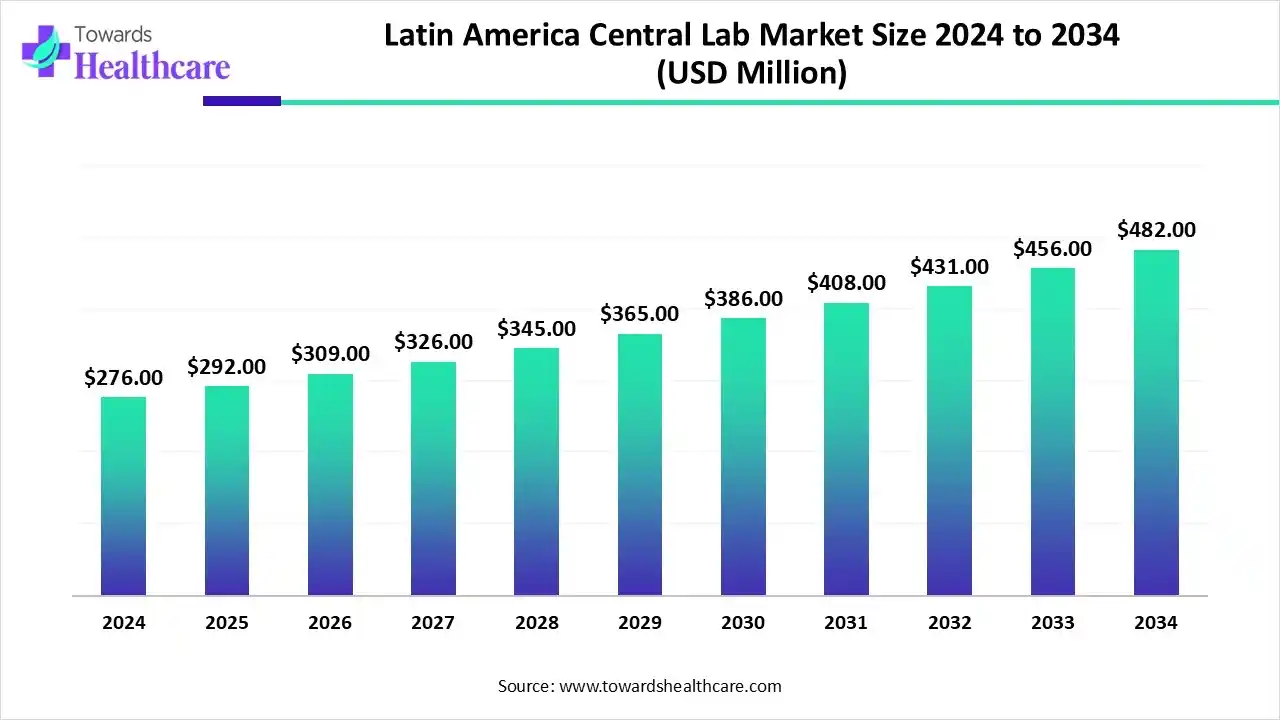

The Latin America central lab market size reached US$ 289.89 million in 2025 and is anticipate to increase to US$ 322.51 million in 2026. By 2035, the market is forecasted to achieve a value of around US$ 773.25 million, growing at a CAGR of 10.20%.

")

The Latin America central lab market is experiencing steady growth, driven by the rising number of clinical trials, expanding pharmaceutical and biotechnology sectors, and improved regulatory frameworks. Growing demand for high-quality diagnostic services and standardized testing supports this trend. Among regional countries, Brazil dominates the market due to its advanced healthcare infrastructure, skilled workforce, and strong government initiatives to promote clinical research and innovation.

The Latin America central lab market is expanding as global pharma companies increasingly outsource laboratory services to the region for cost efficiency and access to a diverse patient population. It is a network of specialized laboratories that support clinical trials by providing standardized testing, data management, and analytical services across the region.

The market is increasing due to its cost-effective operations, growing pool of treatment-naïve patients, and improving regulatory standards that attract global clinical trials. The region offers diverse patient demographics, faster recruitment rates, and expanding research infrastructure, making it an appealing destination for pharmaceutical and biotech companies. Additionally, increasing collaboration between international CROs and local labs further enhances efficiency and quality in clinical trial support services.

AI is transforming the Latin America central lab market by enhancing data accuracy, automating sample analysis, and improving turnaround times for clinical trial results. It enables predictive analytics, real-time monitoring, and efficient data management, reducing human error and operational costs. Additionally, AI-driven platforms support faster decision-making in drug development and patient safety assessment, positioning Latin America as a competitive hub for global clinical research and laboratory innovation.

| Company Name | Headquarters | Recent Product Focus |

| QIAGEN | Venlo, Netherlands | Focuses on the automated PCR system and its syndromic testing platforms |

| OPKO Health, Inc. | Miami, Florida, U.S. | Focus on the 4Kscore test, which helps to assess the risk for prostate cancer. |

| Charles River Laboratories | Wilmington, Massachusetts, U.S. | Focuses on advanced therapies like cell and gene therapy and accelerated digital-enabled drug development. |

| Genomics Health | Redwood City, California, U.S. | Major focus on targeted discovery and drug design for DNA and RNA therapies, and AI-powered solutions for genomic medicine |

| Quest Diagnostics | Secaucus, New Jersey, U.S. | The major focus area is oncology includes MRD and liquid biopsy tests, infectious tests, neurological biomarkers, and cardiometabolic panels. |

| Table | Scope |

| Market Size in 2026 | USD 322.51 Million |

| Projected Market Size in 2035 | USD 773.25 Million |

| CAGR (2025 - 2034) | 10.20% |

| Key Applications | Clinical diagnostics, oncology testing, infectious disease testing, genetic testing, clinical trials, companion diagnostics, pathology services, biomarker analysis, precision medicine |

| Primary End Users | Hospitals, physicians, pharmaceutical companies, CROs, biotechnology companies, academic institutions, government healthcare systems |

| Key Growth Drivers | Rising chronic diseases, increasing clinical trial activity, healthcare outsourcing, expansion of private healthcare networks, adoption of molecular diagnostics, precision medicine growth |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Clinical Trial Phase, By Modality, By End-User |

| Top Key Players | OPKO Health, Inc., Fresenius Medical Care AG & Co. KGaA, QIAGEN, Quest Diagnostics Incorporated, Charles River Laboratories, Laboratory Corporation of America Holdings (LabCorp), Genomic Health (Exact Sciences Corporation), DASA |

The Safety Testing Segment Was Dominant in the Market in 2025

In 2025, the safety testing segment accounted for 29.28% of the Latin America central lab market. Dominance is driven by the fastest expansion in clinical research, mainly in Brazil & Mexico, due to different patient populations, affordable trial implementation, & advanced research infrastructure. The emergence of stringent quality control regulations from regulatory bodies propels the need for the latest safety testing & rigorous adherence to GLP for drug approvals.

However, the genomic & molecular testing segment captured the second-largest share at 19.41% in 2025, due to strong demand for tailored therapies. These therapies need specialized biomarker analysis, companion diagnostics, & targeted variant identification for concerns, such as breast & ovarian cancer. Moreover, Latin America is enforcing an integration of NGS into its routine workflows, enabling central labs to process complex somatic panels & genomic profiles.

The pathology & histology services segment captured a 15.56% share of the Latin America central lab market in 2025. Emerging stress of the geriatric population & diverse chronic illnesses, like cancer, necessitate tissue-based diagnostics & histopathology for screening, staging, & monitoring this surging cancer patient pool. Developing staff shortages & rising sample volumes force central labs to execute high-throughput automated staining, microtomy, & diagnostic software systems.

Moreover, the specialty testing & biomarkers segment accounted for a 15.04% share in 2025 & is predicted to expand fastest at the 11.98% CAGR. Especially, the oncology sector, with patient stratification & effectiveness testing driving the demand for specialized diagnostic assays. Also, central laboratories require operating biomarker analyses, pharmacogenomic testing, & next-generation sequencing (NGS). In addition, the region is fostering robust strategic alliances to introduce specialized capability at the domestic level.

The Oncology Segment Led the Market in 2025

In 2025, the oncology segment dominated with 28.25% of the Latin America central lab market. Key drivers are the increasing prevalence of cancer, due to a massive rise in the ageing population & urbanization, along with elevating use of monoclonal antibodies, checkpoint inhibitors, & targeted therapies. The regional cancer trials are increasingly leveraging genomic sequencing, tumor profiling, & immunohistochemistry, while central labs ensure that these tests are viable, consistent, & compliant with regulatory guidelines across different trial sites.

Whereas the infectious diseases segment held the second-largest share of 27.60% in 2025, due to the high incidence of diseases like dengue, Zika, & tuberculosis in Latin America. Central laboratories play a pivotal role in disease surveillance & outbreak management, driving the growth of this segment in the region. Furthermore, the region promoting incentives powered by the WHO/PAHO is propelling local governments to empower diagnostic networks & surveillance capabilities to prevent the threat of these emerging cases.

In 2025, the cardiovascular & metabolic diseases segment captured 21.70% of the Latin America central lab market. The segmental growth is mainly fueled by expedited urbanization, socioeconomic imbalance, & a high regional propensity to insulin resistance at minimal levels of abdominal obesity. Many regional labs are offering tests for ApoB, Lp(a), & triglyceride-rich remnants to assess residual cardiovascular risk.

The rare diseases & genetic disorders segment held a 3.32% share in 2025 & is estimated to expand at a rapid CAGR of 12.31% in the market. Growing adoption of non-invasive diagnostic methods drives the segmental expansion. Between 26 and 50 million people in this region are living with these disorders, while central labs are advancing their facilities to include modern molecular & biomarker testing. This is raising complex genetic sequencing & gene mutation mapping that acts as a significant factor for accurate, early diagnosis.

The Phase III (Late Phase) Segment Dominated the Market in 2025

In 2025, the Phase III (late phase) segment led with a 47.26% share of the Latin America central lab market. This phase is playing a major role in the development of oncology, infectious diseases, & cardiometabolic disorders areas. Specifically, Brazil, Mexico, Colombia, & Argentina are widely providing late-phase trials with operational cost benefits & rapid patient recruitment timelines.

The Phase I&II (early phase) segment accounted for the second-largest share of 39.72% in 2025 & is anticipated to expand at a 10.81% CAGR. A substantial growth in precision medicine & complex cancer therapies necessitates sensitive, exploratory testing, which fuels higher investments in early drug assessment. Besides this, diverse regulatory bodies, like ANVISA in Brazil & COFEPRIS in Mexico, have actively simplified approval processes, which makes multi-regional trials easier to implement.

The Phase IV (post-marketing surveillance) segment held a notable share of 13.02% of the Latin America central lab market. A key driver is Brazil’s ANVISA & Mexico's COFEPRIS demand for consistent, strong post-marketing safety data & foster localized Qualified Persons for Pharmacovigilance (QPPV) requirement. The diverse patient age groups & affordable clinical trial services are evolving this region as highly attractive to conduct large-scale Phase IV registries & observational cohorts.

The Small Molecules Segment Led the Market in 2025

In 2025, the small molecules segment captured a major share of 37.39% of the market. These molecules are acting as the backbone of unbranded & branded generics, which bolsters a share of the Latin American pharmaceutical industry. Alongside rising cases of cardiovascular diseases, diabetes, & cancer, primarily in Brazil, Mexico, Argentina, & Colombia, are persistently driving demand for accessible, orally administered small-molecule therapeutics.

Whereas the biologics (large molecules) segment captured the second-largest share of 30.44% of the Latin America central lab market in 2025. A major catalyst is local healthcare systems & governments in nations, such as Brazil & Argentina, which highly prefer biosimilars to strengthen patient access & control healthcare expenditures. This further needs comprehensive bioequivalence & immunogenicity testing. The market is boosting a focus on the progression of monoclonal antibodies & immune checkpoint inhibitors, facilitating highly specific treatments for complex diseases.

Moreover, the advanced therapies (ATMP) segment held a 18.07% share in 2025 & is predicted to expand at a 13.99% CAGR. The emergence of mature regulatory landscapes, significantly in Brazil & Mexico, is enabling complex ATMP trials to be processed rapidly. The latest ATMPs are providing curative options instead of just symptom management, propelling both patient & physician advocacy for localized access.

The vaccines segment accounted for a 14.10% share of the Latin America central lab market in 2025, due to a huge burden of different infectious diseases, such as dengue, rotavirus, & pneumococcal infections, which detect the types of vaccines being tested & localized. Specifically, the Pan American Health Organization (PAHO) Revolving Fund ensures affordable & equitable access to essential vaccines across member states.

The Pharmaceutical & Biotechnology Companies Segment Dominated the Market in 2025

The pharmaceutical & biotechnology companies segment led with a 62.67% share of the market in 2025. Major drivers include global pharmaceutical leaders that raise outsourcing of API & drug production to regional hubs in Brazil & Mexico to reduce logistical risks, lower costs, & benefit from trade agreements. Surging use of robust scientific capacity to manufacture & distribute cost-effective biologic therapies drives the respective company’s development.

The contract research organizations (CROs) segment accounted for a 16.88% share in 2025 & is estimated to expand at a 11.58% CAGR in the Latin America central lab market. CROs are highly facilitating rapid patient recruitment, cost-effective trial exploration, & access to large, various, & untreated patient populations. Also, they enable sponsors to simplify clinical development while following local regulatory pathways efficiently.

In 2025, the academic & government research institutes segment held an 11.52% share, due to government health ministries & public institutions highly spurring R&D in genomics, biotechnology, & tropical infectious diseases by offering localized healthcare priorities. While state-backed research institutes & national commissions, like the Argentine National Atomic Energy Commission, promote regional scientific breakthroughs via alliances on cross-border infrastructure.

The clinical diagnostics laboratories segment held an 8.93% share of the Latin America central lab market in 2025. These laboratories are providing enhanced patient outcomes by allowing early disease detection, controlling chronic conditions, & reducing healthcare expenditures. Many labs are expeditiously incorporating automation, digital pathology, & Laboratory Information Management Systems (LIMS) to lower human error, enable remote specialist consultations, & foster AI use in tailored medicine.

In 2025, Brazil registered dominance with a 50.91% share of the Latin America central lab market. In 2025, Brazil's Ministry of Health implemented the Clinical Research Law, aiming to modernize the clinical research framework. This legislation reduces the approval process for clinical trials from up to six months to 30 days, enhancing efficiency and attracting international investments. With a population of approximately 214 million, Brazil's diverse genetic and cultural landscape offers unique opportunities for clinical research, positioning the country as a strategic hub for laboratory-based studies in Latin America.

Why is the Market Expanding in the Rest of Latin America?

The rest of Latin America captured a 29.64% share in 2025 & is predicted to witness rapid expansion at an 11.58% CAGR during 2026-2035. The Latin America central lab market is capturing a significant share and witnessing rapid expansion due to a surge in regional clinical trial outsourcing, cost-efficient trial execution, and a large, diverse patient population. Countries are actively investing in local healthcare infrastructure and diagnostic capabilities to meet global pharmaceutical research demands.

How is Mexico Approaching the Latin America Central Lab Market?

Mexico is approaching the market by expanding partnerships with local laboratories and enhancing molecular and genomic testing capabilities. The company focuses on integrating advanced diagnostic technologies with regional laboratory networks to improve testing efficiency and accessibility. These initiatives aim to support public health programs, infectious disease monitoring, and research initiatives across Latin America. By leveraging local expertise and standardized protocols, MaxiCo seeks to strengthen centralized laboratory services and accelerate market growth.

How is Argentina Accelerating the Latin America Central Lab Market?

Argentina accounted for a 19.45% share of the Latin America central lab market in 2025. Argentina is accelerating the market by expanding its network of accredited central laboratories and promoting molecular and genomic testing across the country. The Ministry of Health has enhanced laboratory infrastructure to support infectious disease monitoring and public health programs, increasing testing coverage nationwide. These initiatives improve diagnostic capabilities, enable faster disease detection, and strengthen the country’s role as a key hub for centralized laboratory services in Latin America.

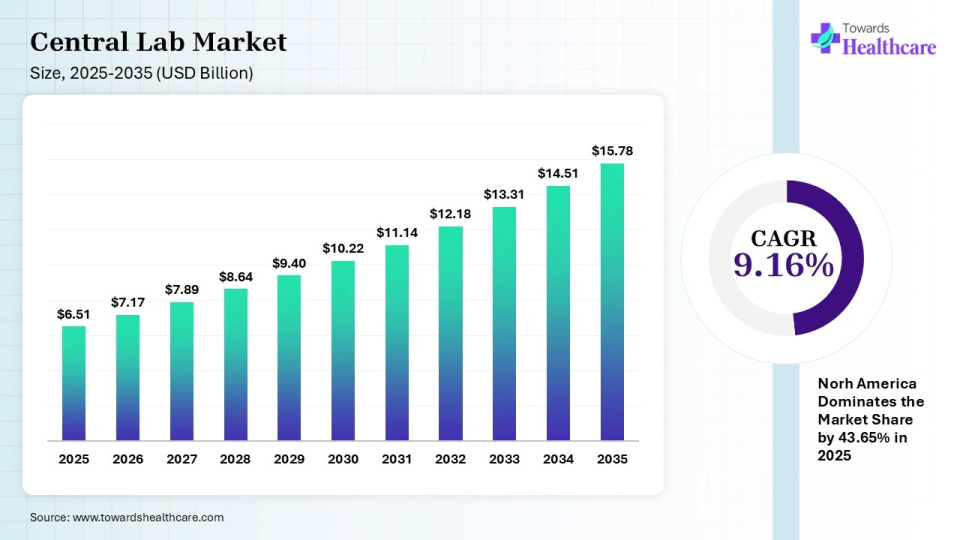

The global central laboratory market is valued at USD 7.17 billion in 2026 and is projected to reach USD 15.78 billion by 2035, growing at a CAGR of 9.16% between 2026 and 2035, driven by increasing investments in R&D and a growing demand for clinical trials.

")

| Category | Market Participants & Role |

| Technology Providers | Diagnostic equipment companies providing analyzers, molecular testing platforms, automation systems, laboratory instruments |

| Product Manufacturers | Companies manufacturing reagents, assays, diagnostic kits, pathology products, molecular testing solutions |

| Service Providers | Central laboratories performing outsourced diagnostic testing and clinical trial sample analysis |

| Platform Providers | Laboratory information systems (LIS), healthcare IT platforms, digital pathology systems |

| CROs/CDMOs | Clinical research organizations supporting pharmaceutical trials with central laboratory services |

| Software Vendors | Laboratory automation, data management, AI diagnostics, workflow optimization platforms |

| Research Institutions | Universities, medical research centers, genomic research organizations |

| End-User Industries | Hospitals, pharma, biotech, clinical research, public health organizations |

Clinical Trials

Regulatory approvals

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 70% | 20% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Quest Diagnostics | Secaucus, New Jersey, USA | United States | One of the world's largest diagnostic laboratory companies with international operations and partnerships supporting Latin American diagnostic demand | Clinical diagnostics, molecular testing, pathology, specialty testing, clinical trial laboratory services |

| Labcorp | Burlington, North Carolina, USA | United States | Global laboratory leader with strong clinical research and diagnostic capabilities serving pharmaceutical and healthcare customers | Central laboratory services, clinical trials, genomic testing, oncology diagnostics |

| Fresenius Medical Care | Bad Homburg, Germany | Germany | Operates healthcare services globally and participates in Latin American healthcare infrastructure | Laboratory-related healthcare services, diagnostics support |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| SYNLAB | Munich, Germany | Germany | Major international laboratory group with Latin American presence through diagnostic networks | Clinical diagnostics, pathology, laboratory outsourcing |

| Laboratorio Médico del Chopo | Mexico City, Mexico | Mexico | Leading Mexican laboratory chain providing diagnostic testing services | Clinical laboratory testing, preventive diagnostics |

| Bio-Manguinhos | Rio de Janeiro, Brazil | Brazil | Important Latin American biotechnology and diagnostics organization | Diagnostic kits, molecular testing, public health diagnostics |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Grupo Diagnóstico Aries | Mexico City, Mexico | Mexico | Regional diagnostic provider expanding laboratory services | Clinical laboratory testing |

| Laboratorio Clínico Roe | Lima, Peru | Peru | Established Peruvian laboratory network | Routine diagnostics, specialized testing |

| Laboratorio Médico Polanco | Mexico City, Mexico | Mexico | Long-standing diagnostic provider in Mexico | Clinical testing, preventive diagnostics |

By Service / Offering

By Test / Technology Type

By End-User / Customer

By Sample Type

By Therapeutic Area / Application

By Business / Operating Model

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar