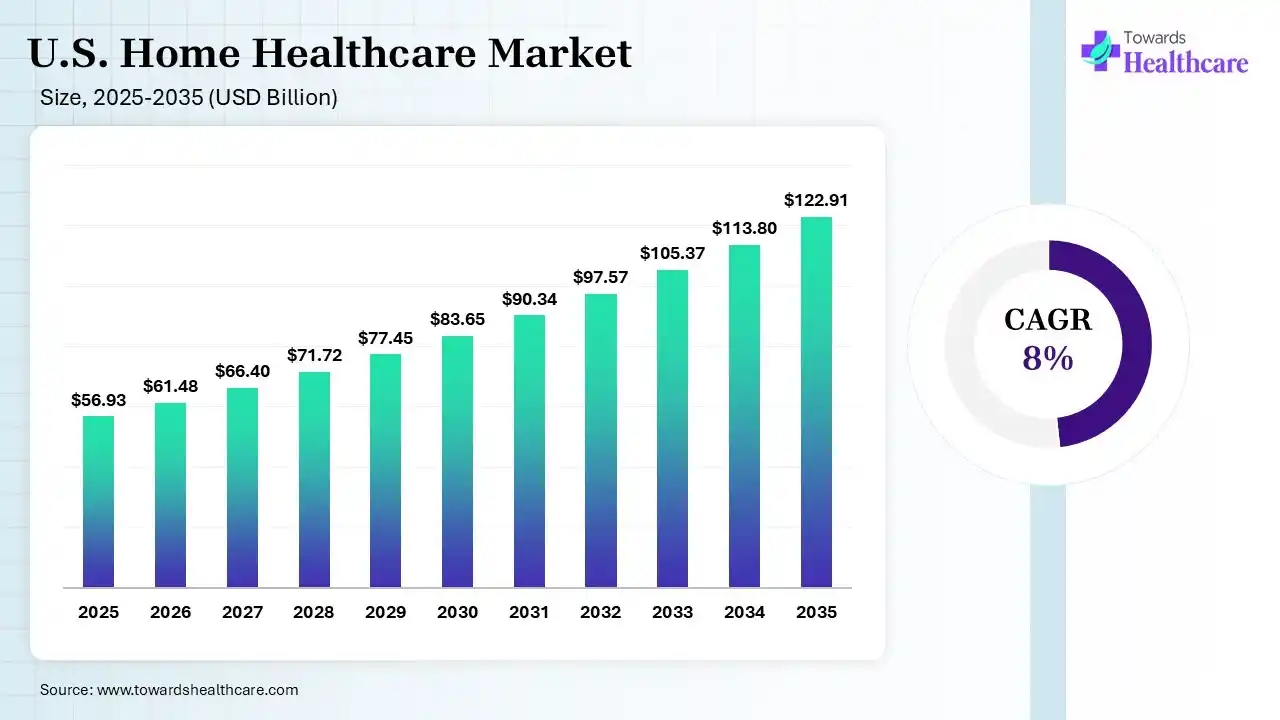

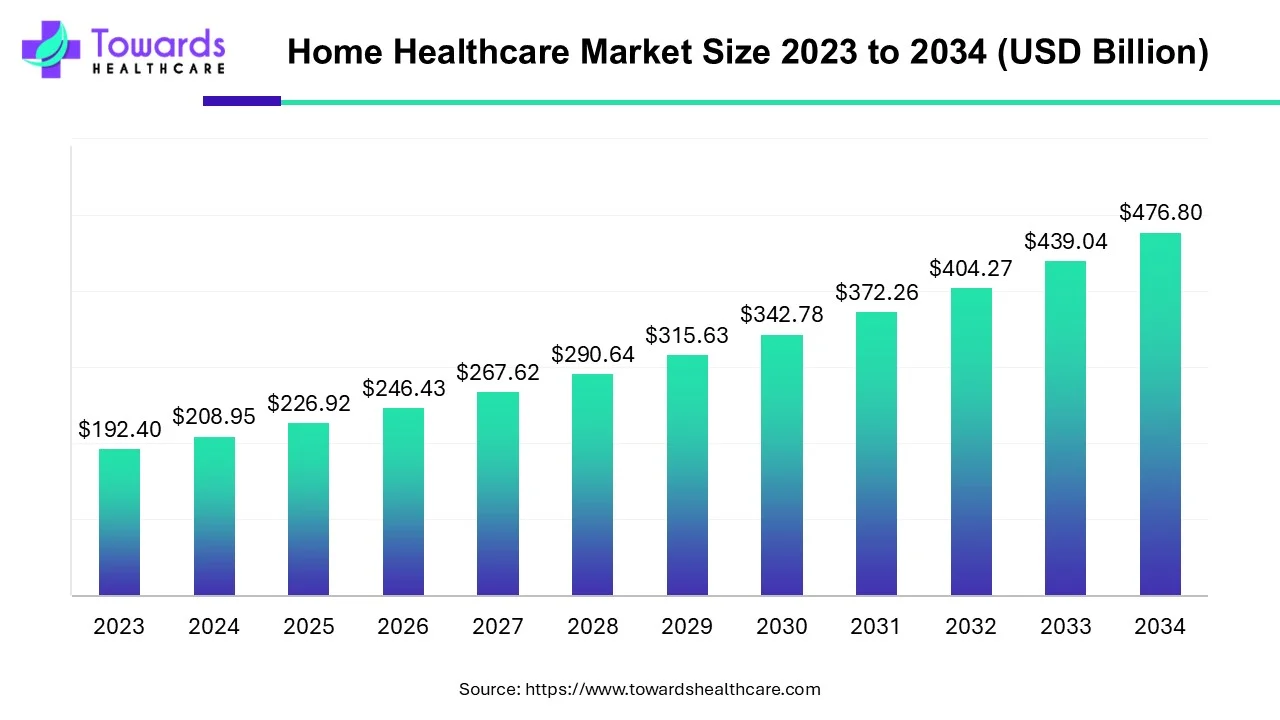

The U.S. home healthcare market size was estimated at USD 56.93 billion in 2025 and is predicted to increase from USD 61.48 billion in 2026 to approximately USD 122.91 billion by 2035, expanding at a CAGR of 8% from 2026 to 2035. The market is growing steadily due to the increasing elderly population, rising chronic health conditions, and higher demand for personalized medical care at home. Technological advancements in telehealth and remote monitoring, along with the focus on reducing hospital stays and healthcare costs, are further driving market expansion.

")

Home healthcare refers to medical and supportive care services to patient in their homes, including nursing care, therapy, rehabilitation, and remote health monitoring. The U.S. home healthcare market is growing due to the increasing aging population, rising prevalence of chronic diseases, and growing preference for receiving medical care at home. Advancements in telehealth, remote patient monitoring, and home-based treatment technologies are improving patient outcomes and convenience. In addition, the need to reduce hospital admissions and healthcare costs, along with supportive reimbursement policies, is further accelerating demand for home healthcare services across the country.

Artificial intelligence is reshaping the market by enabling remote patient monitoring, predictive health analysis, and personalized treatment plans. AI-powered tools help healthcare providers detect health risks early, improve patient engagement, and reduce emergency hospital visits. In addition, virtual assistants, smart wearable devices, and automated care management systems enhance efficiency, lower healthcare costs, and support better decision-making, driving the adoption of advanced home healthcare solutions.

Expansion of Telehealth & Remote Monitoring

The use of telehealth services and remote patient monitoring devices is growing rapidly across the U.S. home healthcare market. These technologies improve access to healthcare, support continuous patient tracking, and reduce unnecessary hospital visits, making home-based care more convenient and efficient.

Increasing Preference for In-Home Elderly Care

The rising aging population in the U.S. is increasing demand for long-term and elderly home healthcare services. Families are increasingly choosing in-home nursing, rehabilitation, and personal care services to improve patient comfort, independence, and quality of life.

Rising Focus on Cost-Effective Healthcare Solutions

Healthcare providers and patients are shifting toward home healthcare services to reduce hospitalization expenses and overall treatment costs. Home-based care offers affordable treatment options while improving recovery outcomes, driving strong market growth and future expansion opportunities in the U.S. healthcare sector.

| Table | Scope |

| Market Size in 2026 | USD 61.48 Billion |

| Projected Market Size in 2035 | USD 122.91 Billion |

| CAGR (2026 - 2035) | 8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Component, By Indication, By Service Type, By Payer, By Delivery Mode |

| Top Key Players | McKesson Medical-Surgical, Inc., NxStage Medical (Fresenius Medical Care), Medline Industries Inc., Medtronic plc, Louisville, Kindred Healthcare LLC, Brookdale Senior Living Inc., Sunrise Senior Living LLC |

")

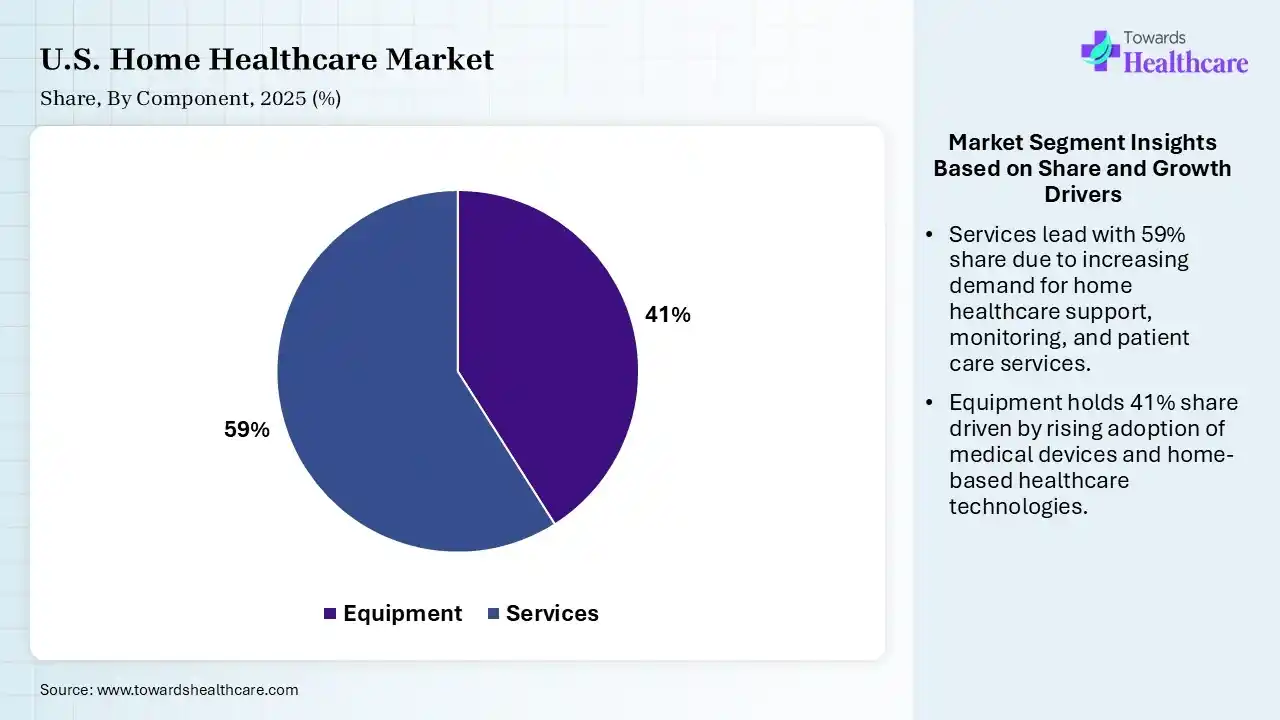

| Segment | Share 2025 (%) |

| Equipment | 41% |

| Services | 59% |

The Services Segment Dominated the U.S. Home Healthcare Market in 2025

The services segment held the largest share of 59% in 2025 and is expected to grow at the fastest CAGR of 8.70% in the U.S. home healthcare market during the forecast period due to the rising demand for skilled nursing, rehabilitation, physical therapy, and personal care services. Increasing elderly populations, higher prevalence of chronic diseases, and the growing preference for personalized in-home treatment are driving services adoption. Additionally, improved healthcare accessibility and the shift towards cost-effective long-term care solutions are further supporting rapid segment growth.

The equipment segment held a significant share of 41% in 2025 due to the rising demand for medical devices such as mobility aids, monitoring systems, oxygen delivery equipment, and home dialysis devices. Increasing cases of chronic diseases, aging populations, and the growing preference for home-based treatment boosted the adoption of advanced healthcare equipment. In addition, technological advancements and improved accessibility of portable medical devices further supported segment growth.

")

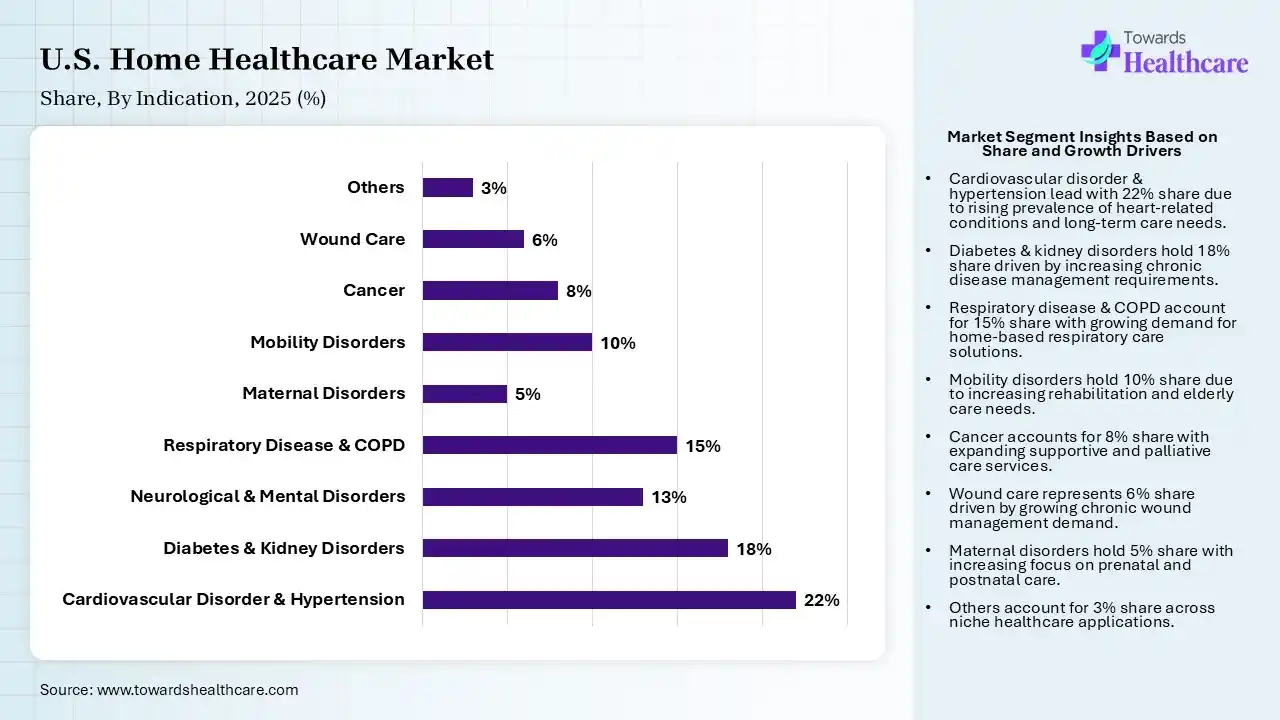

| Segment | Share 2025 (%) |

| Cardiovascular Disorder & Hypertension | 22% |

| Diabetes & Kidney Disorders | 18% |

| Neurological & Mental Disorders | 13% |

| Respiratory Disease & COPD | 15% |

| Maternal Disorders | 5% |

| Mobility Disorders | 10% |

| Cancer | 8% |

| Wound Care | 6% |

| Others | 3% |

The Cardiovascular Disorders & Hypertension Segment Led the Market in 2025 with the Largest Share

The cardiovascular disorders & hypertension segment led the U.S. home healthcare market with a share of 22% in 2025 due to the high prevalence of heart diseases, hypertension, and related chronic conditions among the aging population. Growing demand for continuous patient monitoring, home-based cardiac care, and rehabilitation services has increased the adoption of home healthcare solutions. Additionally, advancements in portable monitoring devices and the need to reduce hospital readmissions further support the segment’s market dominance.

The diabetes & kidney disorders segment held the second-largest share of 18% in 2025 due to the rising incidence of diabetes, chronic kidney diseases, and related complications. Increasing need for long-term disease management, regular monitoring of blood glucose and kidney function, and dialysis at home supports demand. A growing elderly population, unhealthy lifestyle, and preference for convenient, cost-effective home-based care further contribute to the strong growth of this segment.

The neurological & mental disorders segment held a 13% of market share due to the rising prevalence of Alzheimer’s, Parkinson’s disease, stroke-related disabilities, and mental health conditions such as depression and mental health conditions such as depression and anxiety. The increasing need for long-term care, rehabilitation, and cognitive support at home is driving demand. Growing awareness, shortage of institutional care facilities, and preference for patient comfort and personalized treatment are further accelerating segment growth.

The wound care segment held 6% share in 2025 and is expected to grow at the fastest CAGR of 9.20% in the U.S. home healthcare market during the forecast period due to the rising incidence of diabetes-related ulcers, pressure injuries, and post-surgical wounds among the aging population. Increasing demand for advanced wound care products, home-based dressing for advanced wound care products, home-based dressing services, and faster healing solutions is driving growth. Additionally, improved awareness, technological advancements in wound management, and preference for outpatient recovery are further accelerating segment expansion.

")

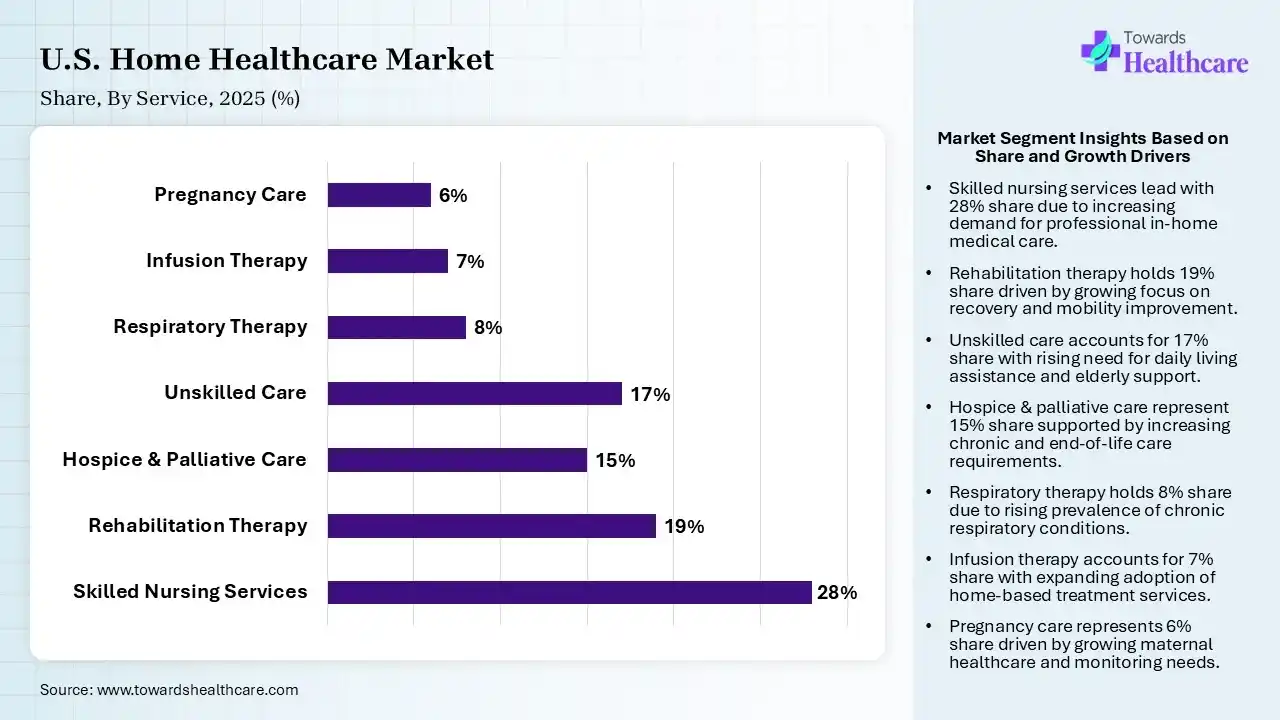

| Segment | Share 2025 (%) |

| Skilled Nursing Services | 28% |

| Rehabilitation Therapy | 19% |

| Hospice & Palliative Care | 15% |

| Unskilled Care | 17% |

| Respiratory Therapy | 8% |

| Infusion Therapy | 7% |

| Pregnancy Care | 6% |

The Skilled Nursing Services Segment Led the U.S. Home Healthcare Market in 2025 with the Largest Share

The skilled nursing services segment dominated the market with a share of 28% in 2025 due to the rising demand for professional medical care at home for elderly and chronically ill patients. Increasing cases of post-surgical recovery, complex health conditions, and the need for continuous monitoring drive demand. Skilled nurses provide essential services such as medication management, wound care, and chronic disease management, while reducing hospital stays and improving patient outcomes and safety.

The rehabilitation therapy segment held the second-largest share of 19% in 2025 due to the rising number of patients recovering from surgeries, stroke, injuries, and chronica condition. Growing demand for physical, occupational, and speed therapy at home supports functional recovery and independence. Increasing elderly population, higher incidence of musculoskeletal disorders, and preference for convenient, personalized, and cost-effective in-home rehabilitation services further drive segment growth.

The unskilled care segment held a 17% of market share due to rising demand for basic personal assistance services such as bathing, feeding, mobility support, and daily living activities. The growing elderly population, increase in chronic illnesses, and shortage of professional caregivers are driving reliance on non-skilled caregivers. Additionally, cost-effective service delivery and preference for long-term home-based supportive care are further accelerating segment growth.

The infusion therapy segment held 7% share in 2025 and is expected to grow at the fastest CAGR of 9.30% in the U.S. home healthcare market during the forecast period due to the rising prevalence of chronic diseases such as cancer, infections, and autoimmune disorders that require long-term intravenous treatment. Increasing preference for home-based infusion over hospital stays, coupled with advancements in portable infusion pumps and improved patient comfort, is driving adoption. Additionally, cost-effectiveness and reduced risk of hospital-acquired infections further support segment growth.

")

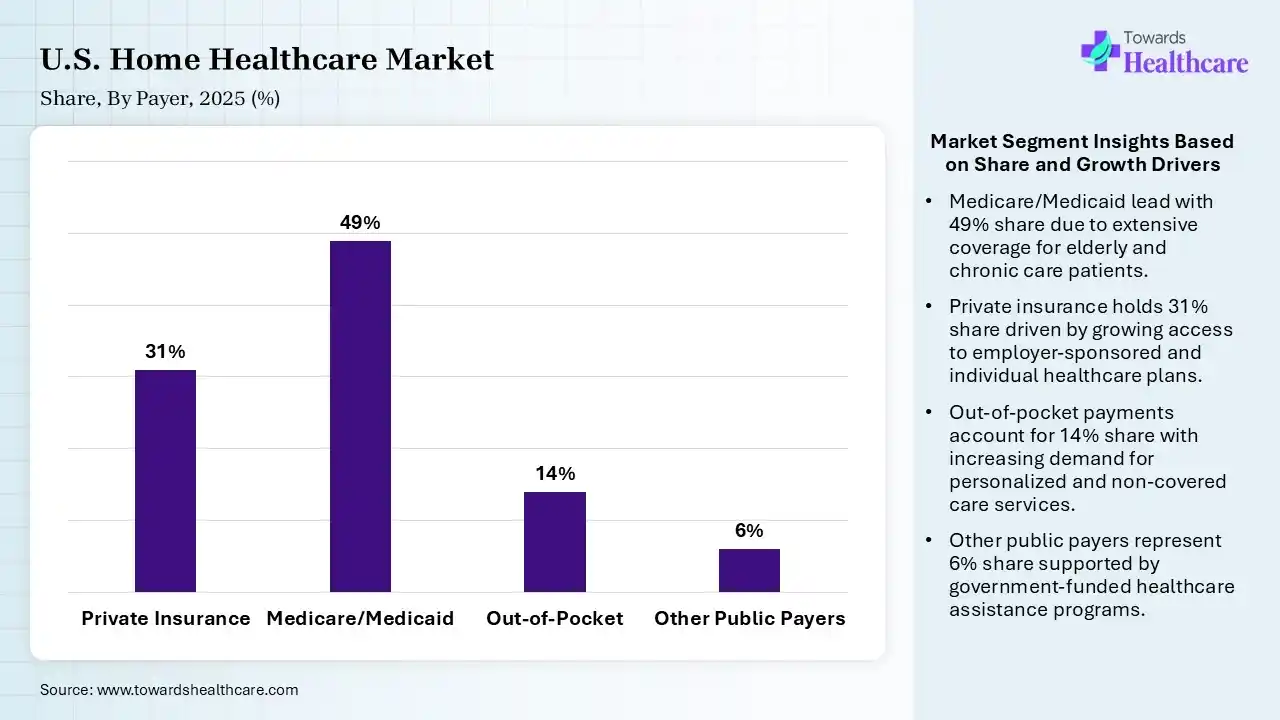

| Segment | Share 2025 (%) |

| Private Insurance | 31% |

| Medicare/Medicaid | 49% |

| Out-of-Pocket | 14% |

| Other Public Payers | 6% |

The Medicare/Medicaid Segment Led the Market in 2025 with the Largest Share

The Medicare/Medicaid segment led the U.S. home healthcare market with a share of 49% in 2025 and is expected to grow at the fastest CAGR of 8.50% in the market during the forecast period due to strong government support for the elderly and low-income populations requiring long-term care. These programs cover a significant portion og home healthcare services, including skilled nursing rehabilitation, and chronic disease management. The rising aging population, increasing prevalence of chronic conditions, and favorable reimbursement policies further drive utilization, making Medicare/ Medicaid the dominant payer segment in the market.

The private insurance segment held the second-largest share of 31% in 2025 due to increasing employer-sponsored health coverage and rising awareness of home-based care benefits. Many private insurance plans now reimburse services such as skilled nursing, rehabilitation, and remote monitoring. Growing preference for personalized and cost-effective treatment, along with expanded insurance plans covering chronic disease management and post-acute care, further support strong demand from the private insurance segment.

The out-of-pocket segment held a 17% of the U.S. home healthcare market share due to increasing demand for immediate and flexible access to care without insurance restrictions. Many patients pay directly for services such as personal caregiving, unskilled support, and additional rehabilitation not fully covered by insurance. Rising elderly populations, growing preference for personalized home care, and gaps in reimbursement coverage are further driving reliance on out-of-pocket payments, supporting segment growth.

")

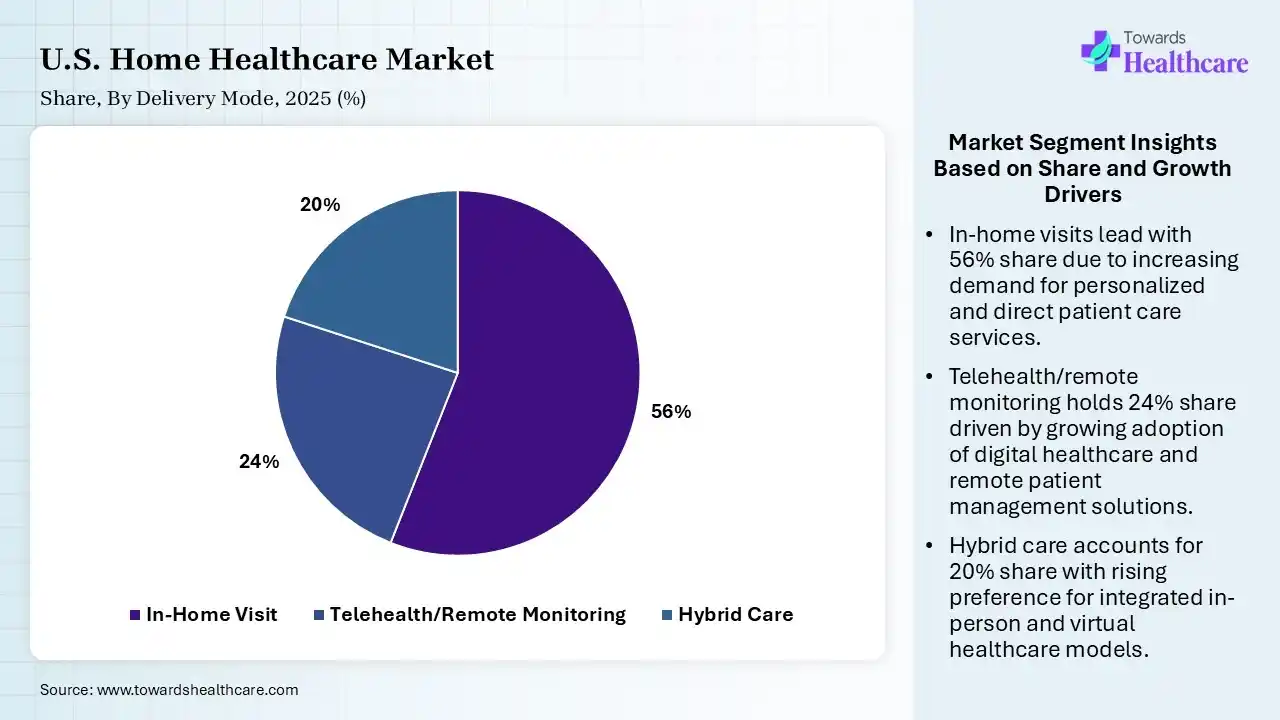

| Segment | Share 2025 (%) |

| In-Home Visit | 56% |

| Telehealth/Remote Monitoring | 24% |

| Hybrid Care | 20% |

The In-Home Visit Segment Dominated the U.S. Home Healthcare Market in 2025

The in-home visit segment held a dominant share of 56% in 2025 due to strong patient preference for receiving care in the comfort of their homes. It enables personalized treatment, continuous monitoring, and better patient-caregiver interaction, especially for elderly and chronically ill individuals. Additionally, reduced hospital visits, lower healthcare costs, and improved accessibility to skilled professionals further support the widespread adoption of in-home visit services across the country.

The telehealth/remote monitoring segment held the second-largest share of 24% in 2025 and is estimated to grow at the highest growth rate of 10.20% during 2026-2035 due to the rising use of remote patient monitoring devices and wearable technologies. These solutions enable continuous tracking of vital signs, early detection of health issues, and timely medical intervention. The growing prevalence of chronic diseases, aging population, and preference for non-invasive, home-based care further drive adoption. Additionally, improved digital health infrastructure supports segment expansion.

The hybrid care segment held a 20% of the U.S. home healthcare market share due to the growing need for a combination of in-person visits and remote monitoring. This model offers greater flexibility, continuous patient engagement, and improved care coordination between healthcare providers and patients. Rising chronic disease burden, increasing adoption of digital health tools, and preference for cost-effective, personalized care are further driving the shift towards hybrid home healthcare solutions.

The global home healthcare market size was estimated at USD 226.92 billion in 2025 and is predicted to increase from USD 246.44 billion in 2026 to approximately USD 517.81 billion in 2035, expanding at a CAGR of 8.6% from 2026 to 2035.

Clinical Trials

Regulatory Approvals

U.S. home healthcare regulation involves two main areas: licensing for care providers and approval of medical devices used at home. Agencies must obtain state-level licenses, meet Medicare/Medicaid certification requirements, and follow CMS standards, while home-use medical devices must be cleared or approved by the FDA. Key players: Centers for Medicare & Medicaid Services, U.S. Food and Drug Administration, McKesson Corporation, Medtronic plc, Baxter International Inc.

Patient Support and Services

| Companies | Headquarters | Offerings |

| McKesson Medical-Surgical, Inc. | Richmond, Virginia, USA. | Medical-surgical supplies, home healthcare equipment distribution, wound care products, and respiratory supplies for home and post-acute care settings. |

| NxStage Medical (Fresenius Medical Care) | Lawrence, Massachusetts, USA. | Home hemodialysis systems, portable dialysis machines, and renal care solutions for chronic kidney disease patients. |

| Medline Industries Inc. | Northfield, Illinois, USA. | Medical supplies, personal protective equipment, wound care products, and home healthcare consumables. |

| Medtronic plc | Dublin, Ireland. | Advanced medical devices, infusion therapy systems, cardiac care devices, and remote patient monitoring technologies. |

| Kindred Healthcare LLC | Louisville, Kentucky, USA. | Home health services, rehabilitation care, and long-term acute care services. |

| Brookdale Senior Living Inc. | Brentwood, Tennessee, USA. | Senior living services, assisted living, memory care, and home-based supportive care services. |

| Sunrise Senior Living LLC | McLean, Virginia, USA | Assisted living, memory care, skilled nursing support, and in-home senior care services. |

Strengths

Weaknesses

Opportunities

Threats

By Component

By Indication

By Service Type

By Payer

By Delivery Mode

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar