Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

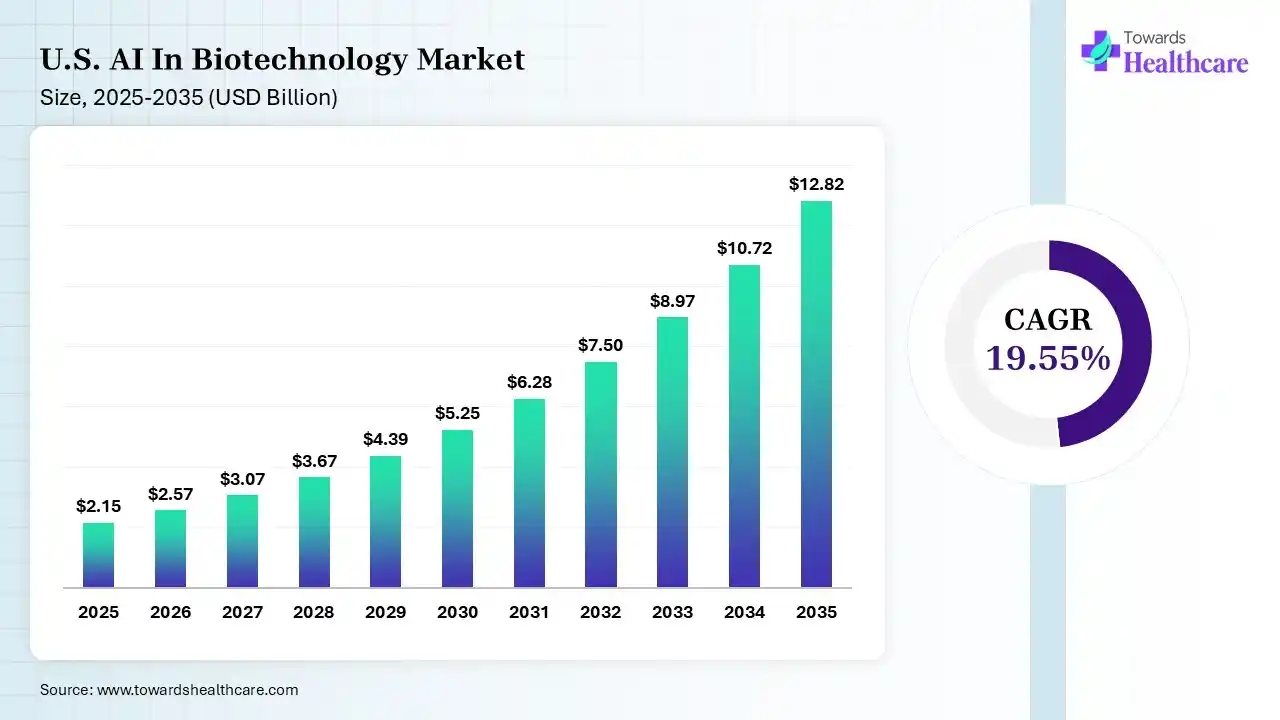

The U.S. AI in biotechnology market size was estimated at USD 2.15 billion in 2025 and is predicted to increase from USD 2.57 billion in 2026 to approximately USD 12.82 billion by 2035, expanding at a CAGR of 19.55% from 2026 to 2035.

")

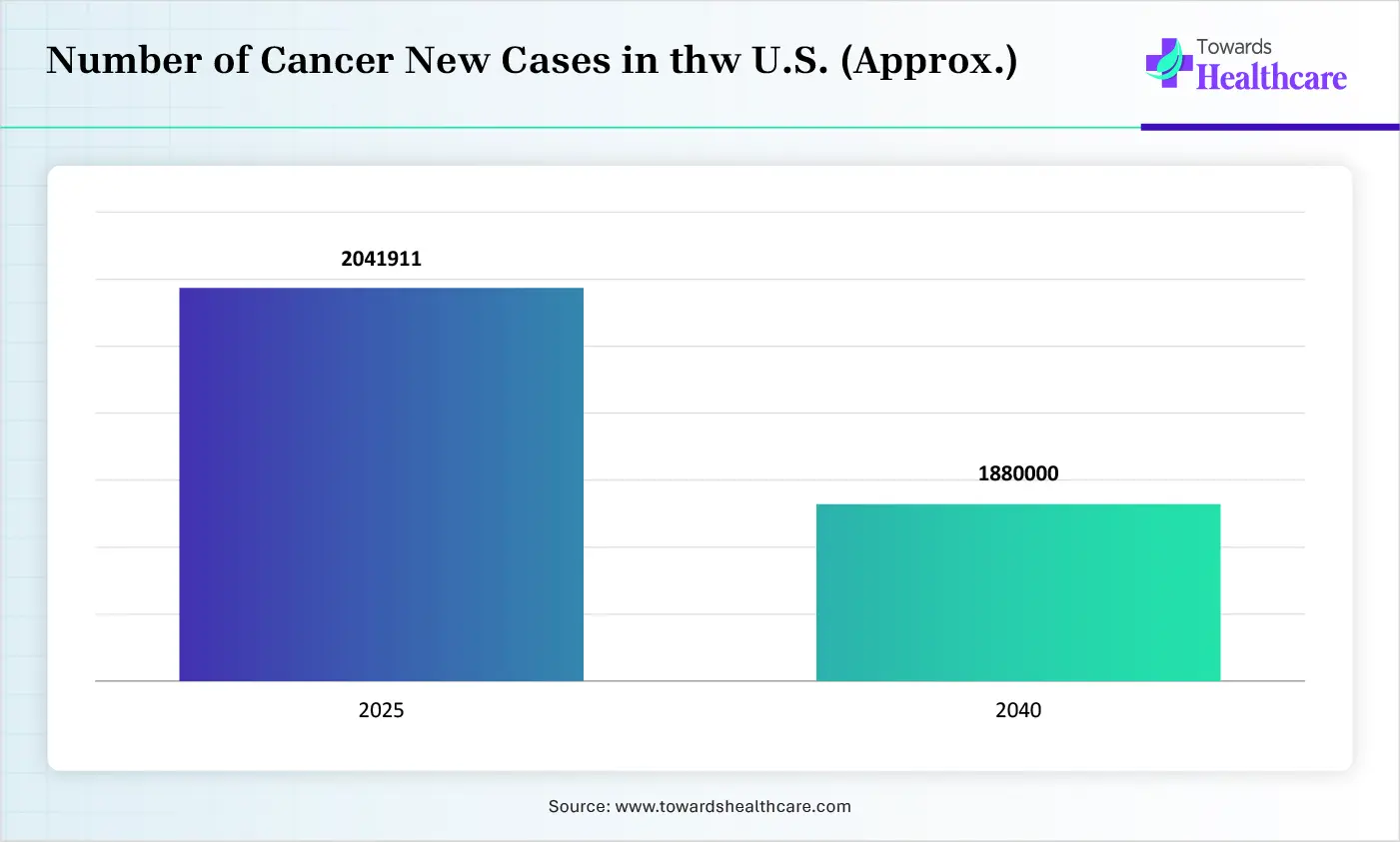

Gradually rising chronic issues, cancer cases are propelling the demand for advanced and novel therapeutics by using AI-powered solutions in drug discovery & development. Ongoing R&D pipelines are increasingly leveraging AI algorithms to reduce the comprehensive costs and time consumption.

This mainly leverages machine learning, deep learning, & sophisticated algorithms in the study of complex biological data, surge drug discovery, protein engineering, & precision medicine. The overall U.S. AI in biotechnology market is fueled by a rise in the need for expedited drug discovery & development, where AI assists in discovering drug targets, estimating molecular interactions, etc. The growing demand for tailored medicine is driving the adoption of AI in the analysis of huge datasets. Moreover, the key pharmaceutical players in the U.S. are joining with AI-specialised firms to implement cutting-edge algorithms & improve their research capabilities.

Focused on Protein Binder Design

Companies are employing AI tools, such as RFdiffusion and AlphaFold, to generate protein binders with sub-Ångström structural fidelity, which allows the targeting of previously undruggable proteins.

Shifting Towards Digital Cell & Simulation

Several key firms are establishing digital twins of cells and molecules to simulate behavior, which lowers wet-lab experimentation, and prominently uses AI to enhance biomanufacturing processes & cell programming.

Transforming Explainable AI (XAI)

A notable effort has been taken in revolutionizing ‘interpretable’ AI models to offer understandable reasons for their decisions, which is essential for regulatory approval in clinical diagnostics.

| Table | Scope |

| Market Size in 2026 | USD 2.57 Billion |

| Projected Market Size in 2035 | USD 12.82 Billion |

| CAGR (2026 - 2035) | 19.55% |

| Key Applications | Drug discovery, target identification, protein design, biomarker discovery, genomics analysis, clinical trial optimization, precision medicine, synthetic biology, antibody engineering |

| Primary End Users | Biotechnology companies, pharmaceutical companies, research institutes, CROs, healthcare organizations, academic laboratories |

| Key Growth Drivers | Rising R&D costs, need for faster drug discovery, advances in generative AI, increasing biotech data volumes, pharma-AI partnerships, precision medicine adoption |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Primary Application/Use Case, By Core AI Technology, By Commercial Model, By End User/Buyer Type |

| Top Key Players | NVIDIA Corporation, Recursion Pharmaceuticals, Schrödinger, Inc., Tempus AI, Insilico Medicine, Atomwise, BPGbio, Generate Biomedicines, Verge Genomics, Relay Therapeutics |

")

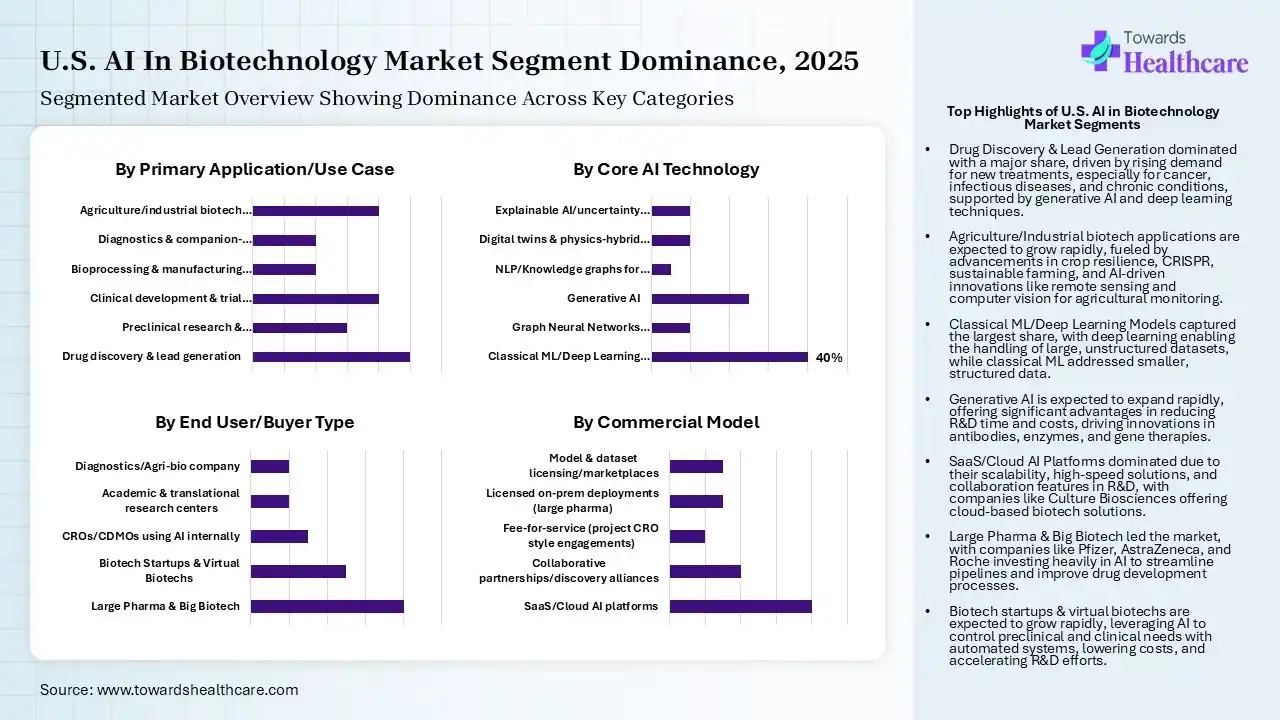

How did the Drug Discovery & Lead Generation Segment Dominate the Market in 2025?

| Segment | Share 2025 (%) |

| Drug discovery & lead generation | 25% |

| Preclinical research & biomarker discovery | 15% |

| Clinical development & trial optimization | 20% |

| Bioprocessing & manufacturing optimization (PAT, yield, QC) | 10% |

| Diagnostics & companion-diagnostics (AI for image/omics readouts) | 10% |

| Agriculture/industrial biotech applications | 20% |

Explanation

In 2025, the drug discovery & lead generation segment held a major share of the U.S. AI in biotechnology market by 25%. Rising demand for new treatments in the accelerating cancer, infectious diseases, and chronic issues, drives the need for novel drug molecules & its discovery efforts. Whereas, for this, generative AI, deep learning, and advanced molecular docking are enabling the development of new, stable proteins and small molecules with enhanced pharmacokinetics. Also, certain firms are using knowledge graphs to find pathogenic genes & select drug targets.

Agriculture/Industrial Biotech Applications

In the future, the agriculture/industrial biotech applications segment is estimated to show rapid growth. Ongoing emphasis on increasing crop resilience, i.e., CRISPR, synthetic biology, sustainable livestock management, & improving bioprocessing is propelling the segmental expansion. Trends mainly include the utilization of AI and remote sensing to track soil carbon sequestration and ensure sustainability metrics. Also, the wider population is leveraging AI-driven computer vision on tractors to monitor fruit size, color, and load. Specific virtual screening supports designing new molecules to target specific proteins in weeds, pests, & diseases.

Which Core AI Technology Led the U.S. AI in Biotechnology Market in 2025?

| Segment | Share 2025 (%) |

| Classical ML/Deep Learning models | 40% |

| Graph Neural Networks (molecular GNNs) | 10% |

| Generative AI | 25% |

| NLP/Knowledge graphs for literature & IP mining | 5% |

| Digital twins & physics-hybrid models | 10% |

| Explainable AI/uncertainty quantification | 10% |

Explanation

The classical ML/deep learning models segment captured the dominating share of the market by 40% in 2025. Firstly, classical ML offers strong, interpretable, and computationally potent solutions for smaller, structured datasets, whereas deep learning manages unstructured data & high-dimensional, vast datasets. Firms are shifting towards transformers to analyze biological sequences as language, and which anticipate structures of all molecules & their interactions. However, models including ESM-2 enable direct 3D structure prediction from a single sequence, with the elimination of the time-consuming multiple sequence alignments (MSA).

Generative AI

Moreover, the generative AI segment is anticipated to expand fastest. Gen AI has numerous advantages, like minimal R&D time by 23–38% and expenditures by 8–15%, with uses in emerging novel antibodies, enzymes, and targeted gene therapies. Also, it is revolutionizing the biotech sector through molecular design, predictive analytics, and automated workflows. The U.S. biotechnology industry is focusing on broader use of gen AI to integrate AI into wet lab experimentation, fostering AI-developed drugs into clinical trials, and establishing ‘digital cell’ models.

Which Commercial Model Dominated the U.S. AI in Biotechnology Market in 2025?

| Segment | Share 2025 (%) |

| SaaS/Cloud AI platforms | 40% |

| Collaborative partnerships/discovery alliances | 20% |

| Fee-for-service (project CRO style engagements) | 10% |

| Licensed on-prem deployments (large pharma) | 15% |

| Model & dataset licensing/marketplaces | 15% |

Explanation

In 2025, the SaaS/cloud AI platforms segment led the market by 40% in 2025 & is predicted to expand rapidly. Its dominance is driven by its high-speed, collaborative, & scalable digital solutions in R&D processes. Also, these platforms allow biotech firms to employ advanced AI models without the requirement for huge, upfront in-house infrastructure investments. Across the U.S., leaders like Culture Biosciences are developing ‘Amazon Web Services for biotechnology,’ which enables researchers to handle bioreactors & continue experiments through the cloud.

Why did the Large Pharma & Big Biotech Segment Lead the Market in 2025?

| Segment | Share 2025 (%) |

| Large Pharma & Big Biotech | 40% |

| Biotech Startups & Virtual Biotechs | 25% |

| CROs/CDMOs using AI internally | 15% |

| Academic & translational research centers | 10% |

| Diagnostics/Agri-bio company | 10% |

Explanation

The large pharma & big biotech segment held the biggest share of the U.S. AI in biotechnology market by 40% in 2025. Specifically, Pfizer, AstraZeneca, Roche, and Novartis, like giant companies, are massively investing in AI to simplify pipelines. Many large pharma leaders are joining with AI specialists, such as Sanofi with Insilico and Exscientia, to achieve expertise in computational design, target detection, & trial improvement.

Biotech Startups & Virtual Biotechs

On the other hand, the biotech startups & virtual biotechs segment is estimated to register rapid expansion. Numerous of these types of firms are moving from pure drug discovery to AI-native platforms that integrate data generation, molecular design, and clinical development. However, virtual biotechs are widely using AI to control 100% of their preclinical and clinical requirements via alliances and automated labs, which lowers capital investment in physical infrastructure & maintain higher R&D speed.

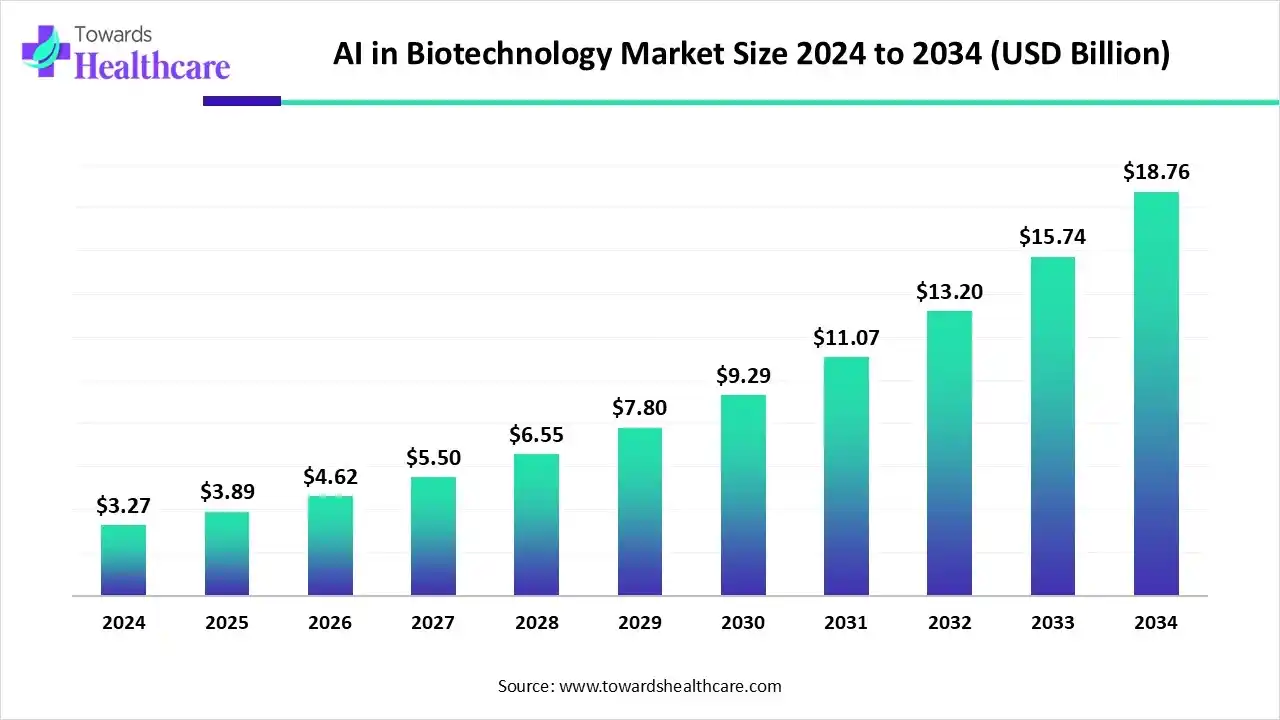

The AI in biotechnology market size reached US$ 3.89 billion in 2025 and is anticipate to increase to US$ 4.63 billion in 2026. By 2035, the market is forecasted to achieve a value of around US$ 22.23 billion, growing at a CAGR of 19.04%.

The U.S. AI in biotechnology market is growing rapidly, dominated by intense activity in California and Massachusetts, which act as primary hubs for AI-driven drug discovery and genomics. San Francisco and Boston concentrate top-tier talent, venture capital funding, and major AI-biotech partnerships, driving the adoption of machine learning in molecular modeling. These regions focus on accelerating early-stage R&D, utilizing advanced AI platforms to reduce the time from target identification to clinical trials.

Texas and Mid-Atlantic Boost Adoption

Growth is expanding significantly in Texas and the Mid-Atlantic, driven by robust institutional investments and the presence of advanced healthcare systems, particularly in medical centers like Houston and Philadelphia. These areas are increasingly implementing AI to optimize biopharmaceutical manufacturing and supply chain logistics, reflecting a shift from pure research toward operational efficiency. The integration of AI tools for personalized medicine is also a major focus, driven by regional partnerships and growing data availability.

The Midwest and Southeast regions are experiencing growth through increased collaborations between AI tech companies and traditional pharmaceutical manufacturers. States like North Carolina are leveraging their research triangle to foster AI in agricultural biotechnology and agricultural-based precision medicine. This regional growth is supported by a surge in demand for AI-driven analytics to improve diagnostic accuracy, bridging the gap between clinical research and commercialized biotech solutions.

Digital Transformation Drives National Growth

Nationwide, the adoption of cloud-based AI solutions is empowering regional hubs to share data, enabling the rapid development of novel biopharmaceuticals. While California and Massachusetts remain key, digital infrastructure allows for widespread AI adoption in drug design and personalized patient care across the country. Key players, including NVIDIA and regional biotech companies, are standardizing the use of AI to analyze vast biological datasets, marking a comprehensive shift towards intelligent biotechnology workflows.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | NVIDIA, Alphabet DeepMind, Microsoft, AWS | AI infrastructure, cloud computing, foundation models, accelerated computing |

| AI Biotech Platform Providers | Recursion Pharmaceuticals, Insilico Medicine, Schrödinger, Generate:Biomedicines, Xaira Therapeutics | AI-driven drug discovery and biological modeling platforms |

| Product Manufacturers | Amgen, Pfizer, Eli Lilly, Merck, Bristol Myers Squibb | Commercialization of AI-enabled therapeutics |

| Service Providers | Benchling, Tempus AI, Owkin | AI software, data platforms, analytics, biomarker solutions |

| CROs | Charles River Laboratories, Labcorp Drug Development, IQVIA | AI-assisted research and clinical development services |

| CDMOs | Lonza, Catalent, Thermo Fisher Scientific | Manufacturing support for AI-developed biologics |

| Software Vendors | Benchling, Schrödinger, Tempus AI, BioAge Labs | Research informatics and computational biology software |

| Research Institutions | Broad Institute, MIT, Stanford University, Harvard Medical School | Foundational AI and biotechnology research |

| End-User Industries | Biotechnology, Pharmaceuticals, Genomics, Precision Medicine, Synthetic Biology | Commercial deployment of AI-enabled biotech solutions |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 62% | 25% | 13% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Recursion Pharmaceuticals | Salt Lake City, Utah | USA | Leading AI-native biotech platform with large-scale biological datasets and multiple clinical programs | Recursion OS, AI drug discovery platform |

| Schrödinger | New York, New York | USA | Industry-leading computational chemistry and AI-enabled molecular design platform used by major pharma companies | Schrödinger Suite, FEP+, AI-assisted drug design |

| Tempus AI | Chicago, Illinois | USA | Major AI-driven precision medicine and clinical data company | Tempus Platform, genomic AI analytics |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Xaira Therapeutics | Brisbane, California | USA | Emerging large-scale AI biology platform backed by leading investors | Foundation models for biology |

| Benchling | San Francisco, California | USA | Dominant cloud R&D platform used across biotech industry | Scientific data cloud and AI workflows |

| Owkin | New York, New York | USA | AI-driven biomarker discovery and clinical research platform | Federated learning and biomedical AI |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Iambic Therapeutics | San Diego, California | USA | Fast-growing AI drug discovery company with major pharma collaborations | NeuralPLexer, AI drug design |

| Terray Therapeutics | Monrovia, California | USA | Combines AI and experimental chemistry for drug discovery | AI-enabled small molecule discovery |

| Chai Discovery | San Francisco, California | USA | Foundation-model-based molecular discovery platform | Generative biology AI models |

Strengths

Weaknesses

Opportunities

Threats

By Primary Application/Use Case

By Core AI Technology

By Commercial Model

By End User/Buyer Type

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar