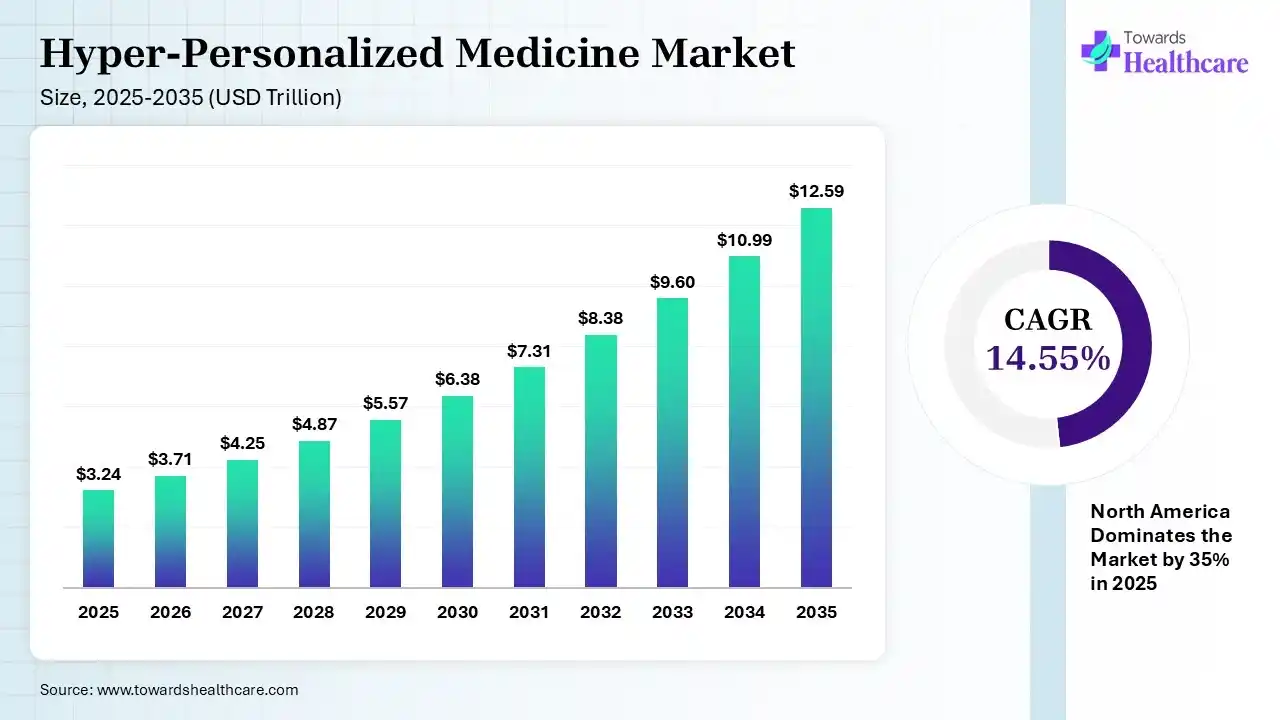

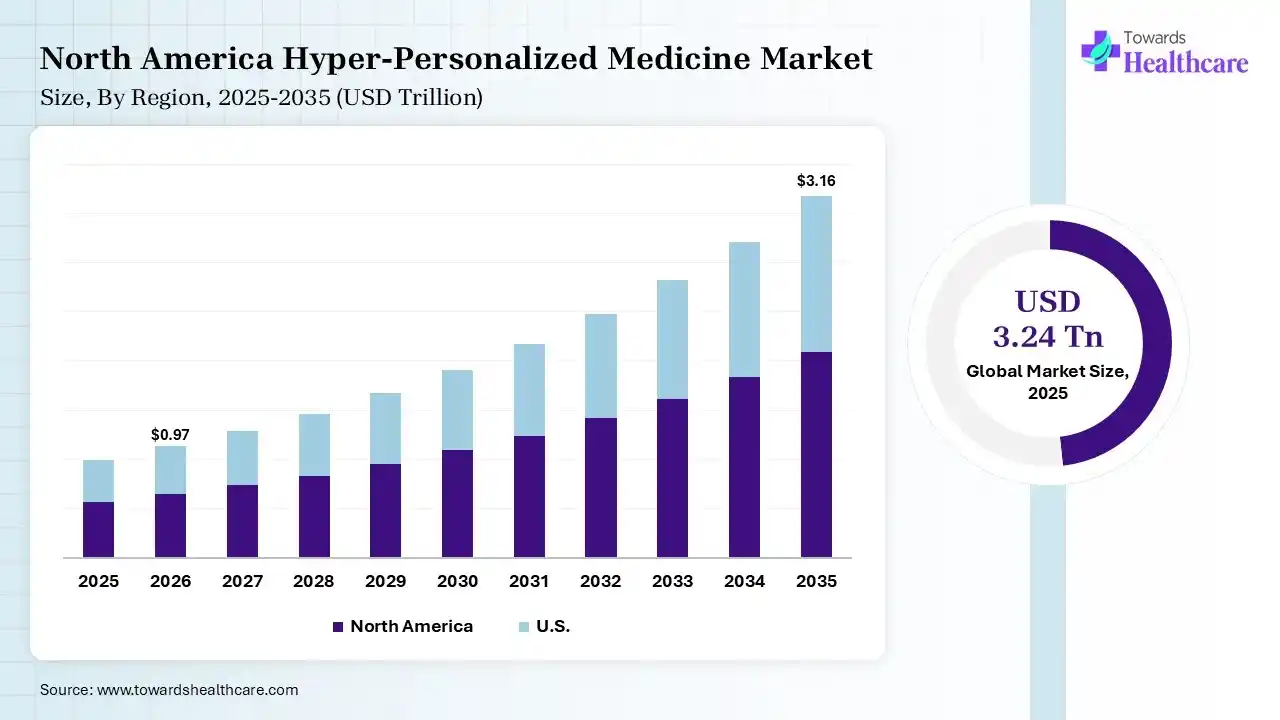

The global hyper-personalized medicine market size was estimated at USD 3.24 trillion in 2025 and is predicted to increase from USD 3.71 trillion in 2026 to approximately USD 12.59 trillion by 2035, expanding at a CAGR of 14.55% from 2026 to 2035. A massive increase in cancer, infectious diseases, & rare diseases cases drives the demand for advanced therapies, like targeted therapies. Moreover, giant firms are revolutionising diagnostics by integrating with AI algorithms, with emphasis on real-world data (RWD).

The hyper-personalized medicine market is defined as an advanced, patient-oriented healthcare model, which customizes mitigation & treatment to each patient’s unique genetic, molecular, environmental, & lifestyle profile. The overall market growth is fueled by ongoing advances in faster, affordable high-throughput genetic sequencing, AI & big data analytics, with surging significant investments in biotechnology & collaboration among diverse firms related to precision medicine.

Hyper-personalized medicine is an advanced healthcare approach that tailors disease prevention, diagnosis, and treatment to an individual’s unique genetic profile, molecular characteristics, lifestyle, environmental factors, and real-time health data. The hyper-personalized medicine market is expanding rapidly due to the increasing demand for precision therapies, growing prevalence of chronic and genetic diseases, and wider adoption of genomic sequencing and biomarker-based diagnostics. Digital health platforms and predictive analytics are enabling highly individualized treatment strategies and improving clinical outcomes. Rising investments in precision healthcare, expanding applications of gene and cell therapies, and increasing use of companion diagnostics are creating substantial growth opportunities. Future market development will be driven by integrated healthcare data ecosystems, wearable health technologies, real-time patient monitoring, and continuous innovation in personalized therapeutics, supporting more effective preventive and patient-centric care.

Primarily, AI supports the interpretation of complex genomic, transcriptomic, & proteomic data to determine disease complications & personalized therapeutic targets, specifically in oncology & rare genetic disorders. Wearable devices & IoT technology led by AI are fostering the monitoring of lifestyle parameters & biomarkers in real-time.

Emphasizing Genomics & Molecular Profiling

The globe is highly leveraging cost-effective, high-throughput Next-Generation Sequencing (NGS), which enables rapid sequencing of individual genomes to assist in treatment decisions.

Investigating AI & Digital Twins

Firms are widely evolving digital twins to simulate disease growth & estimate therapeutic responses, especially in neurology & oncology.

Focusing on Real-World Data (RWD)

Rigorous research activities are aiming to use RWD from wearables & EHRs to develop consistent, real-time care loops instead of episodic treatments

| Table | Scope |

| Market Size in 2026 | USD 3.71 Trillion |

| Projected Market Size in 2035 | USD 12.59 Trillion |

| CAGR (2026 - 2035) | 14.55% |

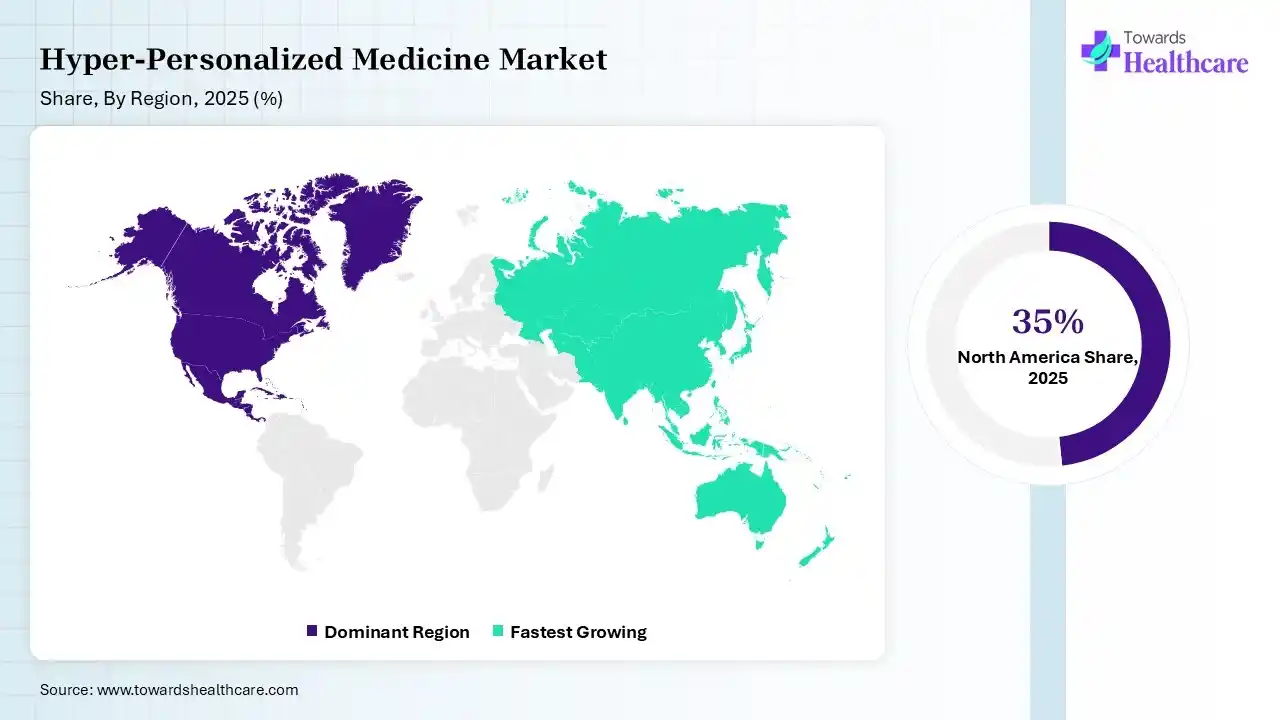

| Leading Region | North America by 35% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Technology, By Application, By End User, By Region |

| Top Key Players | Illumina, Inc., Roche Diagnostics, Novartis, Exact Sciences, AstraZeneca PLC, Bristol-Myers Squibb Co. (BMS), Amgen Inc., QIAGEN, Pfizer Inc., NeoGenomics, Inc. |

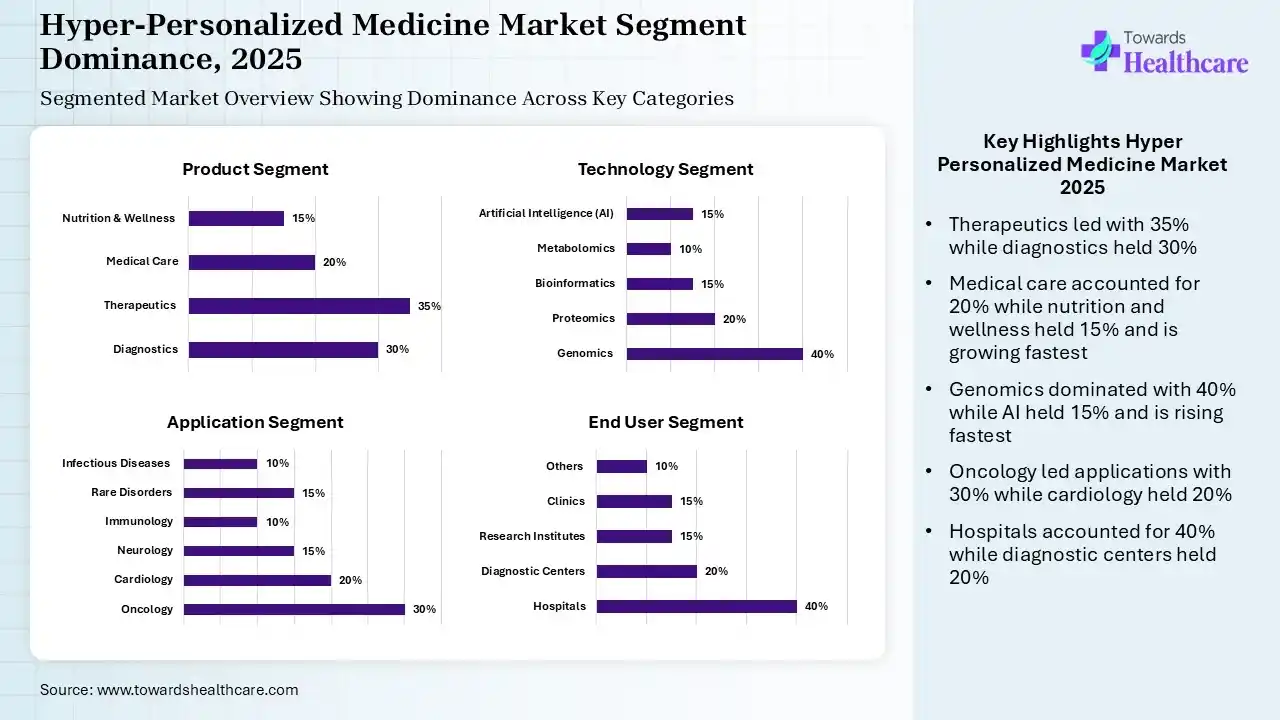

| Segment | Share 2025 (%) |

| Diagnostics | 30 % |

| Therapeutics | 35 % |

| Medical Care | 20 % |

| Nutrition & Wellness | 15 % |

The Therapeutics Segment Led the Market in 2025

In 2025, the therapeutics segment was dominant, with a 35% share of the hyper-personalized medicine market. Continuing demand & expansion of targeted therapies are driving the development of therapeutics, including personalized immunotherapy, gene editing, & cell-based therapies. Globally accelerating awareness & diagnosis of rare diseases is spurring the need for, & adoption of, precision molecular therapies.

The diagnostics segment held the second-largest share of 30% in 2025, due to the rising demand for extensive diagnosis in the increase in oncology & rare diseases cases. Also, the market is experiencing funding from both public & private sectors, which surges innovations in product development.

The medical care segment accounted for 20% share of the hyper-personalized medicine market in 2025. The worldwide growing adoption of telemedicine & AI assistance supports raising patient engagement & care pathways. Trend is transforming 3D printing to allow tailored implants & customized drug delivery systems.

However, the nutrition & wellness segment captured a 15% share in 2025 & is predicted to register rapid growth. The segmental progression is driven by a rise in obesity, cardiovascular diseases, & diabetes, which need targeted diet interventions. Researchers are reinforcing gut microbiota & RNA analysis, like customized probiotic & prebiotic intake to enhance immunity & digestion.

| Segment | Share 2025 (%) |

| Genomics | 40 % |

| Proteomics | 20 % |

| Bioinformatics | 15 % |

| Metabolomics | 10 % |

| Artificial Intelligence (AI) | 15 % |

The Genomics Segment Dominated the Market in 2025

In 2025, the genomics segment held a major share of 40% of the hyper-personalized medicine market. Immersive affordability & rapid actions of whole-genome sequencing, coupled with decreased expenditure from over $100 million to under $1,000, enable broader adoption. The use of data from Genome-Wide Association Studies (GWAS), PRS enables the analysis of polygenic trait risk.

The proteomics segment captured 20% share in 2025, due to the improving protein profiling. This majorly helps in the identification of potential drug targets, recognizing mechanisms of action, & assessing drug efficacy & toxicity. timsTOF & Orbitrap integrated with PASEF allowing for deep proteome coverage in plasma, urine, & biopsy samples.

The bioinformatics segment accounted for 15% share of the hyper-personalized medicine market. This significantly supports biomarker discovery & assists in repurposing drugs, with minimal R&D spending & time-to-result for new therapies. Integration of genomics, transcriptomics, proteomics, and metabolomics to offer a holistic view of a patient’s health.

Whereas the artificial intelligence (AI) segment held 15% share in 2025 & is estimated to expand fastest. Inclusion of AI-powered predictive models is rapidly refining treatment recommendations & outcome projections. AI pushes drug formulation & delivery for each by estimating drug-excipient interactions & simulating metabolism.

The metabolomics segment captured 10% share of the hyper-personalized medicine market, due to the strong assistance in the determination of treatment nonresponders & anticipation of drug toxicity, vital for choosing the appropriate medication, dose, & time for individuals.

| Segment | Share 2025 (%) |

| Oncology | 30 % |

| Cardiology | 20 % |

| Neurology | 15 % |

| Immunology | 10 % |

| Rare Disorders | 15 % |

| Infectious Diseases | 10 % |

The Oncology Segment Was Dominant in the Market in 2025

In 2025, the oncology segment led with 30% share of the market. The globe is facing nearly 20 million new cancer cases & 9.7 million deaths each year, which demands advanced interventions. With a robust investment, researchers are stepping towards stimuli-responsive carriers to release the drug only upon encountering tumor-specific triggers, like elevated glutathione (GSH) or acidic pH.

The cardiology segment captured the second-largest share of 20% in 2025, due to the widespread use of cardiac biomarkers & tailored regimens, which lower morbidity in chronic cardiovascular conditions. Firms are fostering integration of multi-omics, AI-enabled diagnostics, & RNA-based therapies to treat inherited cardiomyopathies & cardiovascular disease (CVD).

The neurology segment held a 15% share of the hyper-personalized medicine market in 2025. Key drivers are the increasing geriatric population & massive investments in neuro-genomic research. The market is leveraging exosomes derived from stem cells & functionalized magnetic nanoparticles to bypass the BBB for targeted delivery of neuroprotective drugs.

The rare disorders segment accounted for 15% share in 2025. The globe is facing a notable increase in Spinal muscular atrophy (SMA), Duchenne Muscular Dystrophy (DMD), & other rare cases, which demand gene therapies & RNA-based medications. Innovations comprise antisense oligonucleotides (ASOs) for a single patient’s unique gene mutation.

The infectious diseases segment held 10% share in 2025 & is predicted to expand at a rapid CAGR. For these prevalences, the market has been implementing various adaptive therapies & expedited diagnostics, which fuel bespoke treatments for emerging pathogens. Another catalyst is extensive government funding for pandemic preparedness, vaccine development, & tailored diagnostics.

| Segment | Share 2025 (%) |

| Hospitals | 40 % |

| Diagnostic Centers | 20 % |

| Research Institutes | 15 % |

| Clinics | 15 % |

| Others | 10 % |

The Hospitals Segment Dominated the Market in 2025

The hospitals segment led with a 40% share of the hyper-personalized medicine market in 2025. Dominance is fueled by the increased patient volumes, well-nurtured infrastructure, & wider adoption of AI-enabled diagnostic tools for customized therapies. Clinicians are emphasizing AI-driven solutions & detection of risk factors years before disease onset.

The diagnostic centers segment captured 20% share of the market in 2025, as the globe is spurring high-throughput genomic & biomarker lab-scale precision diagnostics adoption. They foster the analysis of cell-free DNA (cfDNA) & circulating tumour cells (CTCs) from blood samples, to allow non-invasive, real-time monitoring of tumour assessment & treatment response.

The research institutes segment held a15% share of the hyper-personalized medicine market, due to the significant R&D investment to explore innovations. These institutes are widely leveraging proteoforms of a protein product from a single gene by employing high-throughput mass spectrometry.

Moreover, the others segment held a 10% share in 2025 & is estimated to witness rapid expansion. This mainly covers Ambulatory Surgical Centers (ASCs), which unite with value-based healthcare models to focus on excellent patient outcomes at reduced spending. A particular adoption of 3D printing for orthopedic plates, surgical guides, & tailored implants that impacts the overall ASC’s progression.

")

North America registered dominance with 35% share in 2025, due to the advanced research infrastructure & substantial investments in biotech R&D. Canada has been executing specialized platforms that offer AI-assisted decision support, with diagnostics, treatments, & medication delivery.

For instance,

U.S. Market Trends

Whereas the U.S. startups are widely utilizing AI to roll out prognostic tests for breast cancer to estimate patient results. The Personalized Medicine Coalition (PMC) revealed that over 25% of new FDA-authorized drugs are now tailored medicines.

Canada Accelerates Growth in Hyper-Personalized Medicine

Canada is witnessing significant growth in the hyper-personalized medicine market due to increasing investments in precision healthcare, expanding genomic research, and strong adoption of advanced molecular diagnostics. Government support for genomics initiatives and growing collaborations between research institutions and biotechnology companies are accelerating innovation. Rising demand for personalized therapies and precision oncology is further driving market expansion.

Asia Pacific accounted for 20% share of the hyper-personalized medicine market in 2025 & is anticipated to expand fastest in the coming era. This progression is impelled by the broader uptake of the latest technologies, such as genomic sequencing, big data analytics, & AI-driven diagnostics, with heavy investments in these technologies & digital healthcare infrastructure.

For instance,

China Market Trends

However, China is increasingly using Hainan & Beijing as Real-World Data (RWD) pilot zones to speed up the approval of customized drugs & medical devices, specifically in oncology & rare diseases.

India Emerges as a Fast-Growing Hyper-Personalized Medicine Market

India is significantly growing in the hyper-personalized medicine market due to increasing adoption of genomic testing, rising prevalence of chronic and genetic diseases, and expanding investments in precision healthcare. Growing availability of advanced molecular diagnostics, AI-driven clinical decision support, and personalized oncology solutions is accelerating market growth. Government initiatives promoting biotechnology, expanding healthcare infrastructure, and increasing collaborations between research organizations and healthcare providers are further supporting market expansion.

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Company | Description |

| Illumina, Inc. | Its offerings range from high-throughput sequencing instruments to clinical informatics & molecular diagnostic tools. |

| Roche Diagnostics | This firm focuses on next-generation sequencing (NGS), liquid biopsies, & digital pathology to allow precise, personalized care. |

| Novartis | This company invested in the integration of advanced technology, data analytics, & molecular science. |

| Exact Sciences | A player offers molecular diagnostics to guide treatment decisions based on a patient's specific cancer biology. |

| AstraZeneca PLC | It specializes in next-gen therapeutics & companion diagnostics (CDx). |

| Bristol-Myers Squibb Co. (BMS) | This mainly facilitates precision medicine in oncology, hematology, and immunology. |

| Amgen Inc. | Its offerings cover integration of advanced human genetics, artificial intelligence (AI), & molecular biology. |

| QIAGEN | This unveiled solutions in ecology, neurological disorders, & chronic diseases by using Next-Generation Sequencing (NGS), digital PCR (dPCR), & bioinformatics. |

| Pfizer Inc. | A company emphasizes advanced analytics, AI, & genetic profiling, especially in oncology, rare diseases, & mRNA technologies. |

| NeoGenomics, Inc. | This mainly offers over 500 tests across different modalities to guide targeted treatment. |

In May 2026, personalized medicines accounted for more than one-third of all new drug approvals for the sixth consecutive year, while we also continue to see important advances in gene- and cell-based therapies and steady growth in companion diagnostic approvals and authorizations. Together, these trends reflect more than a decade of sustained scientific progress and demonstrate that personalized medicine is no longer an emerging concept it is now a central driver of biomedical innovation and patient care”, said Daryl Pritchard, Senior Vice President, Science Policy at the Personalized Medicine Coalition.

Strengths

Weaknesses

Opportunities

Threats

By Product

By Technology

By Application

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar