")

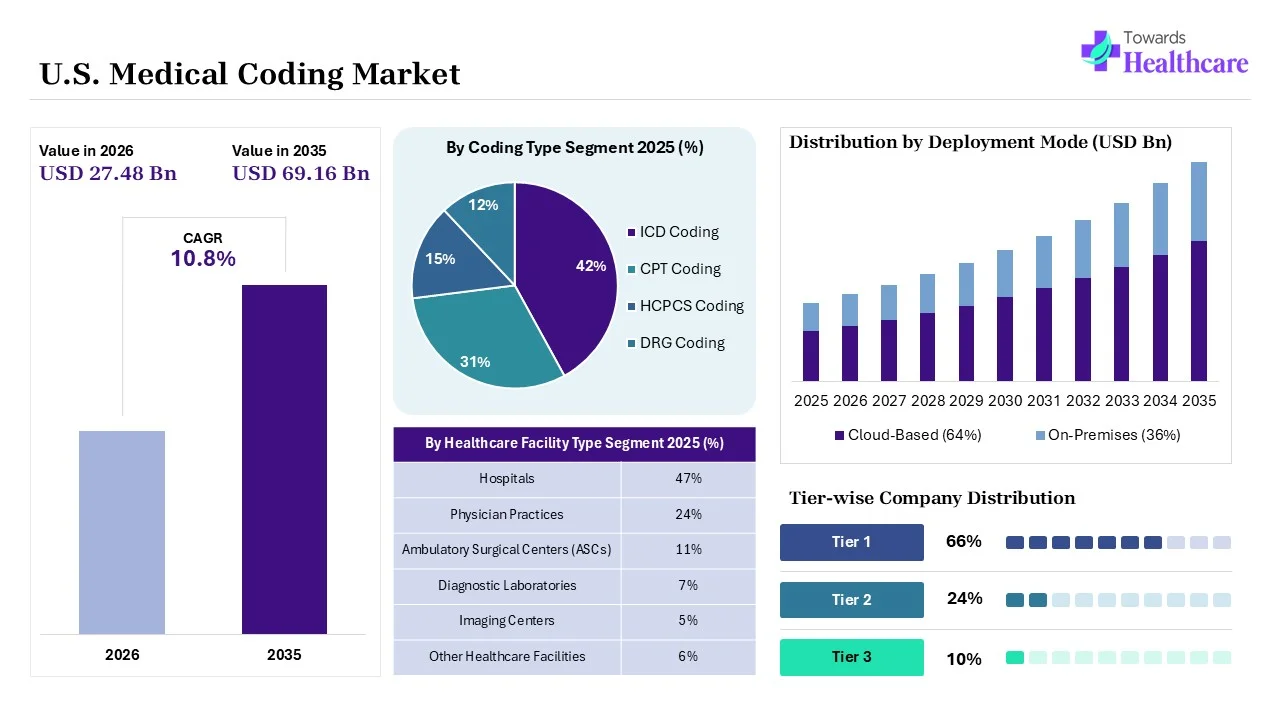

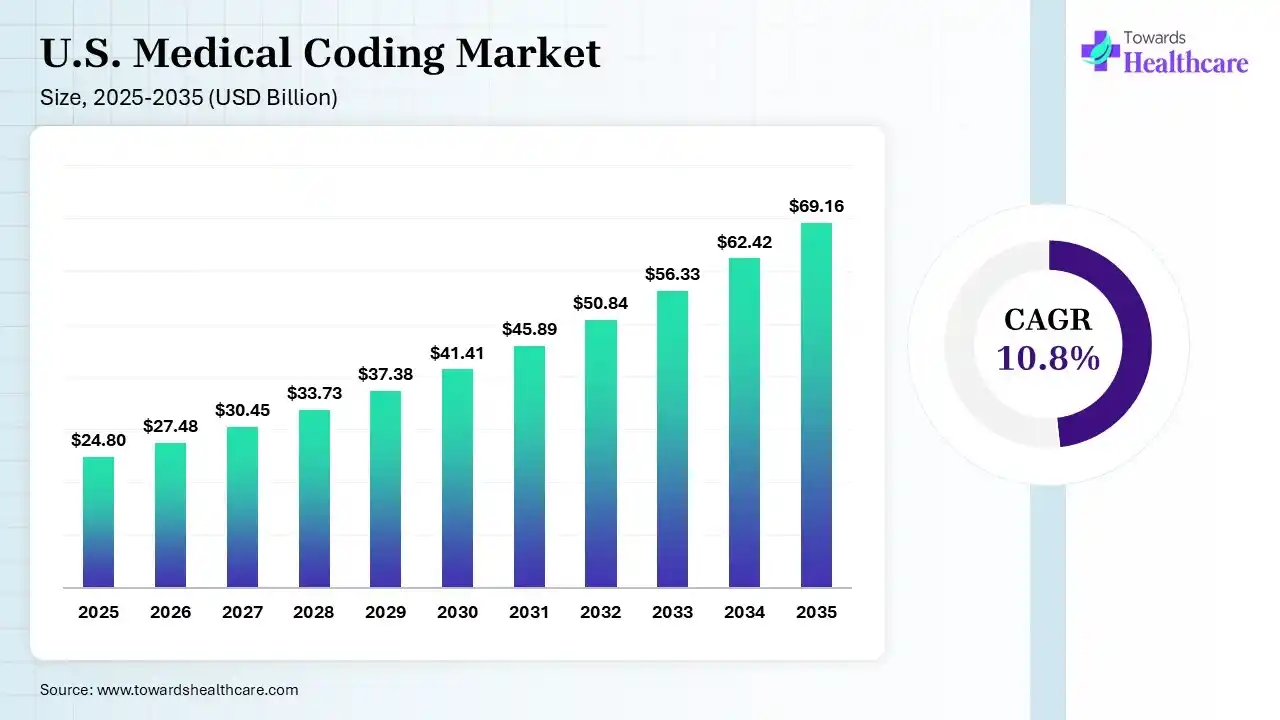

The U.S. medical coding market size was valued at US$ 24.8 billion in 2025 and is projected to grow to 27.48 billion in 2026. Forecasts suggest it will reach approximately US$ 69.16 billion by 2035, registering a CAGR of 10.8% during the period.

")

Medical coding is the process of converting healthcare diagnoses, procedures, medical services, and equipment into standardized alphanumeric codes. These codes are taken from systems such as ICD (International Classification of Diseases), CPT (Current Procedural Terminology), and HCPCS (Healthcare Common Procedure Coding System). It ensures uniform communication between the healthcare providers, insurance companies, and regulatory bodies for accurate documentation and billing.

Medical coding plays a vital role in maintaining consistency, accuracy, and transparency of records. It helps in processing insurance claims and determining reimbursement. It helped in processing insurance claims, determining reimbursements, and supporting compliance with healthcare regulations. By standardizing clinical information, medical coding also enables better data analysis, reporting, and decision-making within healthcare systems.

The U.S. medical coding market is growing due to rising healthcare service volume, increasing complexity of medical billing, and strict compliance requirements like ICD-10 updates. The shift towards value-based care, growing demand for accurate reimbursement, and adoption of AI-driven and automated coding solutions are further driving market expansion.

Macro Factors

Micro Factors

Artificial intelligence is significantly impacting the market by automating code assignment, reducing manual errors, and improving coding accuracy. AI-powered natural language processing (NLP) can analyze clinical documentation in real time, accelerating claim submissions and reimbursement cycles. It also enhances productivity, lowers operational costs, supports regulatory compliance, and enables healthcare organizations to manage growing volumes of patient data more efficiently.

Increasing Shift Toward Outsourced Coding Services

Healthcare providers are increasingly outsourcing medical coding functions to specialized vendors to reduce costs, improve coding accuracy, and address skilled workforce shortages. This trend is expected to strengthen as hospitals and clinics focus on core patient care activities while ensuring efficient revenue cycle management.

Growing Adoption of Cloud-Based Coding Platforms

Cloud-based medical coding solutions are gaining popularity due to their flexibility, scalability, and remote accessibility. These platforms support seamless data sharing, improve workflow efficiency, and enable healthcare organizations to manage coding operations more effectively while maintaining regulatory compliance and data security.

Rising Focus on Regulatory Compliance and Coding Accuracy

As healthcare regulations and reimbursement requirements become more complex, organizations are placing greater emphasis on coding accuracy and compliance. Future growth will be supported by continuous updates to coding standards, enhanced audit processes, and investments in training programs to reduce claim denials and reimbursement delays.

| Table | Scope |

| Market Size in 2026 | USD 27.48 Billion |

| Projected Market Size in 2035 | USD 69.16 Billion |

| CAGR (2026 - 2035) | 10.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Component, By Coding Type, By Deployment Mode, By Healthcare Facility Type, By End User, By Application, By Technology |

| Top Key Players | Optum, 3M Health Information Systems, Aviacode, GeBBS Healthcare Solutions, Dolbey, CorroHealth, Streamline Health Solutions |

")

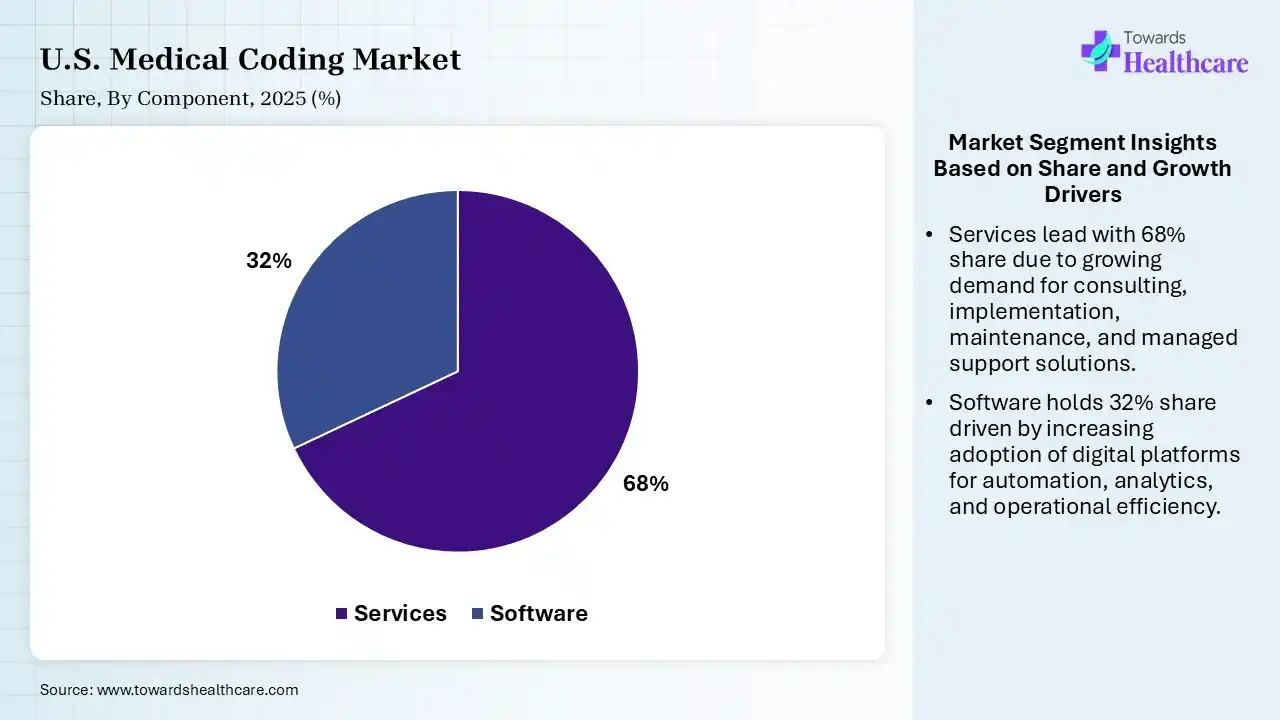

| Segment | Share 2025 (%) |

| Services | 68% |

| Software | 32% |

The Services Segment Dominated the U.S. medical coding Market in 2025

The services segment held a dominant share of 68% in 2025 due to the growing need for accurate coding, regulatory compliance, and efficient claims management. Healthcare providers increasingly rely on outsourced coding, auditing, training, and consulting services to reduce claim denials and administrative burden. The shortage of skilled coders and the complexity of reimbursement requirements further strengthened the demand for specialized medical coding services.

The software segment held the second-largest share of 32% in 2025 and is expected to grow at the fastest CAGR of 12.40% in the U.S. medical coding market during the forecast period due to increasing adoption of automated coding solutions, cloud-based platforms, and integrated healthcare IT systems. A healthcare organization is investing in advanced coding software to improve accuracy, streamline workflows, reduce administrative costs, and support compliance requirements. Growing digitization and demand for efficient revenue cycle management are further accelerating software adoption.

")

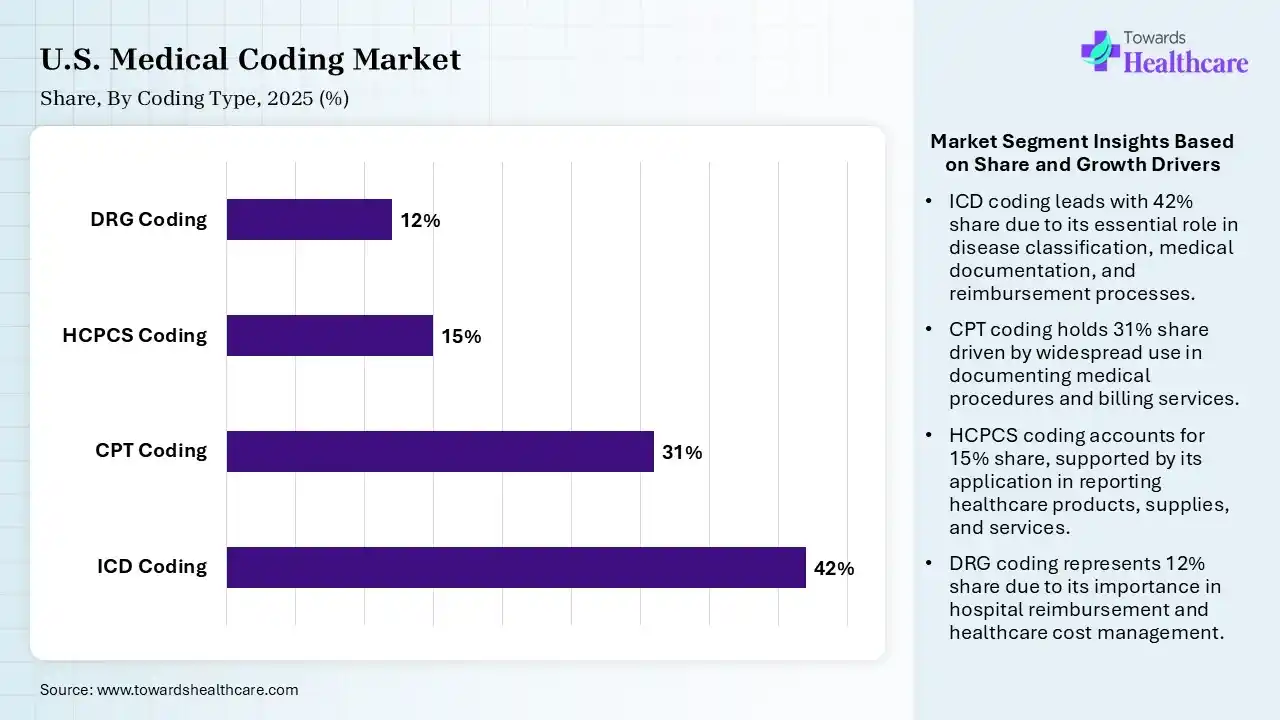

| Segment | Share 2025 (%) |

| ICD Coding | 42% |

| CPT Coding | 31% |

| HCPCS Coding | 15% |

| DRG Coding | 12% |

The ICD Coding Segment led the U.S. medical coding Market in 2025 with the Largest Share

The ICD coding segment held a dominant share of 42% in 2025 because it serves as the foundation for documenting diagnoses, disease classification, and healthcare reporting. ICD codes are mandatory for insurance claims, reimbursement processes, and regulatory compliance across healthcare facilities. The growing prevalence of chronic diseases, increasing patient encounters, and continuous updates to coding standards further drive the widespread adoption of ICD coding services.

The CPT coding segment held the second-largest share of 31% in 2025 because it is essential for documenting and billing medical procedures and physician services. Widespread use of CPT codes for outpatient care, diagnostic testing, and reimbursement claims drives demand. The increasing volume of healthcare services, growing physician visits, and the need for accurate procedures-based continuous support to segment growth.

The HCPCS coding segment held a 15% market share due to the increasing utilization of medical equipment, supplies, pharmaceuticals, and outpatient healthcare services across the U.S. healthcare system. HCPCS codes are essential for Medicare, Medicaid, and private insurance reimbursement of non-physician services and products. Growing demand for home healthcare, durable medical equipment, and specialized treatment is further driving the adoption of HCPCS coding services.

The DGR coding segment held a 12% share in 2025 and is expected to grow at the fastest CAGR of 11.80% in the U.S. medical coding market during the forecast period due to its critical role in inpatient reimbursement and hospital payment systems. Increasing hospital admissions, rising focus on cost control, and the adoption of value-based care models are driving demand for accurate DGR coding. Healthcare providers are increasingly investing in DGR optimization to improve reimbursement accuracy, operational efficiency, and regulatory compliance.

")

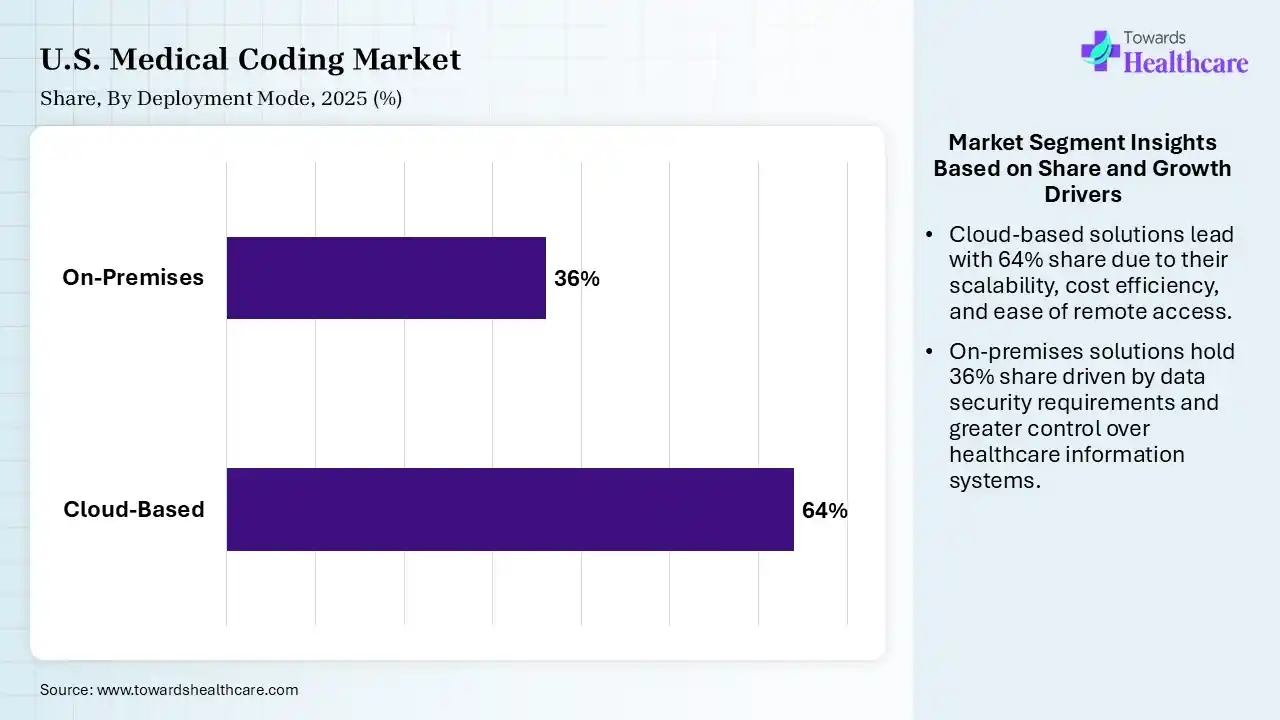

| Segment | Share 2025 (%) |

| Cloud-Based | 64% |

| On-Premises | 36% |

The Cloud-based Segment Led the U.S. Medical Coding Market in 2025 with the Largest Share

The cloud-based segment led the market with a share of 64% in 2025 and is expected to grow at the fastest CAGR of 13.10% in the market during the forecast period due to its ability to provide remote access, seamless data sharing, and scalable operations. Healthcare organizations increasingly prefer cloud platforms for their lower infrastructure costs, faster implementation, and easier integration with EHR and revenue cycle management systems. Enhanced data security, real-time updates, and support for multi-location healthcare networks further contribute to the segment’s dominance.

The on-premises segment held the second-largest share of 36% in 2025 due to its strong data security, greater control over sensitive patient information, and compliance with strict healthcare regulations. Large hospitals and healthcare systems often prefer on-premises deployments to manage complex workflows and maintain customized IT infrastructures. Existing investments in legacy systems and concerns about data privacy continue to support the segment’s substantial market presence.

")

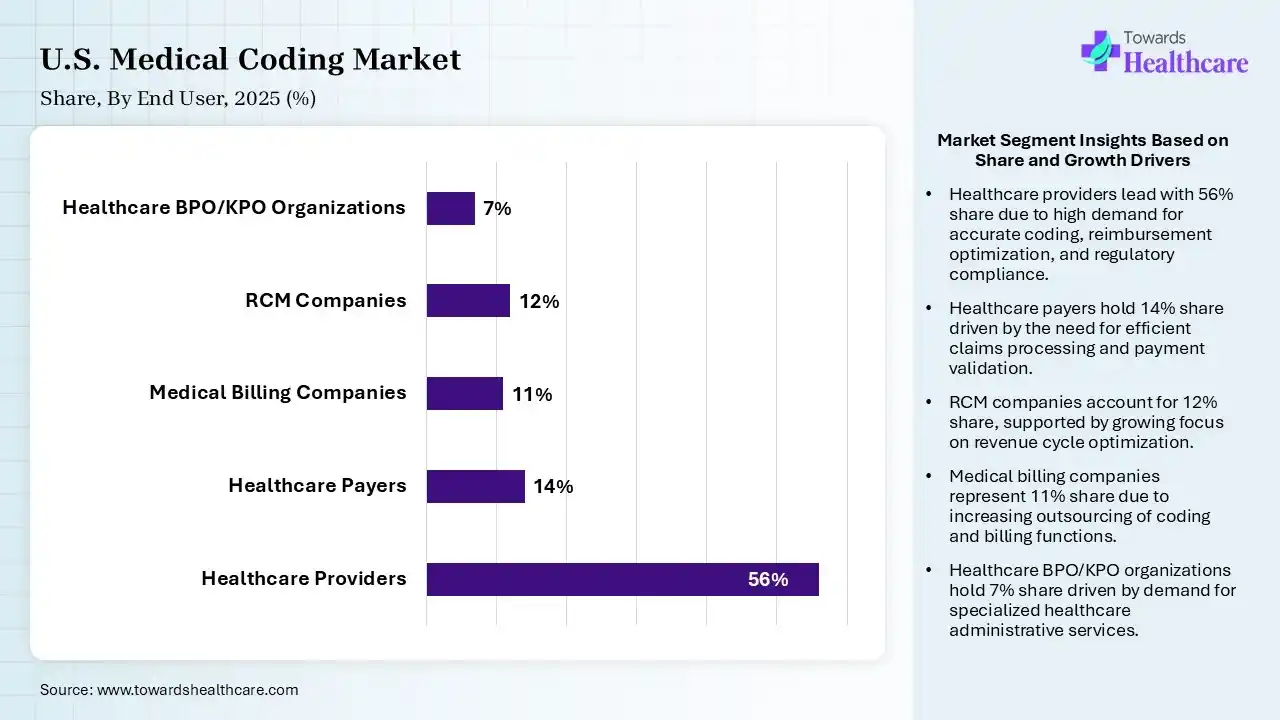

| Segment | Share 2025 (%) |

| Healthcare Providers | 56% |

| Healthcare Payers | 14% |

| Medical Billing Companies | 11% |

| RCM Companies | 12% |

| Healthcare BPO/KPO Organizations | 7% |

The Healthcare Providers Segment Led the Market in 2025 with the Largest Share

The healthcare providers segment dominated the U.S. medical coding market with a share of 56% in 2025 because hospitals, clinics, and physician practices generate a large volume of patient records that require accurate coding for billing and reimbursement. Increasing patient visits, complex treatment procedures, and stringent regulatory requirements drive continuous demand for coding services. Additionally, providers rely heavily on medical coding to optimize revenue cycle management, reduce claim denials, and ensure compliance.

The healthcare payers segment held the second-largest share of 14% in 2025 due to its critical role in claims processing, reimbursement verification, and fraud prevention. Insurance companies rely on accurate medical coding assess coverage, manage costs, and ensure regulatory expenditure, and the need for efficient payment management continuous to drive the need for efficient payment management to drive the adoption of medical coding solutions among healthcare payers.

The RCM companies segment held a 15% market share as healthcare organizations increasingly seek solutions to optimize billing, coding, claims processing, and reimbursement management. Rising healthcare costs, growing claim volumes, and the need to minimize revenue leakage are driving demand for specialized RCM services. Additionally, increasing regulatory complexities and the focus on improving financial performance are encouraging healthcare providers to partner with RCM companies.

The healthcare BPO/KPO organizations segment held a 7% share in 2025 and is expected to grow at the fastest CAGR of 12.80% in the U.S. medical coding market during the forecast period due to the increasing outsourcing of coding and revenue cycle management functions by healthcare providers and payers. These organizations offer cost-effective services, access to skilled coding professionals, and scalable operational support. Growing pressure to improve efficiency, reduce administrative costs, and ensure coding accuracy is further accelerating demand for specialized outsourcing services.

")

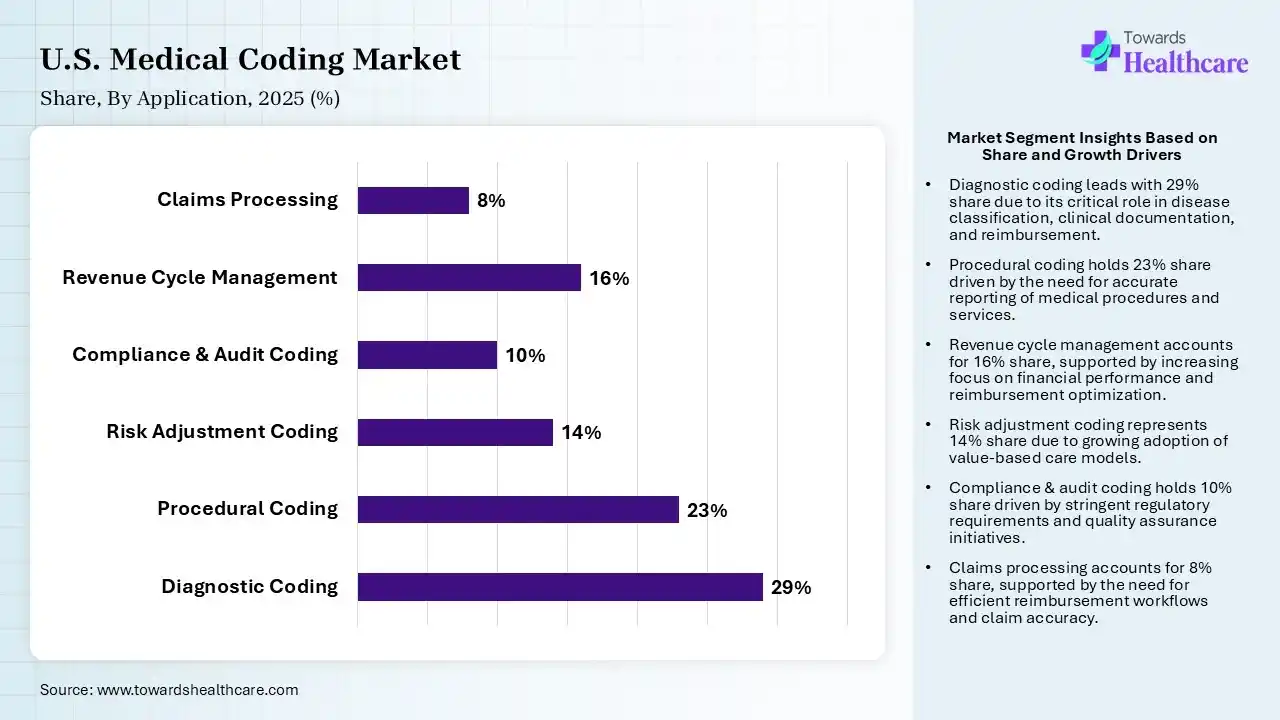

| Segment | Share 2025 (%) |

| Diagnostic Coding | 29% |

| Procedural Coding | 23% |

| Risk Adjustment Coding | 14% |

| Compliance & Audit Coding | 10% |

| Revenue Cycle Management | 16% |

| Claims Processing | 8% |

The Diagnostic Coding Segment Led the U.S. Medical Coding Market in 2025 with the Largest Share

The diagnostic coding segment held a dominant share of 29% in 2025 because it is fundamental to documenting patients' diagnoses, determining treatment pathways, and processing insurance claims. Every healthcare encounter requires accurate diagnosis coding for reimbursements, regulatory compliance, and medical record management. The increasing prevalence of chronic diseases, rising patient volumes, and growing demand for precise clinical documentation continue to drive the widespread use of diagnostic coding services.

The procedural coding segment held the second-largest share of 23% in 2025 due to its critical role in documenting and billing medical procedures, surgeries, diagnostic tests, and therapeutic services. Healthcare providers rely on accurate procedure coding to ensure proper reimbursement and regulatory compliance. The increasing volumes of outpatient services, surgical intervention, and specialized treatments, coupled with growing healthcare expenditure, continue to drive strong demand for procedure coding solutions.

The compliance & audit coding segment held a 15% market share due to increasing regulatory scrutiny and the growing need to ensure coding accuracy across healthcare organizations. Providers and payers are investing in audit and compliance programs to reduce claim denials, prevent fraud, and avoid financial penalties. The rising complexity of coding standards, reimbursement policies, and documentation requirements is further driving demand for compliance and audit coding services.

The risk adjustment coding segment held a 14% share in 2025 and is expected to grow at the fastest CAGR of 13.20% in the U.S. medical coding market during the forecast period due to the increasing adoption of value-based care and Medicare Advantage plans. Accurate risk adjustment coding helps healthcare organizations capture patient complexity, optimize reimbursement, and improve care management. Rising focus on population health management, regulatory compliance, and financial performance is further accelerating demand for specialized risk adjustment coding services.

The market is experiencing strong growth due to rising patient volumes, increasingly complexity of healthcare billing systems, and stringent regulatory requirements. Healthcare providers are increasingly adopting advanced coding solutions to improve reimbursement accuracy, reduce claim denials, and streamline revenue cycle management. Furthermore, the expansion of electronic health records (EHRs), growing healthcare expenditure, and the shift towards value-based care models are creating sustained demand for efficient and compliant medical coding services across the healthcare industry.

| Companies | Headquarters | Offerings |

| Optum | Eden Prairie | Medical coding services, revenue cycle management, claims processing, healthcare analytics, and coding automation solutions |

| 3M Health Information Systems | St. Paul | Computer-assisted coding (CAC), clinical documentation improvement (CDI), coding software, and healthcare data management |

| Aviacode | Salt Lake City | Professional and facility coding, coding audits, compliance services, and coder education |

| GeBBS Healthcare Solutions | Culver City | Medical coding, risk adjustment coding, auditing, revenue cycle management, and consulting services |

| Dolbey | Concord | Computer-assisted coding, clinical documentation improvement, speech recognition, and workflow solutions |

| CorroHealth | Plano | Medical coding, clinical documentation review, risk adjustment, and revenue cycle solutions |

| Streamline Health Solutions | Atlanta | Coding optimization, CDI solutions, revenue integrity, and healthcare |

In April 2026, "We believe her extensive background in helping scale revenue cycle and healthcare technology organizations across both commercial and operating functions, and her deep experience in the provider market, make her exceptionally well-suited to lead Nym through this next chapter," said Rotem Shacham, Director at PSG.

By Component

By Coding Type

By Deployment Mode

By Healthcare Facility Type

By End User

By Application

By Technology

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar