")

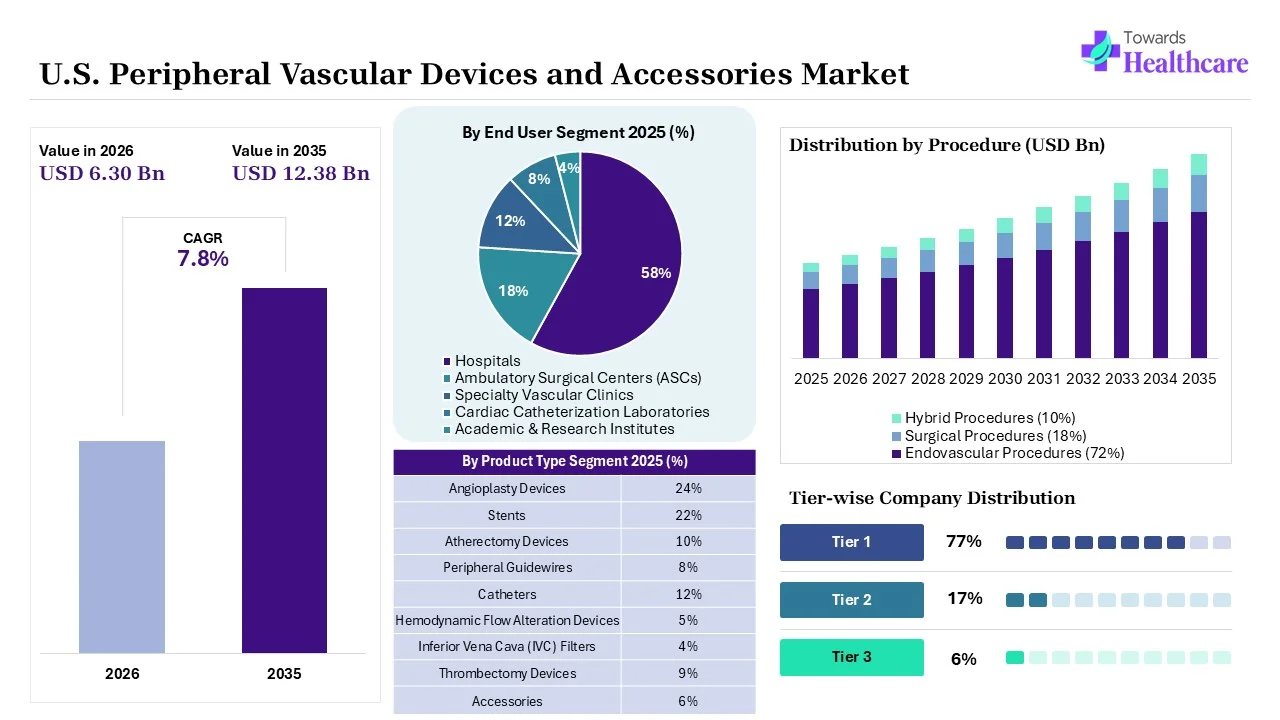

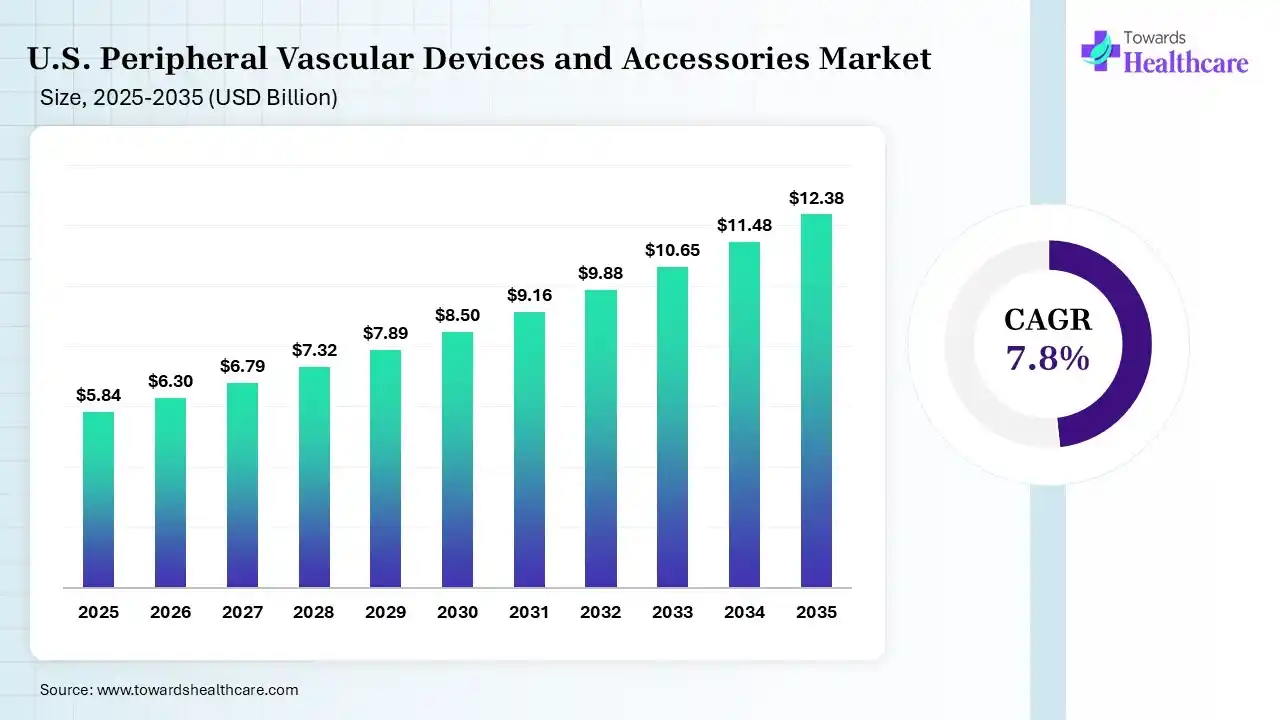

The U.S. peripheral vascular devices and accessories market size was valued at US$ 5.84 billion in 2025 and is projected to grow to 6.3 billion in 2026. Forecasts suggest it will reach approximately US$ 12.38 billion by 2035, registering a CAGR of 7.8% during the period.

")

The U.S. peripheral vascular devices and accessories market is driven by a growing geriatric population, diabetes cases, and a shift towards outpatient labs. The U.S. peripheral vascular devices and accessories encompass medical devices and related accessories used across the U.S. for the diagnosis, treatment, and management of diseases affecting peripheral blood vessels. Peripheral vascular disease (PVD) refers to a circulatory disorder where the blood vessels outside the heart and brain are blocked, narrowed, or damaged, leading to reduced blood flow to the limbs and other body extremities. Peripheral arterial disease, deep vein thrombosis, varicose veins, chronic venous insufficiency, and critical limb ischemia are different types of peripheral vascular diseases. The common causes of the disease are diabetes, high blood pressure, smoking, obesity, and atherosclerosis.

The growing incidence of these diseases is driving the demand for peripheral vascular devices and accessories across the U.S. to help restore blood flow, prevent vessel narrowing, remove blockages, and treat various conditions affecting veins and arteries. The commonly used devices and accessories include stents, catheters, thrombectomy devices, angioplasty balloons, vascular grafts, atherectomy devices, guidewires, and accessory products. Additionally, increasing demand for endovascular procedures, expanding ambulatory surgical centres, and reimbursement support are also increasing their accessibility, where the growing R&D activities, advances in navigation systems, and growing technological innovations are also enhancing the market growth.

The AI offers automated clot detection, differentiating between blood clots and flowing blood, which drives its demand in the U.S. peripheral vascular devices and accessories market. It also helps in real-time high-definition vessel mapping, lesion measurements, and intelligent imaging guidance. AI is also used for the identification of plaques and their characterization, which supports the selection of the correct atherosclerotic surgery accessories and devices. Automated vessel diameter measurements, precision device sizing, and smart navigation assistance also drive the demand for AI in the market.

Blooming Bioresorbable Stents

Metallic stents often cause late-stage complications, which is increasing the development of bioresorbable stents for the treatment of peripheral artery diseases. These stents are developed using safe biomaterials that gradually dissolve after healing, provide temporary vessel support, and offer enhanced flexibility, which increases their demand. Additionally, growing advancements in cardiovascular devices and vascular therapies are also encouraging their use, eliminating the need for long-term devices.

Rising Focus on Limb Preservation

The growing incidence of peripheral artery disease and critical limb ischemia in the U.S. has increased the demand for limb preservation interventions. This, in turn, is promoting the use of early vascular treatment and revascularization procedures to avoid urgent amputations, which is enhancing the use of various peripheral vascular devices and accessories. Expanding hospitals and favourable reimbursement support are also increasing their accessibility, where increasing advancements in angioplasty, thrombectomy, and atherectomy devices are also promoting their use.

Advancements in Device Technologies

To enhance the safety, durability, and effectiveness of the peripheral vascular devices and accessories, the companies are driving the development of new technologies across the U.S. This, in turn, is promoting the development of new drug-coated balloons, drug-eluting stents, advanced catheters, atherectomy systems, guidewires, thrombectomy devices, and other miniature devices. These solutions are expected to improve complex vascular anatomy navigation, promote efficient plaque or clot removal, enhance procedural precision, and improve success rates.

| Table | Scope |

| Market Size in 2026 | USD 6.3 Billion |

| Projected Market Size in 2035 | USD 12.38 Billion |

| CAGR (2026 - 2035) | 7.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Procedure, By Application, By End User |

| Top Key Players | Medtronic plc, Terumo Corporation, Boston Scientific Corporation, Penumbra, Inc., Abbott Laboratories, Cook Medical Inc., Becton, Dickinson and Company (BD) |

")

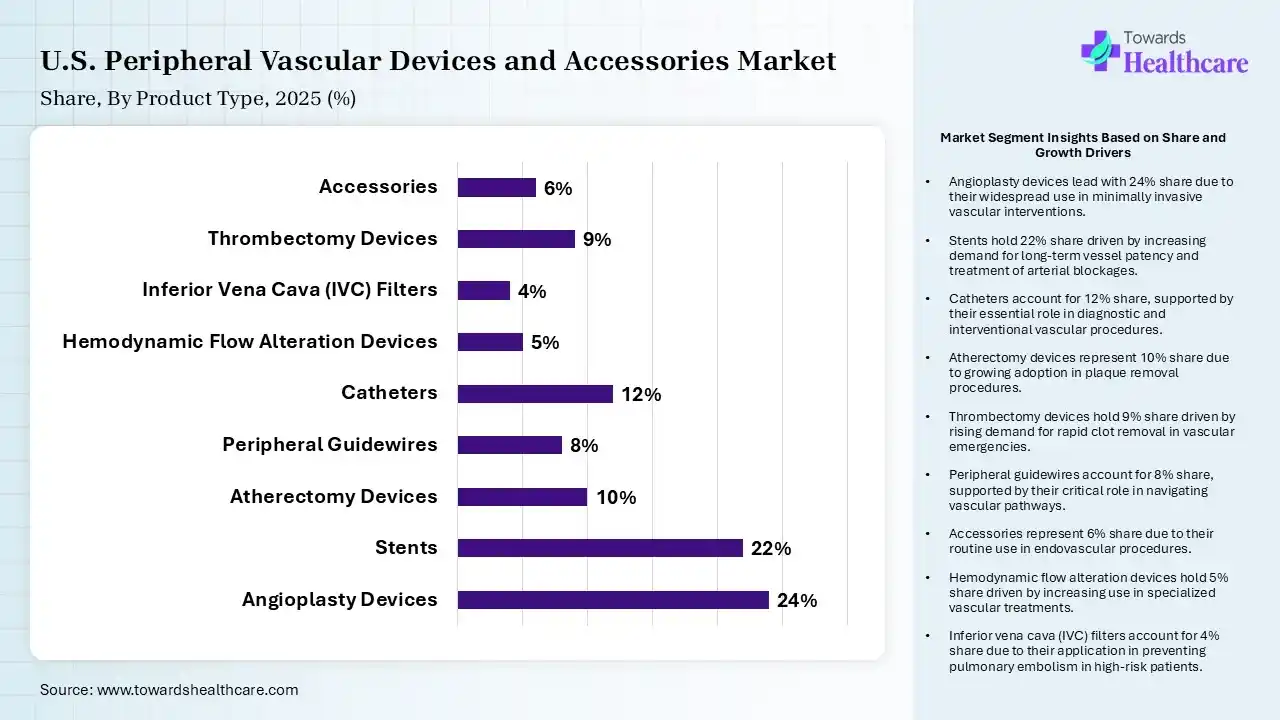

| Segment | Share 2025 (%) |

| Angioplasty Devices | 24% |

| Stents | 22% |

| Atherectomy Devices | 10% |

| Peripheral Guidewires | 8% |

| Catheters | 12% |

| Hemodynamic Flow Alteration Devices | 5% |

| Inferior Vena Cava (IVC) Filters | 4% |

| Thrombectomy Devices | 9% |

| Accessories | 6% |

The Angioplasty Devices Segment Dominated the Market With 24% in 2025

The angioplasty devices segment held the largest revenue share of 24% of the U.S. peripheral vascular devices and accessories market in 2025, due to growth in PAD interventions. Drug-coated balloons also improved outcomes, which increased the use of angioplasty devices. Physicians increasingly preferred minimally invasive treatment, which promoted their use.

The stents segment held the second-largest share of 22% of the market in 2025, driven by growing revascularization procedures, which increase the demand for stents. Improved stent durability, long-term outcomes, and reduced risk of restenosis also support their adoption. The expanding elderly population and advances in stents also drive their demand.

The catheters segment held 12% of the U.S. peripheral vascular devices and accessories market share in 2025, due to growing diagnostic and therapeutic procedures. Microcatheter innovation enhances precision, which encourages its adoption. At the same time, growing intervention complexity and increasing shift towards minimally invasive procedures are also fueling their demand.

The thrombectomy devices segment held 9% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 10.2% during the forecast period, driven by the rising thrombotic disease burden. Faster clot removal technologies are also driving their adoption rates. Hospitals prioritize limb salvage outcomes, which also increases the use of thrombectomy devices.

")

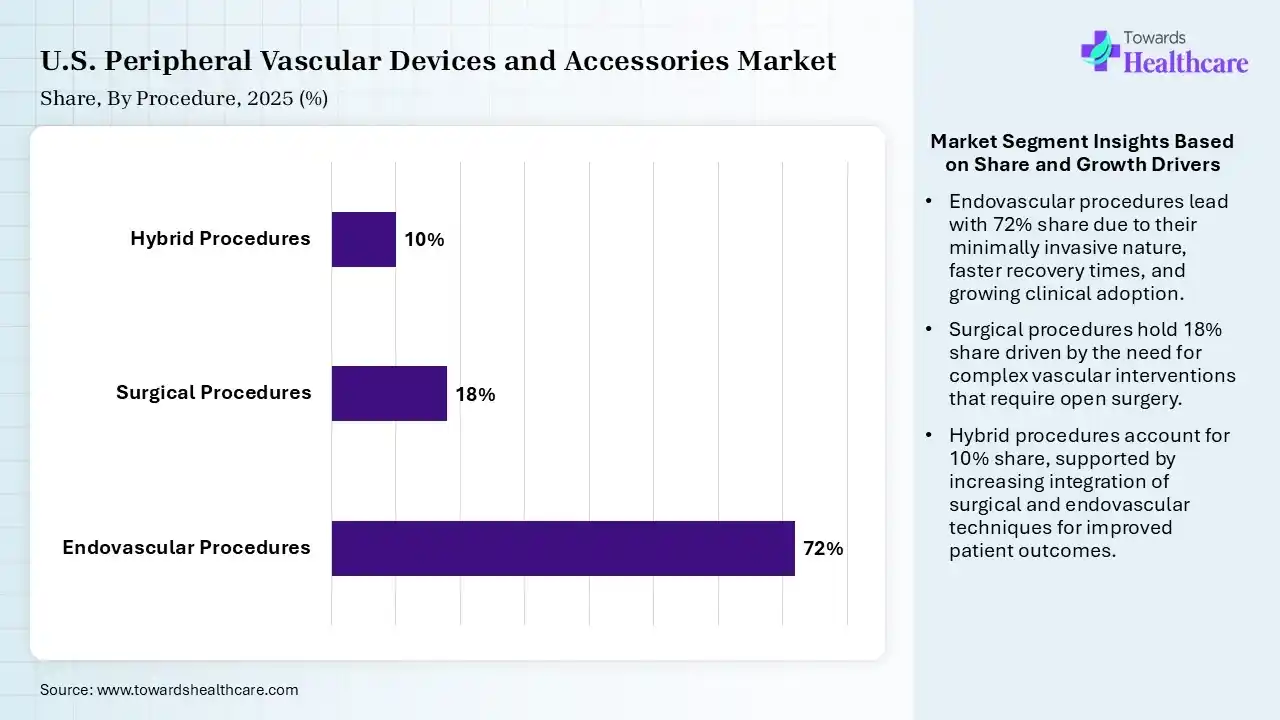

| Segment | Share 2025 (%) |

| Endovascular Procedures | 72% |

| Surgical Procedures | 18% |

| Hybrid Procedures | 10% |

The Endovascular Procedures Segment Dominated the Market With 72% in 2025

The endovascular procedures segment accounted for the highest revenue share of 72% of the U.S. peripheral vascular devices and accessories market in 2025, driven by increased preference by physicians for minimally invasive treatments. Faster recovery improves patient acceptance, which increases the use of endovascular procedures. Technology advancements also expanded the treatable lesions.

The surgical procedures segment held the second-largest share of 18% of the market in 2025, due to the continued rise in demand for surgeries for complex vascular disease. Established reimbursement policies also support these procedures. Severe cases like advanced peripheral artery disease and critical limb ischemia also maintain their utilization.

The hybrid procedures segment held 10% of the U.S. peripheral vascular devices and accessories market share in 2025 and is expected to show the highest growth with a CAGR of 9.1% during the forecast period, driven by the combination approaches that improve outcomes. Hospitals expand hybrid operating suites, which are attracting patients. Increasingly complex PAD cases also support their adoption.

")

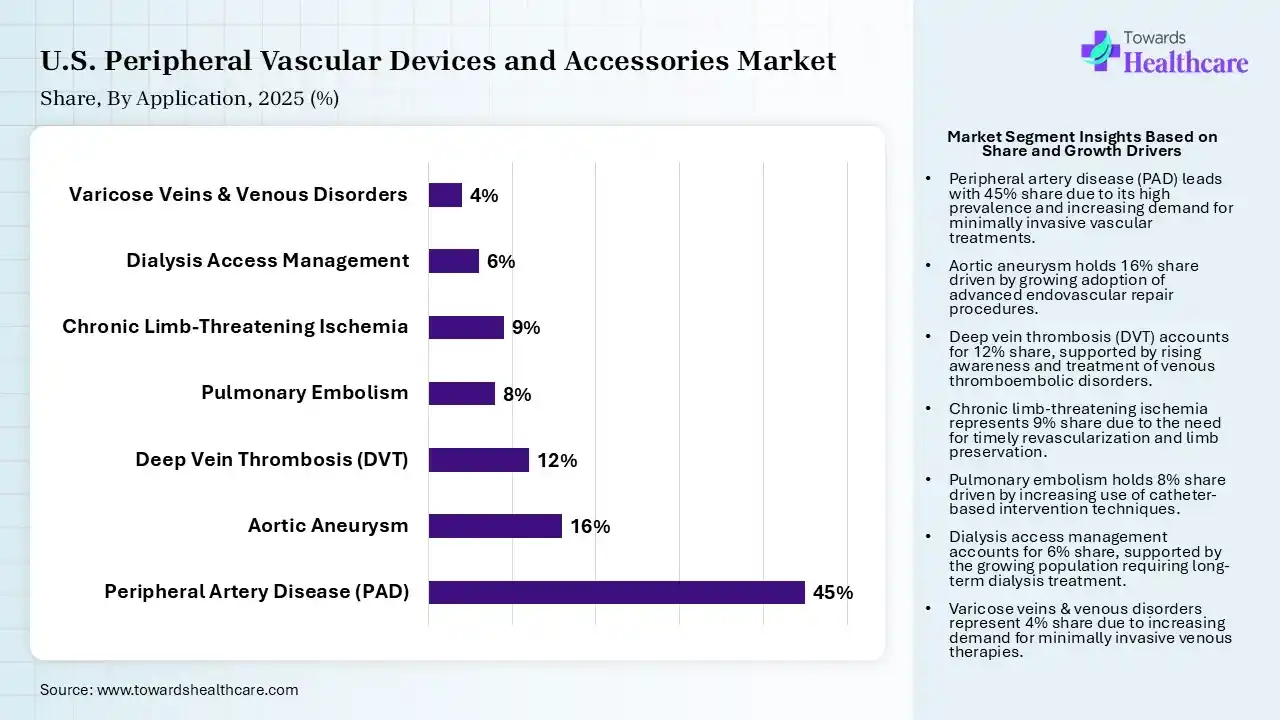

| Segment | Share 2025 (%) |

| Peripheral Artery Disease (PAD) | 45% |

| Aortic Aneurysm | 16% |

| Deep Vein Thrombosis (DVT) | 12% |

| Pulmonary Embolism | 8% |

| Chronic Limb-Threatening Ischemia | 9% |

| Dialysis Access Management | 6% |

| Varicose Veins & Venous Disorders | 4% |

The Peripheral Artery Disease (PAD) Segment Dominated the Market With 45% in 2025

The peripheral artery disease (PAD) segment held a major revenue share of 45% of the U.S. peripheral vascular devices and accessories market in 2025, due to the growth of diabetes prevalence, which increased PAD incidence. The rise in the demand for early diagnosis also expanded their intervention rates. Growth in the advanced devices also improved treatment success.

The aortic aneurysm segment held the second-largest share of 16% of the market in 2025, driven by an expansion in the screening programs that identify more patients. Endovascular repair adoption continues to rise, which drives the demand for peripheral vascular devices and accessories. A rise in the aging population also supports their growth.

The deep vein thrombosis (DVT) segment held 12% of the U.S. peripheral vascular devices and accessories market share in 2025, due to the rising venous disease burden. Greater awareness is driving their early diagnosis, fueling the demand for peripheral vascular devices and their accessories. Expanding use of mechanical thrombectomy is also attracting patients.

The pulmonary embolism segment held 8% of the market share in 2025 and is expected to expand rapidly with a CAGR of 9.3% during the forecast period, driven by increasing catheter-directed therapies. Hospitals prioritize rapid clot removal, which has increased the use of various peripheral vascular devices. Clinical evidence also supports intervention adoption.

")

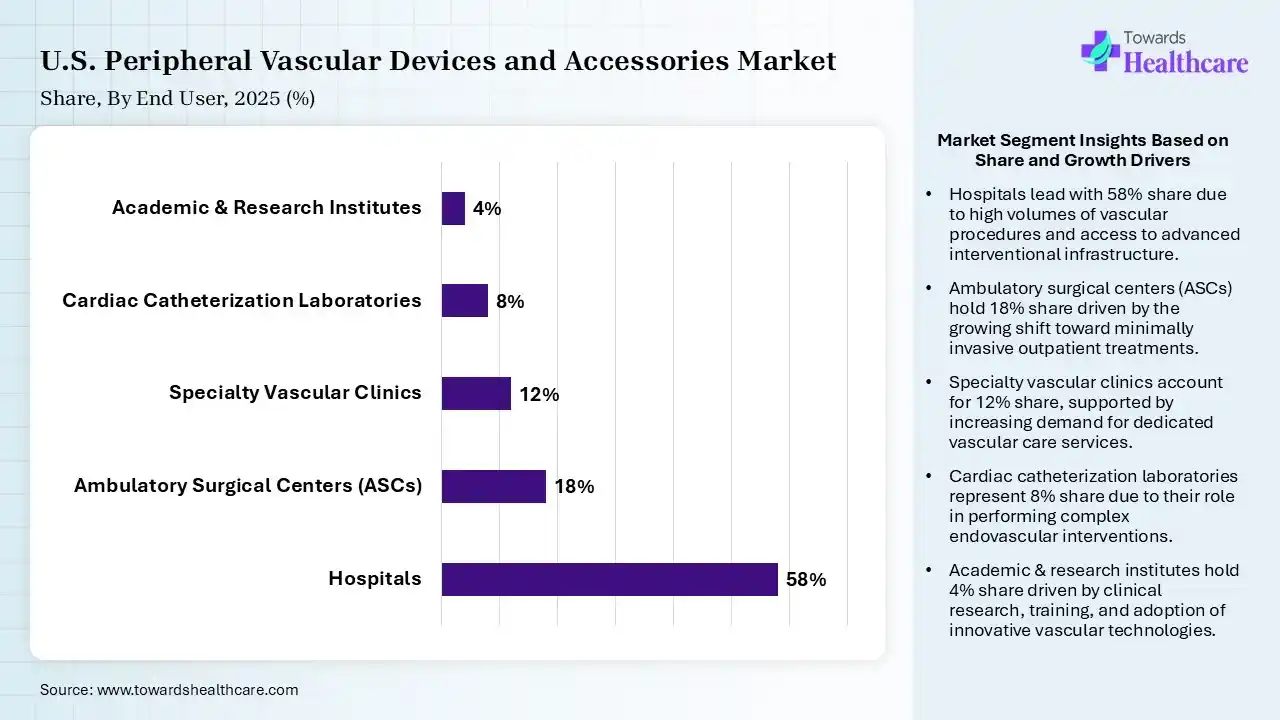

| Segment | Share 2025 (%) |

| Hospitals | 58% |

| Ambulatory Surgical Centers (ASCs) | 18% |

| Specialty Vascular Clinics | 12% |

| Cardiac Catheterization Laboratories | 8% |

| Academic & Research Institutes | 4% |

The Hospitals Segment Dominated the Market With 58% in 2025

The hospitals segment contributed the biggest revenue share of 58% of the U.S. peripheral vascular devices and accessories market in 2025, driven by large patient volumes, which increased the peripheral vascular devices and accessories utilization. Access to advanced imaging also supported the procedures, which increased their acceptance rates. Comprehensive care capabilities also attracted referrals.

The ambulatory surgical centers (ASCs) segment held the second-largest share of 18% of the market in 2025 and is expected to gain the highest share with a CAGR of 9.4% during the forecast period, due to the shift toward outpatient care, which accelerates their adoption. Lower procedure costs are also attracting the payers. Faster patient throughput improves efficiency, encouraging their use.

The specialty vascular clinics segment held 12% of the U.S. peripheral vascular devices and accessories market share in 2025, driven by dedicated vascular care, which increases procedure volumes. Expanding services through the physician-owned facilities is also attracting patients. At the same time, enhanced patient convenience also supports their growth.

The cardiac catheterization laboratories segment held 8% of the market share in 2025, due to existing infrastructure that supports peripheral interventions. Technology upgrades enhance the peripheral vascular device and accessories' capabilities, increasing their use. A rise in their interventional expertise and the availability of minimally invasive procedures also drive their demand.

The U.S. peripheral vascular devices and accessories market is expected to show notable growth during the forecast period, due to growth in the geriatric population and peripheral artery diseases. The growth in cardiovascular and diabetes cases also led to a rise in PAD patients, which increased the use of peripheral vascular devices and their accessories, where the advanced healthcare sector, offering favourable reimbursement support, is also increasing their accessibility. Expanding ambulatory surgical centres also increases their adoption rates, where a rise in the demand for minimally invasive approaches is also driving their demand. Additionally, advanced industries and investments are also accelerating their innovations, which is enhancing the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | U.S. Peripheral Vascular Devices and Accessories Solutions |

| Medtronic plc | Dublin, Ireland | IN.PACT Admiral, SpiderFX, and EverFlex |

| Terumo Corporation | Tokyo, Japan | Radifocus Glide, Pinnacle, and Misago RX |

| Boston Scientific Corporation | Marlborough, U.S. | Eluvia, Jetstream, and Ranger |

| Penumbra, Inc. | Alameda, U.S. | Indigo System, Ruby Coil, and Lightning Intelligent Aspiration |

| Abbott Laboratories | Abbott Park, U.S. | Supera, ProGlide, and Armada |

| Cook Medical Inc. | Bloomington, U.S. | Beacon Tip, Zilver PTX, and Coda |

| Becton, Dickinson and Company (BD) | Franklin Lakes, U.S. | Lutonix 035, Rotarex S, and LifeStent |

In November 2025, after receiving 510(k) clearance from the U.S. FDA for the Recana Thrombectomy Catheter System, the CEO of InterVene, Inc., Jeff Elkins, expressed that “Venous in-stent restenosis and residual native vessel obstructions can lead to long-lasting, debilitating complications for many patients and remain difficult to treat. With the launch of the Recana System, we’re introducing a next-generation technology designed to address this critical need and significantly improve patient outcomes.”

By Product Type

By Procedure

By Application

By End User

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar