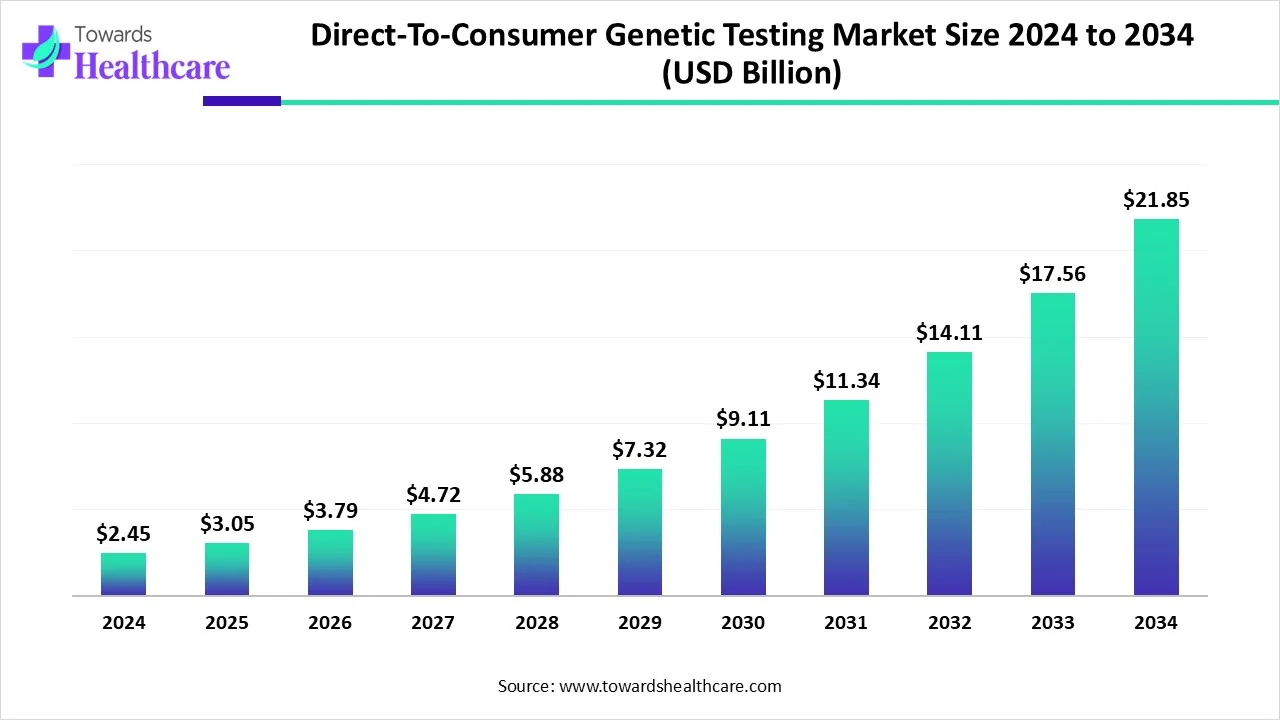

The global direct-to-consumer genetic testing market size is calculated at USD 3.05 billion in 2025, grew to USD 3.79 billion in 2026, and is projected to reach around USD 27.15 billion by 2035. The market is expanding at a CAGR of 24.44% between 2026 and 2035.

Direct-to-consumer genetic testing (DTC-GT) provides as well as advertises genetic testing by companies without the help of conventional healthcare systems directly to consumers. Here, the biological samples, such as blood samples, saliva, or cells from a cheek swab, that contain DNA are collected by the consumers and sent to the DTC-GT company. The DTC-GT company then conducts various tests for identifying genetically related information, pharmacogenomics, genetic health risks, and cancer risks. Depending upon the regulations surrounding DTC-GT, consumers can apply to DTC-GT outside of their country. Furthermore, it also helps in screening single-gene and multifactorial gene disorders.

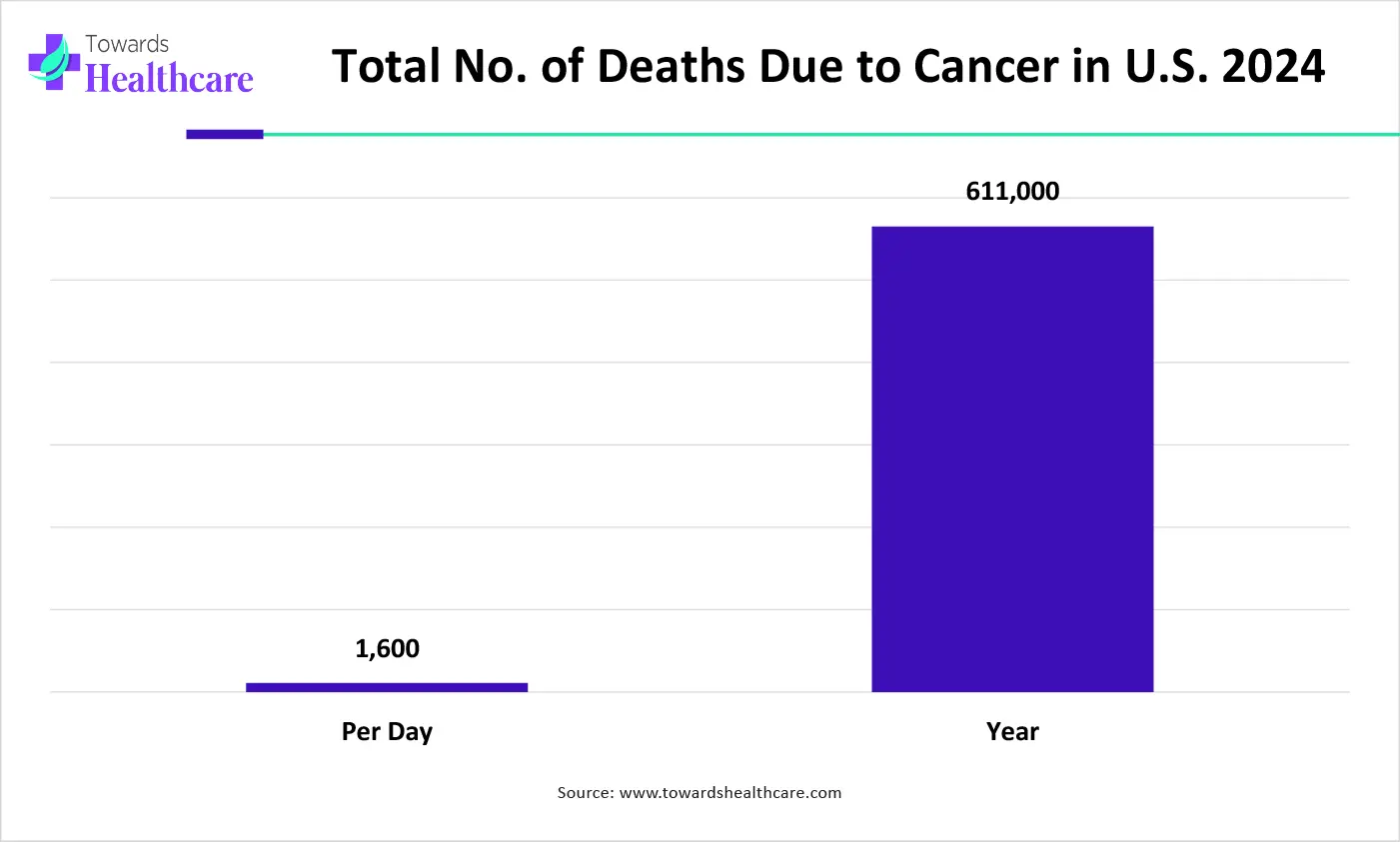

The graph represents the total number of deaths due to cancer observed in the U.S. in year of 2024. It indicates that there is a rise in cases of cancer. Hence, it increases the demand for DTC genetic testing for early diagnosis as well as for the effective management of cancer. Thus, this in turn will ultimately promote the market growth.

AI helps in the analysis of complex genetic data as well as in its interpretation. Moreover, it can also be used to identify drug responses as well as genetic variants, depending on the genetic information of the patient. Hence, all these factors, with the use of AI, help in improving the DTC genetic testing. Furthermore, it also helps in identifying the risk associated with the patients and provides them with personalized treatment plans for the disease and its complications. Additionally, with the use of genetic data, AI can also be used in the drug development process.

Rising Awareness

There is a rise in awareness within the population due to increasing campaigns and programs. This, in turn, raises the importance of early diagnosis as well as healthcare. Furthermore, the rising genetic disorder also contributes to the same. Thus, for proper and effective management of various genetic disorders, genetic screening is increasing. Hence, all these factors increase the demand for the use as well as adoption of direct-to-consumer genetic testing platforms. This enhances the genetic testing as well as patient satisfaction. Thus, this enhances the direct-to-consumer genetic testing market growth.

Privacy Concerns

A large amount of genetic data is collected and stored in the direct-to-consumer genetic testing facilities. This increases the risk of data breaches as well as hacking. This, in turn, can cause the data of an individual to be exposed, which leads to patient dissatisfaction. Thus, the privacy concern results in decreased use of DTC genetic testing.

Increasing Personalized Treatment Approaches

Due to rising genetic disorders, there is a rise in the use of various personalized treatment approaches. Therefore, by using the information gathered from the genetic profile of the patient, new personalized treatment plans are being developed. This, in turn, increases the demand for DTC genetic testing facilities as well as genomic medicines. Personalized treatment approaches also reduce the side effects due to targeted treatments. Thus, all these factors enhance the use of DTC genetic testing as well as promote the direct-to-consumer genetic testing market growth.

For instance,

| Metric | Details |

| Market Size in 2026 | USD 3.79 billion |

| Projected Market Size in 2035 | USD 27.15 billion |

| CAGR (2025 - 2034) | 24.44% |

| Leading Region | North America share by 61% |

| Market Segmentation | By Test Type, By Technology, By Distributional Channel, By Region |

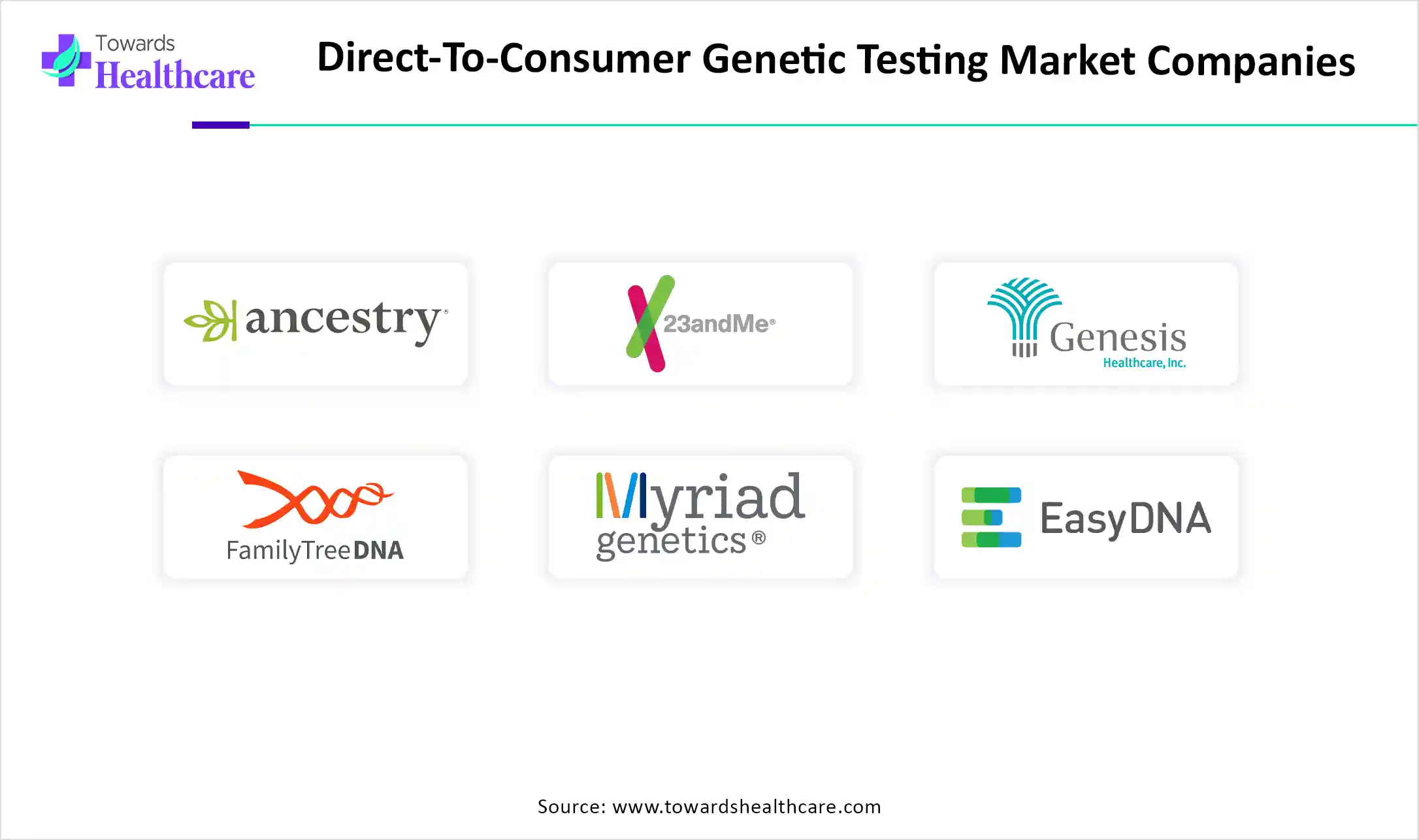

| Top Key Players | Ancestry, 23andMe, Genesis HealthCare, Family Tree DNA, Myriad Genetics Inc., EasyDNA,, Living DNA Ltd., Veritas, Color Health, Inc., Full Genomes Corporation, Inc. |

")

| Segment | Share 2025 (%) |

| Genetic Health Testing | 45% |

| Ancestry Testing | 30% |

| Lifestyle Testing | 15% |

| Pharmacogenomics Testing | 10% |

The Genetic Health Testing Segment Dominated the Genetic Testing for Consumers (DTC) Market in 2025

The genetic health testing segment held a dominant share of 45% in 2025 due to rising consumer awareness regarding inherited diseases, preventive healthcare, and early risk detection. Increasing demand for personalized health insights related to cancer, cardiovascular disorders, and chronic conditions further supported segment growth. Additionally, the growing availability of affordable at-home testing kits and expanding interest in wellness and precision medicine contributed significantly to the segment’s strong market position.

The ancestry testing segment held the second-largest share of 30% in 2025 due to strong consumer interest in exploring family origin, ethnicity, and genealogical connections. The increasing popularity of DNA-based heritage tracking, rising use of online ancestry databases, and growing social curiosity about genetic roots are key drivers. Additionally, affordable testing kits and easy-to-use platforms have made ancestry testing widely accessible, supporting its steady market growth globally.

The pharmacogenomics testing segment held 10% share in 2025 and is expected to grow at the fastest CAGR in the genetic testing for consumers (DTC) market during the forecast period due to rising demand for personalized medicine and optimized drug selection based on genetic profiles. The increasing prevalence of adverse drug reactions, the growing adoption of precision healthcare, and the expansion of prescription-based genetic insights are driving uptake. Additionally, healthcare providers and consumers are increasingly using genetic data to improve treatment effectiveness and reduce medication risks.

The lifestyle testing segment held a 15% of market share due to increasing consumer focus on personalized wellness, including fitness, diet, skincare, and nutrition. Rising health consciousness and demand for preventive healthcare are encouraging individuals to understand how genetic influence daily habits. Affordable at-home kits, easy access, and growing integration with wellness apps are further supporting adoption, making lifestyle-focused genetic insight highly popular among health-conscious consumers globally.

")

| Segment | Share 2025 (%) |

| Microarray Technology | 35% |

| Next-Generation Sequencing (NGS) | 50% |

| Polymerase Chain Reaction (PCR) | 10% |

| Sanger Sequencing | 5% |

The Next-Generation Sequencing (NGS) Segment Led the Market in 2025 with the Largest Share

The next-generation sequencing (NGS) segment led the market with a share of 50% in 2025 and is expected to grow at the fastest CAGR in the genetic testing for consumers (DTC) market during the forecast period due to its high accuracy, scalability, and ability to analyze a large volume of genetic data quickly. It enables comprehensive insights into disease risk, ancestry, and traits at a lower cost compared to traditional methods. Increasing adoption of precision medicine, declining sequencing costs, and rising demand for detailed genetic information are further driving NGS expansion globally.

The microarray technology segment held the second-largest share of 30% in 2025 due to its cost-effectiveness, high throughput capability, and reliable performance in analyzing known genetic variations. It is widely used for ancestry testing and basic health risk screening. Established infrastructure, faster processing time compared to traditional methods, and affordability for large-scale consumer testing have supported its strong adoption, especially in commercial genetic testing services globally.

The polymerase chain Reaction (PCR) segment held 15% of the genetic testing for consumers (DTC) market share due to its high sensitivity, accuracy, and ability to rapidly amplify small DNA samples for analysis. It is widely used for detecting specific genetic markers, disease risk screening, and trait identification. Low-cost, established laboratory use, and compatibility with at-home sample collection kirs further support its increasing adoption in consumer genetic testing services globally.

The Sanger sequencing segment held a 5% of market share due to its high accuracy and reliability in analyzing a specific DNA region and validating genetic variation. It is widely used for confirmatory testing and small-scale genetic analysis. Although less scalable than newer technologies, its proven precision, cost-effectiveness for targeted sequencing, and strong clinical acceptance continue to support its steady adoption in consumer genetic testing applications.

| Segment | Share 2025 (%) |

| Online Platform | 60% |

| OTC | 40% |

How the Online Platform Segment Dominated the Direct-to-Consumer Genetic Testing Market?

By distribution channel type, the online platform segment dominated the global direct-to-consumer genetic testing market by 60% in 2025. The segment dominated because the online platform offered convenience as well as a wider range of DTC genetic testing services, which promoted the market growth.

OTC Platform Segment: Significantly Growing

By distribution channel type, the OTC platform segment is predicted to grow significantly during the forecast period. The OTC platforms are providing easy access, which in turn is enhancing the consumers' satisfaction.

")

| Segment | Share 2025 (%) |

| Online Platforms | 60% |

| In-Store Services | 20% |

| Direct Mail Services | 20% |

The Online Platforms Segment Led the Market in 2025 with the Largest Share

The online platforms segment held a dominant share of 60% in 2025 and is expected to grow at the fastest CAGR in the genetic testing for consumers (DTC) market during the forecast period due to its convenience, easy accessibility, and direct-to-consumer delivery model. It allows users to order kits, submit samples, and receive them digitally without visiting healthcare facilities. Growing interest penetration, rising smartphone usage, and preference for at-home healthcare services further support its dominance. Additionally, integrated dashboards and personalized reports enhance user experience, driving higher adoption of online genetic testing platforms globally.

The direct mail services segment held the second-largest share of 20% in 2025 due to its simplicity, wide accessibility, and strong presence among established genetic testing companies. Consumers receive testing kits directly at home, making sample collection convenient and user-friendly. This model is particularly popular among ancestry and health testing users. Reliable logistics networks, strong brand trust, and ease of kit return for lab analysis further support its steady adoption globally.

The in-store services segment held a 20% of the genetic testing for consumers (DTC) market share due to growing consumer preference for guided testing and professional assistance during sample collection. Physical retail locations, pharmacies, and health clinics provide trust, accuracy, and instant support, which improves user confidence. Increasing collaborations between genetic testing companies and retail chains, along with rising demand for a hybrid online-offline healthcare experience, are further driving the growth of in-store genetic testing services globally.

")

| Segment | Share 2025 (%) |

| Age | 60% |

| Gender | 30% |

| Income Level | 10% |

The Age-Adults segment led the Market in 2025 with the Largest Share

The age-adults segment dominated the genetic testing for consumers (DTC) market with the highest share in 2025 due to higher health awareness, stronger purchasing power, and greater interest in preventive healthcare. Adults are more likely to seek insights into disease risk, ancestry, fertility, and lifestyle optimization. Increasing adoption of personalized wellness solutions and easy availability of at-home testing kits further support this dominance. Additionally, rising focus on early disease detection and long-term health management drives strong demand among adult consumers globally.

The gender-female segment held the second-largest share in 2025 due to increasing focus on reproductive health, carrier screening, fertility planning, and hereditary disease risk assessment. Women are also highly engaged in wellness, skincare, and lifestyle-based genetic insights. Growing awareness of preventive healthcare and rising adoption of personalized health solutions further demand. Additionally, easy access to at-home testing kits and digital health platforms is driving strong participation among female consumers globally.

The income level-high segment held a significant share of the genetic testing for consumers (DTC) market due to increasing willingness to spend on advanced personalized healthcare and wellness solutions. High-income consumers are more likely to adopt premium genetic testing services for disease risk assessment, nutrition, fitness, and preventive care. Growing awareness of precision medicine, access to digital health technologies, and demand for comprehensive genomic insight are further driving growth within this consumer group globally.

")

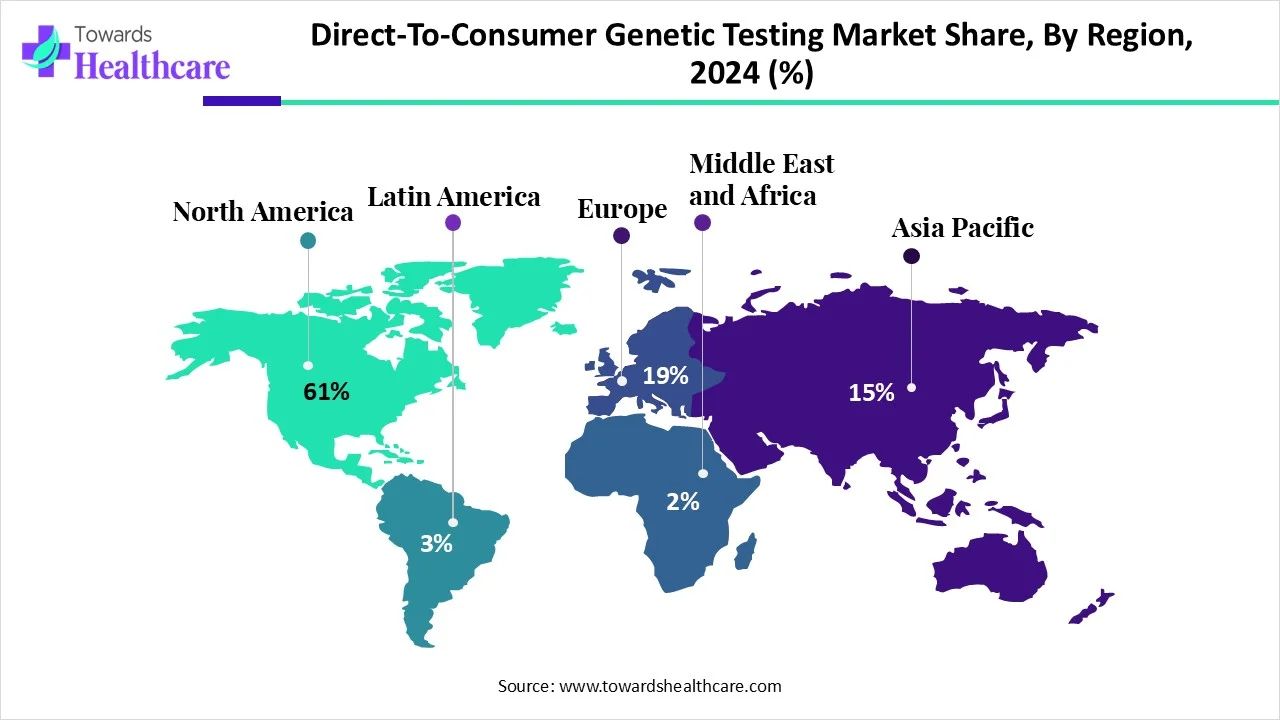

North America dominated the genetic testing for consumers (DTC) market with a share of 40% in 2025 due to high consumer awareness regarding personalized healthcare, strong adoption of preventive health solutions, and widespread availability of advanced genetic testing services. The presence of major market players, well-developed digital health infrastructure, and increasing demand for ancestry and health-risk testing further support regional dominance. Additionally, rising healthcare spending and strong consumer acceptance of at-home diagnostic technologies continue to drive market growth across the region.

U.S. Market Trends

The U.S. leads the genetic testing for consumers (DTC) market due to strong consumer awareness, advanced healthcare infrastructure, and the presence of major genetic testing companies offering innovative at-home testing solutions. High adoption of personalized healthcare, increasing interest in ancestry and disease-risk analysis, and growing investment in genomic research further support market leadership. Additionally, widespread internet access and digital health adoption continue to strengthen the expansion of DTC genetic testing services across the country.

Europe is estimated to host the fastest-growing direct-to-consumer genetic testing market during the forecast period. Europe is experiencing a rise in awareness about the early diagnosis of genetic diseases or any other diseases. This enhances the market growth.

The Germany Direct-To-Consumer Genetic Testing Market Trends

The increasing awareness, as well as the rising genetic diseases, is driving the demand for genetic testing. This, in turn, increases the use of DTC genetic testing for early diagnosis as well as effective treatment plans.

The UK Direct-To-Consumer Genetic Testing Market Trends

The use of DTC genetic testing is increasing in the UK due to the growing awareness about the disease, as well as for proper management of health. At the same time, the technological advancements used in DTC are also enhancing the genetic testing conducted.

Asia Pacific is anticipated to grow at the fastest CAGR in the genetic testing for consumers (DTC) market due to rising healthcare awareness, increasing disposable income, and growing adoption of personalized healthcare solutions. Expanding internet penetration, rapid digital health adoption, and improving access to at-home testing services are further supporting market growth. Additionally, increasing investments in genomic research and growing interest in preventive healthcare are accelerating demand across the region.

India Market Trends

India is expected to grow at the fastest CAGR in the genetic testing for consumers (DTC) market due to rising awareness of preventive healthcare, increasing disposable income, and rapid digital health adoption. Growing internet penetration and expanding access to affordable at-home genetic testing kits are further driving demand. Additionally, increasing focus on personalized wellness, ancestry, and genomics research initiatives is supporting strong market growth across the country.

Latin America is expected to grow at a notable CAGR in the direct-to-consumer genetic testing market in the foreseeable future. The rising prevalence of genetic disorders, growing genomics research, and favorable government policies are the major growth factors of the market in Latin America. Government bodies launch initiatives to create awareness among the general public for screening and early diagnosis of genetic disorders. The number of clinical laboratories in Latin America is increasing with the adoption of massive parallel sequencing. The increasing awareness of personalized medicines also propels market growth.

Latin America is expected to grow significantly in the direct-to-consumer genetic testing market during the forecast period. Latin America is experiencing a rise in advancements in the direct-to-consumer genetic testing platforms. This is increasing the utilization of sequencing and genomics technologies for the development of accurate and affordable genetic testing tools. At the same time, predictive testing approaches are also being developed.

Furthermore, the increasing demand and development of personalized medicines are also increasing their use. This, in turn, is also increasing their purchase through various online distribution platforms. These developments are further being supported by the government investments. Thus, this is enhancing the market growth.

Mexico Market Trends

The Mexican Rare Disease Patient Registry is an open, online, self-reporting registry study to gather information about the rare disease prevalence in Mexico. It was reported that around 71.53% of registered patients were informed that their condition could have a genetic origin. Out of these, 27.77% of patients had a genetic test performed. (Source: Science Direct)

Argentina Market Trends

Congenital anomalies are the second leading cause of death among infants in Argentina. It is estimated that approximately 1.7% of babies born are affected by congenital anomalies. According to the International Trade Administration, there are around 6,500 clinical laboratories in Argentina, of which 1,000 are public and 5,500 are private. (Source: Trade Administration)

The Middle East and Africa are expected to show lucrative growth in the direct-to-consumer genetic testing market during the predicted time. The awareness about the genetic disorder among the populations of the Middle East and Africa is increasing. This, in turn, is increasing the demand for direct-to-consumer genetic testing options for early detection.

At the same time, the growing research development is increasing its use. This, in turn, is leading to new collaborations among the industries as well as institutes. Moreover, the increasing adoption of advanced technologies is increasing their development and production. Thus, all these developments are promoting the market growth.

R&D

Clinical Trials

Patient Support and Services

| Companies | Headquarters | Offerings |

| 23andMe | United States (California) | Provides ancestry analysis, health risk reports, carrier screening, and personalized genetic trait insights directly to consumers. |

| Family Tree DNA | United States (Texas) | Offers DNA testing focused on genealogy, including Y-DNA, mtDNA, and autosomal tests for family lineage tracking. |

| Ancestry | United States (Utah) | Specializes in ancestry DNA testing combined with family history records and ethnicity estimation services. |

| Genesis HealthCare | United States (Pennsylvania) | Delivers healthcare services, diagnostic support, and wellness-related genetic and clinical testing solutions. |

| EasyDNA | Malta | Provides at-home DNA testing services, including ancestry, relationship testing, and lifestyle-related genetic analysis. |

| Veritas | United States (Massachusetts) | Focuses on whole genome sequencing and preventive genetic insights for personalized health management. |

| Myriad Genetics | United States (Utah) | Offers clinical-grade genetic testing for cancer risk, hereditary conditions, and precision medicine applications. |

Strengths

Weaknesses

Opportunities

By Testing Type

By Technology

By Service

By Consumer Demographics

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar