")

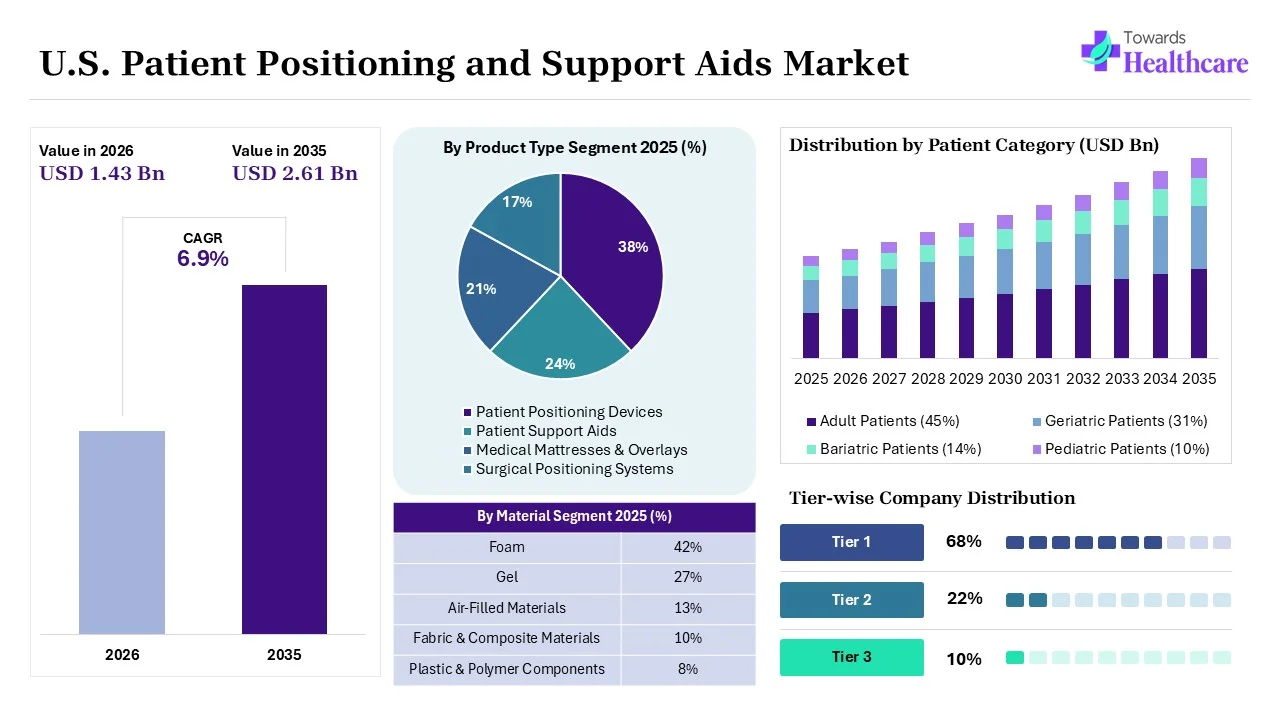

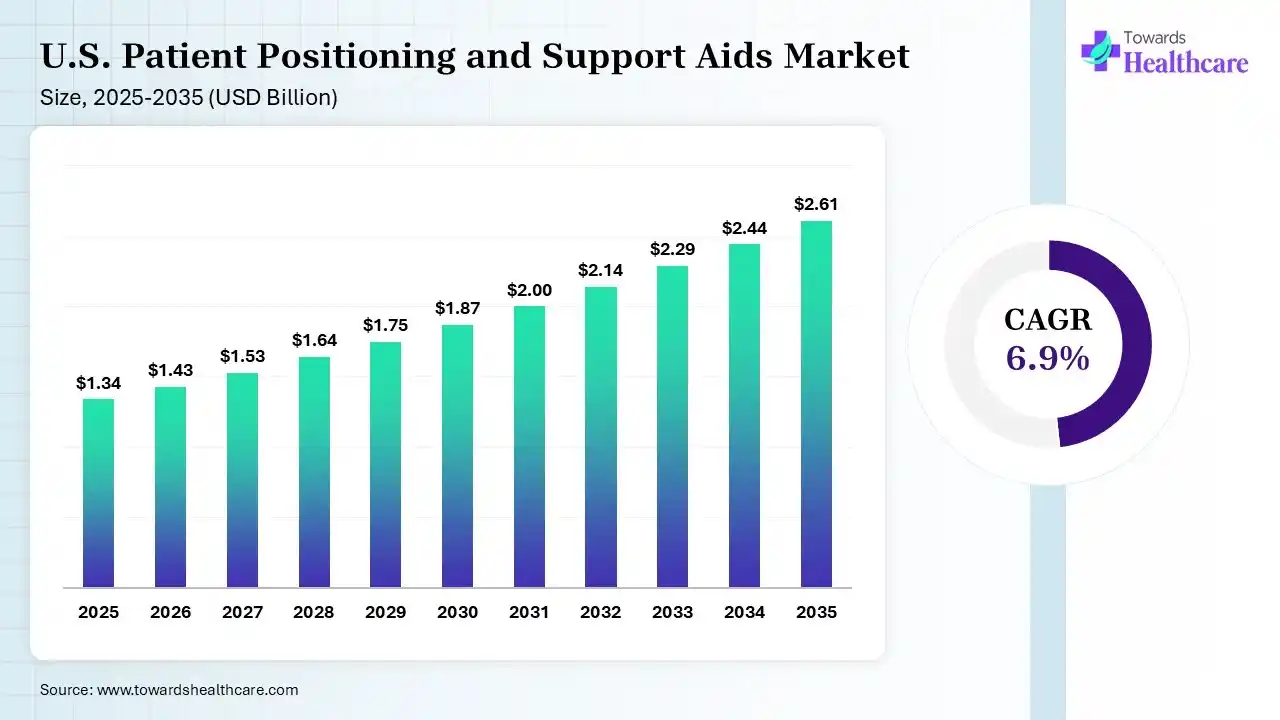

The U.S. patient positioning and support aids market size was valued at US$ 1.34 billion in 2025 and is projected to grow to 1.43 billion in 2026. Forecasts suggest it will reach approximately US$ 2.61 billion by 2035, registering a CAGR of 6.9% during the period.

")

The U.S. patient positioning and support aids are medical devices used to properly stabilize and support patients during surgical procedures, diagnostic imaging, and long-term care. They help maintain correct alignment, enhance comfort, and ensure safety by reducing movement, pressure points, and long-term care. They maintain correct body alignment, enhance comfort, and ensure safety by reducing movement, pressure points, and the risk of pressure injuries during extended medical procedures.

These devices are commonly used in hospitals, ambulatory surgical centers, and rehabilitation facilities. They include cushions, pads, wedges, headrests, and transfer aids that assist healthcare professionals in safe patient handling, improve procedure accuracy, and support better clinical outcomes across various healthcare settings.

The U.S. patient positioning and support aids market is growing due to rising surgical volumes, an aging population, and increasing chronic diseases requiring long-term care. A strong focus on preventing pressure injuries and improving patient safety in hospitals and surgical centers is further driving adoption. Expanding healthcare infrastructure and demand for advanced, ergonomic positioning solutions are boosting market growth across the country.

AI is enhancing the market by improving precision in surgical positioning, reducing pressure injury risks through predictive analytics, and optimizing patient monitoring in real time. Smart sensors and AI-driven support systems enable better posture alignment and personalized care. AI also supports workflow efficiency in hospitals, improves clinical decision-making, and accelerates the development of advanced ergonomic and adaptive positioning devices.

Increasing Surgical Procedures

The rising number of surgeries in the U.S. is driving demand for patient positioning and support aids. These devices ensure proper alignment, stability, and safety during operations, helping surgeons perform procedures more accurately and efficiently.

Growing Elderly Population

The expanding geriatric population increases the need for mobility support and pressure injury prevention. Patient positioning aids help elderly and bedridden patients stay comfortable, reduce complications, and improve overall care quality in hospitals and long-term care facilities.

Focus on Patient Safety

Hospitals are increasingly adopting advanced support aids to prevent pressure ulcers and improve patient safety. These devices enhance comfort during long treatments and reduce risks associated with improper positioning during surgical and diagnostic procedures.

| Table | Scope |

| Market Size in 2026 | USD 1.43 Billion |

| Projected Market Size in 2035 | USD 2.61 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Material, By Application, By End User, By Patient Category, By Distribution Channel |

| Top Key Players | Stryker Corporation, Hillrom, Arjo, AliMed, GF Health Products, Inc., EHOB, Inc., Span-America Medical Systems, Blue Chip Medical Products, Inc. |

")

| Segment | Share 2025 (%) |

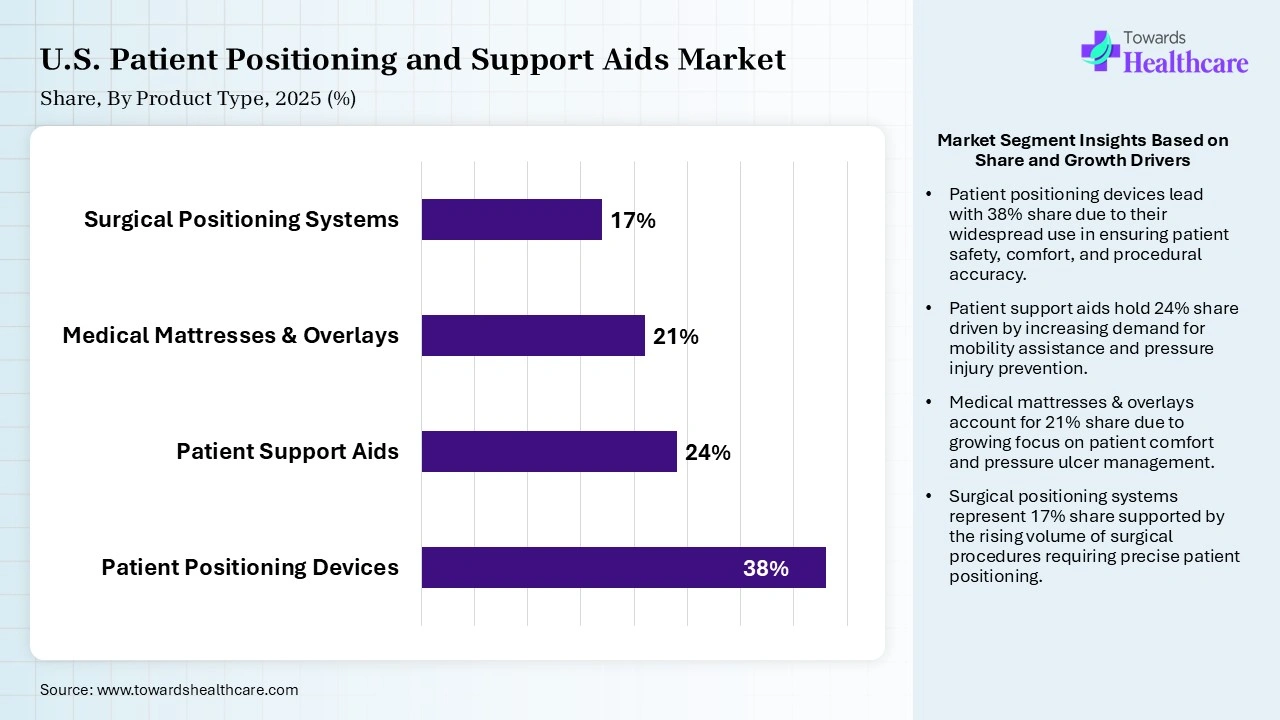

| Patient Positioning Devices | 38% |

| Patient Support Aids | 24% |

| Medical Mattresses & Overlays | 21% |

| Surgical Positioning Systems | 17% |

The Patient Positioning Devices Segment Dominated the U.S. Patient Positioning and Support Aids Market in 2025.

The patient positioning devices segment held a dominant share of 38% in 2025 due to their essential role in ensuring patient safety, stability, and proper anatomical alignment during surgical, diagnostic, and therapeutic procedures. These devices help reduce the risk of pressure injuries, nerve damage, and procedural complications. Rising surgical volumes, increasing focus on patient comfort, and growing adoption of advanced positioning solutions across healthcare facilities further supported the segment’s market leadership.

The patient support aids segment held the second-largest share of 24% in 2025 due to its vital role in enhancing patient comfort, reducing pressure injuries, and improving mobility during prolonged hospital stays and recovery periods. Products such as cushions, gel pads, and positioning supports are widely used across hospitals, long-term care facilities, and home healthcare settings. Growing emphasis on patient safety and quality care further supports the segment’s strong demand.

The medical mattresses & overlays held a 21% market share due to increasing focus on preventing pressure injuries and improving patient comfort during extended hospital stays. These products help distribute pressure evenly, enhance support, and reduce the risk of skin breakdown in immobile patients. Rising hospitalization rates, growing elderly populations, and increasing demand for long-term care and home healthcare services are further driving segment growth.

The surgical positioning systems segment held a 17% share in 2025 and is expected to grow at the fastest CAGR of 8.40% in the U.S. patient positioning and support aids market during the forecast period due to the increasing volume of complex surgical procedures and the growing emphasis on patient safety and surgical precision. Healthcare facilities are adopting advanced positioning technologies to improve procedural outcomes, reduce complications, and enhance operating room efficiency. Continuous innovation in ergonomic design and pressure-relief features is further accelerating segment growth.

")

| Segment | Share 2025 (%) |

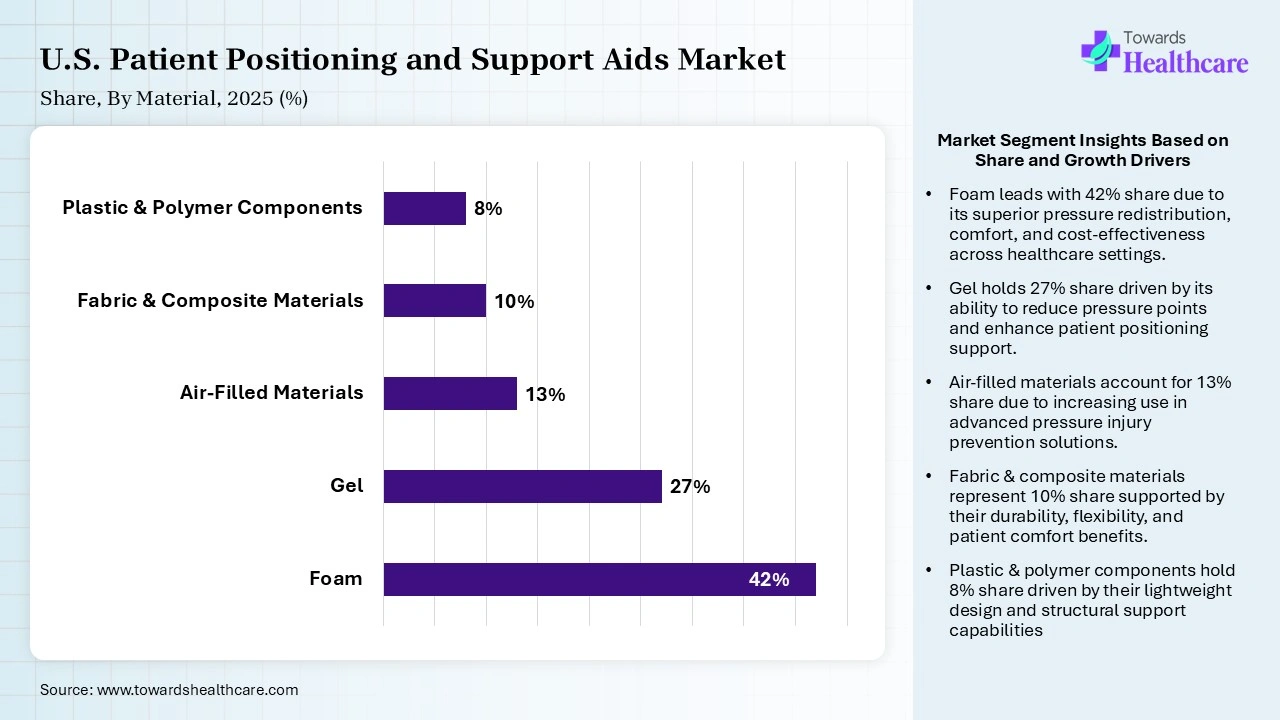

| Foam | 42% |

| Gel | 27% |

| Air-Filled Materials | 13% |

| Fabric & Composite Materials | 10% |

| Plastic & Polymer Components | 8% |

The Foam Segment Led the Market in 2025 with the Largest Share

The foam segment dominated the U.S. patient positioning and support aids market with a share of 42% in 2025 due to its excellent pressure redistribution properties, lightweight design, and cost-effectiveness. Foam-based products are widely used in surgical procedures, patient support surfaces, and long-term care settings to enhance comfort and reduce the risk of pressure injuries. Their versatility, durability, and ease of customization for various clinical applications further contributed to their market leadership.

The gel segment held the second-largest share of 27% in 2025 due to its superior pressure redistribution, cushioning performance, and ability to reduce tissue stress during prolonged procedures. Gel-based positioning products are widely used in surgical and critical care settings to enhance patient comfort and minimize the risk of pressure injuries. Their durability, stability, and effectiveness in supporting the vulnerable patient population have contributed significantly to sustained market demand.

The air-filled materials segment held a 13% share in 2025 and is expected to grow at the fastest CAGR of 8.2% in the U.S. patient positioning and support aids market during the forecast period due to its superior pressure redistribution capabilities, lightweight design, and adaptability to individual patient needs. These products help minimize pressure injuries and improve comfort during prolonged care. Increasing demand for advanced support surfaces in hospitals, long-term care facilities, and home healthcare settings is further accelerating adoption and driving segment growth.

The fabric & component materials segment held a 10% market share due to increasing demand for durable, breathable, and infection-resistant materials used in patient positioning and support products. Advanced fabrics improve comfort, moisture management, and skin protection, making them suitable for long-term patient care. Growing focus on patient safety, pressure injury prevention, and the development of high-performance healthcare texiles in further driving adoption across hospitals and care facilities.

")

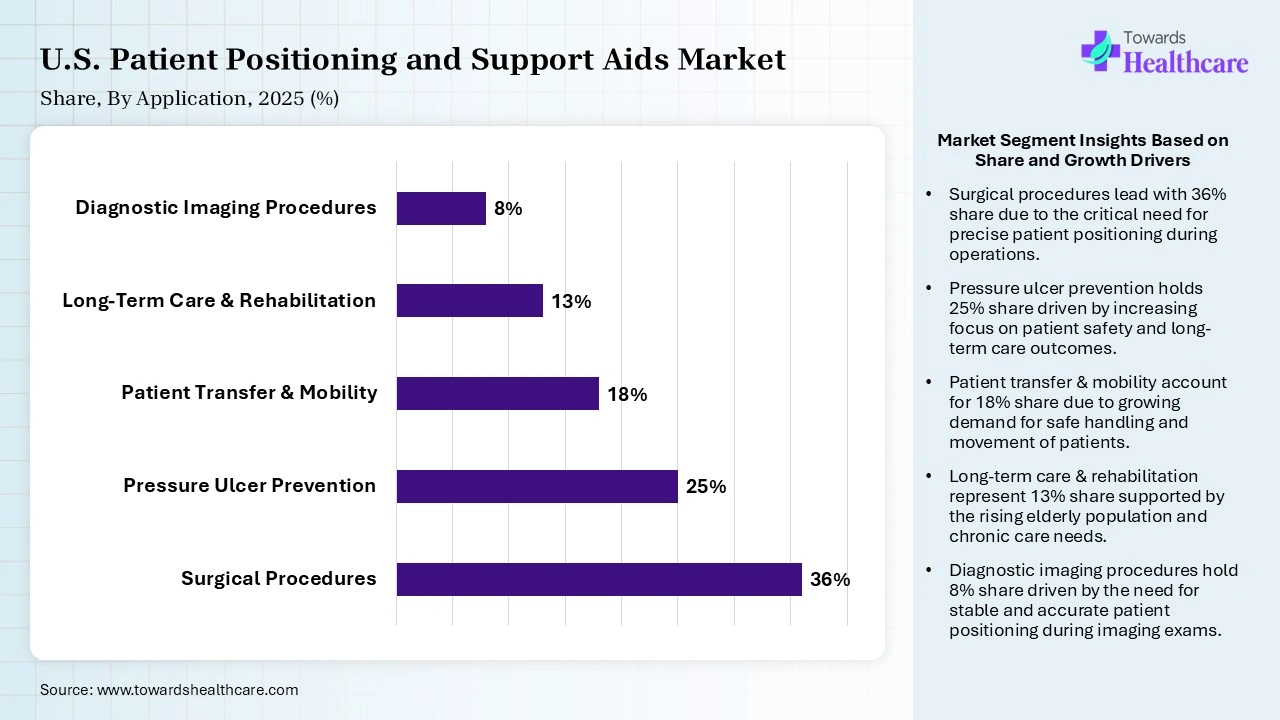

| Segment | Share 2025 (%) |

| Surgical Procedures | 36% |

| Pressure Ulcer Prevention | 25% |

| Patient Transfer & Mobility | 18% |

| Long-Term Care & Rehabilitation | 13% |

| Diagnostic Imaging Procedures | 8% |

The Surgical Procedures Segment Led the U.S. Patient Positioning and Support Aids Market in 2025 with the Largest Share

The surgical procedures segment led the market with a share of 36% in 2025 due to the critical need for proper patient alignment, stability, and pressure management during operations. Positioning devices help improve surgical access, enhance patient safety, and reduce the risk of complications such as nerve injuries and pressure ulcers. Increasing surgical volumes, advancements in operating room technologies, and growing emphasis on quality patient care further supported the segment’s dominance.

The pressure ulcer prevention segment held the second-largest share of 25% in 2025 due to the growing focus on reducing hospital-acquired pressure injuries and improving patient outcomes. Healthcare providers increasingly utilize specialized positioning devices, mattresses, and support surfaces to protect high-risk patients during extended hospital stays. Rising elderly populations, increasing prevalence of chronic conditions, and stricter patient safety standards have further strengthened demand for pressure ulcer prevention solutions.

The patient transfer & mobility segment held an 18% market share due to increasing emphasis on safe patient care, injury prevention, and improved caregiver efficiency. Hospitals and long-term care facilities are adopting advanced transfer aids and mobility support devices to reduce the risk of falls, musculoskeletal injuries, and patient discomfort. Rising elderly populations, growing rehabilitation needs, and increasing demand for home healthcare services are further driving segment growth.

The diagnostic imaging procedures segment held an 8% share in 2025 and is expected to grow at the fastest CAGR of 8.30% in the U.S. patient positioning and support aids market during the forecast period due to the rising volume of MRI, CT, X-ray, and ultrasound examinations worldwide. Accurate patient positioning is essential for obtaining high-quality images, reducing repeat scans, and improving diagnostic accuracy. Increasing investments in advanced imaging technologies, growing chronic disease burden, and expanding healthcare infrastructure are further accelerating demand for specialized positioning and support solutions.

")

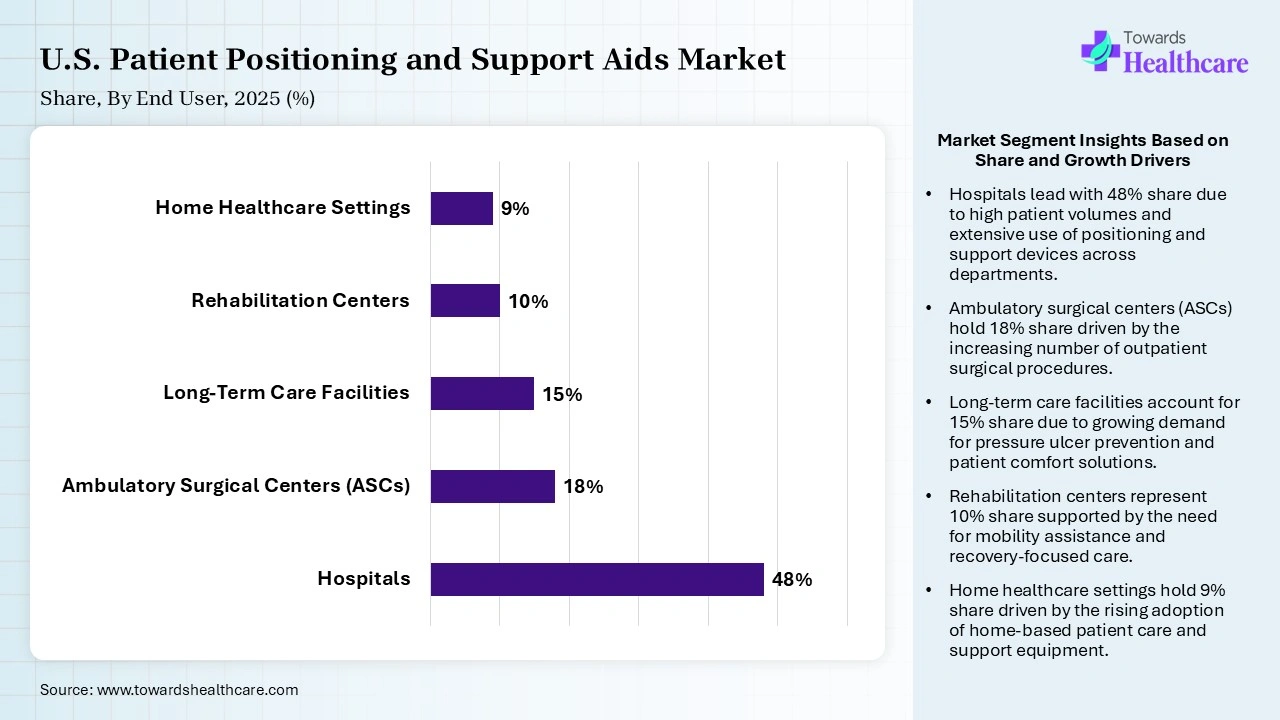

| Segment | Share 2025 (%) |

| Hospitals | 48% |

| Ambulatory Surgical Centers (ASCs) | 18% |

| Long-Term Care Facilities | 15% |

| Rehabilitation Centers | 10% |

| Home Healthcare Settings | 9% |

The Hospitals Segment Led the U.S. Patient Positioning and Support Aids Market in 2025 with the Largest Share

The hospitals segment led the market with a share of 48% in 2025 due to the large number of surgical procedures, diagnostic examinations, and inpatient admissions performed in these facilities. Hospitals require a wide range of positioning devices, support surfaces, and mobility aids to ensure patient safety and comfort. Growing healthcare infrastructure, increasing surgical volumes, and strong investments in advanced patient care technologies further supported the segment’s market leadership.

The ambulatory surgical centers (ASCs) segment held a 18% share in 2025 and is expected to grow at the fastest CAGR of 8.1% in the U.S. patient positioning and support aids market during the forecast period due to the increasing shift toward outpatient procedures, lower treatment costs, and shorter recovery times. ASCs are increasingly adopting advanced patient positioning and support solutions to enhance procedural efficiency, patient safety, and comfort. Growing demand for minimally invasive surgeries and expanding ASC infrastructure are further accelerating segment growth.

The long-term care facilities segment held a share of 15% in 2025 due to the high demand for patient positioning, support surfaces, and mobility aids among elderly and chronically ill patients requiring extended care. These facilities prioritize pressure injury prevention, patient comfort, and safer mobility management. The growing aging population, increasing prevalence of chronic diseases, and rising need for continuous care services further contributed to the segment’s substantial market presence.

The rehabilitation centers segment held a 10% market share due to the growing demand for post-surgical recovery, physical therapy, and long-term rehabilitation services. These facilities increasingly utilize patient positioning and support aids to improve mobility, enhance comfort, and reduce the risk of complications during recovery. Rising incidences of musculoskeletal disorders, neurological conditions, and sports injuries, along with an aging population, are further driving demand for rehabilitation-focused care solutions.

")

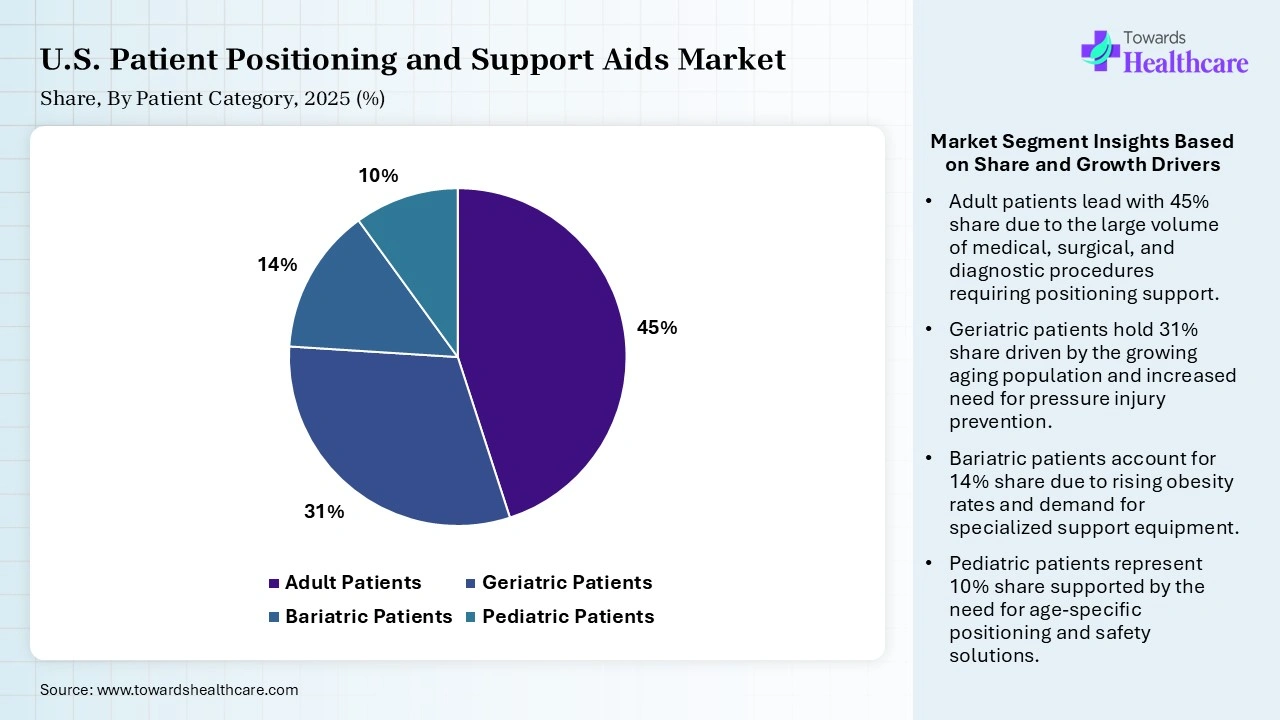

| Segment | Share 2025 (%) |

| Adult Patients | 45% |

| Geriatric Patients | 31% |

| Bariatric Patients | 14% |

| Pediatric Patients | 10% |

The Adult Patients Segment Led the Market in 2025 with the Largest Share

The adult patients segment held a dominant share of the U.S. patient positioning and support aids market of 45% in 2025 due to the high volume of surgical procedures, diagnostic imaging examinations, and hospital admissions among the adult population. Adults account for a significant share of patients requiring positioning devices, support surfaces, and mobility aids. The increasing prevalence of chronic diseases, obesity, and age-related conditions further contributed to strong demand and market leadership.

The geriatric patients segment held the second-largest share of 31% in 2025 due to the higher prevalence of chronic diseases, mobility limitations, and age-related health conditions, requiring extended medical care. Older adults frequently need patient positioning devices, pressure-relief surfaces, and mobility aids to enhance comfort and prevent complications. The growing aging population increased hospitalization rates, and rising demand for long-term and home healthcare services further supported the segment’s significant market presence.

The bariatric patients segment held a 14% share in 2025 and is expected to grow at the fastest CAGR of 8.50% in the U.S. patient positioning and support aids market during the forecast period due to the rising prevalence of obesity and related chronic health conditions across the United States. Bariatric patients require specialized positioning devices, support surfaces, and transfer aids designed to accommodate higher weight capacities safely. Increasing bariatric surgical procedures, greater focus on patient safety, and expanding investments in specialized healthcare equipment are further driving segment growth.

The pediatric patients segment held a 10% of the U.S. patient positioning and support aids market share due to increasing demand for child-specific positioning and support solutions in hospitals, surgical centers, and diagnostic imaging facilities. Children require specialized devices that ensure safety, comfort, and proper anatomical alignment during medical procedures. Rising pediatric healthcare utilization, growing awareness of pediatric patient care standards, and advancements in pediatric medical equipment are further contributing to the segment’s continued growth.

")

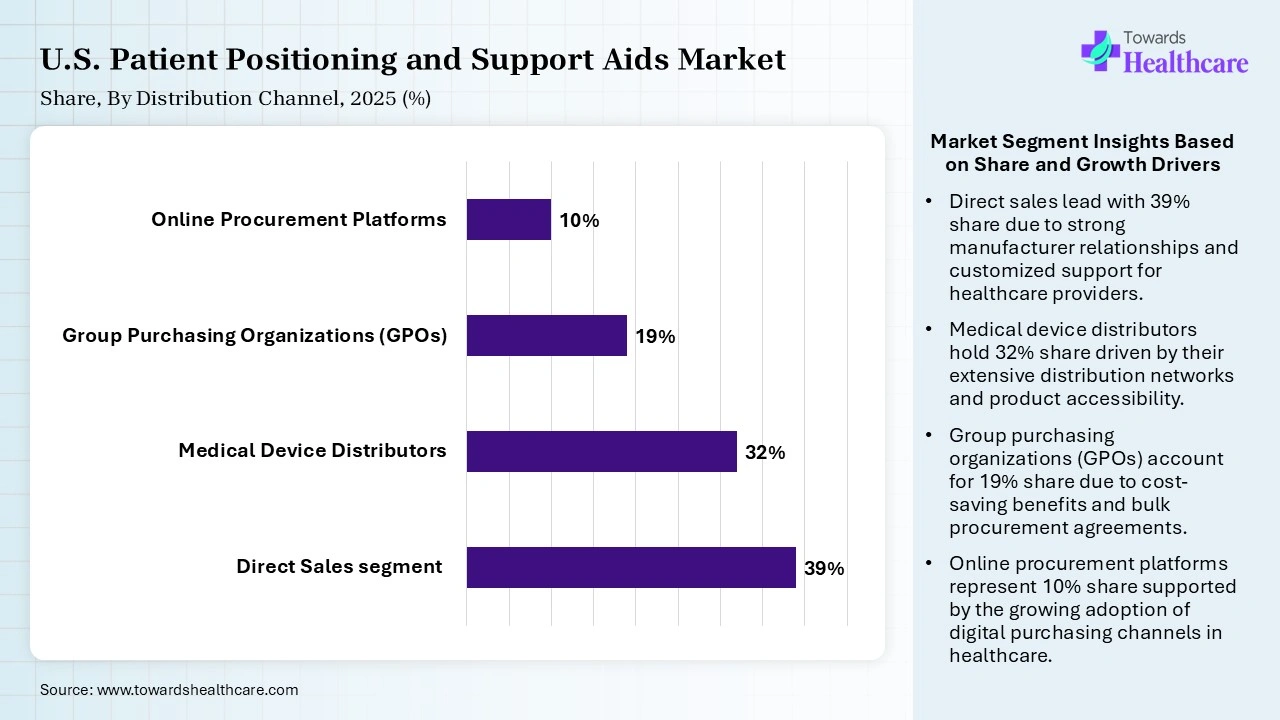

| Segment | Share 2025 (%) |

| Direct Sales segment | 39% |

| Medical Device Distributors | 32% |

| Group Purchasing Organizations (GPOs) | 19% |

| Online Procurement Platforms | 10% |

The Direct Sales Segment Led the U.S. Patient Positioning and Support Aids Market in 2025 with the Largest Share

The direct sales segment held a dominant share of 39% in 2025 due to strong relationships between manufacturers and healthcare providers, including hospitals, surgical centers, and long-term care facilities. Direct sales enable customized product solutions, technical support, bulk purchasing agreements, and faster service delivery. The growing demand for specialized positioning equipment and the need for reliable after-sales support further reinforced the segment’s market leadership.

The medical device distribution segment held the second-largest share of 32% in 2025 due to its extensive networks, broad product availability, and ability to efficiently serve diverse healthcare facilities. Distributors play a crucial role in ensuring timely access to patient positioning and support aids across hospitals, clinics, and long-term care centers. Their established logistics capabilities, product expertise, and value-added services have contributed significantly to the segment’s strong market presence.

The group purchasing organizations (GPOs) segment held a 19% market share due to its ability to help healthcare providers reduce procurement costs and improve purchasing efficiency. GPOs leverage collective buying power to negotiate favorable pricing and contract terms for patients’ positioning and support aids. Increasing cost-containment initiatives across hospitals and healthcare systems, along with the need for streamlined supply chain management, are driving greater adoption of GPO-based purchasing models.

The online procurement platforms segment held a 10% share in 2025 and is expected to grow at the fastest CAGR of 9.10% in the U.S. patient positioning and support aids market during the forecast period due to increasing digitalization of healthcare purchasing processes. These platforms offer a convenient product comparison, streamlined ordering, transparent pricing, and improved supply chain efficiency. Growing adoption of e-commerce solutions by hospitals, ambulatory surgical centers, and long-term care facilities, along with the need for faster procurement and inventory management, is accelerating segment growth.

The U.S. Patient positioning and support aids market led in 2025 due to its advanced healthcare infrastructure, high volume of surgical and diagnostic procedures, and strong adoption of innovative medical technologies. Growing demand for patient safety and pressure technologies. Growing demand for patient safety, pressure injury prevention, and efficient clinical workflows has accelerated the use of positioning and support solutions. Additionally, rising healthcare spending and the presence of leading medical device manufacturers continue to strengthen market growth.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| Stryker Corporation | Kalamazoo, Michigan, USA | Surgical positioning products, operating room support systems, patient transfer solutions |

| Hillrom | Chicago, Illinois, USA | Patient positioning devices, specialty mattresses, pressure injury prevention solutions |

| Arjo | Roswell, Georgia, USA | Patient handling equipment, positioning aids, mobility, and pressure-relief products |

| AliMed | Dedham, Massachusetts, USA | Surgical positioning devices, cushions, gel pads, patient safety products |

| GF Health Products, Inc. | Atlanta, Georgia, USA | Patient support surfaces, transfer aids, positioning accessories |

| EHOB, Inc. | Indianapolis, Indiana, USA | Pressure injury prevention products, positioning cushions, support overlays |

| Span-America Medical Systems | Greenville, South Carolina, USA | Therapeutic mattresses, positioning supports, pressure redistribution products |

| Blue Chip Medical Products, Inc. | Warren, Michigan, USA | Surgical table pads, patient positioning devices, operating room accessories |

In February 2025, “During her Harris Health career, Glorimar has excelled in progressive leadership roles that include medical director, Ambulatory Surgical Center at LBJ Hospital; executive vice president and administrator, Ambulatory Care Services; and most recently, executive vice president and administrator, Ben Taub Hospital,” says Louis Smith, chief operations officer (COO), Harris Health.

By Product Type

By Material

By Application

By End User

By Patient Category

By Distribution Channel

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar