Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

The seasonal vaccines market is rapidly advancing on a scale, with expectations of accumulating hundreds of millions in revenue between 2025 and 2034. Market forecasts suggest robust development fueled by increased investments, innovation, and rising demand across various industries.

The growing diseases, geriatric population, and awareness are increasing the demand for seasonal vaccines. To advance their development and to enhance their safety and effectiveness, the use of AI is increasing. Moreover, the growing innovations and expanding healthcare are increasing the use of these vaccines across various regions, where companies are developing and launching their new seasonal vaccines, promoting the market growth.

The seasonal vaccines market is driven by annual influenza vaccines due to increased public health awareness, ongoing technological advancements, and government immunization programs. The seasonal vaccines include vaccines developed and administered periodically to protect against pathogens exhibiting annual or cyclical prevalence patterns. Major examples include influenza, respiratory syncytial virus (RSV), and other viral or bacterial agents showing seasonality in infection rates. Seasonal vaccines encompass both monovalent and multivalent formulations across inactivated, live-attenuated, recombinant, and mRNA platforms.

Various opportunities promoting their development and optimization strategies for seasonal vaccines are being provided by AI. It also helps in antigen selection, adjuvant identification, and epitope prediction, where the AI algorithms are being combined with protein structures, immune system interactions, and genomic data to assess immunogenicity, predict antigenic epitopes, and prioritize antigens for experimentation. It also helps in enhancing the safety and efficacy profiles of the vaccines, and improving vaccine design precision and scalability by integrating with synthetic biology and single-cell omics.

In August 2025, VaxSeer, an AI system identifying the most protective vaccine candidates and predicting dominant flu strains, was developed by the collaboration between MIT’s Computer Science and Artificial Intelligence Laboratory (CSAIL) and the MIT Abdul Latif Jameel Clinic for Machine Learning in Health.

By vaccine type, the influenza vaccines segment held the dominating share of approximately 60% in the market in 2024, due to a growth in influenza recurrence. Moreover, their complication also increased the mortality rates, which increased the use of the vaccines. The companies also contributed to their growth by increasing their production.

By vaccine type, the RSV (Respiratory Syncytial Virus) vaccines segment is expected to show the highest growth during the predicted time. The growing disease burden is increasing the use of these vaccines. This, in turn, is also growing their awareness and production rates.

By technology platform type, the inactivated/split virion vaccines segment led the market with approximately a 35% share in 2024, as they provided enhanced safety in the geriatric, pediatric population, and in pregnant women. Moreover, they also minimize the risk of vaccine-derived infection. Additionally, their affordability and stability also enhanced their acceptance rates.

By technology platform type, the mRNA-based vaccines segment is expected to show the fastest growth rate during the predicted time. These platforms provide high efficacy, which in turn is increasing their use in respiratory viruses. They are also being used in the development of multi-pathogen vaccines.

By route of administration type, the intramuscular segment held the largest share of approximately 70% in the market in 2024, as it provided strong and fast immune activation. Moreover, they showed consistent absorption and improved safety and efficacy. Furthermore, they were preferred for a wide range of vaccines.

By route of administration type, the intranasal segment is expected to show the highest growth during the upcoming years. They are being used against respiratory viruses and are ideal for children and needle-phobic patients. This is increasing the patient compliance and acceptance rates, increasing their development.

By end user, the public health agencies segment led the global market with approximately 45% share in 2024, driven by the bulk use of seasonal vaccines. At the same time, they enhanced access to the vaccines by providing funds for the high-risk population. Moreover, they also increased vaccination awareness through campaigns and enhanced their distribution through hospitals and clinics.

By end user, the pharmacies & retail vaccination centers segment is expected to show the fastest growth rate during the upcoming years. These centers are widely available and provide quick services, which increases the reliance on them for seasonal vaccines. Moreover, their growing legalization of vaccination is also decreasing the hospital and clinic vaccination burden.

")

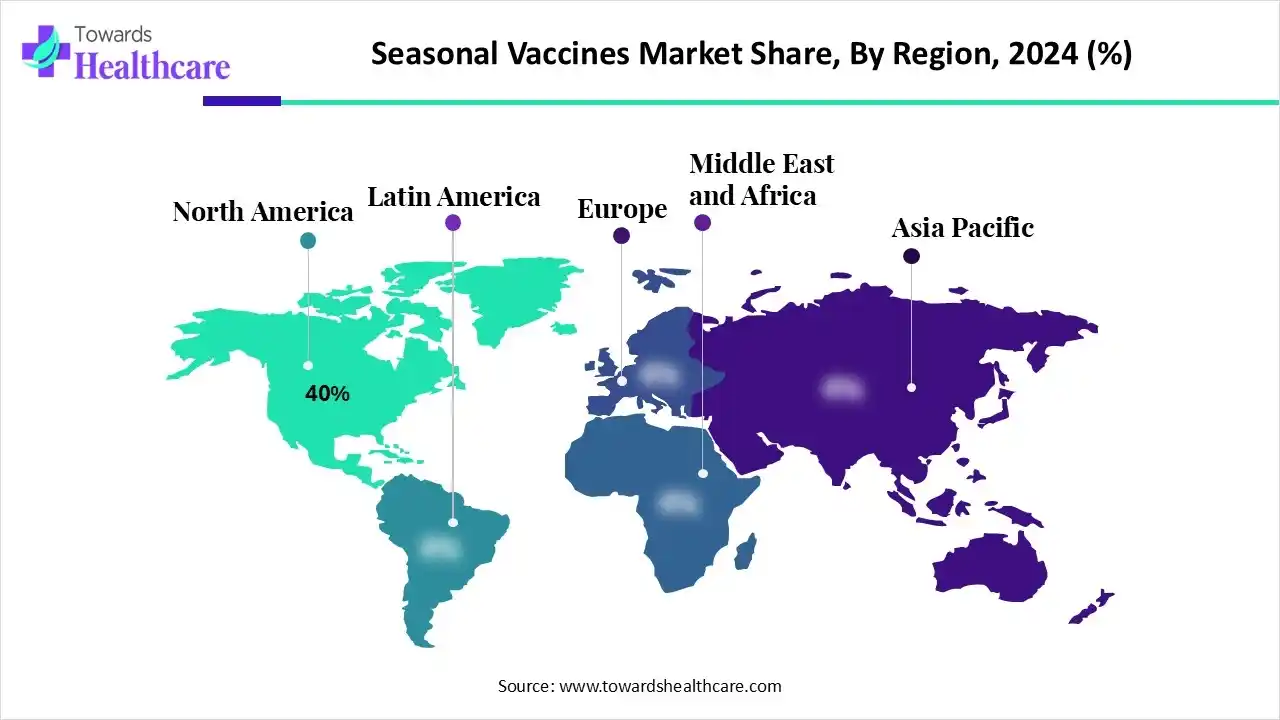

North America dominated the seasonal vaccines market with 40% in 2024, due to growth in the healthcare investments, which increases the affordability and assess to the seasonal vaccines. At the same time, the growing awareness through campaigns or programs supported by the government is increasing their use. Moreover, the industries are utilizing advanced technologies to enhance the development of these vaccines, which has contributed to the market growth.

The growing government vaccination campaigns are increasing the use of seasonal vaccines in the U.S., where their growing production and innovations are also being supported by healthcare investments. Moreover, to avoid the risk of complications in geriatric or pediatric populations, the companies are developing RSV vaccines, COVID-19 vaccines, along with the flu vaccines. Additionally, the faster approvals are encouraging their innovations as well as their use.

For instance,

Asia Pacific is expected to host the fastest-growing seasonal vaccines market during the forecast period, due to a large population, which increases the risk of infectious and chronic diseases. This, in turn, is increasing the demand for seasonal vaccines, whose use is also driven by growing government immunization programs. Moreover, the expanding healthcare is increasing the adoption of advanced technologies, which is promoting the development of next-generation vaccines, enhancing the market growth.

The growth in the immunization campaigns conducted by the government and private sector to deal with the growing diseases is increasing the awareness among the population of India. This is increasing the use of seasonal vaccines, especially in the pediatric population. At the same time, the industries are developing various vaccines for different diseases at affordable prices, which is increasing their use.

For instance,

Europe is expected to grow significantly in the seasonal vaccines market during the forecast period. The presence of a strong healthcare system is increasing the use of seasonal vaccines throughout the vaccination programs for the geriatric population, healthcare workers, and patients with chronic diseases. These programs are supported by government funding, which makes them affordable, accessible, and increases their use, where companies are also contributing by developing new seasonal vaccine candidates. Thus, this is promoting the market growth.

The use of seasonal vaccines across Germany is increasing due to the presence of robust health insurance policies. Moreover, the growth in seasonal flu and the geriatric population is increasing the use of these vaccines. Additionally, the industries are developing new COVID boosters, RSV vaccines, and combination vaccines.

For the 2024/2025 season, Germany saw influenza A and B co-circulate. Interim vaccine effectiveness against any influenza was estimated at 31% in primary care and 69% in secondary care. Measles vaccination is mandatory.

To develop the next generation platforms, such as nanoparticles, mRNA, and viral vectors, to enhance vaccine effectiveness, production speed, and long-lasting protection against evolving influenza strains, is the main focus of R&D for seasonal vaccines.

Key Players: Sanofi, CSL Seqirus, GlaxoSmithKline plc, Merck & Co., Inc., AstraZeneca plc.

The clinical trial approval for seasonal vaccines depends on their safety and effectiveness, while the regulatory approvals are based on minimal or no new clinical data if the manufacturing process is consistent and new strains are similar to previously approved ones.

Key Players: Sanofi, CSL Seqirus, GlaxoSmithKline plc, Merck & Co., Inc., AstraZeneca plc, Pfizer Inc.

The formulation and final dosage preparation of seasonal vaccines involves the combination of specific viral antigens, selected by global health authorities, with stabilizing and other inert ingredients into a liquid suspension, which is diluted to the precise final dosage and filled in single-dose syringes or multi-dose vials for distribution.

Key Players: Sanofi, CSL Seqirus, GlaxoSmithKline plc, Merck & Co., Inc., AstraZeneca plc, Abbott Laboratories.

The patient support and services in the seasonal vaccines involve educational campaigns to promote vaccine importance and reduce hesitancy, and patient assistance programs to cover the costs of uninsured or underserved individuals.

Key Players: Sanofi, CSL Seqirus, GlaxoSmithKline plc, Merck & Co., Inc., AstraZeneca plc, Abbott Laboratories.

By Vaccine Type

By Technology Platform

By Route of Administration

By End-User

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar