")

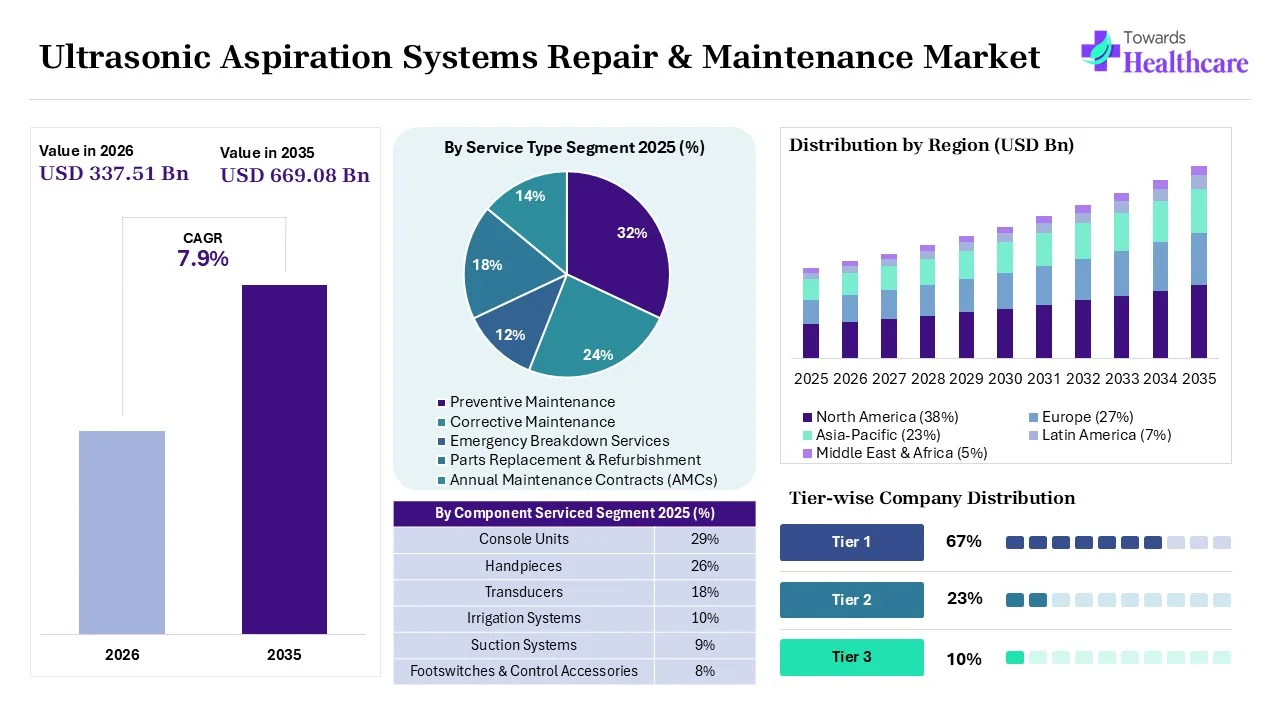

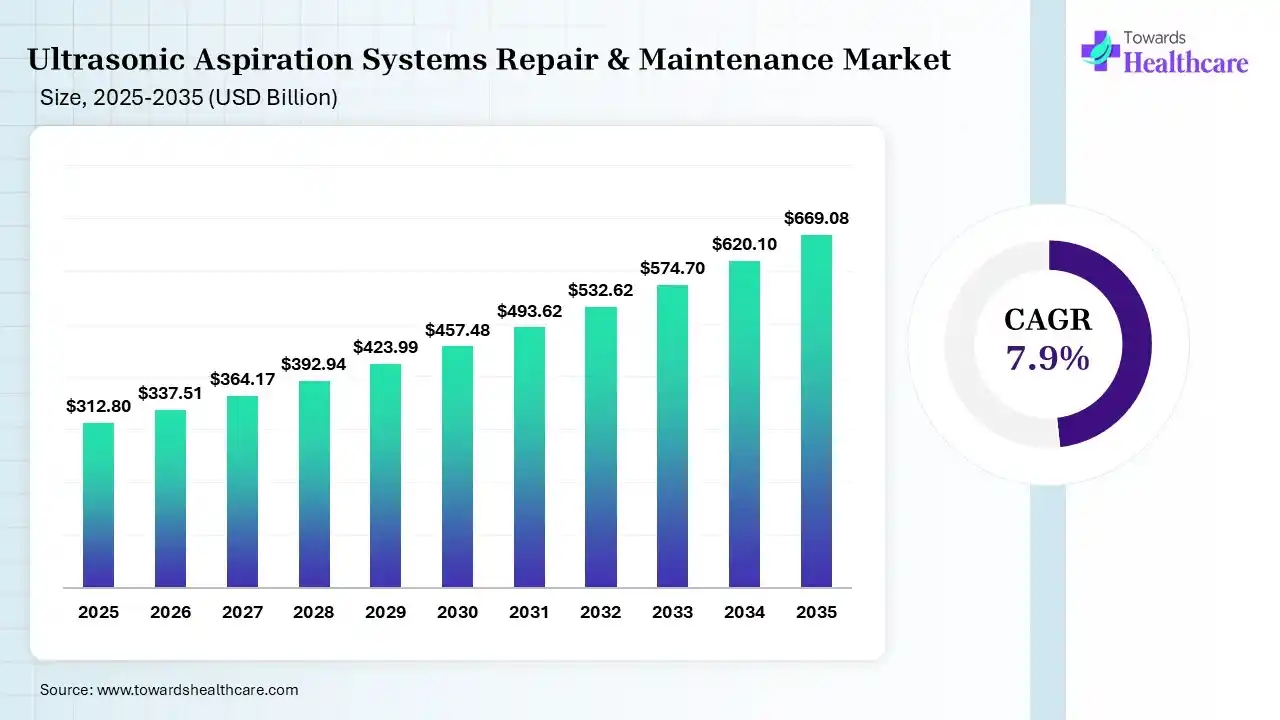

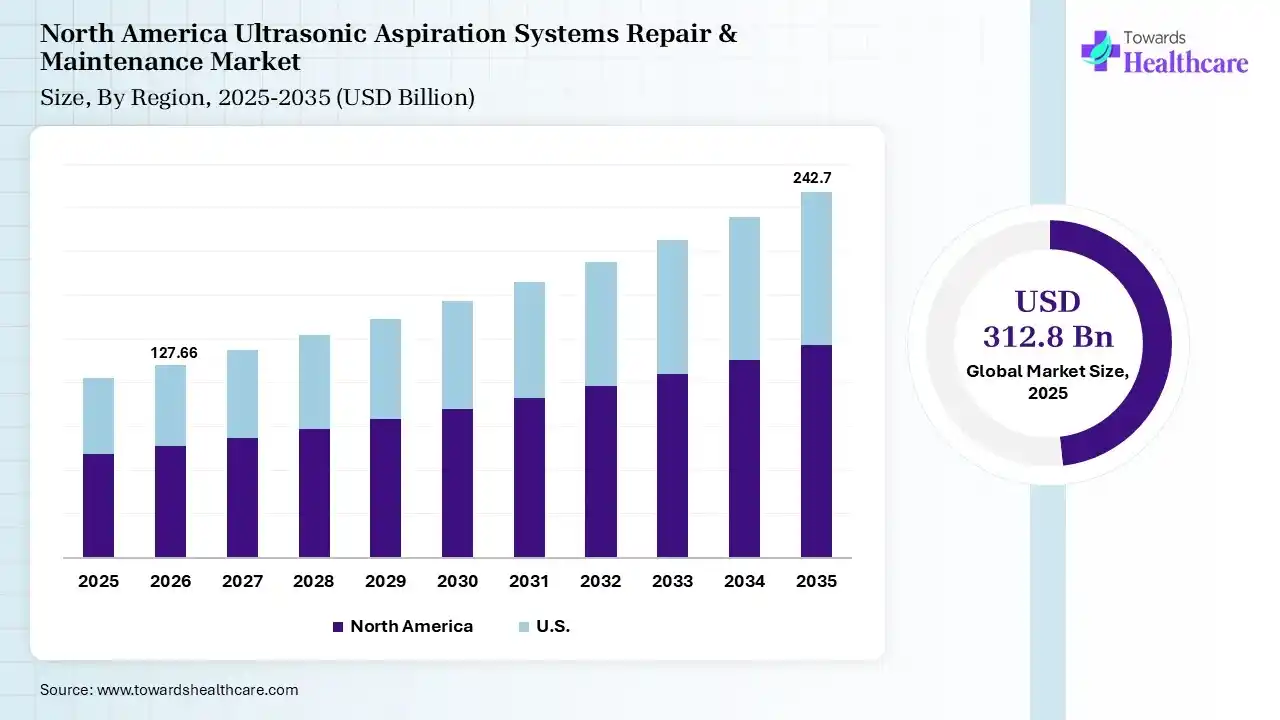

The global ultrasonic aspiration systems repair & maintenance market size was estimated at USD 312.8 billion in 2025 and is predicted to increase from USD 337.51 billion in 2026 to approximately USD 669.08 billion by 2035, expanding at a CAGR of 7.9% from 2026 to 2035. Increasing surgical volume is driving the demand for ultrasonic aspiration systems repair and maintenance services globally. Expanding healthcare facilities, investments, remote diagnostic services, and new service launches are also enhancing the market growth.

")

The ultrasonic aspiration systems repair & maintenance market is driven by increasing surgical volumes and growing focus on extending the lifespan of high-capital surgical assets. The ultrasonic aspiration systems repair & maintenance encompass services ensuring ultrasonic aspiration systems' efficiency, safety, and accuracy. The ultrasonic aspiration systems are surgical devices that are used to remove soft tissue without damaging surrounding tissues with the use of ultrasonic vibrations. This drives their use for tumor resection, neurosurgeries, liver surgeries, gynecological surgeries, urological surgeries, cardiothoracic surgeries, and other complex surgeries, where the growing incidence of multiple cancer types is also increasing the demand for ultrasonic aspiration systems globally.

This, in turn, is increasing the use of ultrasonic aspiration systems for repair and maintenance services to minimize equipment downtime, maintain surgical precision, reduce repair costs, support regulatory compliance, and ensure patient safety. The repair and maintenance services provided by the companies involve preventive maintenance, corrective repairs, component replacement, performance testing, software updates, technical support, and refurbishment services. At the same time, the growing adoption of ultrasonic aspiration systems, expanding healthcare facilities, increasing investments, stringent regulations, and expanding remote diagnostics are enhancing the market growth.

The use of AI in the ultrasonic aspiration systems repair & maintenance market is increasing as it offers predictive maintenance and helps in reducing the chances of component failure. It also offers real-time performance monitoring, automated diagnostics, and remote monitoring support, which drives faster troubleshooting and detection of changes in system operations. AI is also used for maintenance scheduling, analysis of sensor data, and spare parts forecasting, which in turn helps in enhancing equipment performance, reliability, and lifespan.

Shift Towards Preventive Maintenance

In order to reduce unexpected equipment failures, ensure uninterrupted surgical workflows, and enhance system reliability, healthcare providers are shifting towards preventive maintenance services. This, in turn, is increasing the demand for ultrasonic aspiration systems repair and maintenance services for their timely calibration, component replacement, and software updates. Additionally, long service agreements and contracts are also being formed among the healthcare facilities, which are also promoting their use.

Rising Remote Monitoring Trends

Expanding telehealthcare services are driving the demand for remote diagnostics and cloud-connected service platforms. They are being utilized to provide real-time monitoring of equipment health, detection of technical issues, troubleshooting issues remotely, and proactive maintenance, which is enhancing service efficiency and minimizing operational costs. This is driving the development and adoption of cloud-based platforms, connected devices, and IoT-enabled sensors, which also help in reducing on-site visits and maintenance costs associated with them.

Focus on Equipment Lifecycle Extension

With the growing use and importance of ultrasonic aspiration systems globally, companies are focusing on enhancing their usability and extending their lifecycle. This, in turn, is increasing their focus on optimizing lifecycle extension services, capital expenditures, and refurbishments, where they will offer continuous software enhancements, upgrades, and component replacements. The cost-conscious healthcare facilities are also increasing their demand to enhance ultrasonic aspiration systems' sustainability and reduce the chance of equipment replacement.

| Table | Scope |

| Market Size in 2026 | USD 337.51 Billion |

| Projected Market Size in 2035 | USD 669.08 Billion |

| CAGR (2026 - 2035) | 7.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Equipment Type, By Component Serviced, By Service Provider, By End User, By Contract Duration, By Maintenance Mode, By Region |

| Top Key Players | Stryker Corporation, Olympus Corporation, Integra LifeSciences Corporation, Richard Wolf GmbH, Misonix Inc., Medtronic plc, Soring GmbH |

")

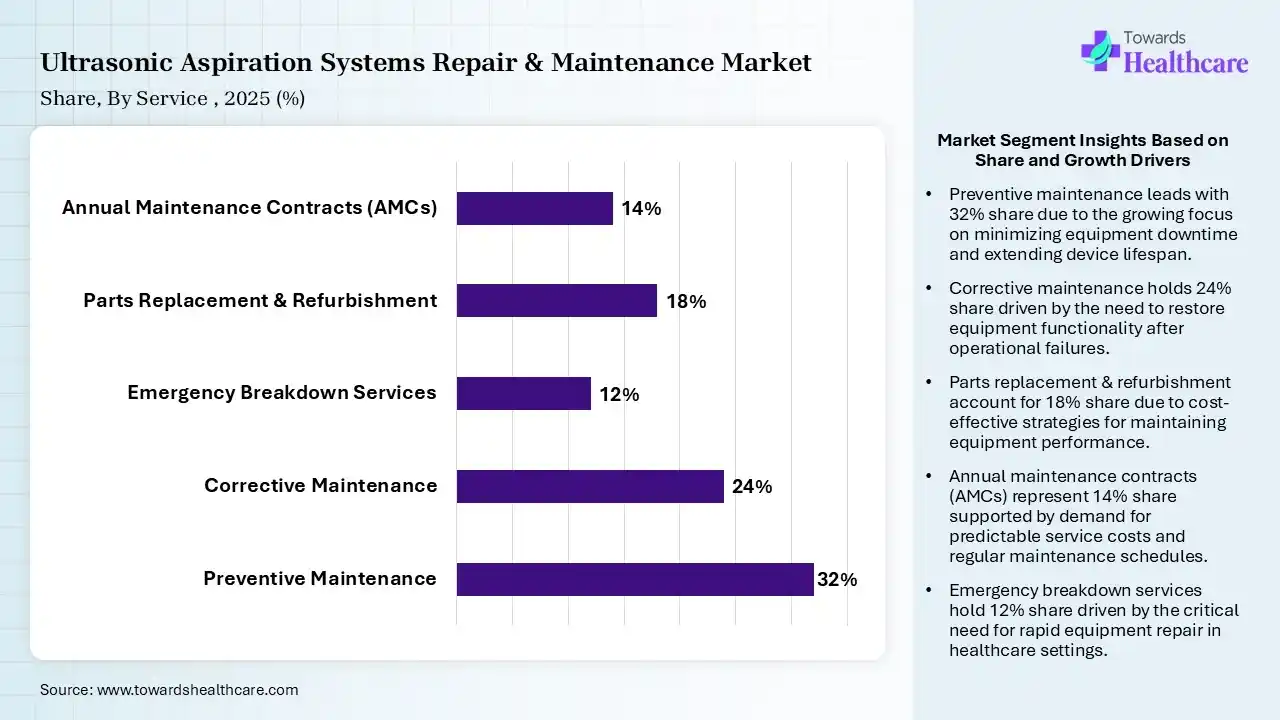

| Segment | Share 2025 (%) |

| Preventive Maintenance | 32% |

| Corrective Maintenance | 24% |

| Emergency Breakdown Services | 12% |

| Parts Replacement & Refurbishment | 18% |

| Annual Maintenance Contracts (AMCs) | 14% |

The Preventive Maintenance Segment Dominated the Market With 32% in 2025

The preventive maintenance segment led the ultrasonic aspiration systems repair & maintenance market with a 32% share in 2025, due to a rise in hospitals prioritizing uptime and compliance. Scheduled servicing reduced unexpected failures, which increased the shift towards preventive maintenance. Growth in the installed base also supported their recurring maintenance demand.

The corrective maintenance segment held the second-largest share of 24% of the market in 2025, as aging systems require component-level repairs. Complex surgical environments increase wear rates, which in turn drives the demand for these services. At the same time, cost control encourages targeted repair activities, enhancing their acceptance rates.

The parts replacement & refurbishment segment held 18% of the ultrasonic aspiration systems repair & maintenance market share in 2025, as refurbishment extends the equipment lifecycle. Facilities seek lower ownership costs, promoting their use. Demand for certified replacement components continues to expand, encouraging their adoption.

The annual maintenance contracts (AMCs) segment held 14% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 9.4% during the forecast period, due to long-term service agreements, which provide predictable budgets. OEMs increasingly bundle service offerings. Healthcare systems are also favoring comprehensive maintenance planning.

")

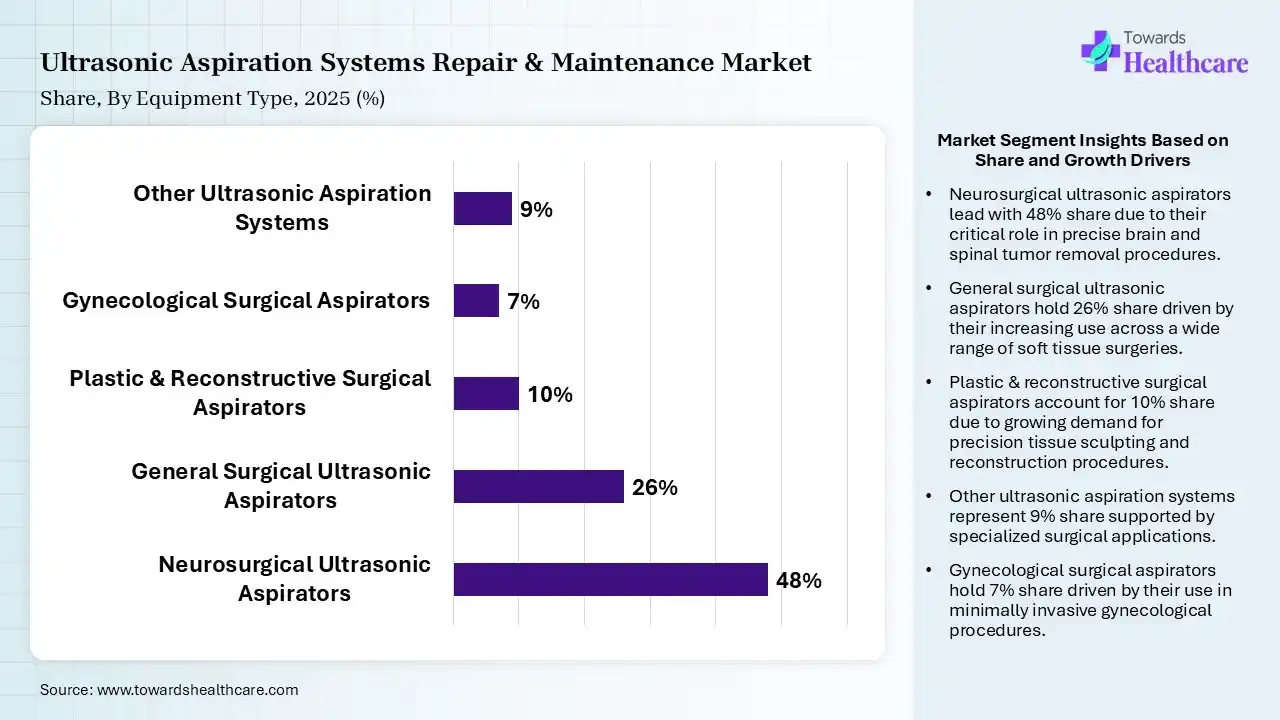

| Segment | Share 2025 (%) |

| Neurosurgical Ultrasonic Aspirators | 48% |

| General Surgical Ultrasonic Aspirators | 26% |

| Plastic & Reconstructive Surgical Aspirators | 10% |

| Gynecological Surgical Aspirators | 7% |

| Other Ultrasonic Aspiration Systems | 9% |

The Neurosurgical Ultrasonic Aspirators Segment Dominated the Market With 48% in 2025

The neurosurgical ultrasonic aspirators segment accounted for the highest revenue share of 48% of the ultrasonic aspiration systems repair & maintenance market in 2025, driven by high utilization in tumor resections, which increased service needs. Advanced systems require specialized maintenance, which promotes the use of various repair and maintenance services. Expansion of the neurosurgical procedures also supported their growth.

The general surgical ultrasonic aspirators segment held the second-largest share of 26% of the market in 2025, due to the rising hepatic and gastrointestinal surgeries, which increase equipment usage. Hospitals are also maintaining operational efficiency through servicing. Procedure volumes continue expanding globally, which ultimately drives the demand for repair and maintenance services.

The plastic & reconstructive surgical aspirators segment held 10% of the ultrasonic aspiration systems repair & maintenance market share in 2025, due to the growth in reconstructive procedures, which raises equipment demand. Clinics prioritize reliability and precision. Regular servicing preserves treatment outcomes, which increases the use of ultrasonic aspiration systems, repair & maintenance services.

The other ultrasonic aspiration systems segment held 9% of the market share in 2025 and is expected to show the highest growth with a CAGR of 8.6% during the forecast period, driven by emerging applications that broaden utilization. Healthcare providers are also adopting specialized systems. This increases the demand for service with new installations.

")

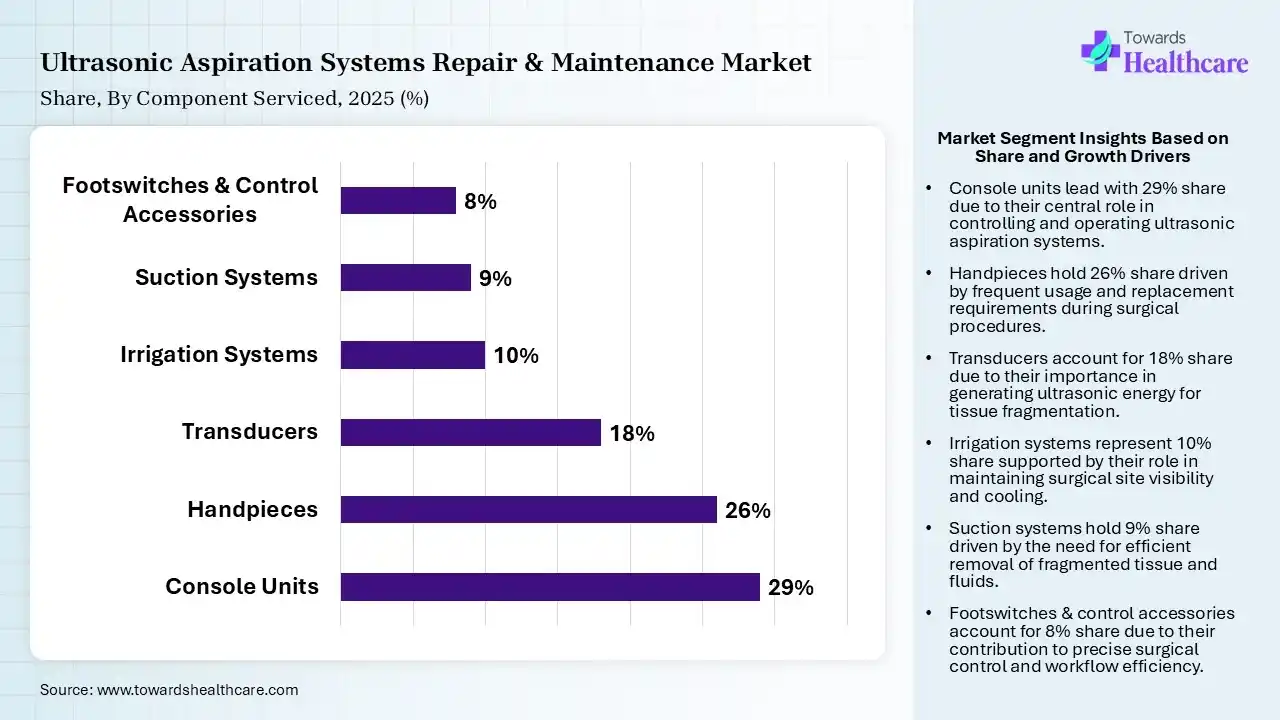

| Segment | Share 2025 (%) |

| Console Units | 29% |

| Handpieces | 26% |

| Transducers | 18% |

| Irrigation Systems | 10% |

| Suction Systems | 9% |

| Footswitches & Control Accessories | 8% |

The Console Units Segment Dominated the Market With 29% in 2025

The console units segment held a major revenue share of 29% of the ultrasonic aspiration systems repair & maintenance market in 2025, as central control systems required periodic servicing. Electronic modules experience operational stress, which contributes to the rise in the demand for their repair and maintenance services. Software integration also increased maintenance complexity.

The handpieces segment held the second-largest share of 26% of the market in 2025, driven by frequent clinical use, which accelerates wear, driving the demand for their repair and maintenance services. Additionally, precision requirements necessitate regular servicing. Replacement cycles also remain relatively short, encouraging the use of these services.

The transducers segment held 18% of the ultrasonic aspiration systems repair & maintenance market share in 2025, as the core ultrasonic functionality depends on transducer performance. Their intensive use impacts efficiency, which increases the demand for their continuous maintenance. Facilities increasingly replace aging units, contributing to the growth in their repair and maintenance services.

The footswitches & control accessories segment held 8% of the market share in 2025 and is expected to expand rapidly with a CAGR of 9.1% during the forecast period, due to the increasing accessory replacement frequency. Advanced control systems require calibration, which promotes the use of ultrasonic aspiration systems for repair & maintenance solutions. Additionally, their growing adoption is also supporting service revenues.

")

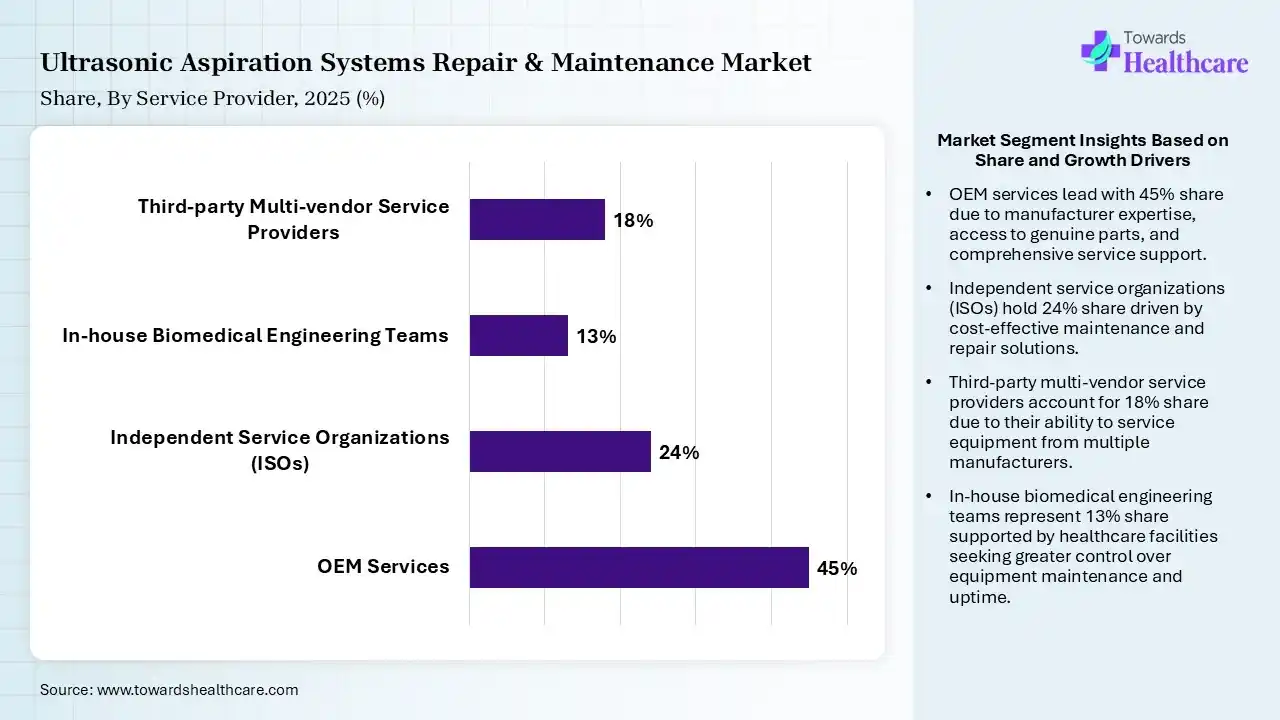

| Segment | Share 2025 (%) |

| OEM Services | 45% |

| Independent Service Organizations (ISOs) | 24% |

| In-house Biomedical Engineering Teams | 13% |

| Third-party Multi-vendor Service Providers | 18% |

The OEM Services Segment Dominated the Market With 45% in 2025

The OEM services segment held the largest revenue share of 45% of the ultrasonic aspiration systems repair & maintenance market in 2025, as a large number of hospitals preferred manufacturer-certified maintenance. Proprietary technologies also favored OEM involvement, where warranty-linked servicing also remained common. Faster access to various diagnostic tools also encouraged their use.

The independent service organizations (ISOs) segment held the second-largest share of 24% of the market in 2025, due to their cost-effective alternatives, which attract healthcare facilities. Technical capabilities continue improving, which promotes their adoption rates. Multi-brand expertise and fast services also support their adoption. Their customized and user-friendly solutions are driving their demand.

The third-party multi-vendor service providers segment held 18% of the ultrasonic aspiration systems repair & maintenance market share in 2025 and is expected to grow with the fastest CAGR of 9.2% during the forecast period, as consolidated service management reduces complexity. Multi-vendor support also improves their efficiency. Healthcare networks are also increasingly outsourcing maintenance.

The in-house biomedical engineering teams segment held 13% of the market share in 2025, driven by large hospitals maintaining internal capabilities. Routine servicing is performed internally, where immediate troubleshooting also promotes their use. Their fast response to technical issues and compliance with regulatory standards also promote their use.

")

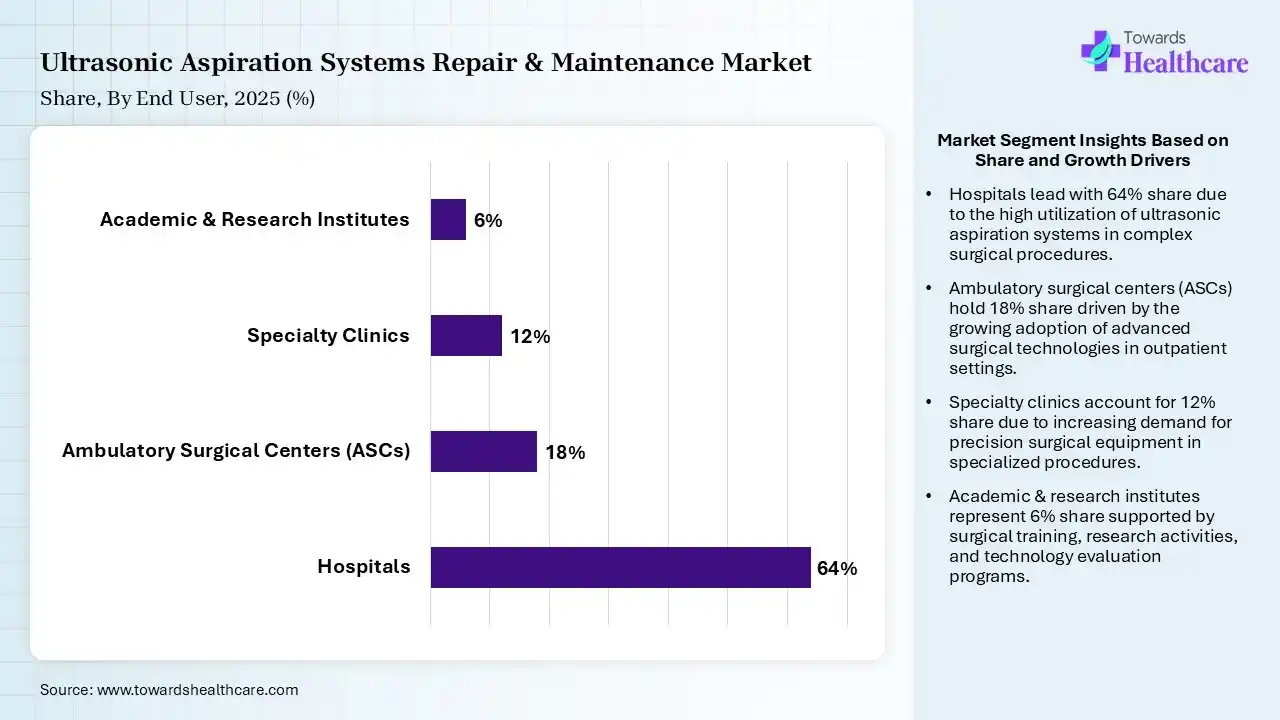

| Segment | Share 2025 (%) |

| Hospitals | 64% |

| Ambulatory Surgical Centers (ASCs) | 18% |

| Specialty Clinics | 12% |

| Academic & Research Institutes | 6% |

The Hospitals Segment Dominated the Market With 64% in 2025

The hospitals segment contributed the biggest revenue share of 64% of the ultrasonic aspiration systems repair & maintenance market in 2025, due to the concentration of major surgical procedures in hospitals. A large installed equipment base also increased maintenance demand. Continuous operation required comprehensive servicing, which increased the use of ultrasonic aspiration systems' repair and maintenance services.

The ambulatory surgical centers (ASCs) segment held the second-largest share of 18% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.8% during the forecast period, due to the fact that outpatient surgery volumes are continuing to increase. Facilities seek high equipment availability, driving the demand for repair and maintenance. Service contracts also support operational continuity.

The specialty clinics segment held 12% of the ultrasonic aspiration systems repair & maintenance market share in 2025, due to the specialized surgical centers expand utilization. Precision equipment requires regular maintenance, which drives the demand for ultrasonic aspiration systems repair & maintenance services. Growing procedural complexity also supports their growing usage.

The academic & research institutes segment held 6% of the market share in 2025, driven by research facilities that maintain advanced surgical equipment. A rise in funding is also supporting periodic servicing. At the same time, growing R&D activities and training also drive equipment longevity demand, promoting the use of ultrasonic aspiration systems repair & maintenance services.

North America dominated the ultrasonic aspiration systems repair & maintenance market with 38% in 2025, due to a large installed base and advanced surgical infrastructure, which supported the rise in demand. High service contract penetration and a rise in the number of neurosurgical and oncological procedures also increased the recurring revenues. At the same time, technology upgrades also sustained maintenance requirements, which contributed to the market growth.

U.S. Market Trends

The presence of an extensive installed base and high surgical volume in the U.S. supported service demand. Advanced healthcare infrastructure and a rise in their expenditures also increase contract adoption, which in turn drives the demand for various ultrasonic aspiration systems repair & maintenance. Continuous technology upgrades are also sustaining maintenance activity.

Canada Market Trends

Public healthcare investment supports equipment upkeep across Canada. Hospitals prioritize reliability and compliance, which drives the use of ultrasonic aspiration systems repair & maintenance services. Preventive maintenance adoption remains strong, which in turn increases their use, where growing demand for minimally invasive surgeries also drives their demand.

Asia Pacific held a 23% share of the ultrasonic aspiration systems repair & maintenance market in 2025 and is expected to grow at the fastest CAGR of 9.8% during the forecast period, due to the expanding healthcare infrastructure, which boosts installations. At the same time, the continuous rise in surgical procedure volumes is also increasing the demand for ultrasonic aspiration systems repair & maintenance. Rapid adoption of advanced equipment and growing technological advancements are also increasing service demand, enhancing the market growth.

China Market Trends

Rapid healthcare expansion across China is driving ultrasonic aspiration system installations, ultimately promoting the demand for their repair and maintenance services. Growing neurosurgical capacity, along with rising oncology and complex surgical procedures, is boosting maintenance needs. Investments in advanced surgery and expanding medical device companies are also supporting the market growth.

India Market Trends

Rapid hospital expansion across India is accelerating equipment deployment, which in turn is increasing the demand for ultrasonic aspiration systems repair & maintenance. Rising surgical volumes and preventive maintenance awareness are also increasing servicing needs. Furthermore, increasing private healthcare investment, as well as expanding medical tourism, also supports market growth.

| Companies | Headquarters | Ultrasonic Aspiration Systems Repair & Maintenance Services |

| Stryker Corporation | Kalamazoo, U.S. | Stryker ProCare Services |

| Olympus Corporation | Tokyo, Japan | Olympus Surgical Endoscopy and Energy Services Contracts |

| Integra LifeSciences Corporation | Princeton, U.S. | Integra International Service and Repair programs |

| Richard Wolf GmbH | Knittlingen, Germany | Richard Wolf Field Service and Technical Lifecycle Management |

| Misonix Inc. | Farmingdale, U.S. | Bioventus Surgical Technical Support and Depot Repair |

| Medtronic plc | Dublin, Ireland | Medtronic Biomedical Lifecycle Services |

| Soring GmbH | Quickborn, Germany | Spring Authorized Technical Service and Repair |

In May 2026, after the announcement of collaboration between Stryker’s Neurosurgical team which offered Sonopet iQ Ultrasonic Aspirator and National Brain Tumor Society (NBTS), the Vice President and General Manager of Stryker's Neurosurgical business, Mitch Foley, expressed "We're proud to partner with the society to support, empower, and amplify the voice of the brain tumor community as we work to advance neurosurgery and transform lives,"

By Service Type

By Equipment Type

By Component Serviced

By Service Provider

By End User

By Contract Duration

By Maintenance Mode

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar