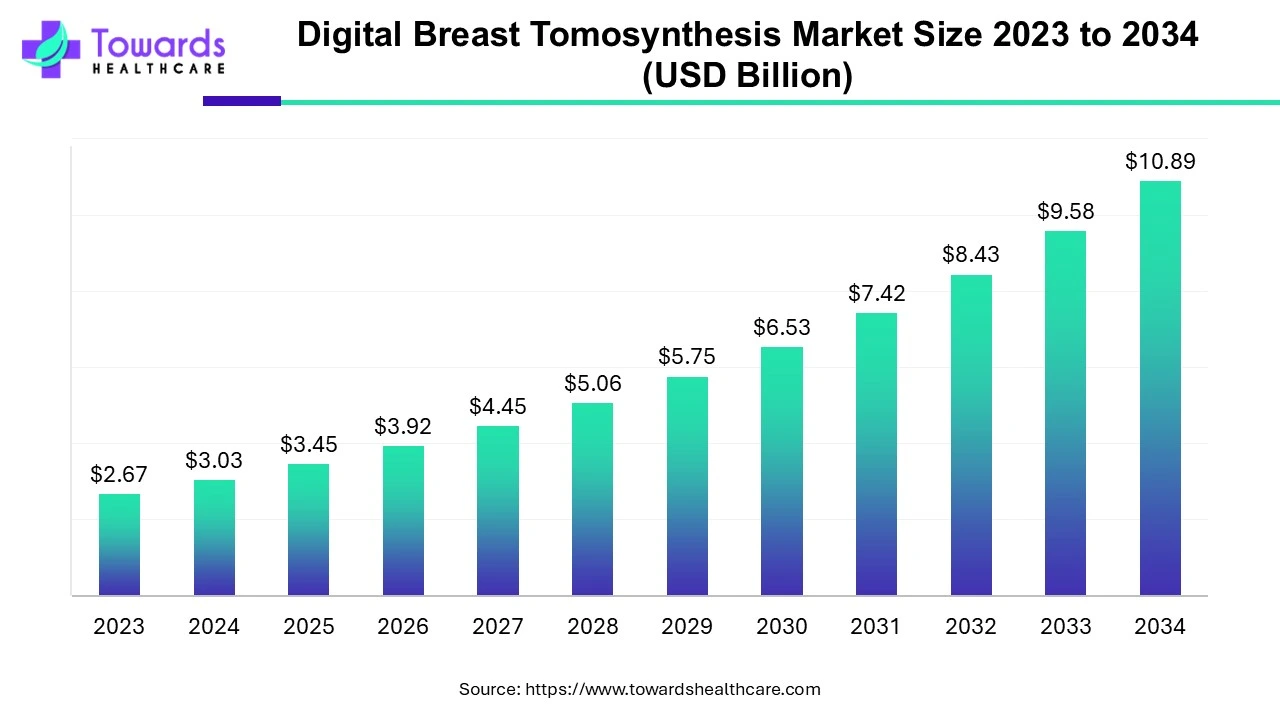

The global digital breast tomosynthesis market size is calculated at USD 3.45 billion in 2025, grew to USD 3.92 billion in 2026, and is projected to reach around USD 12.38 billion by 2035. The market is expanding at a CAGR of 13.63% between 2026 and 2035. The rising incidences of breast cancer, technological advancements, and favorable government initiatives drive the market.

")

Tomo mammography (3D mammogram) or digital breast tomosynthesis (DBT) is an advanced form of medical imaging to detect breast cancer. It can help detect early signs of breast cancer in women with no symptoms and in women with dense breasts. It shows superior benefits over standard mammograms, such as the detection of hidden tumors, greater accuracy in pinpointing the cancer, and clearer images of breast abnormalities. It takes multiple pictures of the breast from different angles using an X-ray arc. These pictures are reconstructed or synthesized to form a set of 3D images. Thus, DBT reduces the chances of false positive results.

The increasing incidences of breast cancer necessitate detecting breast cancer, boosting the market. It is estimated that around half of all the women and people assigned female at birth have dense breasts. Tumors in denser breasts are more difficult to detect in a standard 2D mammogram, increasing the demand for DBT. The advent of advanced technologies drives the latest innovations in medical imaging. The increasing investments and favorable government policies to combat breast cancer also potentiate the market.

Artificial intelligence (AI) can transform the way breast cancer is diagnosed using DBT. AI simplifies the task of radiologists and clinicians to detect breast cancer, reducing manual errors. AI and machine learning (ML) with computer-aided detection help healthcare professionals with effective disease prediction and image segmentation. Some AI algorithms have been shown to match the performance of radiologists. Thus, this significantly reduces the time taken for detection, enhancing precision. AI and ML can even detect minute abnormalities in breast tissue, reducing the overall load on radiologists. Additionally, AI can introduce automation in medical imaging techniques. Hence, AI enhances diagnostic accuracy in DBT and reduce recall rates, presenting future growth opportunities for the market.

Driver

Increasing Awareness

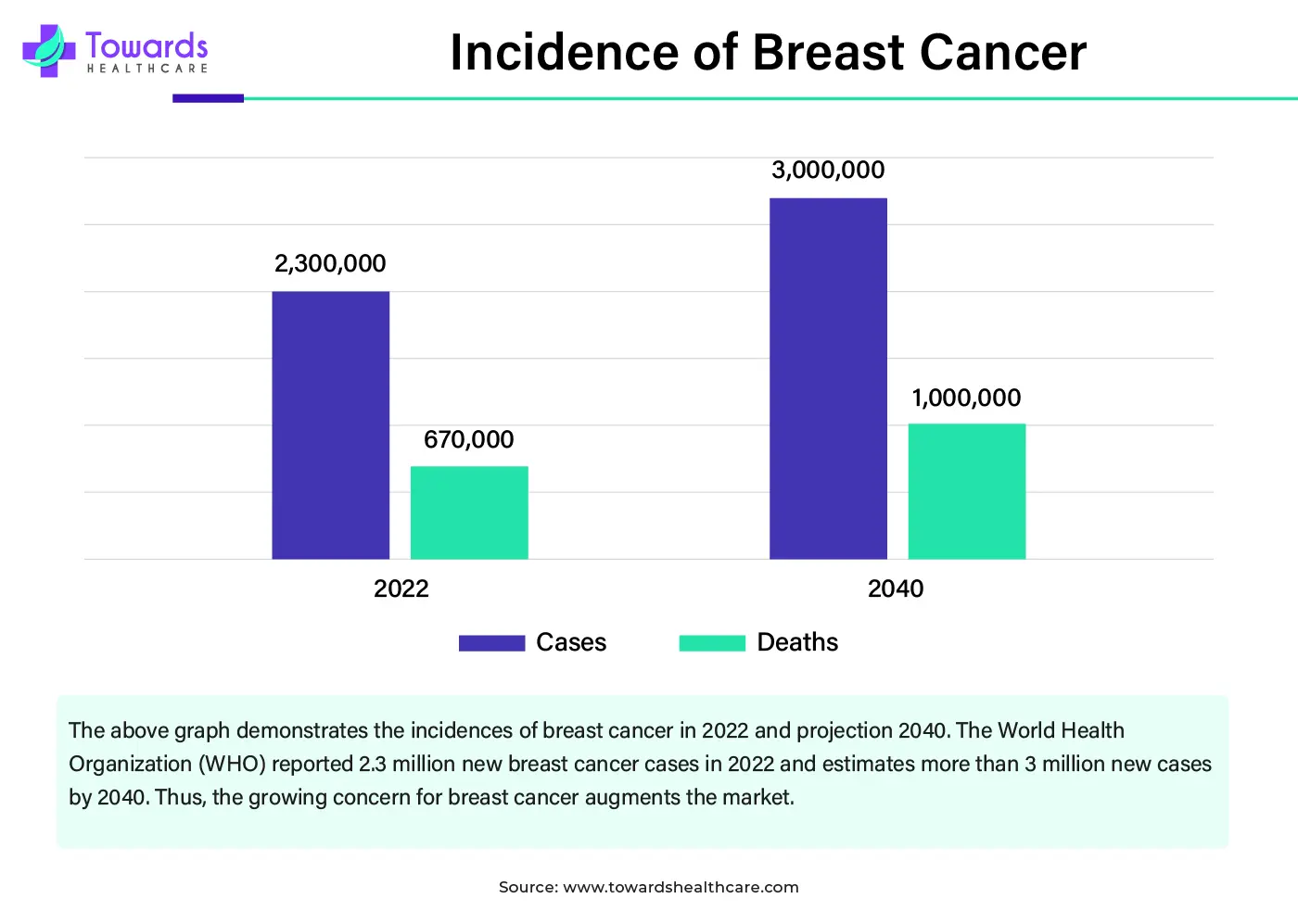

The major growth factor of the digital breast tomosynthesis market is increasing awareness about early detection of breast cancer. Breast cancer is the most common type of cancer among women and one of the leading causes of death. Several government organizations release initiatives and guidelines to increase awareness among common people, especially in low- and middle-income countries. The World Health Organization (WHO) released a new “Global Breast Cancer Initiative Framework,” providing a roadmap to attain the target to save 2.5 million lives by 2040. The WHO also encourages other countries to implement the three pillars of health promotion for early detection, timely diagnosis, and comprehensive management. Apart from these, numerous government and private research institutions organize seminars, conferences, and symposiums to increase awareness. Hence, these measures potentiate the need for tomosynthesis equipment.

Restraint

High Installation Cost

The major challenge faced by the market is the high installation cost of the equipment. The average cost of DBT ranges from $150,000 to $300,000, limiting the affordability of several companies in underdeveloped and developing countries. Other than the installation cost, maintenance costs are also high. Numerous people from low- and middle-income groups also find it difficult to afford breast cancer screening tests as they range from $99 to $359, restricting market growth.

Opportunity

Growing Adoption

The future of the digital breast tomosynthesis market is promising, driven by the growing adoption of the equipment. Several hospitals and other healthcare organizations have increased the adoption and installation of DBT due to increasing breast cancer cases. The rising investments by several government and private organizations promote the adoption of DBT. Healthcare companies and start-ups raise funding from venture capitalists to develop novel equipment. Advancements in technology, such as AI and ML, introduce the latest features in DBT, enhancing its demand. The rising adoption of DBT in healthcare organizations allows them to offer advanced care and diagnostic solutions to patients. The increasing awareness for breast cancer screening and early detection is also a major growth factor to promote installing DBT. All these efforts increase DBT's sales, fueling market growth.

| Table | Scope |

| Market Size in 2026 | USD 3.92 Billion |

| Projected Market Size in 2035 | USD 12.38 Billion |

| CAGR (2026 - 2035) | 13.63% |

| Leading Region | North America by 41% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By End-Use, By Region |

| Top Key Players | Adaptix, Ltd., DMS Imaging, Fujifilm, GE Healthcare, Guangzhou Ysenmed Co. Ltd., Hologic, IMS Giotto S.p.A., Philips Healthcare, Planmed Oy, Siemens Healthineers, Sino Medical Device Technology Co. Ltd., Volpara Health Technologies Ltd. |

| Segments | Shares % |

| Standalone 3D Systems | 62% |

| 2D/3D Combination Systems | 38% |

Standalone 3D Systems Dominated

By product, the standalone 3D systems segment held a dominant presence with the share of 62% in the digital breast tomosynthesis market in 2025. Standalone 3D systems generate high-quality and high-resolution 3D images of breast tumors. 3D systems are widely preferred as they are more accurate and can detect 20% to 65% of more invasive breast cancers compared to 2D systems. Technological advancements such as AI present advanced features in DBT, enhancing precision. 3D systems are beneficial for women with dense breasts and detect hidden tumors that are otherwise not visible through 2D systems. Thus, these systems increase cancer detection rates and decrease recall and false positives.

2D/3D Combination Systems: Fastest-Growing

By product, the 2D/3D combination systems segment is expected to grow at the fastest rate in the digital breast tomosynthesis market during the forecast period. 2D/3D combination systems offer benefits of both 2D and 3D systems, presenting more opportunities for efficient cancer detection. It can capture both 2D mammograms and 3D images of the breast tissue, enabling healthcare professionals to reduce errors during examination. The major limitation of a 3D system is a higher irradiation dose, which can be overcome through combination systems. This leads to shorter examination times and reduced compression, improving patient comfort. In addition, the interpretation of microcalcifications and masses is easier. All these features and benefits are likely to increase the demand for combination systems over the years.

| Segments | Shares % |

| Hospitals | 68% |

| Diagnostic Centers | 25% |

| Others | 7% |

Hospitals Segment Led in 2025

By end-use, the hospitals segment led the global digital breast tomosynthesis market by 68% share in 2025. The segmental growth is attributed to favorable infrastructure and suitable capital investments. Hospitals have professionals from multiple departments, providing expertise from all aspects to patients. Favorable reimbursement policies also increase the number of hospital admissions of breast cancer patients. Moreover, hospitals follow stringent regulatory guidelines, providing enhanced care. Several hospitals also organize awareness campaigns to promote early detection and screening of breast cancer.

Diagnostic Centers: Fastest-Growing

By end-use, the diagnostic centers segment is anticipated to grow with the highest CAGR in the digital breast tomosynthesis market during the studied years. Diagnostic centers adopt a wide range of specialized equipment for diagnosing various types of diseases. The presence of advanced equipment, increasing investments, and the rising number of diagnostic centers propel the segment’s growth. There are around 72 NCI-designated Cancer Centers in the U.S.

North America held the largest share of the digital breast tomosynthesis market with share of 41% in 2025. The presence of key players, technological advancements, and favorable government support drive the market. Key players like Philips Healthcare, GE Healthcare, and Hologic hold a major share of the North American market. The Centers for Disease Control and Prevention works with public, non-profit, and private partners to address breast cancer in women younger than 45 years of age.

U.S. Market Trends

The growing adoption of DBT in the U.S. and Canadian healthcare organizations potentiates the market. There are around 26,045 mammography systems in service in the U.S., out of which 12,442 are digital breast tomosynthesis. Favorable regulatory policies support the development of DBT in North America. Furthermore, increasing investments also promote the market. The government of Canada announced an investment of $545,000 for two initiatives aiming to advance research and raise awareness of breast cancer screening.

Asia-Pacific is anticipated to grow at a significant rate in the digital breast tomosynthesis market by 20% share during the forecast period. The rising incidences of breast cancer, increasing awareness, and the burgeoning healthcare sector drive the market. It is estimated that breast cancer cases will increase by 50,000 annually this decade in India. While in China, around 350,000 new breast cancer cases are estimated to be diagnosed annually. Government initiatives have accelerated cancer research in Asia-Pacific countries, potentiating the need for early detection. The Indian Government announced an increase of Rs. 4,000 crore in funding for the National Health Mission from the union budget for FY2024-25. The increasing public-private partnerships and mergers & acquisitions promote the development and adoption of DBT. Several government and private organizations conduct conferences and workshops to increase awareness about breast cancer screening and train individuals to use advanced DBT.

For instance,

The European Digital Breast Tomosynthesis (DBT) market by 26% share is rapidly expanding as it transitions from 2D to 3D systems. This growth is driven by increasing cancer rates, more frequent screenings, and supportive AI imaging regulations. Western European healthcare systems are upgrading to higher-resolution 3D imaging, while Eastern Europe is utilizing COVID recovery funds for these purchases. DBT gantries are replacing Full-Field Digital Mammography (FFDM) systems across Europe to improve diagnostic quality. The increase in breast cancer screening programs, particularly for women with dense breast tissue, is propelling this shift. DBT's ability to reduce false positives and enhance radiologists' diagnostic confidence is a significant advantage in the European market.

Germany Market Trends

Germany's market is growing, bolstered by its status as Europe's leading mammography market with digital systems. Key drivers include government-funded screening programs for women aged 50-69, the adoption of 3D technology, and significant hospital investments in AI-driven diagnostic imaging. Regulatory approvals from the German Federal Joint Committee (G-BA) and EU reforms promoting early detection are fostering investment in advanced imaging tools. Organized screenings for women aged 50-69 occur every two years, funded by public health insurance, improving access to advanced systems. The shift from traditional 2D mammography to superior 3D imaging (DBT) is fueled by better cancer detection in dense breast tissue. Increased awareness of breast cancer and the importance of early detection are accelerating adoption to reduce mortality, further supported by AI technologies that enhance diagnostic speed and accuracy.

Dana Brown, President and CEO of iCAD commented that the FDA clearance of ProFound Detection Version 4.0 sets a new benchmark in cancer detection, especially in the most challenging cases where accurate and early detection is critical. She added that this advancement strengthens their competitive position and represents a powerful driver for long-term growth.

Strengths

• Digital Breast Tomosynthesis (DBT) provides 3D images that significantly improve the detection of lesions, particularly in dense breast tissue, while also reducing the number of false-positive recalls compared to traditional 2D mammography.

• The use of advanced imaging technologies, often alongside 2D systems, is becoming the standard of care, supported by major contributions from top companies like Hologic and GE Healthcare.

• Strong government backing for mammography screening programs and regulatory approvals, such as those from the FDA, helps promote the use of this technology.

Weaknesses

• The high costs of DBT equipment can hinder its use in smaller healthcare facilities and in developing areas.

• Additionally, the need for specialized training for technicians, along with the extra time radiologists must spend interpreting three-dimensional images instead of two-dimensional ones, creates more challenges.

• Producing multiple images requires more data storage and an improved IT infrastructure.

Opportunities

• The use of Artificial Intelligence in this area could improve screening efficiency, speed up diagnostic processes, and reduce the workload for radiologists.

• Furthermore, the increasing healthcare spending in the Asia-Pacific region, especially in countries like India and China, offers significant growth opportunities due to greater awareness of screening practices.

• There is also ongoing work to develop faster, portable, and lower-dose tomosynthesis systems.

Threats

• However, new competition could come from improvements in breast MRI, molecular breast imaging, or automated ultrasound technologies.

• Inconsistent insurance coverage and reduced reimbursement rates for new technologies in some regions might limit growth opportunities.

• Additionally, changes in regulatory rules or trade tariffs could affect supply chains and restrict market access.

By Product

By End-Use

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar