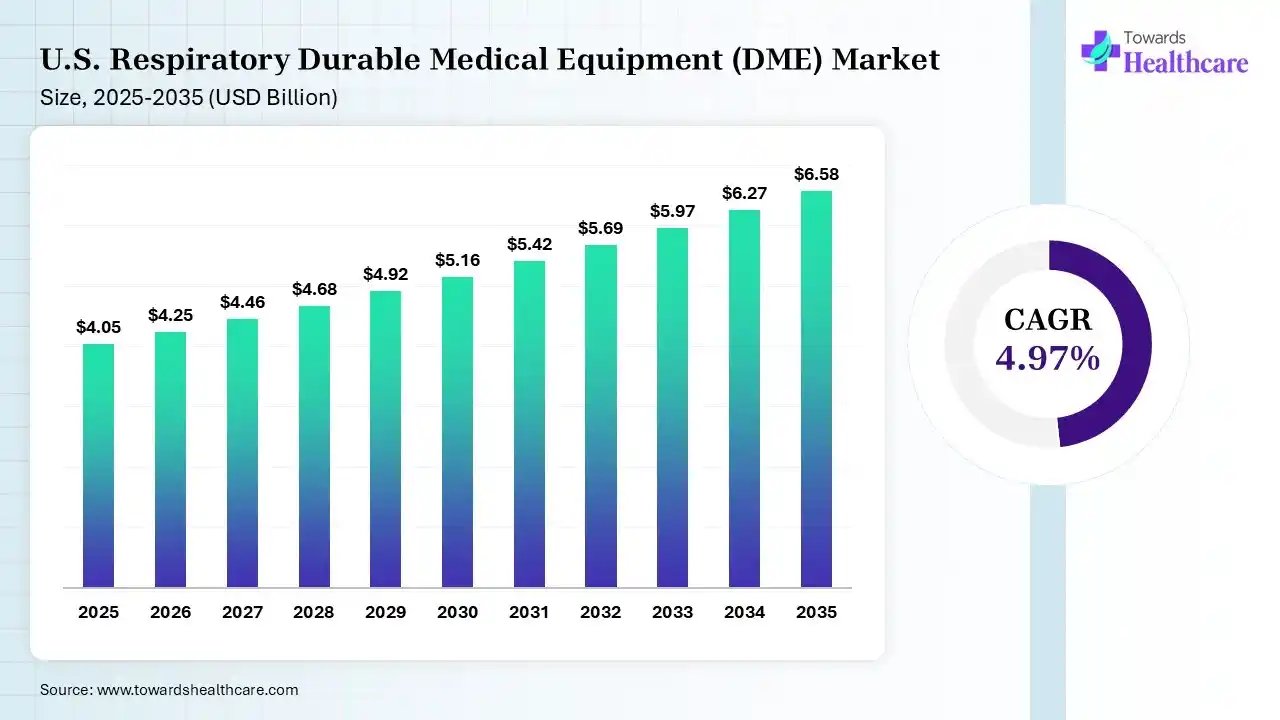

The U.S. respiratory durable medical equipment (DME) market size was estimated at USD 4.05 billion in 2025 and is predicted to increase from USD 4.25 billion in 2026 to approximately USD 6.58 billion by 2035, expanding at a CAGR of 4.97% from 2026 to 2035.

Market Size 2025 - 2035 (USD Billion)")

The market is expanding steadily, supported by growing cases of chronic respiratory conditions, an aging population, and rising preference for home-based care, with increasing use of devices such as oxygen therapy systems and sleep apnea equipment.

U.S. respiratory durable medical equipment (DME) refers to reusable medical devices used for long-term respiratory care, such as oxygen concentrators, ventilators, and CPAP machines, primarily designed for home or clinical use to manage chronic breathing conditions. The U.S. respiratory durable medical equipment (DME) market is growing due to the increasing prevalence of chronic respiratory diseases like COPD and sleep apnea, along with a rapidly aging population. Rising demand for home healthcare, supported by cost-effective treatment options, is boosting device adoption. Technological advancements in portable and user-friendly equipment, along with favorable reimbursement policies and heightened awareness after respiratory outbreaks, are further accelerating market expansion.

| Diseases | Cases | Dealths |

| COPD | 11,100,000 | 145,357 |

| Asthma | 26,800,000 | 3,517 |

| Chronic Lower Respiratory Diseases (Total) | 16,000,000 | 145,357 |

AI is transforming the market by enabling intelligent devices that support real-time monitoring, early detection of respiratory issues, and personalized treatment plans. These smart systems improve patient adherence and reduce emergency hospital visits. Additionally, AI enhances predictive maintenance, and provider integration with telehealth platforms further strengthens remote care delivery, making respiratory management more proactive, data-driven, and cost-efficient across healthcare settings.

Rising Preference for Home-Based Care

More patients are managing respiratory conditions at home due to convenience and lower treatment costs. This is increasing demand for compact, easy-to-use devices that support long-term therapy outside hospital settings while maintaining effective care.

Growth of Smart and Connected Devices

Manufacturers are focusing on devices with digital features like remote monitoring and data tracking. These tools help doctors adjust treatments faster, improve patient compliance, and enable more personalized and efficient respiratory care.

Continue Product Innovation

Ongoing advancements are leading to lighter, quieter, and more efficient equipment. Improved device design and performance are enhancing patient comfort, expanding usage across age groups, and supporting better management of chronic respiratory diseases.

| Table | Scope |

| Market Size in 2026 | USD 4.25 Billion |

| Projected Market Size in 2035 | USD 6.58 Billion |

| CAGR (2026 - 2035) | 4.97% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Distribution & Service Channel |

| Top Key Players | Arjo AB, Baxter International Inc., Becton, Dickinson and Co., Cardinal Health Inc., Compass Health Brands, GF Healthcare Technologies, GF Health Products, Inc. |

Market Segmentation")

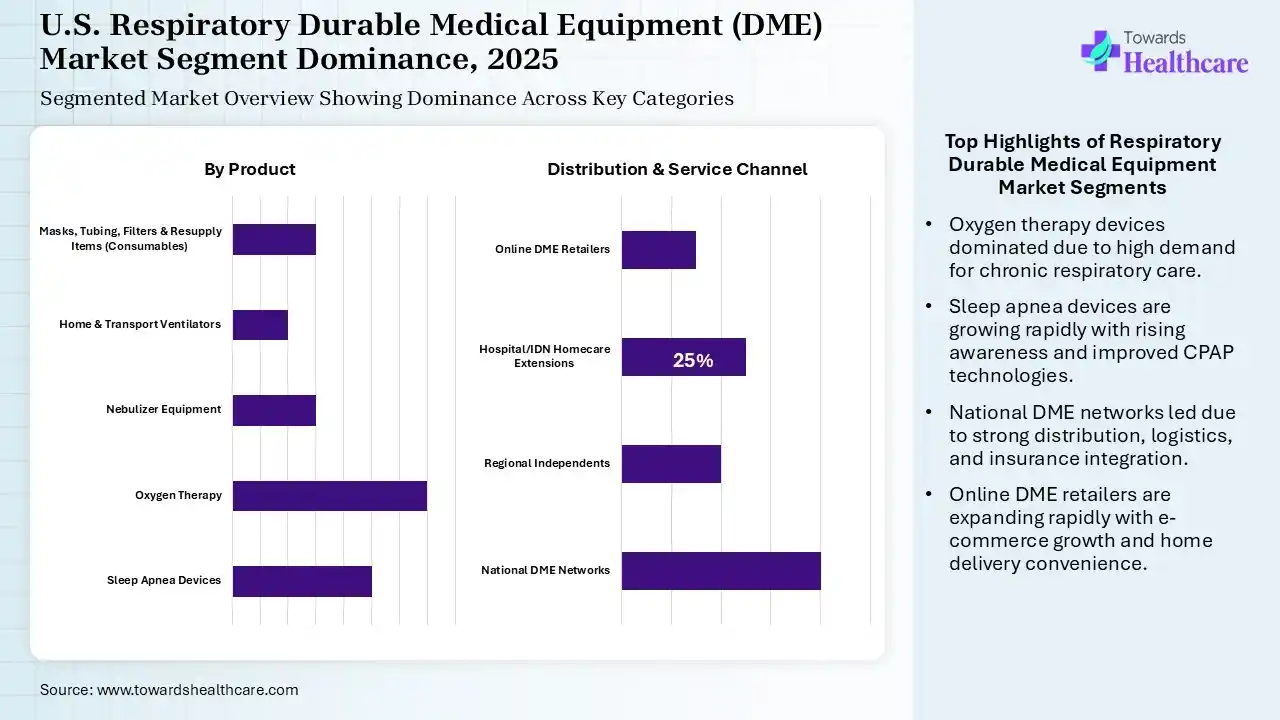

Why Did the Oxygen Therapy Devices Segment Dominate in the Market in 2025?

The oxygen therapy devices segment dominated the U.S. respiratory durable medical equipment (DME) market by 25% in 2025 due to the high prevalence of chronic respiratory diseases such as COPD and asthma requiring continuous oxygen support. These devices are widely used in both clinical and home settings, making them essential for long-term care. Increasing preference for portable oxygen concentrators, along with improved accessibility and ease of use, has further strengthened their adoption, contributing significantly to segment leadership.

Sleep Apnea Devices

The sleep apnea devices segment is expected to grow at the fastest CAGR due to rising diagnosis rates of sleep disorders and increasing awareness about the risks of untreated sleep apnea. Growing obesity levels and lifestyle-related conditions are further driving demand. Additionally, advancements in CPAP and BIPAP devices, including quieter and more comfortable designs, are improving patient compliance. Expanding home-based sleep testing and treatment options are also accelerating segment growth.

| Segment | Share 2025 (%) |

| National DME Networks | 40% |

| Regional Independents | 20% |

| Hospital/IDN Homecare Extensions | 25% |

| Online DME Retailers | 15% |

What Made the National DME Networks Segment Dominant in the Market in 2025?

The national DME networks segment dominated the U.S. respiratory durable medical equipment (DME) market by 40% in 2025 due to its extensive distribution reach, standardized service quality, and strong relationships with healthcare providers and insurance. These networks ensure timely product availability, efficient logistics, and consistent patient support across regions. Their ability to handle large patient volumes, streamline reimbursement processes, and offer integrated care solutions has made them a preferred choice, strengthening their leading position in the market.

Online DME Retailers

The online DME retailers segment is expected to grow at the fastest CAGR due to increasing digital adoption and preference for convenient purchasing options. Patients benefit from easy product comparison, home delivery, and competitive pricing. Expanding e-commerce platforms and direct-to-consumer models are improving accessibility to respiratory devices. Additionally, growing awareness, improved online support services, and integration with telehealth are further accelerating the shift towards online purchasing channels.

The U.S. respiratory durable medical equipment (DME) market is experiencing robust growth driven by an aging population, rising chronic respiratory conditions, and a surge in home-based care. Technological advancements in portable oxygen concentrators, CPAP, and ventilators are boosting adoption across all regions. The shift toward patient-friendly, lightweight, and connected devices is accelerating market expansion. Key regional variations exist due to demographic trends, healthcare infrastructure, and specific regional health challenges.

The South is currently experiencing intense demand for respiratory DME, largely due to high prevalence rates of chronic obstructive pulmonary disease and smoking-related illnesses. A significant geriatric population in states like Florida and Texas is driving the need for home oxygen and ventilators. Enhanced healthcare infrastructure, coupled with comprehensive Medicare coverage for respiratory therapies, is expanding access, enabling patients to effectively manage chronic issues in home settings.

The Northeast is characterized by a strong, concentrated healthcare system, fostering rapid adoption of advanced respiratory technologies. High population density, coupled with an older demographic in areas like Pennsylvania and New York, fuels the demand for sophisticated home ventilators and CPAP equipment. The region is a key adopter of smart, connected, and Internet of Things (IoT) integrated respiratory devices that improve patient monitoring and caregiver efficiency.

In the Midwest, growth is driven by a focus on comprehensive home-based care and the increasing prevalence of respiratory ailments. Local initiatives emphasizing chronic disease management are accelerating the adoption of home oxygen concentrators and nebulizers. The U.S. respiratory durable medical equipment (DME) market is supported by established healthcare networks expanding home care services, thus reducing hospital readmissions. This regional growth is further supported by proactive Medicare Part B coverage for essential respiratory devices.

The Western U.S. shows dynamic growth, particularly in the adoption of portable, lightweight oxygen devices and advanced sleep therapy products. The high prevalence of active lifestyles, even among seniors, creates demand for compact, efficient respiratory equipment that facilitates mobility. Furthermore, the region's strong focus on telemedicine integration allows for better management of COPD and sleep apnea, driving the demand for specialized, high-tech respiratory equipment.

R&D

Regulatory Approvals

Patient Support and Services

Market Top Companies")

| Companies | Headquarters | Offerings |

| Arjo AB | Sweden | Patient mobility solutions, hospital beds, hygiene systems, and therapeutic support surfaces are used in long-term and home care settings. |

| Baxter International Inc. | USA | Infusion systems, renal care products, and critical care equipment supporting chronic disease management. |

| Becton, Dickinson and Co. | New Jersey, USA | Medical supplies, diagnostic devices, and patient monitoring tools are used alongside DME in home and clinical care. |

| Cardinal Health Inc. | Ohio, USA | Distribution of medical supplies, respiratory equipment, and home healthcare products across DME networks. |

| Compass Health Brands | Ohio, USA | Mobility aids, respiratory products, bathroom safety equipment, and home care solutions. |

| DRIVE MEDICAL GMBH and CO. KG | Germany | Wheelchairs, oxygen therapy equipment, beds, and daily aids for homecare patients. |

| GF Healthcare Technologies | Illinois, USA | Imaging systems, monitoring devices, and digital health solutions supporting respiratory and critical care. |

| GF Health Products, Inc. | Georgia, USA | Patient beds, respiratory equipment, mobility products, and rehabilitation aids for home and institutional use. |

Strengths

Weaknesses

Opportunities

Threats

By Product

By Distribution & Service Channel

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar