases. Thus, all these factors, along with government support, are promoting the market growth.

To enhance the diagnostic accuracy and clinical outcomes, the R&D of preimplantation genetics diagnosis (PGD) is focusing on developing high-resolution genetic analysis techniques, such as less invasive embryo biopsy methods and next-generation sequencing.

Key Players: Thermo Fisher Scientific, Illumina, Revvity, Agilent Technologies, The Cooper Companies Inc.

The clinical trials of preimplantation genetics diagnosis (PGD) include the development of best practices and clinical utility, while the regulatory approval focuses on its quality assurance.

Key Players: Thermo Fisher Scientific, Illumina, Agilent Technologies, Roche, PerkinElmer.

The prevention of mixups and preservation of the samples is included in the packaging and serialization of the preimplantation genetics diagnosis (PGD).

Key Players: Abdos Labtech Private Limited, Thermo Fisher Scientific, Cole-Parmer, World Courier.

The preimplantation genetics diagnosis (PGD) distribution to hospitals includes the transportation of embryonic cells from fertility clinics to genetic testing facilities.

Key Players: Natera, MedGenome, IGENOMIX, World Courier.

The psychological and specialized genetic counselling is offered to the couples to navigate ethical dilemmas, understand complex results, and cope with the significant emotional stress of testing and IVF procedures, in the patient support and services of the preimplantation genetic diagnosis (PGD).

Key Players: NovaIVF Fertility, Apollo Fertility, Cloudnine Fertility, Birla Fertility and IVF, Indira IVF, Carrot Fertility, FertileThoughts.

Market Top Key Players")

In June 2025, the Founder and CEO of Juniper Genomics, Jeremy Grushcow, stated that there is a growth in the questions arising from patients as the IVF journey can be emotionally exhausting, expensive, and low success rate for embryo testing. Most failures are because of the embryos that are not viable. Therefore, they focus on providing the families the compassionate, clear, and responsible care at every step by combining cutting-edge science with rigorous ethical standards by collaborating with IVF clinicians.

By Clinical Purpose/Test Indication

By Biopsy Stage/Sample Type

By Testing Technology/Laboratory Method

By Service Model/Delivery

By End-User/Buyer Type

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar