")

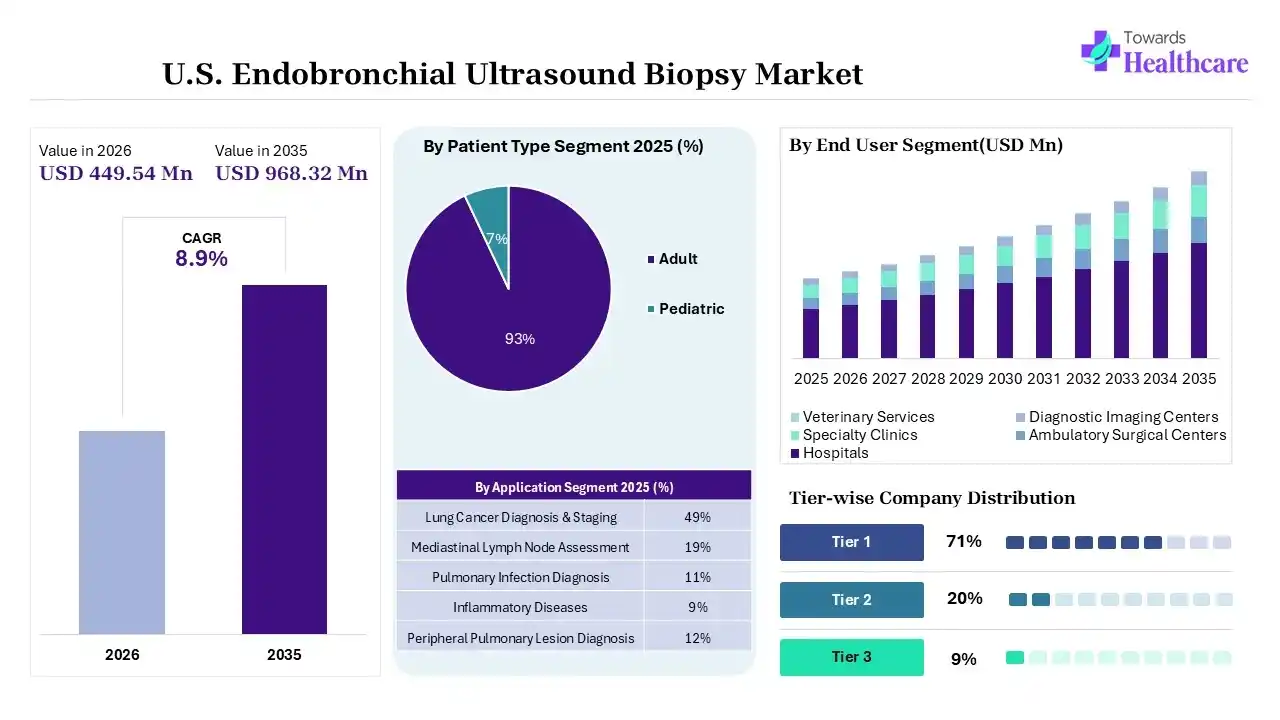

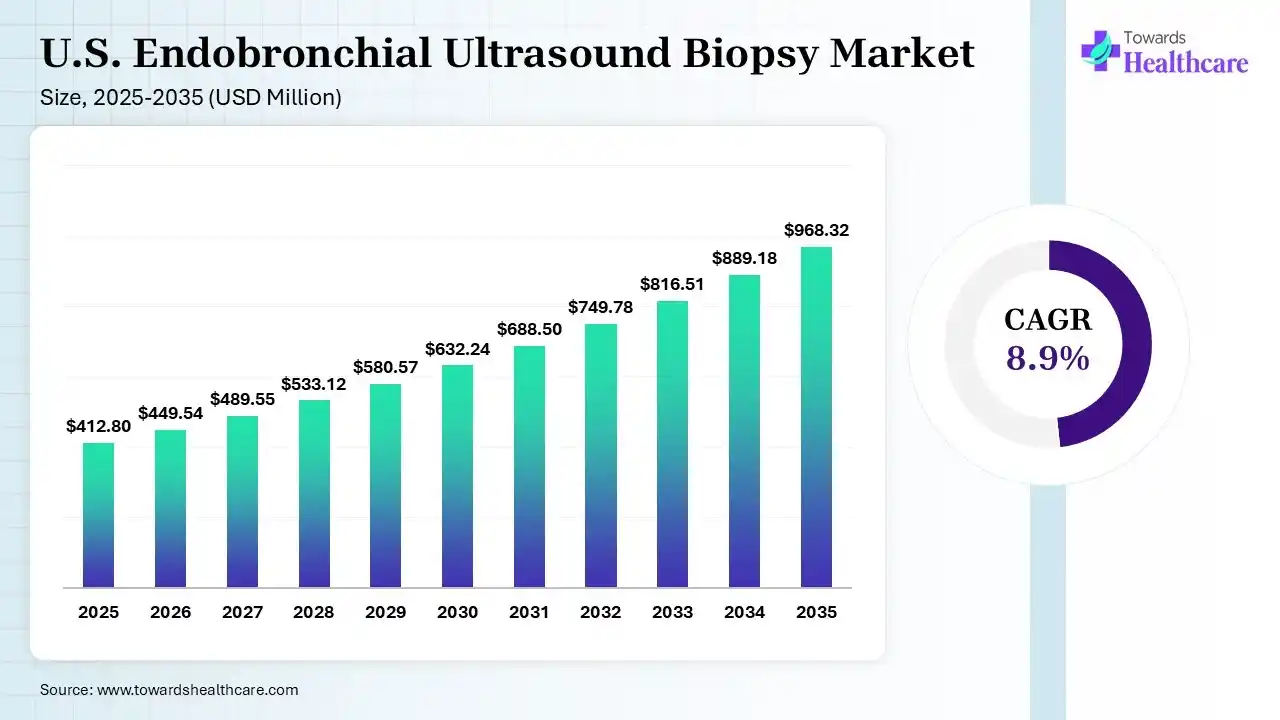

The U.S. endobronchial ultrasound biopsy market size was estimated at USD 412.8 million in 2025 and is predicted to increase from USD 449.54 million in 2026 to approximately USD 968.32 million by 2035, expanding at a CAGR of 8.9% from 2026 to 2035. The growing lung cancer burden across the U.S. is increasing the demand for endobronchial ultrasound biopsies. Increasing R&D activities, demand for molecular diagnostics, rise in personalized medicines, technological advancements, and new product launches are also enhancing the market growth.

")

The U.S. endobronchial ultrasound biopsy market is driven by a surge in lung cancer screenings and a shift towards minimally invasive diagnostic procedures. The U.S. endobronchial ultrasound biopsy encompasses the devices, accessories, and procedures for endobronchial ultrasound biopsy, driving real-time visualization of lungs, lymph nodes, and airways. It is used for the diagnosis of lung cancer, sarcoidosis, tuberculosis, and enlarged lymph nodes.

AI is used in the U.S. endobronchial ultrasound biopsy market for real-time image analysis and early lung cancer diagnosis. It also helps in the detection and characterization of lesions and lymph nodes, as well as personalized treatment planning. AI also helps in automated image interpretation and in the development of robotic bronchoscopy systems.

Expanding Cancer Screening Programs

Increasing cancer prevalence rates in the U.S. are driving their screening programs. This is promoting the use of endobronchial ultrasound biopsy for early and accurate detection of lung cancers.

Rising Molecular Testing Solutions

The growing demand for targeted and personalized cancer treatment drives the use of endobronchial ultrasound biopsy. They are being used for the analysis of high-quality tissue samples for genomic profiling and biomarker analysis.

Escalating Technological Advancements

Expanding technological advancements are driving the development of next-generation EBUS bronchoscopes. Therefore, the companies are developing EBUS bronchoscopes with higher resolution, maneuverability, and enhanced needle guidance systems.

| Table | Scope |

| Market Size in 2026 | USD 449.54 Million |

| Projected Market Size in 2035 | USD 968.32 Million |

| CAGR (2026 - 2035) | 8.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Procedure Type, By Product Type, By Application, By End User, By Patient Type, By Technology, By Biopsy Needle Size, By Imaging Modality Integration |

| Top Key Players | Olympus Corporation, Medtronic plc, Fujifilm Holdings Corporation, Medi-Globe GmbH, PENTAX Medical, Micro-Tech Endoscopy, Boston Scientific Corporation, Verna Medical Technologies, Cook Medical, Medtronic plc |

")

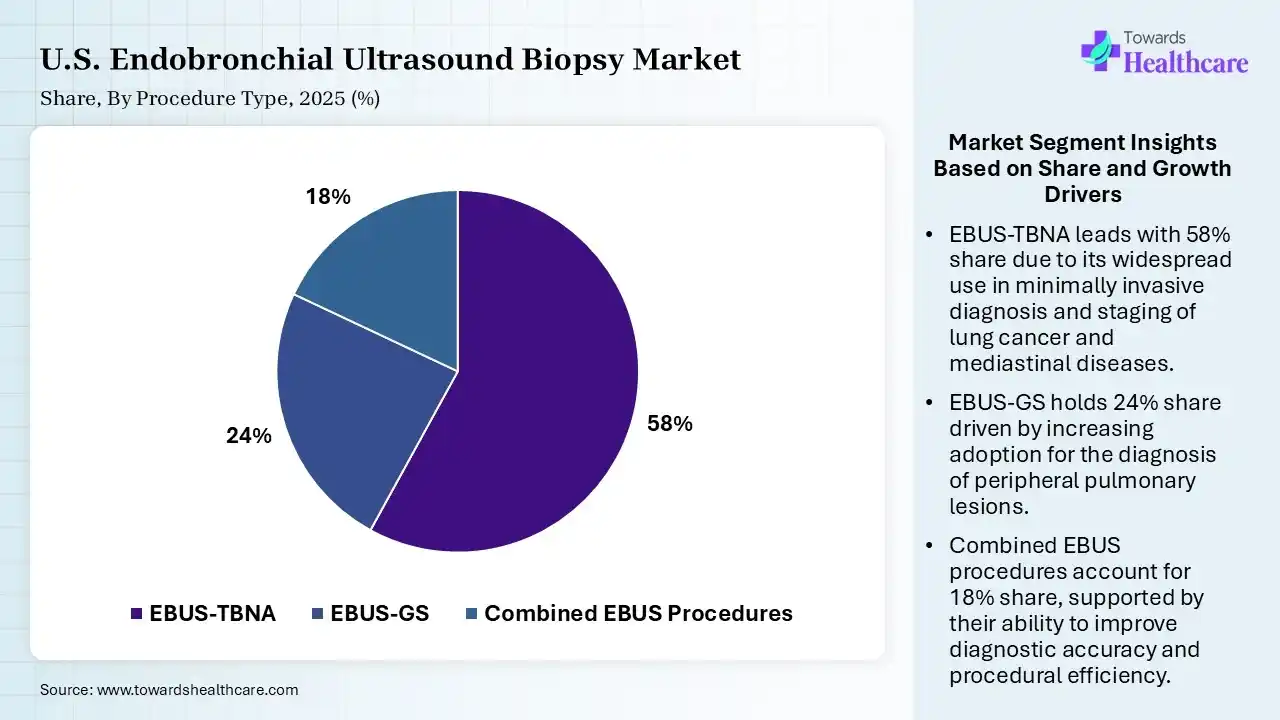

| Segment | Share 2025 (%) |

| EBUS-TBNA | 58% |

| EBUS-GS | 24% |

| Combined EBUS Procedures | 18% |

The EBUS-TBNA Segment Dominated the Market With 58% in 2025

The EBUS-TBNA segment held the largest revenue share of 58% of the U.S. endobronchial ultrasound biopsy market in 2025, due to increased lung cancer staging procedures, which enhanced demand across tertiary hospitals. Minimally invasive sampling also improved physician preference. Favorable reimbursement also supported procedural adoption.

The EBUS-GS segment held the second-largest share of 24% of the market in 2025, driven by the rising diagnosis of peripheral pulmonary lesions, which accelerates their usage. Technological advancements also improve lesion access accuracy. Growing outpatient bronchoscopy volumes also support their expansion.

The combined EBUS procedures segment held 18% of the U.S. endobronchial ultrasound biopsy market share in 2025 and is expected to witness the fastest growth with a CAGR of 11.40% during the forecast period, due to the integration with robotic bronchoscopy, which enhances procedural precision. Complex pulmonary diagnostics also require multimodal navigation systems. Hospitals are also increasingly investing in advanced hybrid bronchoscopy suites.

")

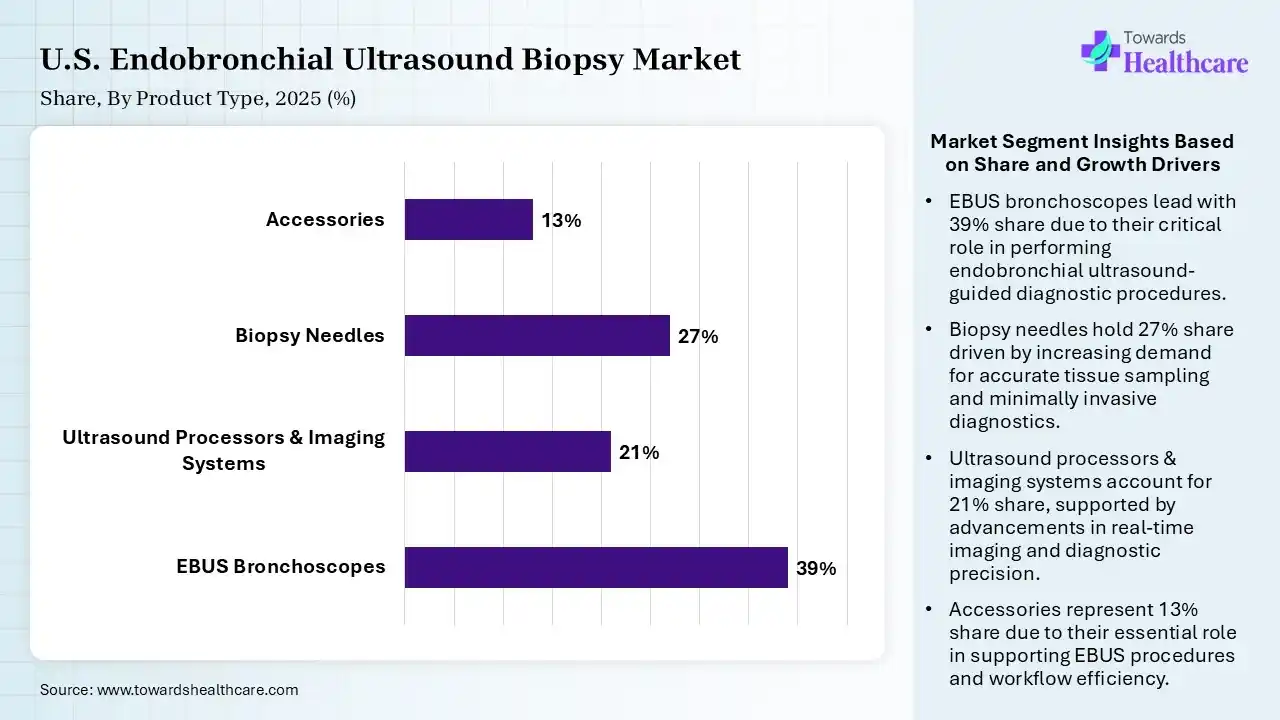

| Segment | Share 2025 (%) |

| EBUS Bronchoscopes | 39% |

| Ultrasound Processors & Imaging Systems | 21% |

| Biopsy Needles | 27% |

| Accessories | 13% |

The EBUS Bronchoscopes Segment Dominated the Market With 39% in 2025

The EBUS bronchoscopes segment accounted for the highest revenue share of 39% of the U.S. endobronchial ultrasound biopsy market in 2025, driven by hospitals continuing to replace conventional bronchoscopes with ultrasound-enabled systems. Increased bronchoscopy procedure volumes also sustained equipment demand. Advanced visualization capabilities also improved clinician confidence.

The biopsy needles segment held the second-largest share of 27% of the market in 2025 and is expected to show the highest growth with a CAGR of 9.6% during the forecast period, due to growing procedural frequency, which increases recurring needle consumption. Improved tissue acquisition for molecular testing also boosts their adoption. Single-use sterile designs also strengthen purchasing trends.

The ultrasound processors & imaging systems segment held 21% of the U.S. endobronchial ultrasound biopsy market share in 2025, driven by integrated imaging platforms, which improve workflow efficiency in pulmonary departments. Demand for real-time imaging also supports technology upgrades. Academic centers also expand advanced imaging infrastructure.

The accessories segment held 13% of the market share in 2025, as supporting accessories enhance procedural flexibility and sampling precision. Expansion of bronchoscopy labs also increases accessory utilization. Manufacturers are also introducing disposable accessory portfolios for infection control.

")

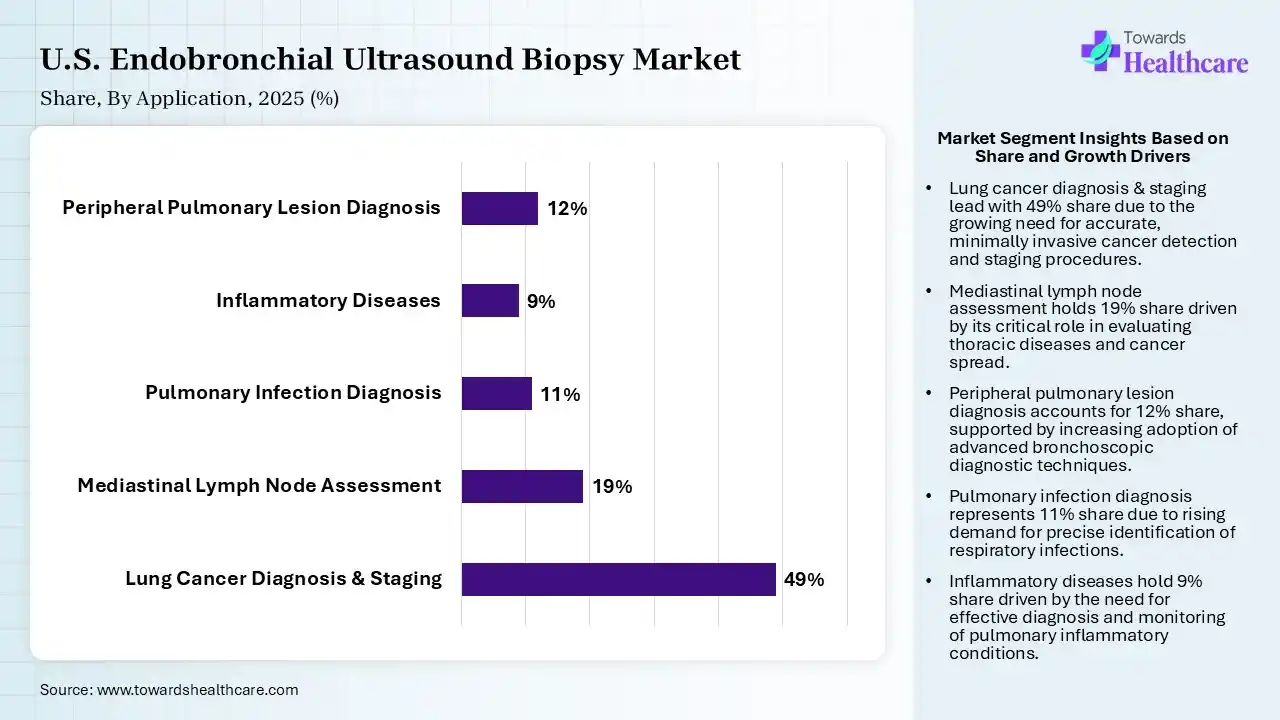

| Segment | Share 2025 (%) |

| Lung Cancer Diagnosis & Staging | 49% |

| Mediastinal Lymph Node Assessment | 19% |

| Pulmonary Infection Diagnosis | 11% |

| Inflammatory Diseases | 9% |

| Peripheral Pulmonary Lesion Diagnosis | 12% |

The Lung Cancer Diagnosis & Staging Segment Dominated the Market With 49% in 2025

The lung cancer diagnosis & staging segment held a major revenue share of 49% of the U.S. endobronchial ultrasound biopsy market in 2025, due to growth in the incidence of lung cancer, which increased demand for minimally invasive diagnostics. Precision oncology also requires accurate nodal staging. National screening initiatives also support earlier detection rates.

The mediastinal lymph node assessment segment held the second-largest share of 19% of the market in 2025, as physicians are increasingly preferring EBUS over surgical mediastinoscopy. Improved diagnostic sensitivity also enhances their adoption. A growing pulmonary disease burden also supports procedure growth.

The peripheral pulmonary lesion diagnosis segment held 12% of the U.S. endobronchial ultrasound biopsy market share in 2025 and is expected to expand rapidly with a CAGR of 11.80% during the forecast period, due to increasing CT screening, which detects more peripheral lung nodules. Navigation-assisted EBUS also improves lesion localization efficiency. Robotic bronchoscopy integration also accelerates their adoption.

The pulmonary infection diagnosis segment held 11% of the market share in 2025, as infectious pulmonary diseases require accurate tissue and fluid sampling. Hospitals are also adopting EBUS for complex respiratory infections. Immunocompromised patient populations also increase diagnostic demand.

")

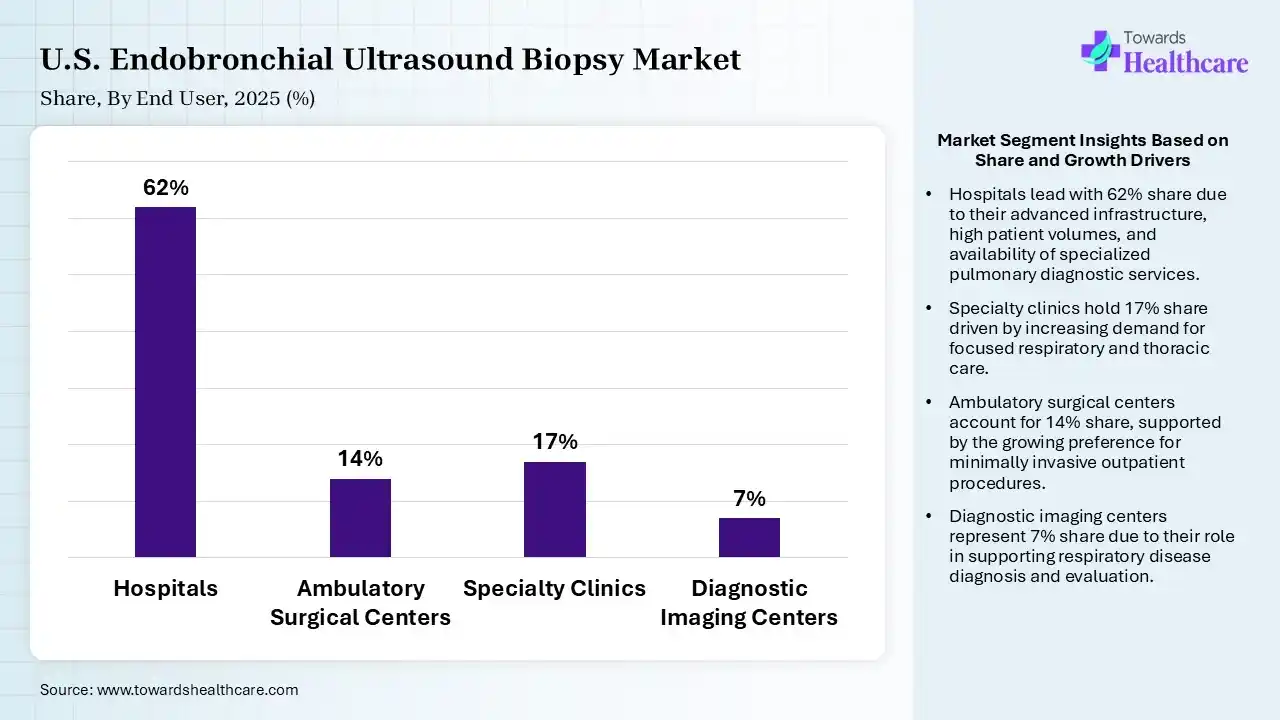

| Segment | Share 2025 (%) |

| Hospitals | 62% |

| Ambulatory Surgical Centers | 14% |

| Specialty Clinics | 17% |

| Diagnostic Imaging Centers | 7% |

The Hospitals Segment Dominated the Market With 62% in 2025

The hospitals segment contributed the biggest revenue share of 62% of the U.S. endobronchial ultrasound biopsy market in 2025, as large hospitals maintained advanced bronchoscopy infrastructure. High patient inflow also supported procedural volumes. Multidisciplinary oncology programs also accelerated technology procurement.

The specialty clinics segment held the second-largest share of 17% of the market in 2025 and is expected to gain the highest share with a CAGR of 10.60% during the forecast period, as specialized pulmonology clinics increasingly invest in minimally invasive diagnostics. Faster patient turnaround also improves operational scalability. Expanding private pulmonary networks also fuels market penetration.

The ambulatory surgical centers segment held 14% of the U.S. endobronchial ultrasound biopsy market share in 2025, due to a shift toward outpatient pulmonary procedures, which increases EBUS biopsy utilization. Lower operational costs also improve procedural efficiency. Favorable reimbursement also encourages ASC adoption.

The diagnostic imaging centers segment held 7% of the market share in 2025, driven by imaging centers integrating diagnostic bronchoscopy services with radiology workflows. Demand for comprehensive pulmonary diagnostics also supports their growth. Collaborations with hospitals also expand referral networks.

The U.S. endobronchial ultrasound biopsy market is expected to show considerable growth during the forecast period, due to the growth in lung cancer rates. A shift towards minimally invasive diagnostic procedures also increased their demand. The presence of advanced healthcare infrastructure also increased their use for personalized treatment development, which contributed to the market growth.

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Companies | Headquarters | U.S. Endobronchial Ultrasound Biopsy Systems |

| Olympus Corporation | Tokyo, Japan | BF-UC190 Convex Probe EBUS scope, ViziShot 2 EBUS-TBNA needles, and UM-DG28 Radial Probe |

| Medtronic plc | Dublin, Ireland | Illumisite Electromagnetic Navigation Bronchoscope (ENB) platform |

| Fujifilm Holdings Corporation | Tokyo, Japan | EB-710P Slim EBUS scope, SU-1 Ultrasound Processor, and PB22 M2 Radial EBUS probe |

| Medi-Globe GmbH | Grassau, Germany | SonoTip II and SonoTip TopSpeed EBUS-TBNA Needle Systems |

| PENTAX Medical | Tokyo, Japan | EB19-J10U Convex Probe EBUS bronchoscope and PENTAX EBUS-TBNA needles |

| Micro-Tech Endoscopy | Ann Arbor, U.S. | Arete EBUS-TBNA Needles |

| Boston Scientific Corporation | Marlborough, U.S. | Expect EBUS-TBNA Biopsy Needles and Exalt Model B |

| Verna Medical Technologies | St. Louis, U.S. | SPiN Thoracic Navigation System |

| Cook Medical | Bloomington, U.S. | EchoTip Ultra and EchoTip ProCore EBUS TBNA Needle Systems |

| Medtronic plc | Largo, U.S. | 10-100 Series EBUS-TBNA Needles |

Strengths

Weaknesses

Opportunities

Threats

By Procedure Type

By Product Type

By Application

By End User

By Patient Type

By Technology

By Biopsy Needle Size

By Imaging Modality Integration

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar