Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

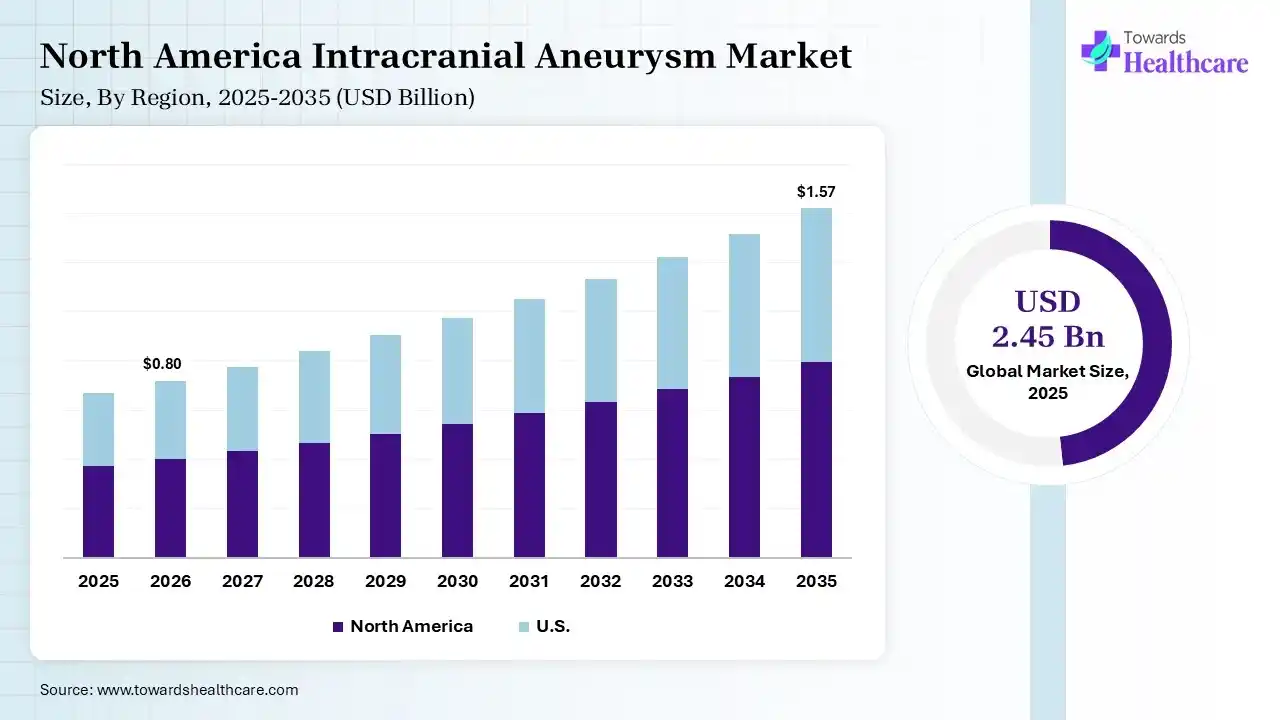

The global intracranial aneurysm market size was estimated at USD 2.45 billion in 2025 and is predicted to increase from USD 2.66 billion in 2026 to approximately USD 5.64 billion by 2035, expanding at a CAGR of 8.7% from 2026 to 2035. The market is witnessing strong momentum, fueled by rising awareness of neurological disorders and increasing preference for advanced minimally invasive treatment options. Continuous innovation in neurovascular devices and improved diagnostic capabilities are further accelerating market growth and shaping future opportunities.

")

An intracranial aneurysm is a weak, bulging area in a blood vessel wall within the brain that balloons outward due to pressure from blood flow. If it ruptures, it can cause serious bleeding in the brain and become life-threatening. The intracranial aneurysm market is experiencing steady growth due to the increasing incidence of brain vascular disorders, hypertension, and an aging population. Growing demand for early diagnosis, improved neuroimaging systems, and minimally invasive treatment options such as coiling and flow diversion is further boosting market expansion. Continuous technological advancements in neurovascular devices are also creating strong opportunities for future growth.

Intracranial aneurysms are abnormal bulges or weakened areas in the walls of brain arteries that can rupture, causing life-threatening bleeding and requiring timely diagnosis and treatment. The intracranial aneurysms market is expanding due to the increasing prevalence of cerebrovascular disorders, growing awareness of early aneurysm screening, and rising demand for minimally invasive endovascular procedures. Technological advancements, including flow diversities, intrasaccular devices, bioactive embolization coils, high-resolution neurovascular imaging, and AI-assisted diagnostic platforms, are improving treatment precision and patient outcomes. A key market trend is the increasing adoption of image-guided neurointerventional procedures in specialized stroke and neurosurgical centers. Future opportunities lie in robotic-assisted neurovascular interventions, next-generation biomaterials, personalized treatment planning, and expanding healthcare systems, supported by continuous innovation and favorable reimbursement initiatives.

AI is positively impacting the market by improving the speed and accuracy of diagnosis, helping assess rupture risk, and supporting personalized treatment decisions. Its integration with advanced imaging and surgical planning tools enhances procedural precision, improves patient outcomes, and increases demand for innovative neurovascular devices and smart healthcare solutions.

| Table | Scope |

| Market Size in 2026 | USD 2.66 Billion |

| Projected Market Size in 2035 | USD 5.64 Billion |

| CAGR (2026 - 2035) | 8.7% |

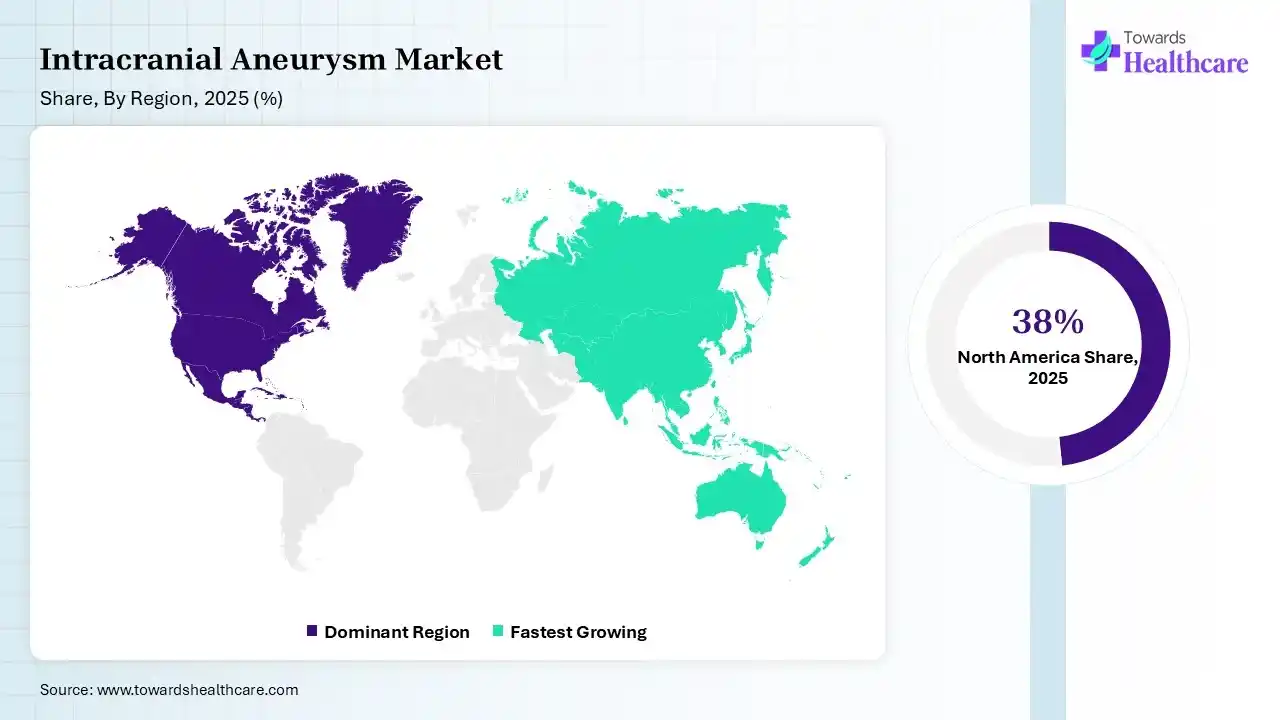

| Leading Region | North America by 38% |

| Key Applications | Aneurysm diagnosis, endovascular coiling, flow diversion, stent-assisted coiling, surgical clipping, neurovascular imaging, rupture risk assessment |

| Primary End Users | Hospitals, Neurosurgery Centers, Neurovascular Clinics, Ambulatory Surgical Centers (ASCs), Diagnostic Imaging Centers |

| Key Growth Drivers | Rising incidence of cerebrovascular disorders, aging population, increasing adoption of minimally invasive procedures, AI-enabled imaging, improved neurovascular diagnostics |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Treatment Type, By End User, By Diagnosis Modality, By Region |

| Top Key Players | Strayer Corporation, Medtronic, MicroPort Scientific Corporation, Johnson & Johnson, Terumo Corporation, Penumbra, Inc. |

")

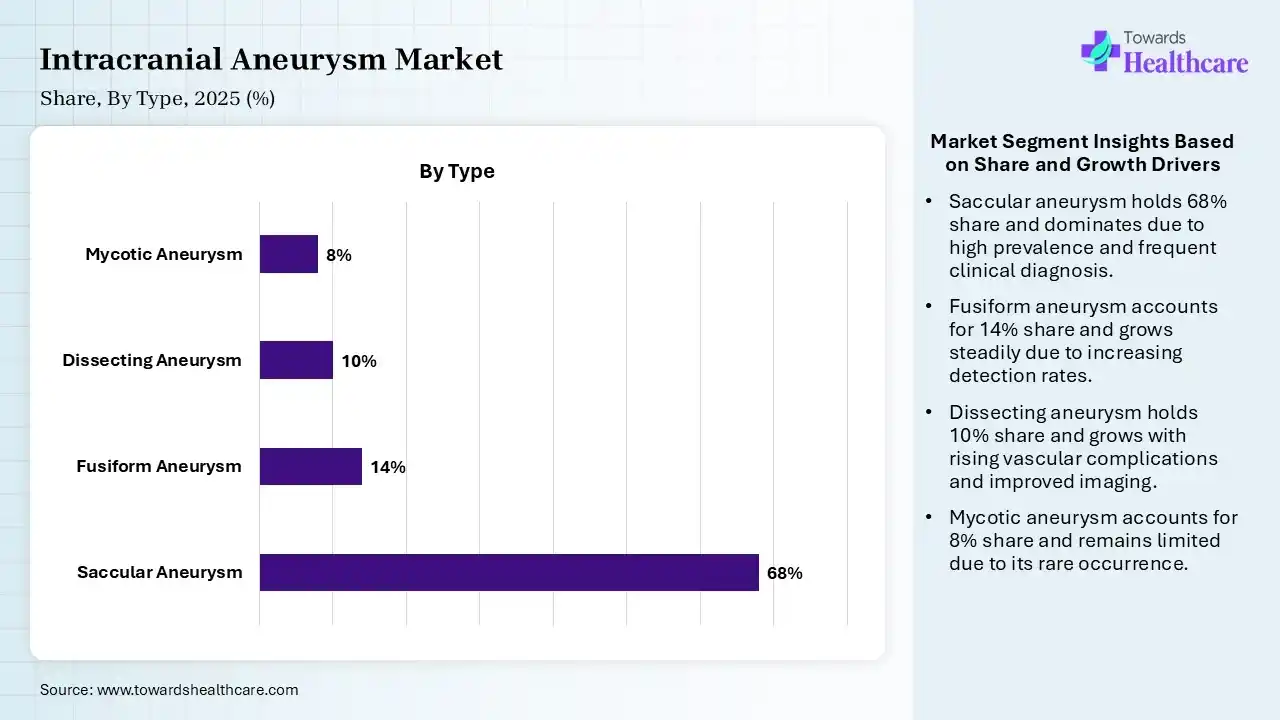

| Segment | Share 2025 (%) |

| Saccular Aneurysm | 68% |

| Fusiform Aneurysm | 14% |

| Dissecting Aneurysm | 10% |

| Mycotic Aneurysm | 8% |

The Saccular Aneurysm Segment Dominated the Market in 2025

The saccular aneurysm segment dominated the intracranial aneurysm market with a share of 68% in 2025 because it is the most frequently diagnosed type of intracranial aneurysm, making it the primary focus of diagnosis and treatment. Its dominance is further supported by strong adoption of minimally invasive procedures, better clinical detection rates, and continuous advancements in neurovascular devices, which together contributed to the market growth.

The fusiform aneurysm segment held the second-largest share of 14% of the market in 2025 and is expected to grow at the fastest CAGR of 9.2% in the market during the forecast period due to the increasing incidence of complex vascular abnormalities and growing diagnosis rates through advanced imaging technologies. Rising adoption of specialized endovascular treatment and improved clinical management for difficult aneurysms further supported segment growth, contributing significantly to its strong market presence and revenue share.

The dissecting aneurysm segment held 10% of the intracranial aneurysm market share in 2025 due to rising awareness of rare cerebrovascular conditions and improved detection through high-resolution imaging technologies. Increasing cases linked to trauma, hypertension, and vascular disorders are also contributing to demand. In addition, advancements in specialized endovascular treatment options and growing access to neurovascular care are supporting the segment’s continued expansion across healthcare markets.

The mycotic aneurysm segment held 8% of the intracranial aneurysm market share in 2025 due to the increasing incidence of bloodstream infections, infective endocarditis, and weakened immune conditions that raise the risk of infected cerebral aneurysms. Improved diagnostic imaging and earlier clinical recognition are supporting faster diagnosis and treatment. Additionally, growing use of targeted antimicrobial therapies and advanced neurovascular interventions is further driving segment growth.

")

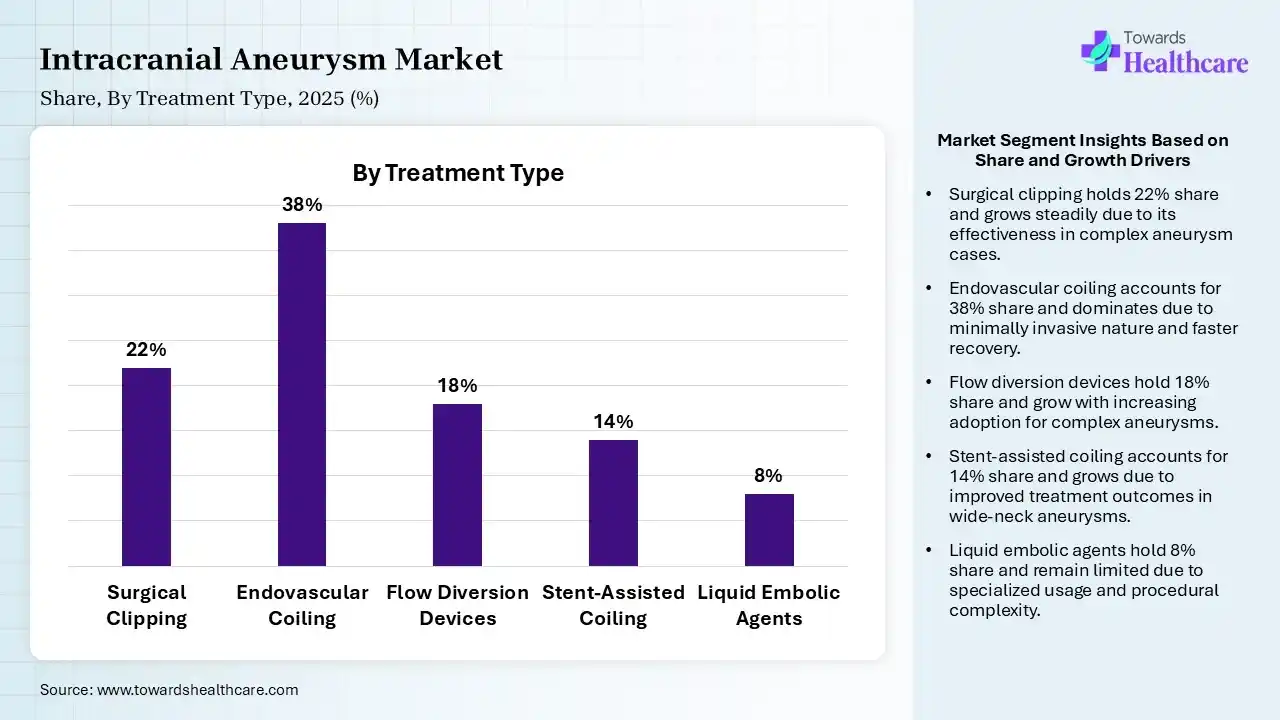

| Segment | Share 2025 (%) |

| Surgical Clipping | 22% |

| Endovascular Coiling | 38% |

| Flow Diversion Devices | 18% |

| Stent-Assisted Coiling | 14% |

| Liquid Embolic Agents | 8% |

The Endovascular Coiling Segment Led the Market in 2025 with the Largest Share

The endovascular coiling segment led the intracranial aneurysm market with a 38% share in 2025 due to its strong preference as a minimally invasive treatment option for intracranial aneurysms. It offers shorter recovery time, reduced surgical risk, and lower hospital stay compared with open surgery. Its wide clinical acceptance, high success rate, and continuous advances in coil technology have further strengthened its dominant market position.

The surgical clipping segment second-largest share of 22% of the market in 2025 due to its continued use in treating complex and large aneurysms that may not be suitable for minimally invasive procedures. It remains a trusted option for long-term aneurysm closure, especially in critical cases requiring direct surgical access. Strong clinical confidence, established surgical expertise, and consistent demand in tertiary care centers continue to support its market position.

The flow diversion devices segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 11.2% in the market during the forecast period due to rising adoption for treating complex, wide-neck, and large intracranial aneurysms. These devices offer improved long-term vessel reconstruction, lower recurrence rates, and better outcomes in difficult cases. Continuous technological advancements and increasing physician preference for minimally invasive neurovascular solutions are further accelerating segment growth.

The stent-assisted coiling segment held 14% of the intracranial aneurysm market share in 2025 due to its increasing use in treating wide-neck and complex intracranial aneurysms that are difficult to manage with conventional coiling alone. The technique provides better coil stability, improves aneurysm occlusion, and reduces recurrence risk. Rising adoption of advanced stent technologies and growing preference for minimally invasive neurovascular procedures are further supporting segment growth.

")

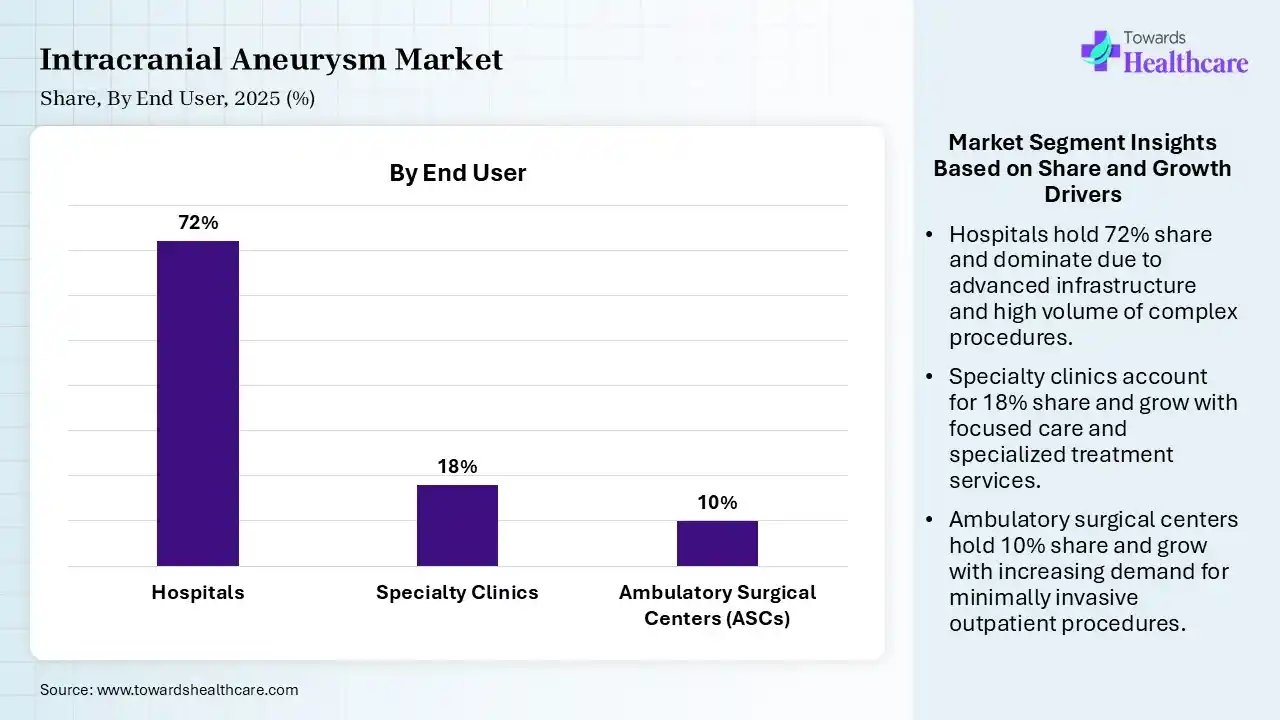

| Segment | Share 2025 (%) |

| Hospitals | 72% |

| Specialty Clinics | 18% |

| Ambulatory Surgical Centers (ASCs) | 10% |

The Hospitals Segment held a Dominant Position in the Market in 2025

The hospitals segment held a dominant share of 72% in 2025 due to the high volume of intracranial aneurysm diagnoses, emergency admissions, and advanced treatment procedures performed in hospital settings. Hospitals are equipped with specialized neuroimaging systems, neurosurgical teams, and intensive care facilities, making them the primary choice for both diagnosis and complex interventions, thereby driving their leading market share.

The specialty clinics segment held the second-largest share of 18% of the intracranial aneurysm market in 2025 and is expected to grow at the fastest CAGR of 9.1% in the market during the forecast period due to the growing demand for focused neurovascular care, faster diagnosis, and specialized treatment services. These clinics offer consultations, advanced imaging support, and minimally invasive treatment options in a more streamlined setting. Increasing patient preference for specialized care and shorter waiting times further contributed to the segment’s strong market presence.

The ambulatory surgical centers (ASCs) segment held 10% market share in 2025 and is growing steadily due to increasing preference in outpatient settings. ASCs offer shorter procedure times, reduced hospital stays, and faster patient recovery, making them an attractive option for selected aneurysm treatments. Rising healthcare cost pressure and expanding availability of advanced neurovascular technologies are further supporting segment growth.

")

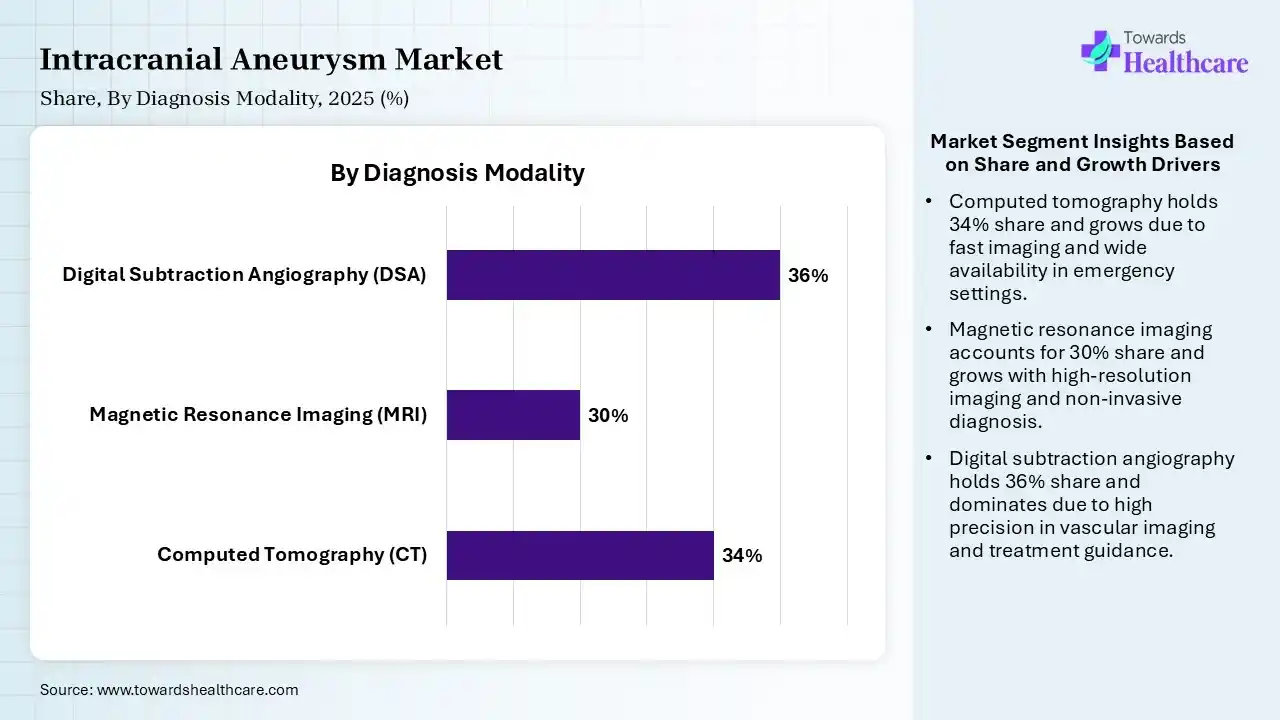

| Segment | Share 2025 (%) |

| Computed Tomography (CT) | 34% |

| Magnetic Resonance Imaging (MRI) | 30% |

| Digital Subtraction Angiography (DSA) | 36% |

The Digital Subtraction Angiography (DSA) Segment Dominated the Market in 2025

The digital subtraction angiography (DSA) segment led the intracranial aneurysm market with a share of 36% in 2025 due to its high accuracy in detecting intracranial aneurysms and detailed visualization of cerebral blood vessels. It remains the gold-standard diagnostic technique for precise aneurysm localization, size assessment, and treatment planning. Its widespread use in hospitals and neurovascular centers for both diagnosis and interventional guidance further strengthened its market leadership.

The computed tomography (CT) segment held the second-largest share of 34% of the market in 2025 due to its rapid imaging capability, wide availability, and strong use in emergency settings for suspected aneurysm rupture cases. CT scans enable the quick detection of brain bleeding and support timely clinical decisions. Growing adoption of advanced CT angiography systems and improved imaging resolution further contributed to the segment’s substantial market share.

The magnetic resonance imaging (MRI) segment held 30% share in 2025 and is expected to grow at the fastest CAGR of 9.0% in the intracranial aneurysm market during the forecast period due to its superior soft-tissue visualization, non-invasive nature, and absence of radiation exposure. Increasing use for early aneurysm detection, follow-up monitoring, and detailed vascular assessment is driving demand. Advancements in high-resolution MR angiography technologies are further accelerating segment growth across diagnostic centers and hospitals.

")

North America dominated the intracranial aneurysm market with a share of 38% in 2025 due to its advanced healthcare infrastructure, high awareness of neurological disorders, and strong adoption of minimally invasive neurovascular procedures. The region also benefits from the advances of major medical device companies, widespread access to advanced imaging technologies, and the increasing incidence of hypertension and age-related cerebrovascular conditions, which continue to drive market growth.

U.S. Market Trends

The U.S. intracranial aneurysm market is leading due to its advanced healthcare infrastructure, high adoption of innovative neurovascular devices, and strong presence of major medical technology companies. The rising prevalence of hypertension, stroke risk, and age-related cerebrovascular disorders further supports demand. In addition, widespread access to advanced imaging systems and specialized neurosurgical centers continues to strengthen the country’s dominant market position.

Canada Strengthens Its Position in Advanced Intracranial Aneurysm Care

Canada intracranial aneurysms market is witnessing significant growth due to its advanced neurovascular healthcare infrastructure, increasing prevalence of endovascular treatments. Strong investments in neurological research, widespread availability of high-resolution diagnostic imaging, and growing use of flow diverters and embolization devices are enhancing treatment outcomes. Additionally, supporting government healthcare funding and expanding specialized stroke centers continue to drive market growth.

Asia Pacific captured 24% of the total market share in 2025 and is anticipated to grow at the fastest CAGR of 10.1% in the intracranial aneurysm market during the forecast period due to improving healthcare infrastructure, rising awareness of neurological disorders, and increasing access to advanced diagnostic and treatment technologies. Growing elderly population, higher incidence of hypertension and stroke-related conditions, along with expanding investments in healthcare facilities, are further accelerating market growth across the region.

India Market Trends

India is anticipated to grow at the fastest CAGR in the intracranial aneurysm market during the forecast period due to improving healthcare infrastructure, rising awareness of neurological disorders, and increasing access to advanced diagnostic imaging and minimally invasive treatments. A large patient population, growing incidence of hypertension and stroke-related conditions, along with higher investments in specialty hospitals and neurovascular care, are further accelerating market expansion.

China Accelerates Growth Through Advanced Neurovascular Innovation

China’s intracranial aneurysms market is expanding significantly due to the rising burden of cerebrovascular diseases, increasing healthcare expenditure, and rapid adoption of minimally invasive neurointerventional procedures. Growing investments in advanced medical technologies, expansion of tertiary hospitals, and wider availability of high-resolution diagnostic imaging are improving early detection and treatment. Additionally domestics medical devices innovation and supportive healthcare reforms are strengthening the country’s neurovascular care capabilities.

| Ecosystem Category | Key Participants | Role in Market |

| Technology Providers | Medtronic, Stryker, Terumo, Penumbra | Develop neurovascular intervention technologies and treatment platforms |

| Product Manufacturers | Medtronic, Stryker, MicroPort Scientific, Balt, Acandis | Manufacture coils, flow diverters, stents, catheters, embolization systems |

| Service Providers | Mayo Clinic, Cleveland Clinic, Mass General Brigham | Deliver aneurysm diagnosis, treatment, and patient management services |

| Platform Providers | Siemens Healthineers, GE HealthCare, Philips | Advanced imaging and angiography platforms for aneurysm detection and intervention |

| CROs | IQVIA, ICON plc, Medpace | Support clinical trials for neurovascular devices and therapies |

| Software Vendors | Viz.ai, RapidAI, Brainomix | AI-powered neuroimaging analysis and clinical decision support |

| Research Institutions | Mayo Clinic, Johns Hopkins University, Barrow Neurological Institute | Neurovascular research, clinical studies, device evaluation |

| End-User Industries | Hospitals, Specialty Clinics, Imaging Centers | Adoption and utilization of aneurysm diagnosis and treatment technologies |

Clinical Trials

R&D

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 24% | 8% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medtronic | Dublin | Ireland | Global neurovascular leader with broad aneurysm treatment portfolio | Pipeline Flex Embolization Device, coils, microcatheters |

| Stryker | Kalamazoo, Michigan | USA | Strong global presence in aneurysm intervention technologies | Neuroform Atlas, Target Coils, flow diversion systems |

| Terumo Corporation | Tokyo | Japan | Major supplier of neurovascular intervention devices | WEB Aneurysm Embolization System, microcatheters |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| MicroPort Scientific Corporation | Shanghai | China | Expanding neurovascular portfolio and APAC presence | Coil embolization systems, neurovascular implants |

| Balt | Montmorency | France | Specialized neurovascular device manufacturer | Silk flow diverters, aneurysm treatment systems |

| Acandis GmbH | Pforzheim | Germany | Strong European neurovascular specialization | Acclino, Acandis aneurysm solutions |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Viz.ai | San Francisco, California | USA | AI-enabled aneurysm and neurovascular imaging solutions | Viz Aneurysm platform |

| RapidAI | Menlo Park, California | USA | Advanced neuroimaging analytics | AI-assisted aneurysm detection software |

| Brainomix | Oxford | United Kingdom | Expanding neurovascular AI diagnostics | Brainomix 360 platform |

In October 2025, “With already limited NIH funding for brain aneurysm research now at risk, our ongoing support for this work has become even more critical,” “We must work to ensure that promising science receives the resources needed to become life-saving treatments. We are proud to support the remarkable work of these researchers and to know that the funds we raise go directly to those who can have the greatest impact in the field and for the patients”, said Christine Buckley, executive director of the BAF.

Strengths

Weaknesses

Opportunities

Threats

By Type

By Treatment Type

By End User

By Diagnosis Modality

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar