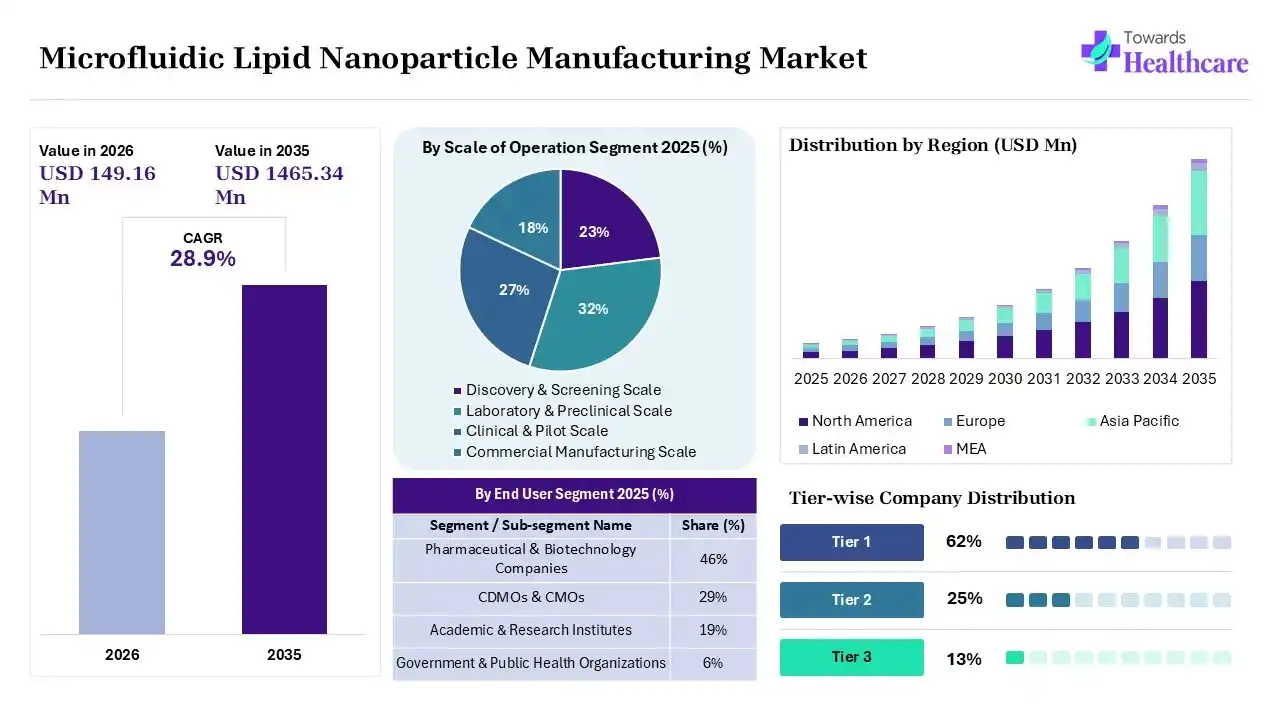

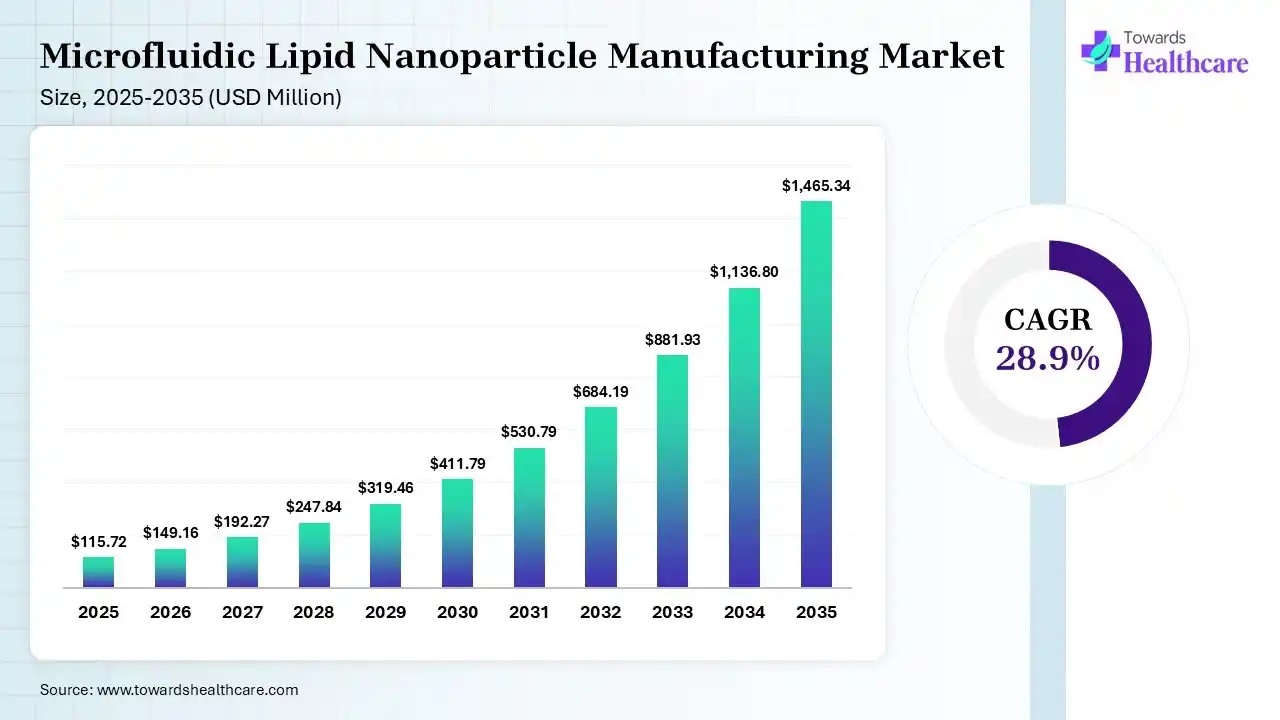

The global microfluidic lipid nanoparticle manufacturing market size is calculated at USD 115.72 million in 2025, driven by increasing demand for mRNA therapeutics. The market continues to grow USD 149.16 million in 2026 due to the growing nucleic acid pipeline, demand for single-use manufacturing systems, and AI integration. It is expected to reach USD 1465.34 million by 2035, expected to maintain a CAGR of 28.9% from 2026 to 2035 as continued healthcare digitization, technological advancements, and expanding applications accelerate market expansion. North America accounted for 43% of the market in 2025 due to high healthcare investments, leading biotechnology hubs, and established CDMO ecosystems.

")

")

The microfluidic lipid nanoparticle manufacturing market is driven by growing demand for mRNA, increasing adoption of genetic medicines, and technological advancements. Microfluidic lipid nanoparticle manufacturing refers to the process of producing lipid nanoparticles with the use of microfluidic technologies, which help in precise mixing of lipids and therapeutic agents. They help in the delivery of mRNA, gene therapies, siRNA therapeutics, DNA therapies, cancer therapies, and rare disease treatment.

The approval of liposomes in 1995 increased the demand for their large-scale manufacturing processes, where the growth in the use of microchannels also increased the innovations of microfluidic technologies between 2017 and 2022. Additionally, growth in the applications of LNP also encouraged the development of single-use manufacturing systems.

The growing R&D activities focused on LNP formulations are increasing the demand for microfluidic lipid nanoparticle manufacturing systems. They are also being used in the development of mRNA and gene therapies, where growth in the use of vaccines are also increasing their adoption rates.

Commercial Opportunity Created by the Expanding RNA Therapeutics Pipeline

Focuses on the mRNA, siRNA, saRNA, gene-editing, and other nucleic acid pipelines translating into demand for microfluidic LNP manufacturing technologies.

Transition from Platform Sales to Recurring Consumables and Service Revenue

Involves opportunities created by single-use cartridges, chips, consumables, software, maintenance, process-development support, and other recurring revenue models.

Emerging Opportunity in Clinical-to-Commercial Scale-Up

The ability to maintain particle quality and process consistency during scale-up represents a major commercial opportunity and competitive differentiator.

Technology Adoption and Manufacturing Transformation in Microfluidic LNP Production

Focus on advances in microfluidics, automation, process control, and continuous manufacturing is changing LNP development and production economics.

Comparison of Major Microfluidic Mixing Technologies and Their Commercial Suitability

It compares staggered herringbone mixing, hydrodynamic flow focusing, T- and Y-junction mixing, chaotic advection micromixers, and impingement jet microfluidics based on throughput, reproducibility, scalability, and application suitability.

Shift Toward Continuous and Parallelized Scale-Out Manufacturing

Manufacturers are addressing throughput limitations through continuous processing and parallelized microfluidic architectures, driving the market growth.

Role of Closed, Automated, and Single-Use Manufacturing Systems

The closed, automated, and single-use manufacturing systems enhance efficiency, scalability, consistency, sterility, and regulatory compliance.

Artificial Intelligence, Automation, and Digital Process Control in LNP Manufacturing

Based on our research, digital technologies are improving formulation development, process optimization, manufacturing control, and quality assurance.

AI-Assisted Formulation Design and Experimental Optimization

AI helps in optimizing lipid composition and flow rates, which increases their demand. They also help in optimization of mixing parameters, particle size, and encapsulation efficiency.

Real-Time Process Monitoring and Predictive Manufacturing Control

The companies are using sensors and process analytical technology to enhance manufacturing consistency. Additionally, automated feedback systems and predictive analytics are also being used for real-time process monitoring and predictive manufacturing control.

Digital Data Infrastructure for Process Development and Technology Transfer

The growth in digital transformation is driving the development of standardized process supporting scale-up, regulatory documentation, manufacturing transfer, and multi-site production.

Growing Demand for Commercial-Scale Microfluidic Manufacturing Platforms

The movement beyond laboratory systems toward high-throughput platforms capable of supporting clinical and commercial production is increasing the use of microfluidic manufacturing platforms, where demand for RNA-based therapeutics is also driving the demand for commercial-scale microfluidic manufacturing platforms.

Rising Adoption of Single-Use Microfluidic Chips and Fluid Paths

To reduce the chances of contamination and enhance manufacturing speed and flexibility, the demand as well as the adoption of single-use microfluidic chips and fluid paths are increasing.

Expansion of LNP Applications Beyond Conventional mRNA Vaccines

Growing applications in gene editing, cancer vaccines, protein replacement, rare diseases, and other advanced therapeutics are driving the demand for microfluidic lipid nanoparticle manufacturing systems.

Increasing Outsourcing of LNP Development and Manufacturing to CDMOs

Biotechnology companies are using specialist service providers to access advanced infrastructure, specialized equipment, and reduce capacity investment requirements, which are promoting outsourcing of LNP development and manufacturing to CDMOs.

Market Drivers Supporting Rapid Commercial Expansion

The growth in the RNA therapeutic pipelines, non-viral delivery demand, precision manufacturing requirements, biotechnology funding, and investment in advanced biomanufacturing are some of the major microfluidic lipid nanoparticle manufacturing market drivers.

Market Restraints Limiting Broader Adoption

High equipment costs, scale-up complexity, specialized expertise requirements, intellectual property constraints, and evolving regulatory expectations act as the market restraints.

Operational and Commercial Challenges Facing Market Participants

Growth in throughput limitations, process transfer, raw-material consistency, manufacturing validation, and integration with downstream processing are some of the challenges faced by the market participants.

High-Value Opportunities for Existing Companies and New Entrants

Emerging opportunities in commercial-scale systems, modular manufacturing, single-use technologies, analytics, CDMO services, and emerging geographic markets are creating new opportunities and enhancing the market expansion.

Demand at Discovery and High-Throughput Formulation Screening Stages

The rise in demand at discovery and high-throughput formulation screening stages focuses on the requirements for low-volume, flexible, high-throughput systems used to compare lipid compositions and formulation parameters.

Demand During Preclinical and Clinical Development

Demand during preclinical and clinical development for microfluid lipid nanoparticle manufacturing is driven by growing need for reproducibility, GMP compatibility, process transferability, and controlled scale-up.

Demand for Commercial Manufacturing and Long-Term Production Capacity

Demand for commercial manufacturing and long-term production capacity depends on requirements for throughput, automation, reliability, continuous operation, quality control, and validated manufacturing systems.

Performance Criteria Driving Platform Selection

The performance criteria driving platform selection are based on the importance of particle-size consistency, encapsulation efficiency, throughput, batch reproducibility, payload flexibility, and process yield.

Operational and Economic Criteria Influencing Purchasing Decisions

System price, consumable costs, ease of operation, scalability, maintenance, validation requirements, and total cost of ownership drive the operational and economic criteria influencing purchasing decisions.

Supplier Selection Criteria for Regulated Manufacturing Environments

Supplier selection criteria for regulated manufacturing environments depend on the importance of GMP compatibility, technical support, documentation, system reliability, regulatory experience, and long-term supply assurance.

Pricing Structure Across Benchtop, Pilot-Scale, and Commercial Systems

The pricing structure across benchtop, pilot-scale, and commercial systems compares pricing logic across different manufacturing scales and focuses on advanced technologies, GMP compliance, and regulatory requirements that create premium pricing.

Recurring Revenue Potential from Chips, Cartridges, and Consumables

The strategic importance of installed equipment bases and recurring consumable demand are responsible for recurring revenue potential from chips, cartridges, and consumables.

Service, Software, and Process Development Revenue Opportunities

Service, software, and process development revenue opportunities involve additional revenue streams from formulation support, software subscriptions, maintenance, training, and technology transfer

Critical Raw Materials and Components Required for Microfluidic Systems

The critical raw materials and components required for microfluidic systems involve microfluidic chips, pumps, sensors, tubing, connectors, single-use assemblies, specialized materials, and control components.

Supply Dependencies in Lipids and Nucleic Acid Manufacturing

The supply dependencies in lipids and nucleic acid manufacturing focus on the availability and quality of ionizable lipids, helper lipids, PEG-lipids, RNA, and other inputs that affect manufacturing operations.

Supply Chain Risks and Localization Opportunities

Supply chain risks and localization opportunities are driven by supplier concentration, lead times, quality requirements, regional manufacturing capacity, and opportunities for localized supply networks.

Upstream Technology and Component Suppliers

Platform Developers and Equipment Manufacturers

CDMOs, Pharmaceutical Companies, and Biotechnology Developers

Research Institutions and Technology Commercialization Networks

GMP Requirements for Clinical and Commercial LNP Manufacturing

GMP requirements for clinical and commercial LNP manufacturing involve closed processing, contamination control, documentation, validation, reproducibility, and manufacturing consistency.

Regulatory Expectations for Critical Quality Attributes

Regulatory expectations for critical quality attributes evaluate requirements related to particle size, size distribution, encapsulation efficiency, potency, purity, and batch consistency.

Process Validation and Technology Transfer Challenges

The process validation and technology transfer challenges cover regulatory and operational challenges involved in moving formulations between equipment platforms and manufacturing scales.

Investment in RNA Therapeutics and Non-Viral Delivery Platforms

Investment in RNA therapeutics and non-viral delivery platforms are driven by venture capital, pharmaceutical investment, and public funding, influencing demand for LNP manufacturing infrastructure.

Expansion of CDMO and In-House LNP Manufacturing Capacity

Expansion of CDMO and in-house LNP manufacturing capacity is driven by major capacity additions and their implications for equipment suppliers and service providers.

Investment Priorities Across North America, Europe, and Asia-Pacific

Investment priorities across North America, Europe, and Asia-Pacific focus on regional investment patterns and strategies important for expanding manufacturing capabilities.

High-Throughput and Commercial-Scale Microfluidic Platform Innovation

High-throughput and commercial-scale microfluidic platform innovation focuses on increasing production capacity without compromising nanoparticle quality.

Integrated End-to-End LNP Manufacturing Systems

Integrated end-to-end LNP manufacturing systems combine mixing, downstream processing, analytics, and aseptic handling within closed manufacturing workflows, increasing their adoption.

Next-Generation Microfluidic Architectures for New Payloads

The growing technology requirements for gene-editing components, saRNA, complex nucleic acids, and emerging therapeutic payloads are driving the demand for next-generation microfluidic architectures for new payloads.

| Table | Scope |

| Market Size in 2026 | USD 149.16 Million |

| Projected Market Size in 2035 | USD 1465.34 Million |

| CAGR (2026 - 2035) | 28.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product & Offering, By Mixing Technology, By Scale of Operation, By Workflow, By Payload Type, By Application, By End User, By Region |

| Top Key Players | Danaher Corporation, Elveflow, Merck KGaA, IDEX Corporation, PreciGenome LLC |

")

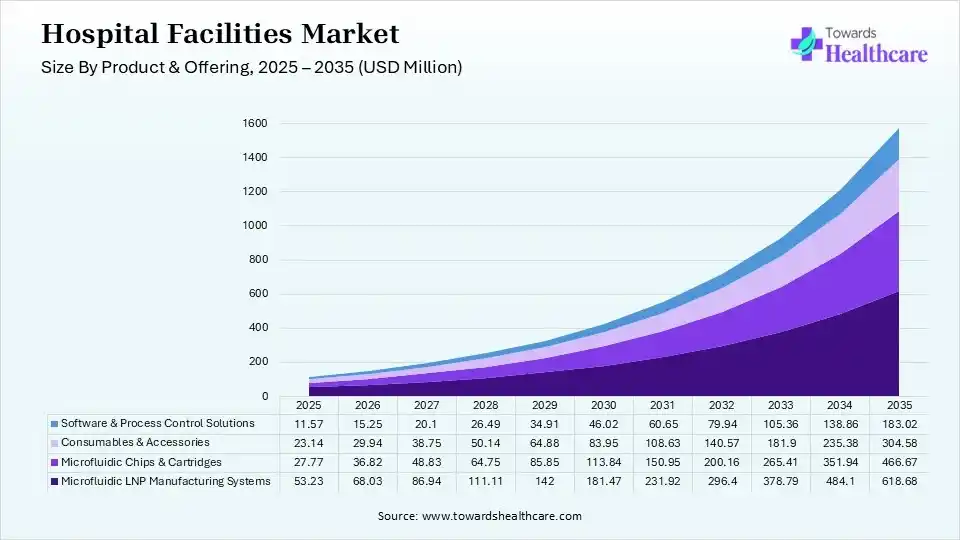

| Segment | Share 2025 (%) |

| Microfluidic LNP Manufacturing Systems | 46% |

| Microfluidic Chips & Cartridges | 24% |

| Consumables & Accessories | 20% |

| Software & Process Control Solutions | 10% |

The Microfluidic LNP Manufacturing Systems Segment Dominated the Market With 46% in 2025

The microfluidic LNP manufacturing systems segment held the largest revenue share of 46% of the market in 2025, as drug developers deploy integrated systems to improve formulation reproducibility. Scalable platforms accelerated translation from research to clinical manufacturing. Automation also reduced operator-dependent variability, which increased their use.

The microfluidic chips & cartridges segment held the second-largest share of 24% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to witness the fastest growth with a CAGR of 32.60% during the forecast period, driven by single-use formats that reduce cross-contamination and cleaning requirements. Rapid formulation screening also increases cartridge consumption. Scale-out manufacturing expands demand for disposable flow paths.

")

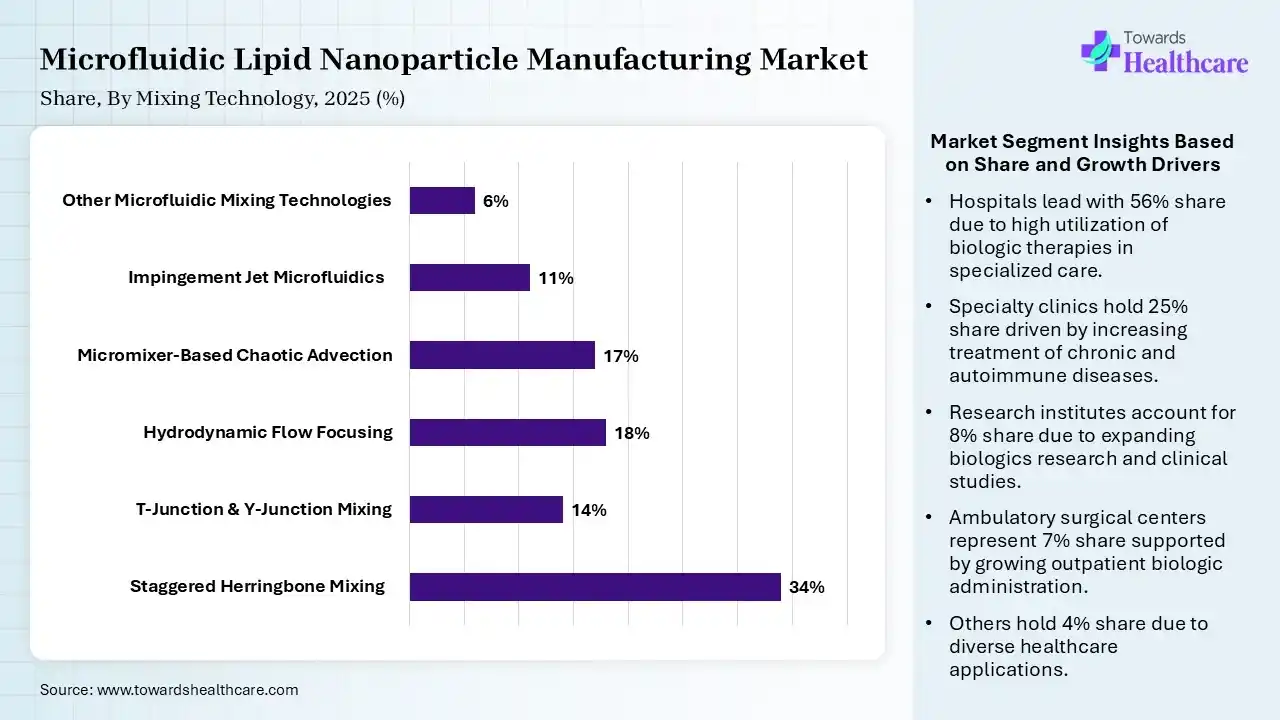

| Segment | Share 2025 (%) |

| Staggered Herringbone Mixing | 34% |

| T-Junction & Y-Junction Mixing | 14% |

| Hydrodynamic Flow Focusing | 18% |

| Micromixer-Based Chaotic Advection | 17% |

| Impingement Jet Microfluidics | 11% |

| Other Microfluidic Mixing Technologies | 6% |

The Staggered Herringbone Mixing Segment Dominated the Market With 34% in 2025

The staggered herringbone mixing segment accounted for the highest revenue share of 34% of the market in 2025, driven by chaotic advection, which enabled rapid and reproducible lipid-payload mixing. Established commercial platforms supported their broad adoption. Precise flow control also improved particle-size uniformity.

The impingement jet microfluidics segment held the second-largest share of 11% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to show the highest growth with a CAGR of 33.70% during the forecast period, due to high-throughput mixing supporting larger manufacturing volumes. Continuous processing also improves production efficiency. Commercial RNA programs also increase demand for scalable architectures.

| Segment | Share 2025 (%) |

| Discovery & Screening Scale | 23% |

| Laboratory & Preclinical Scale | 32% |

| Clinical & Pilot Scale | 27% |

| Commercial Manufacturing Scale | 18% |

The Laboratory & Preclinical Scale Segment Dominated the Market With 32% in 2025

The laboratory & preclinical scale segment led the market with 32% share in 2025, as preclinical programs required reproducible small-batch manufacturing. Researchers increasingly replaced bulk mixing with microfluidics. Growth in LNP libraries also expanded formulation workloads.

The commercial manufacturing scale segment held the second-largest share of 18% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to expand rapidly with a CAGR of 34.20% during the forecast period, due to continuous and parallelized manufacturing increasing production capacity. Commercial RNA therapeutics require reproducible large-volume output. Manufacturers are also investing in closed automated systems.

| Segment | Share 2025 (%) |

| Lipid Preparation | 13% |

| Nucleic Acid/Active Payload Preparation | 12% |

| Microfluidic Mixing & Nanoparticle Formation | 31% |

| Downstream Processing | 20% |

| Fill-Finish & Aseptic Handling | 14% |

| Process Analytical Technology & Quality Control | 10% |

The Microfluidic Mixing & Nanoparticle Formation Segment Dominated the Market With 31% in 2025

The microfluidic mixing & nanoparticle formation segment held a major revenue share of 31% of the market in 2025, as direct mixing controlled LNP size and encapsulation performance. Microfluidics delivered superior process reproducibility, which increased their use. Manufacturers also prioritized precise flow-rate control.

The process analytical technology & quality control segment held the second-largest share of 10% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to expand rapidly with a CAGR of 34.50% during the forecast period, driven by real-time analytics improving process understanding and consistency. Continuous manufacturing requires rapid quality monitoring, increasing their demand. Automation also enables data-driven process control.

")

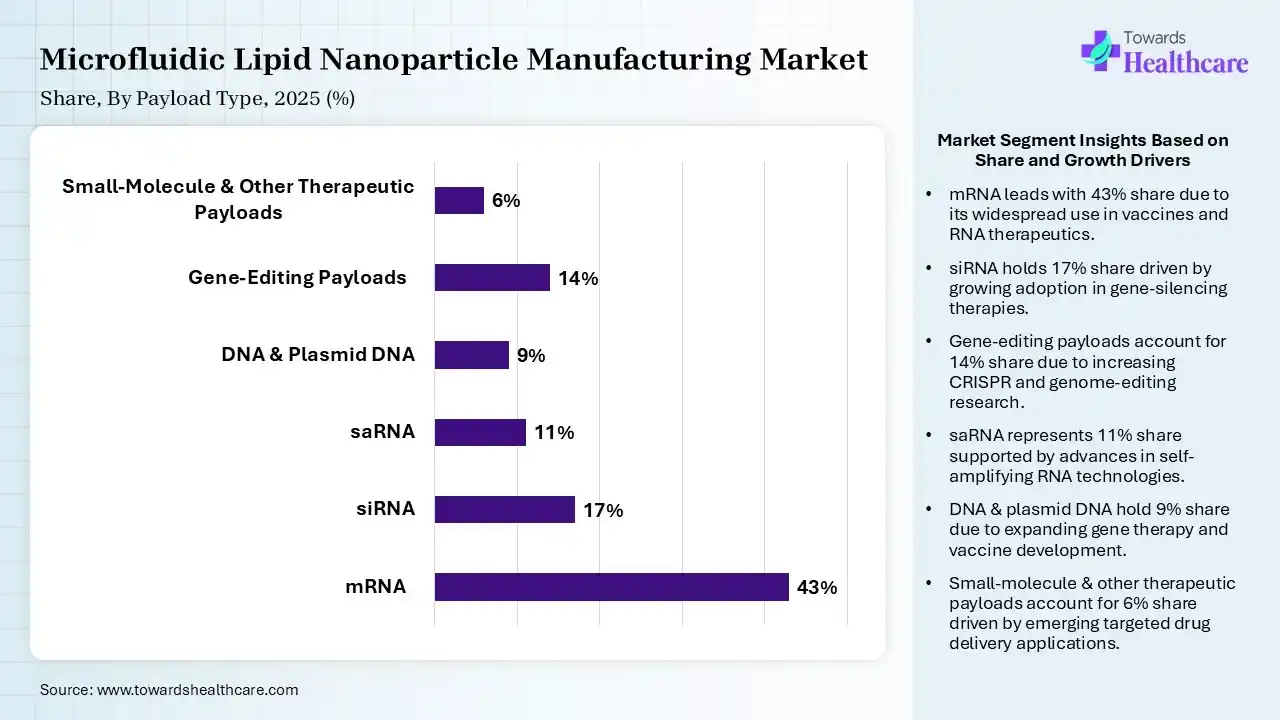

| Segment | Share 2025 (%) |

| mRNA | 43% |

| siRNA | 17% |

| saRNA | 11% |

| DNA & Plasmid DNA | 9% |

| Gene-Editing Payloads | 14% |

| Small-Molecule & Other Therapeutic Payloads | 6% |

The mRNA Segment Dominated the Market With 43% in 2025

The mRNA segment accounted for the highest revenue share of 43% of the market in 2025, driven by growth in vaccine and therapeutic pipelines, which sustained strong formulation demand. LNPs remained a leading delivery system for mRNA. Personalized oncology programs broaden application opportunities, which increased their use.

The gene-editing payloads segment held the second-largest share of 14% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to expand rapidly with a CAGR of 36.10% during the forecast period, as CRISPR programs require safe non-viral delivery technologies. Transient delivery can reduce prolonged nuclease exposure. Growing in vivo gene editing expands LNP manufacturing demand.

")

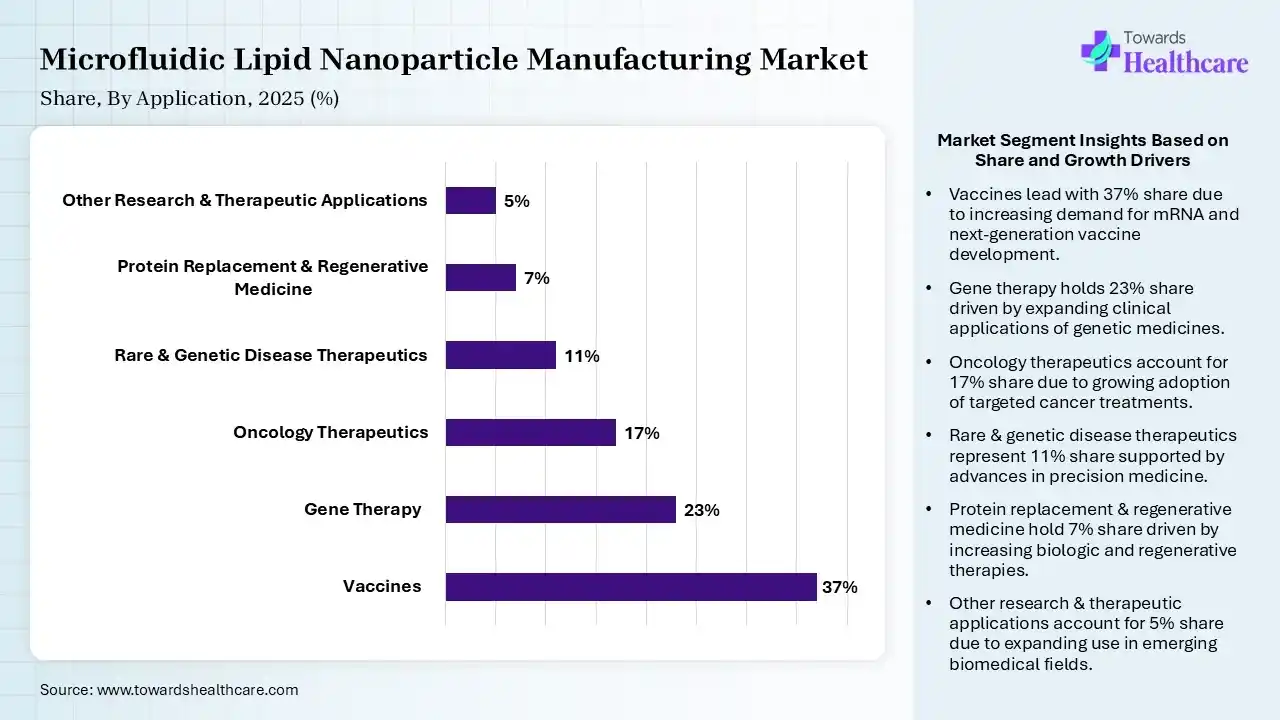

| Segment | Share 2025 (%) |

| Vaccines | 37% |

| Gene Therapy | 23% |

| Oncology Therapeutics | 17% |

| Rare & Genetic Disease Therapeutics | 11% |

| Protein Replacement & Regenerative Medicine | 7% |

| Other Research & Therapeutic Applications | 5% |

The Vaccines Segment Dominated the Market With 37% in 2025

The vaccines segment held a major revenue share of 37% of the market in 2025, as mRNA vaccine platforms sustained demand for reproducible LNP production. Cancer vaccine pipelines broaden the addressable market. Rapid-response vaccine development favored flexible microfluidic systems adoption.

The gene therapy segment held the second-largest share of 23% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to expand rapidly with a CAGR of 35.20% during the forecast period, due to non-viral delivery gaining importance in gene editing and replacement. In vivo therapeutic programs are also expanding rapidly, increasing their demand. LNP platforms reduce dependence on viral vectors.

")

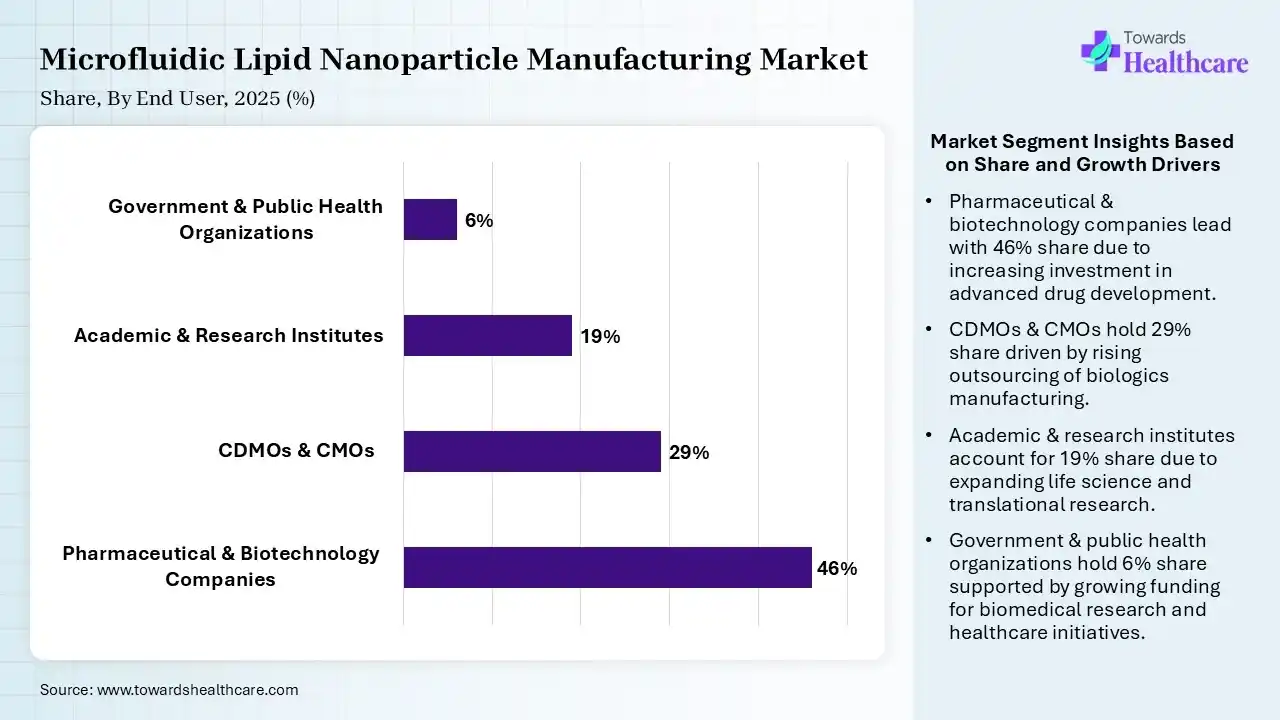

| Segment | Share 2025 (%) |

| Pharmaceutical & Biotechnology Companies | 46% |

| CDMOs & CMOs | 29% |

| Academic & Research Institutes | 19% |

| Government & Public Health Organizations | 6% |

The Pharmaceutical & Biotechnology Companies Segment Dominated the Market With 46% in 2025

The pharmaceutical & biotechnology companies segment contributed the biggest revenue share of 46% of the market in 2025, driven by expansion of RNA and gene therapy pipelines, which increased internal manufacturing demand. Growth in the companies' investment in proprietary formulation capabilities also increased their demand. Microfluidics accelerated candidate optimization.

The CDMOs & CMOs segment held the second-largest share of 29% of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to gain the highest share with a CAGR of 34.10% during the forecast period, due to drug developers increasingly outsourcing specialized LNP manufacturing. CDMOs expand GMP RNA production capacity, increasing the demand for microfluidic lipid nanoparticle manufacturing systems. Multi-client platforms also improve manufacturing economics.

")

")

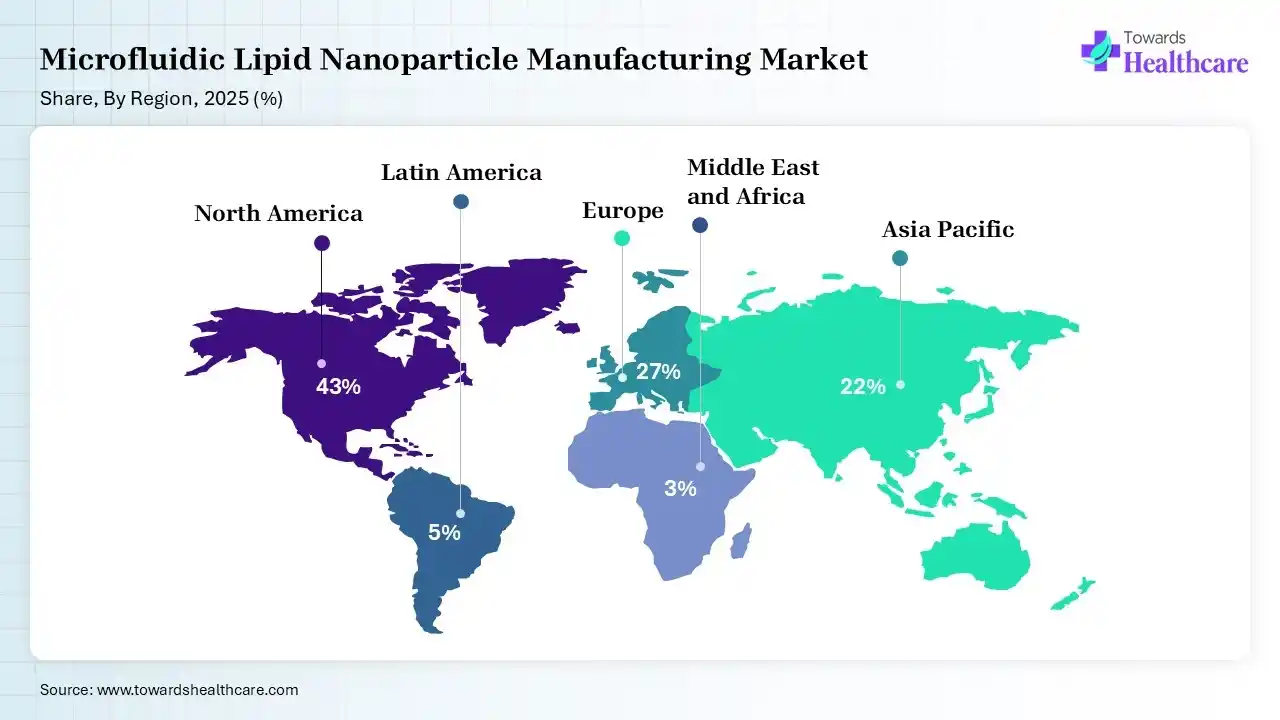

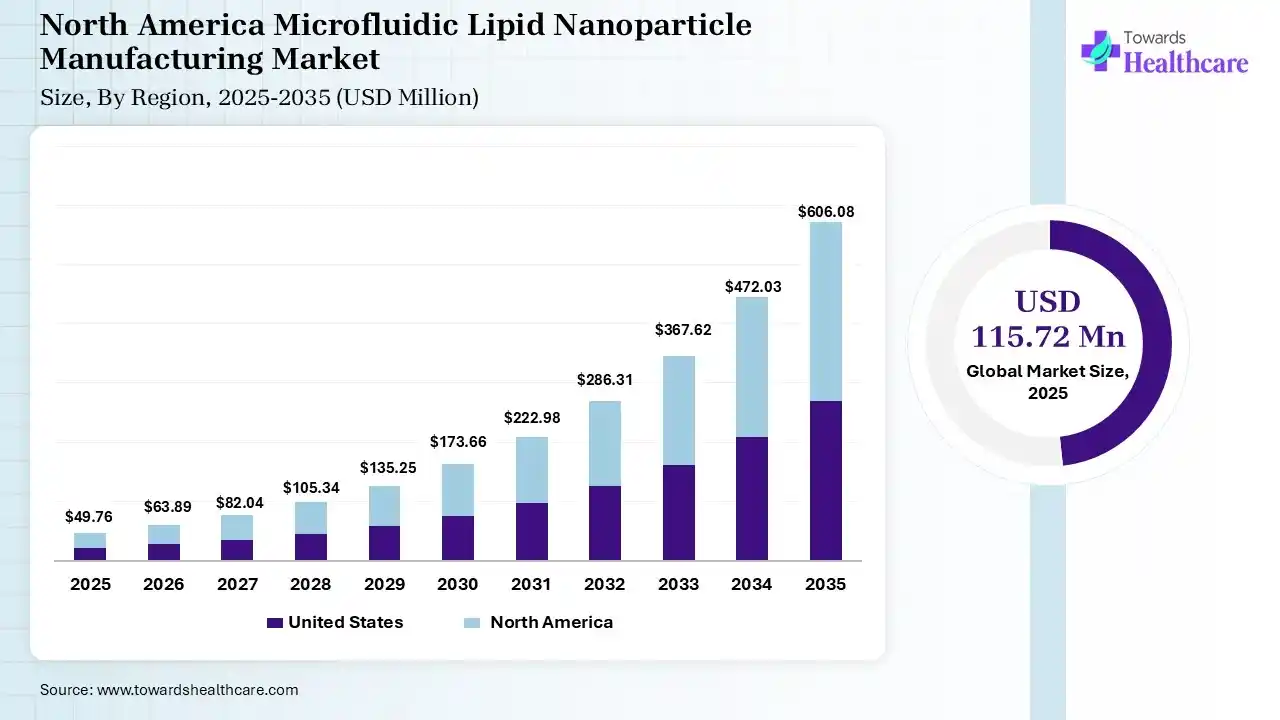

North America dominated the market with 43% in 2025, due to strong RNA therapeutics investment, which sustained technology adoption. Leading biotechnology clusters accelerated platform commercialization, where established CDMO capacity also supported clinical manufacturing. Growth in government funding also increased the adoption of various microfluidic manufacturing technologies, where continuous innovations focused on drug delivery technologies and nanomedicines also increased their demand. Rise in drug development and expansion of biomanufacturing facilities also increased their use, which contributed to the market growth.

US Market Growth

U.S. held a 37% share of the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to grow with the highest CAGR of 28.80% during the studied years, driven by Extensive mRNA and gene therapy pipelines, which increased system deployment. Growth venture funding also supported emerging biotechnology companies, where the presence of advanced manufacturing infrastructure accelerated scale-up. High R&D activities and clinical trials also increased the use of microfluidic lipid nanoparticle manufacturing systems, where the presence of advanced CDMOs also increased their demand.

Canada Market Growth

Canada held a 4% share in the microfluidic lipid nanoparticle manufacturing market in 2025, due to government investment strengthening domestic biomanufacturing. Research institutions advance LNP technologies, where growing biotechnology activity also supports a rise in the demand for microfluidic lipid nanoparticle manufacturing systems. Increasing use of RNA therapeutics and gene therapies is also driving their demand, where expanding pharmaceutical manufacturing capabilities are driving their adoption. Growing focus on pandemic preparedness is also increasing their use for vaccine and nucleic acid therapeutics development.

Europe held a 27% share of the market and is expected to grow significantly during the forecast period, due to strong biopharmaceutical research supporting LNP development. Growing regional manufacturing investments are expanding RNA capabilities, where a rise in collaborative research also accelerates platform innovation. Well-established research institutes have also increased their demand due to growing LNP innovation, where government funding also encourages their adoption. Increasing demand for personalized medicines and biologics is also enhancing the market growth.

Germay Market Growth

Germany held a 7% share in the microfluidic lipid nanoparticle manufacturing market in 2025, driven by strong biopharmaceutical manufacturing, which supported adoption of microfluidic lipid nanoparticle manufacturing systems. Growth in RNA technology expertise also stimulated investments, where the shift towards automation also strengthened advanced production capacity. A rise in interest in precision medicine, gene therapies, and mRNA therapeutics also increased the use of these systems. The presence of a well-established CDMO ecosystem and new collaborations also increased their use.

UK Market Growth

UK held a 5% share in the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to witness the fastest growth with a CAGR of 28.50% over the forecast period, due to biotechnology clusters accelerating RNA therapeutic development. Academic spinouts expand formulation research, where growing investment supports advanced manufacturing, driving the demand for microfluidic lipid nanoparticle manufacturing systems. Growing government support and collaborations are also accelerating the adoption of these systems, where favourable regulatory support is also promoting innovations, ultimately increasing the use of these systems.

Asia Pacific held a 22% share of the market in 2025 and is expected to grow at the fastest CAGR of 34.70% during the forecast period, due to rapid expansion of advanced biomanufacturing across China, Japan, India, and South Korea. Growing local RNA pipelines increase equipment demand, while increasing government investment also accelerates domestic technology development. Expanding pharmaceutical and biotechnology companies are also increasing the adoption of microfluidic lipid nanoparticle manufacturing technologies, where growing clinical activities are also driving demand, enhancing market growth.

China Market Growth

China held an 8% share of the microfluidic lipid nanoparticle manufacturing market in 2025, driven by large biotechnology investment, which expanded RNA therapeutic pipelines. Domestic equipment development also reduced technology dependence, where rapid growth in commercial manufacturing capacity increased the adoption of microfluidic lipid nanoparticle manufacturing systems. The presence of a large patient population also increased the demand for vaccines and advanced treatment options, which contributed to a rise in their use.

India Market Growth

India held a 3% share in the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to expand rapidly with a CAGR of 37.10% in the coming years, due to expanding vaccine manufacturing capabilities creating strong scale-up potential. Growing biotechnology investment expands RNA research, where cost-efficient manufacturing is also attracting global partnerships. Expanding CDMO ecosystem and government initiatives are also driving the demand for microfluidic lipid nanoparticle manufacturing systems. At the same time, continuous innovations and growing collaborations are also promoting the adoption of advanced technologies, creating new opportunities.

Latin America held a 5% share in the market in 2025 and is expected to show lucrative growth during the forecast period, due to growing vaccine manufacturing initiatives strengthening regional capabilities. Growing public health investments are supporting biotechnology infrastructure expansion, where increasing local production strategies are also encouraging advanced manufacturing adoption. Expanding clinical research and government initiatives are also increasing the adoption of microfluidic lipid nanoparticle manufacturing systems, and a rise in collaborations are also increasing their use. Additionally, growing vaccine and RNA therapeutic development are also fueling the market expansion.

Brazil Market Growth

Brazil held a 3% share in the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to gain the highest market share with a CAGR of 27.10% during the forecast period, driven by the presence of strong vaccine institutions, which supported LNP technology adoption. Growth in domestic biomanufacturing investment also expanded capacity, where a rise in research collaborations also accelerated RNA development. Growth in R&D activities and clinical trials also increased the use of microfluidic lipid nanoparticle manufacturing systems, where the large patient population also contributed to their increased use.

Mexico Market Growth

Mexico held a 1% share in the microfluidic lipid nanoparticle manufacturing market in 2025, due to growing pharmaceutical production supporting technology transfer. Growing regional partnerships expand manufacturing capabilities, where biotechnology investments are also increasing gradually, driving the demand for microfluidic lipid nanoparticle manufacturing technologies. At the same time, expanding healthcare infrastructure is also driving their adoption rates, where growing government initiatives and demand for vaccines and biologics are also encouraging their use.

MEA held a 3% share in the market in 2025 and is expected to show notable growth during the forecast period, due to growing healthcare diversification programs supporting biomanufacturing investment. Vaccine security initiatives are also encouraging local production, where growing innovations are also driving the demand for microfluidic lipid nanoparticle manufacturing systems. Increasing collaborations and improving research infrastructure are also increasing their adoption, where expanding biotechnology hubs are also driving their demand, promoting the market growth.

Saudi Arabia Market Growth

Saudi Arabia held a 0.80% share in the microfluidic lipid nanoparticle manufacturing market in 2025, driven by growth in biotechnology localization programs, which attracted manufacturing investment. A rise in healthcare transformation also supported advanced therapies development, which increased the use of microfluidic lipid nanoparticle manufacturing systems. Growth in strategic partnerships transferred technical capabilities, where vision development investments also increased the use of these systems. Expansion of vaccine manufacturing and nanomedicine technologies also increased their utilization.

Israel Market Growth

Israel held a 0.60% share in the microfluidic lipid nanoparticle manufacturing market in 2025 and is expected to show the fastest growth with a CAGR of 28.10% over the forecast period, due to strong biotechnology innovation supporting nanoparticle research. Academic expertise advances drug-delivery technologies, driving the demand for microfluidic lipid nanoparticle manufacturing technologies, where increasing startup activity is also accelerating commercialization, increasing their adoption. Growing R&D activities supported by funding and investments are also supporting their utilization, where a rise in collaborations is also creating new opportunities.

| Companies | Headquarters | Solutions |

| Danaher Corporation | Washington, D.C., U.S. | NanoAssemblr Platform |

| Elveflow | Paris, France | TAMARA Integrated Microfluidic System |

| Merck KGaA | Darmstadt, Germany | NanoFabTx Microfluidic Nano Device System |

| IDEX Corporation | Northbrook, U.S. | Microfluidizer Reaction Technology |

| PreciGenome LLC | San Jose, U.S. | NanoGenerator Nanoparticle Synthesis System |

Competitive Positioning by Research, Clinical, and Commercial Manufacturing Capability

Depending on the research, clinical, and commercial manufacturing capabilities, Danaher Corporation, Merck KGaA, and Lonza Group AG dominated the market.

Competitive Differentiation Through Scalability, Throughput, and Process Reproducibility

Danaher Corporation, IDEX Corporation, and KNAUER Wissenschaftliche Geräte GmbH registered the market dominance by considering the technical capabilities that influence customer selection and long-term market positioning.

Competitive Strategies Based on Partnerships, Licensing, and Ecosystem Expansion

The leaders in the market based on pharmaceutical collaborations, CDMO partnerships, distribution agreements, and technology alliances are Danaher Corporation, Genevant Sciences, and Acuitas Therapeutics.

Company Benchmarking by Product Portfolio and Manufacturing Scale

Based on the company system offerings from discovery-scale platforms through commercial manufacturing solutions, Danaher Corporation, Merck KGaA, and Thermo Fisher Scientific Inc. dominated the market.

Company Benchmarking by Technology and Application Coverage

Depending on the mixing technologies, payload compatibility, automation, software, and therapeutic applications, Danaher Corporation, Merck KGaA, and Evonik Industries AG were considered the market leaders.

Company Benchmarking by Geographic Reach and Customer Base

By focusing on commercial presence, distribution networks, strategic customers, and regional expansion, Thermo Fisher Scientific Inc., Danaher Corporation, and Evonik Industries AG dominated the market.

| Company | Business Focus | Product Portfolio | Technology Capabilities | Geographical Presence |

| KNAUER Wissenschaftliche Geräte GmbH | manufactures high-end scientific instruments | LC systems, life science systems, software, modules, and LC supplies | IJM NanoScaler and IJM NanoProducer | Across Germany |

| Inside Therapeutics | develops cutting-edge equipment for nanoparticle screening & production dedicated to drug delivery | Nanomedicine formulations and payloads | TAMARA Nanoparticle Formulation System and NanoPulse Platform | Across France |

| Unchained Labs | Develops biologics, gene therapies, and AI-driven automation | Biologics, gene therapy, cell Therapy, nanoparticles, exosomes, genomics, and automation | Microfluidic Mixing and Microfluidic Viscosity Measurements Solutions | U.S., UK, Belgium, Japan, and China |

| Company | Strategic Developments |

| Acuitas Therapeutics | Acquired a majority stake in RNA Technologies & Therapeutics (RNA T&T), |

| Danaher Corporation | Finalized agreement to acquire Masimo Corporation |

| Biocytogen Pharmaceuticals | Evaluation and option agreement with Merck KGaA |

In March 2026, LIBRIS, an automated microfluidic platform capable of generating LNP formulations, was developed by the engineers at the University of Pennsylvania. The platform is expected to accelerate lipid nanoparticle development by as much as 100-fold.

In April 2025, a system for the production of lipid nanoparticles (LNPs) was developed by the collaboration between Shin-Etsu Chemical and Hokkaido University. The system incorporates a microfluidic device of Hokkaido University, along with materials (primarily synthetic quartz) and processing technology of Shin-Etsu Chemical.

In April 2025, after the launch of NanoCalibur™, which is a cutting-edge, scalable nanoparticle (NP) production system, the CEO of MEPSGEN, YongTae Kim, expressed that, "We are thrilled to bring NanoCalibur™, a stable, reliable, and high-precision nanoparticle synthesis platform, to the U.S. market. With its cutting-edge microfluidics technology and user-friendly design, this micro-lab makes it easier for researchers to focus on their mission to develop the next generation of nanoparticle-based therapeutics."

Most Attractive Market Entry Opportunities

The most attractive market entry opportunities involve the combinations of new microfluidic manufacturing platforms, expanding application, growing customer group, expanding manufacturing scale, and emerging markets.

Barriers to Entry and Capabilities Required for Sustainable Competition

The barriers to entry and capabilities required for sustainable competition include the shortage of technology expertise, stringent intellectual property requirements, regulatory capabilities requirements, strong customer validation, capital requirements, and supply-chain access.

Partnership and Acquisition Opportunities

Growing strategic alliances, technology licensing, acquisitions, or CDMO partnerships are expected to accelerate market expansion.

Technology and Scale-Up Risks

The technology and scale-up risks evaluate challenges associated with throughput, reproducibility, platform transfer, and commercial-scale validation.

Regulatory and Quality Risks

The regulatory and quality risks are driven by evolving regulatory expectations and the cost of meeting clinical and commercial manufacturing standards.

Commercial and Competitive Risks

Commercial and competitive risks depend on customer concentration, technology substitution, pricing pressure, intellectual property constraints, and competitive disruption

Expected Shift from Research-Led Demand to Commercial Manufacturing

The expected shift from research-led demand to commercial manufacturing for microfluidic lipid nanoparticles is anticipated to rise due to a revenue mix that could change as more RNA and gene-editing products progress toward commercialization.

Technologies and Applications Expected to Create the Next Growth Cycle

The rise in commercial-scale microfluidics, gene-editing delivery, integrated manufacturing, continuous processing, and advanced process analytics as potential growth areas are expected to expand the market technologies and applications.

Strategic Priorities for Companies Seeking Long-Term Market Leadership

The companies prioritizing scalability, GMP readiness, recurring revenue, customer support, automation, and global manufacturing partnerships are anticipated to lead the market expansion.

By Product & Offering

By Mixing Technology

By Scale of Operation

By Workflow

By Payload Type

By Application

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar