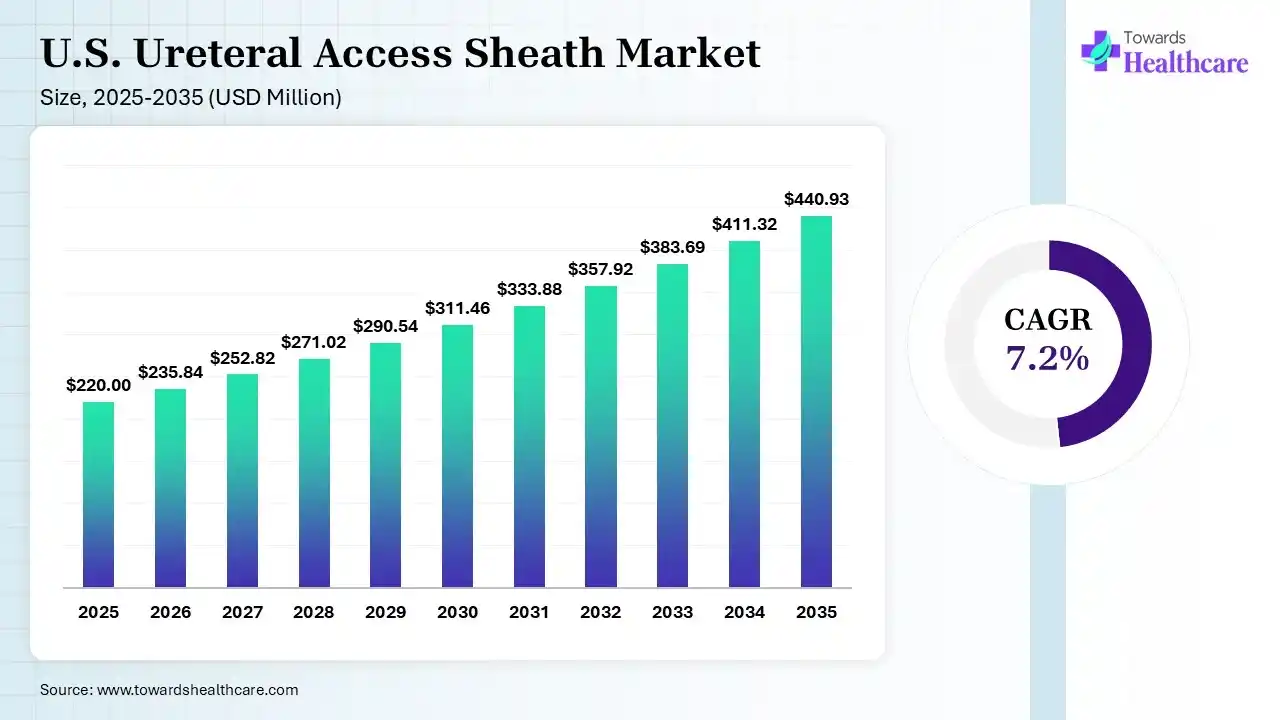

The U.S. ureteral access sheath market size was estimated at USD 220 million in 2025 and is predicted to increase from USD 235.84 million in 2026 to approximately USD 440.93 million by 2035, expanding at a CAGR of 7.2% from 2026 to 2035. The U.S. ureteral access sheath market is growing due to the growing prevalence of kidney stones, the modification to minimally invasive technology, the growth in outpatient care, and better-quality patient safety.

")

The U.S. ureteral access sheath market is growing, as this type of sheath (UASs) is part of a urologist's armamentarium when performing retrograde intrarenal surgery (RIRS). Ureteral access sheaths (UASs) are applied to protect the FURS scope and lower intrarenal pressure. UASs through suction functionality are progressively used during FURS. Ureteral access sheath is a specialized tool applied during ureteroscopic and retrograde intrarenal operations. It offers an incessant access channel to the ureter and kidney, enabling safe passage of flexible tools. This sheath supports lowers trauma and maintains consistent dilation through the technology. They became broadly adopted in the 2000s as flexible ureteroscopes increased in popularity. The ureteral access sheath is a significant device in modern endourological technology, offering a balance of access, safety, and control for urologists.

AI-driven technology in the U.S. ureteral access sheath provides planning, execution, and postoperative assessment, which optimizes stone targeting, enhances navigation, and elevates overall action precision. The continuing development of these technologies is completed by the entrance of AI-based technology into urological procedures. AI-based systems analyse 2D fluoroscopic images to reconstruct 3D replicas of the ureter for advanced navigation and planning. AI-based support to minimize the challenges of post-operative infectious complications such as urosepsis and renal injury.

| Table | Scope |

| Market Size in 2026 | USD 235.84 Million |

| Projected Market Size in 2035 | USD 440.93 Million |

| CAGR (2026 - 2035) | 7.2% |

| Key Applications | Kidney stone management, ureteroscopy, laser lithotripsy, retrograde intrarenal surgery (RIRS), diagnostic ureteroscopy, ureteral tumor biopsy |

| Primary End Users | Hospitals, Ambulatory Surgery Centers (ASCs), Specialty Urology Clinics |

| Key Challenges | Ureteral injury risks, pricing pressure, reimbursement constraints, physician preference variability, regulatory requirements |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Material, By Size (Diameter), By Length, By End User, By Usage, By Application, By Distribution Channel |

| Top Key Players | Applied Medical Resources Corporation, BD, Merit Medical Systems, Inc., Boston Scientific Corporation, Rocamed, Well Lead Medical |

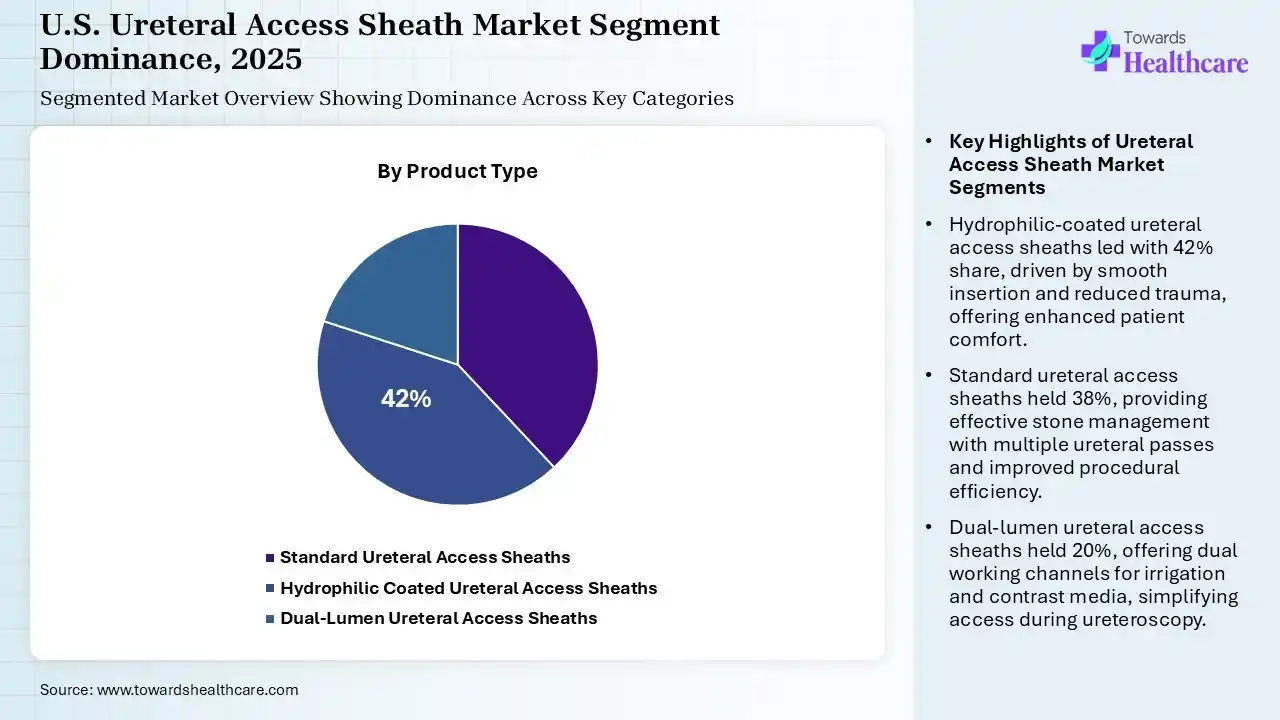

The Hydrophilic-Coated Ureteral Access Sheaths Segment Led the U.S. Ureteral Access Sheath Market in 2025

| Segment | Share 2025 (%) |

| Standard Ureteral Access Sheaths | 38% |

| Hydrophilic Coated Ureteral Access Sheaths | 42% |

| Dual-Lumen Ureteral Access Sheaths | 20% |

The hydrophilic-coated ureteral access sheaths segment held 42% share of the U.S. ureteral access sheath market in 2025, and is estimated to grow at the highest CAGR of 7.50% as hydrophilic coating allows smooth insertion and negligible trauma. Hydrophilic coatings substantially lower the friction between the sheath and ureteral walls, enhancing insertion smoothness and patient comfort.

The standard ureteral access sheaths segment held 38% in 2025, as it offers a pathway for the entry of the ureteroscope and drainage in the ureter, helping in determining the aforementioned challenges. It allows multiple ureteral passes, enhancing time effectiveness and procedural standardization in stone management. The S-UAS facilitates effective stone dust evacuation, enhances immediate clinically acceptable SFRs, and lowers auxiliary technology rates without growing complications.

Whereas the dual-lumen ureteral access sheaths segment held a notable share of 20% in the market in 2025, as a dual-lumen catheter intended for over-the-wire placement, offering two separate working channels for second wire placement or injection. It provides simple access for delivering irrigation fluid and contrast media into the renal cavities while using ureteroscopy technology by keeping the guidewire in place.

Polymer-based Sheaths Segment Led the U.S. Ureteral Access Sheath Market in 2025

| Segment | Share 2025 (%) |

| Polymer-based Sheaths | 55% |

| Silicone-based Sheaths | 20% |

| Hybrid Materials | 25% |

The polymer-based sheaths segment captured the largest market share of approximately 55% in 2025, as polyolefin sheath materials offer numerous benefits, including durability, chemical resistance, flexibility, thermal stability, electrical insulation properties, environmental resistance, cost-effectiveness, safety, and versatility. These advantages make them an excellent choice for protecting and insulating cables in various applications.

The hybrid materials segment held the second largest share of approximately 25% of the U.S. ureteral access sheath market in 2025, and is expected to grow at a CAGR of 7.10% during the predicted time as it enhances the balance among insertion safety, navigating challenging anatomy, and increasing surgical efficiency. The applications of ureteral access sheaths (UAS) improve both access and the process's efficiency. It offers major benefits such as lessening of intrarenal pressure, lowering the risk of infection, enhanced irrigation and drainage, and improved visualization during stone retrieval.

Whereas the silicone-based sheaths segment held a notable share of 20% in the market in 2025, as silicone is a super smooth material with an increasing degree of flexibility, making insertion easy and leading to less irritation to the urethra. They have minimal encrustation as compared to latex and are more tissue-friendly.

The Disposable (single-use) Segment held the Largest Share in the Market in 2025

| Segment | Share 2025 (%) |

| Disposable (Single-use) | 70% |

| Reusable | 30% |

The disposable (single-use) segment contributed the largest market share of approximately 70% in 2025, and is expected to grow at the highest CAGR of 7.60% during the forecast period, as disposable ureteral access sheaths (UAS) are significant tools in modern retrograde intrarenal surgery (RIRS), intended to simplify safe and well-organized access to the upper urinary tract. It has evolved as a less invasive substitute to percutaneous nephrolithotomy while handling larger renal stones.

The reusable segment held the second largest share of 30% of the U.S. ureteral access sheath market in 2025. Reusable laparoscopic tools substantially lower the expenses of laparoscopic operations, without compromising the safety of patients and healthcare personnel. Reusables provide significant long-standing cost savings, particularly in amenities with specialized or lower-volume technology.

The Kidney Stone Management Segment held the Largest Share of the Market in 2025

| Segment | Share 2025 (%) |

| Kidney Stone Management | 65% |

| Ureteral Stricture Management | 20% |

| Diagnostic Procedures | 15% |

The kidney stone management segment contributed the largest market share of approximately 65% in 2025, and is estimated to grow at a CAGR of 7.30% during 2026-2035 as applications of UAS for renal stones are safe with no intra-operative challenges. Ureteral access sheaths allow multiple ureteral passes, enhancing time effectiveness and technical standardization in stone management. The flexible vacuum-driven ureteral access sheath integrated with a flexible ureteroscope is effective in the treatment of large renal stones over 3 cm.

The ureteral stricture management segment held the second largest share of 20% of the U.S. ureteral access sheath market in 2025, as it offers an opportunity for the entry of the ureteroscope and drainage in the ureter, assisting in undertaking the aforementioned challenges. It enhances intraoperative visibility and lowers postoperative difficulties.

Whereas the diagnostic procedures segment held a notable share of 15% in the market in 2025, as the ureteral access sheath helps to better irrigation flow and lowers intrarenal pressure during complex stone removal technology. Facilitating easy and safe access during ureteroscopy and RIRS measures.

The Direct Sales Segment held the Largest Share of the Market in 2025

| Segment | Share 2025 (%) |

| Direct Sales | 50% |

| Distributors | 35% |

| Online Sales | 15% |

The direct sales segment contributed the largest market share of 50% in 2025, as the direct sales approach enables businesses to engage customers without intermediaries, allowing for greater control over the sales process, pricing, and customer relationships. Direct sales typically possess more control over prices because these companies don't require wholesalers and retailers or store spaces.

The distributors segment held the second largest share of 35% of the U.S. ureteral access sheath market in 2025, as distributors provide designed, local sales teams who offer immediate technical help and training to physicians, which is significant for the acceptance of specialized devices such as suction-enabled or tip-bendable UAS.

Whereas the online sales segment held a notable share of approximately 15% of the market in 2025, and is estimated to achieve the highest growth rate of 8.10%, because it provides major advantages, such as saving time and expenses, and having access to a broad range of ureteral products. Online sales of healthcare devices that provide remote patient monitoring. It is also beneficial because it provides a significant level of convenience.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Boston Scientific, Olympus, BD, Cook Medical | Design and development of access sheath technologies, coatings, materials, and procedural innovations |

| Product Manufacturers | Boston Scientific, Cook Medical, Olympus, Coloplast, BD, Richard Wolf | Manufacturing and commercialization of ureteral access sheaths |

| Service Providers | Hospitals, ASCs, Urology Centers | Clinical utilization during ureteroscopy and stone removal procedures |

| Platform Providers | Olympus, Boston Scientific, Richard Wolf, Karl Storz | Integrated endourology platforms combining ureteroscopes and access devices |

| CROs / Clinical Research Organizations | IQVIA, ICON, Parexel | Support clinical studies and regulatory validation of urology devices |

| Software Vendors | Olympus Digital Solutions, Boston Scientific Digital Health Platforms | Procedure workflow and imaging integration |

| Research Institutions | Mayo Clinic, Cleveland Clinic, Johns Hopkins Medicine | Clinical research and evaluation of endourology technologies |

| End-User Industries | Hospitals, Ambulatory Surgery Centers, Specialty Urology Practices | Final purchasers and users of UAS products |

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 72% | 20% | 8% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Boston Scientific Corporation | Marlborough, Massachusetts | USA | Market leader with extensive endourology portfolio and Navigator UAS family | Navigator™ Ureteral Access Sheath, Navigator™ HD UAS |

| Cook Medical | Bloomington, Indiana | USA | Long-established leader in stone management and ureteral access technologies | Flexor® Ureteral Access Sheaths |

| Olympus Corporation | Tokyo | Japan | Major U.S. endourology presence and integrated ureteroscopy ecosystem | Ureteroscopy systems and access sheaths |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Richard Wolf GmbH | Knittlingen | Germany | Leading endourology equipment manufacturer | Endoscopic urology access solutions |

| Applied Medical Resources Corporation | Rancho Santa Margarita, California | USA | Active in minimally invasive surgical access technologies | Urology procedural access devices |

| Rocamed SAM | Monaco | Monaco | Strong European and growing U.S. urology footprint | Ureteral access and stone management devices |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| AMECATH | Cairo | Egypt | Growing international urology device supplier | Ureteral access sheaths |

| ACE Medical Devices | Seoul | South Korea | Specialized disposable urology devices | Access sheath portfolio |

| SCW Medicath Ltd | Shenzhen, Guangdong | China | Emerging global exporter of urology consumables | UAS and stone management products |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Material

By Size (Diameter)

By Length

By End User

By Usage

By Application

By Distribution Channel

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar