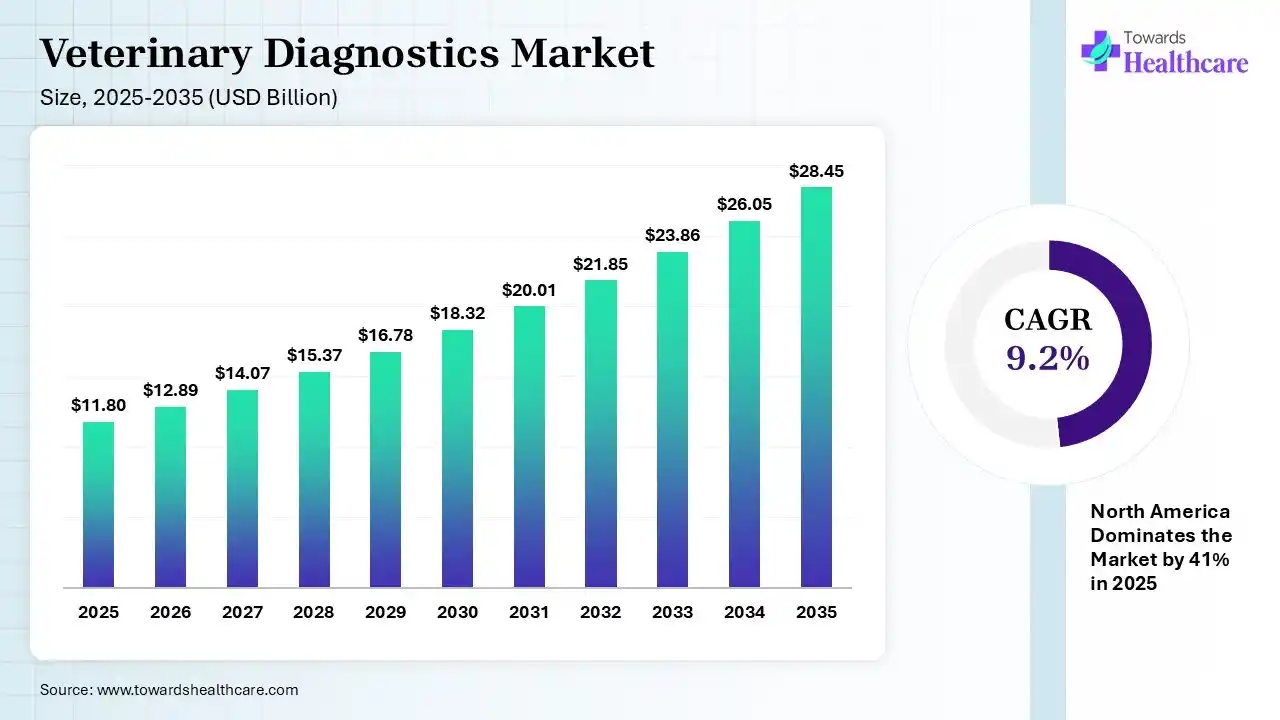

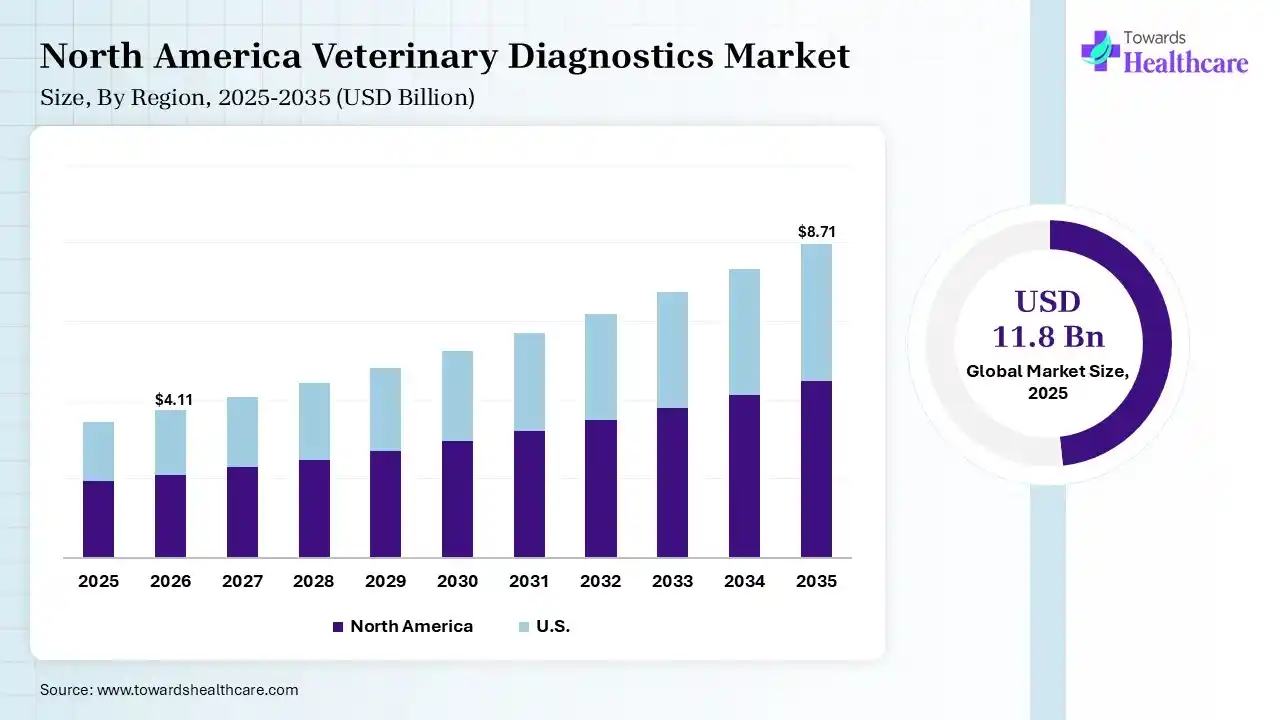

The global veterinary diagnostics market size was estimated at USD 11.8 billion in 2025 and is predicted to increase from USD 12.89 billion in 2026 to approximately USD 28.45 billion by 2035, expanding at a CAGR of 9.2% from 2026 to 2035. The market is growing steadily due to rising pet ownership, increasing incidence of animal diseases, and greater focus on early and accurate disease detection in animals. Advancements in rapid testing, molecular diagnostics, and point-of-care technologies are further driving adoption across veterinary healthcare systems globally.

")

Veterinary diagnostics refers to the use of laboratory tests and diagnostic tools to detect, monitor, and prevent diseases in animals. It helps in identifying health conditions in livestock and pets for timely and effective treatment. The veterinary diagnostics market is growing due to rising pet ownership, increasing awareness of animal health, and the need for early disease detection in livestock and companion animals. Growing outbreaks of zoonotic and infectious diseases are boosting demand for advanced testing. In addition, technological advancements such as rapid point-of-care tests, molecular diagnostics, and digital veterinary solutions are improving the accuracy, speed, and accessibility of animal healthcare services globally.

Veterinary diagnostic refers to the use of laboratory tests, imaging technologies, and molecular diagnostics tools to detect, monitoir, and manage diseases in companion tool to detect, monitoring and manage disease in companion and livestock animals. The veterinary diagnostic market is expanding due to the increasing prevalence of zoonotic and infectious diseases, growing pet ownership, rising livestock health management needs, and greater awareness of preventive animal healthcare. Technological advancements, including AI-powered diagnostic platforms, molecular diagnostics, point-of-care testing, digital imaging and automated laboratory systems, are improving diagnostic speed and accuracy. A key market trend is the increasing adoption of rapid, portable diagnostic solutions in veterinary clinics and field settings. Future opportunities lie in precision veterinary medicine, genomic testing, connected diagnostics platforms, and remote animal health monitoring. Continued investment in animal welfare, food safety, and advanced veterinary infrastructure is further accelerating innovation and long-term market growth.

AI is transforming the market by enabling faster and more accurate disease detection through image analysis, predictive analytics, and automated laboratory workflows. It supports early diagnosis, improves treatment decisions, and enhances operational efficiency in veterinary clinics and diagnostic labs. The integration of AI-powered tools is also driving innovation in point-of-care testing and remote animal health monitoring.

Rising Demand for Rapid Testing

The market is moving toward faster diagnostic solutions that provide quick and accurate results. This trend supports timely treatment decisions and is expected to increase adoption across veterinary clinics, hospitals, and livestock care settings.

Integration of AI and Advanced Technologies

The use of AI, digital imaging, and automated diagnostic systems is improving diagnostic precision and efficiency. These technologies are expected to play a major role in shaping the future growth of the veterinary diagnostics market.

Growing Focus on Preventive Animal Healthcare

Increasing awareness regarding routine health screening and early disease detection is driving market demand. Rising pet ownership and greater attention to livestock health are expected to support long-term market expansion.

| Table | Scope |

| Market Size in 2026 | USD 12.89 Billion |

| Projected Market Size in 2035 | USD 28.45 Billion |

| CAGR (2026 - 2035) | 9.2% |

| Leading Region | North America by 41% |

| Key Applications | Infectious disease testing, clinical pathology, oncology diagnostics, genetic testing, endocrinology, preventive screening |

| Primary End Users | Veterinary hospitals, veterinary clinics, diagnostic laboratories, research institutes, universities, livestock producers |

| Key Growth Drivers | Rising pet ownership, zoonotic disease surveillance, molecular diagnostics adoption, AI-enabled diagnostics, livestock health management |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Technology, By Animal Type, By Application, By End User, By Region |

| Top Key Players | IDEXX Laboratories, Inc., Zoetis, Antech Diagnostics, Inc. (Mars Inc.), Agrolabo S.p.A., Embark Veterinary, Inc., Esaote SPA |

")

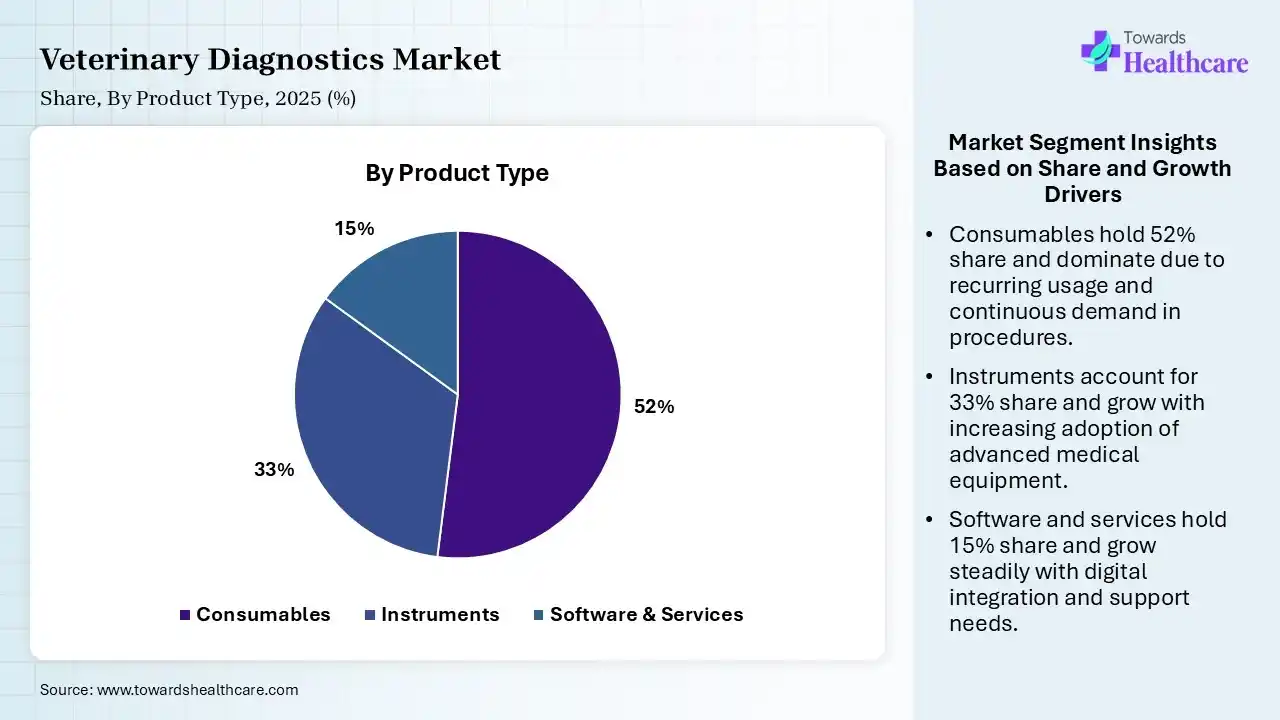

| Segment | Share 2025 (%) |

| Consumables | 52% |

| Instruments | 33% |

| Software & Services | 15% |

The Consumables Segment Dominated the Market in 2025

The consumables segment dominated the veterinary diagnostics market with a share of 52% in 2025 due to the high recurring demand for test kits, reagents, assay cartridges, and sample collection supplies used in routine diagnostic procedures. Their frequent replacements, widespread use in disease screening, and growing volumes of animal testing across and laboratory significantly supported segment leadership.

The instruments segment held the second-largest share of 33% of the market in 2025 due to rising adoption of analysis, imaging systems, PCR devices, and automated laboratory equipment. These tools are essential for accurate and high-volume testing in clinics and diagnostic labs. Growing investment in advanced veterinary infrastructure and technological upgrades continues to strengthen the segment’s market position and future growth.

The software & services segment held 15% share in 2025 and is expected to grow at the fastest CAGR of 10.80% in the veterinary diagnostics market during the forecast period due to increasing adoption of digital diagnostic platforms, data management systems, AI-based analytics, and cloud-enabled veterinary solutions. Growing demand for workflow automation, remote monitoring, and efficient record management in veterinary clinics and laboratories is accelerating segment growth and supporting long-term market expansion.

")

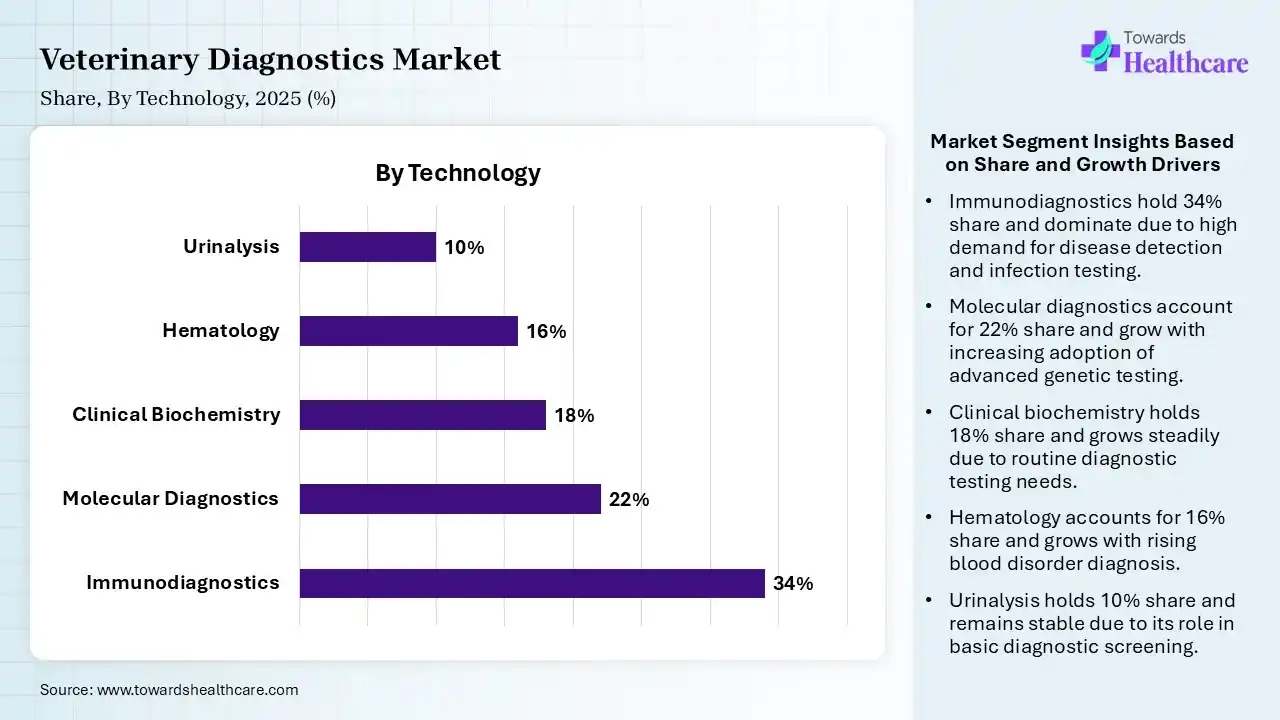

| Segment | Share 2025 (%) |

| Immunodiagnostics | 34% |

| Molecular Diagnostics | 22% |

| Clinical Biochemistry | 18% |

| Hematology | 16% |

| Urinalysis | 10% |

The Immunodiagnostics Segment Led the Market in 2025 with the Largest Share

The immunodiagnostics segment led the veterinary diagnostics market with a share of 34% in 2025 due to its widespread use in detecting infectious diseases, hormonal disorders, and immune-related conditions in animals. These tests offer high accuracy, rapid results, and cost-effective screening, making them highly preferred across veterinary clinics and laboratories. Rising demand for early disease detection and routine animal health screening further strengthened the segment’s dominant market share.

The molecular diagnostics segment held the second-largest share of 22% of the market in 2025 and is expected to grow at the fastest CAGR of 11.20% in the market during the forecast period due to its high sensitivity and precision in detecting infectious, genetic, and zoonotic diseases in animals. Technologies such as PCR and DNA-based testing enable early and accurate diagnosis, supporting effective treatment decisions. Increasing focus on advanced disease surveillance, outbreak control, and personalized veterinary care continues to drive strong demand for this segment.

The clinical biochemistry segment held 18% of the veterinary diagnostics market share in 2025 due to increasing demand for routine blood chemistry testing to assess organ function, metabolic disorders, and overall animal health. These tests are widely used in veterinary clinics for diagnosing liver, kidney, and endocrine conditions. Rising pet healthcare spending, growing awareness of preventive diagnostics, and the need for regular health monitoring in companion and livestock animals are driving segment growth.

The hematology segment held 16% of the veterinary diagnostics market share in 2025 due to the rising use of blood-based tests for diagnosing infections, anemia, inflammation, and blood-related disorders in animals. Veterinary clinics increasingly rely on hematology analyzers for rapid and accurate complete blood count testing. Growing emphasis on routine wellness screening, early disease detection, and improved diagnostic capabilities in companion and livestock healthcare is driving strong segment growth.

")

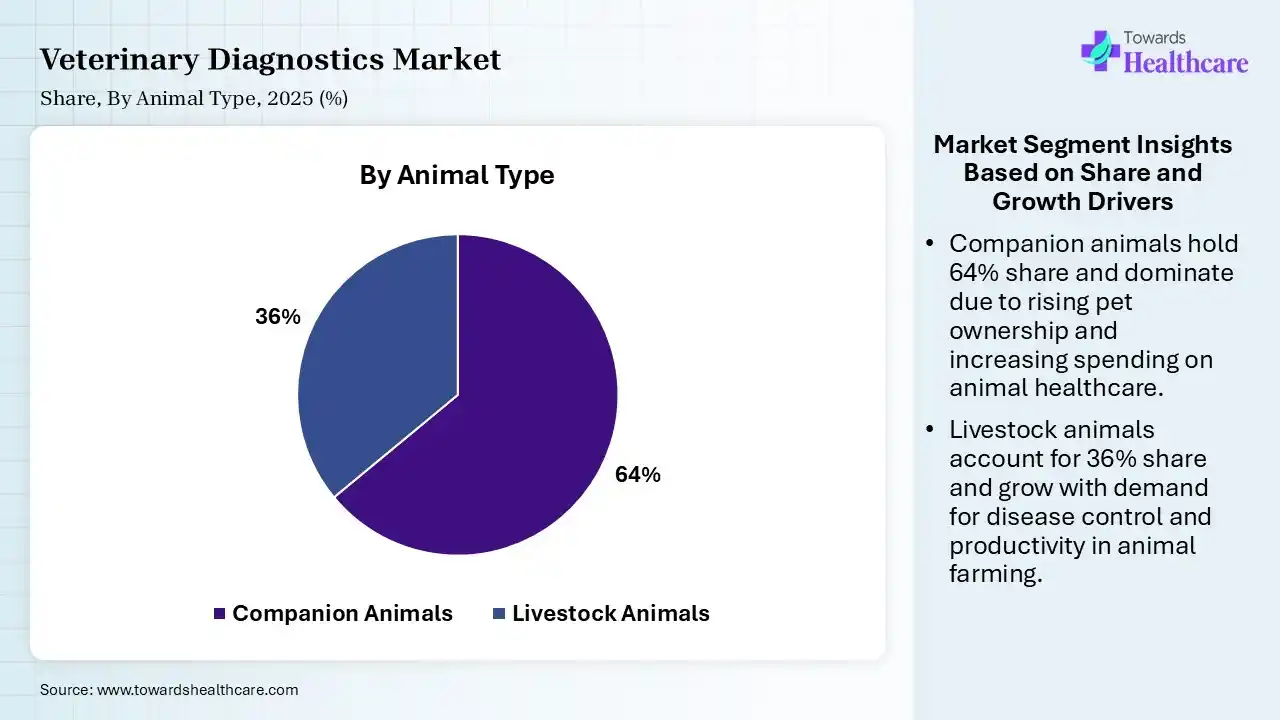

| Segment | Share 2025 (%) |

| Companion Animals | 64% |

| Livestock Animals | 36% |

The Companion Animals Segment Led the Market in 2025 with the Largest Share

The companion animals segment held a dominant share of 64% in veterinary diagnostics in 2025 and is expected to grow at the fastest CAGR of 9.60% in the market during the forecast period due to rising pet ownership, increasing spending on pet healthcare, and growing awareness of preventive diagnostics among pet owners. Dogs, cats, and other companion animals undergo frequent health screenings, vaccinations, and disease testing, driving high demand for diagnostic services. The trend of pet humanization and access to advanced veterinary care further strengthened the segment’s leading market share.

The livestock animals segment held the second-largest share of 36% of the market in 2025 due to the growing need for disease surveillance, herd health management, and productivity monitoring in cattle, poultry, swine, and other farm animals. Rising concerns over zoonotic diseases, food safety, and economic losses from infections are driving demand for regular diagnostic testing, supporting strong adoption across commercial farming and animal healthcare operations.

")

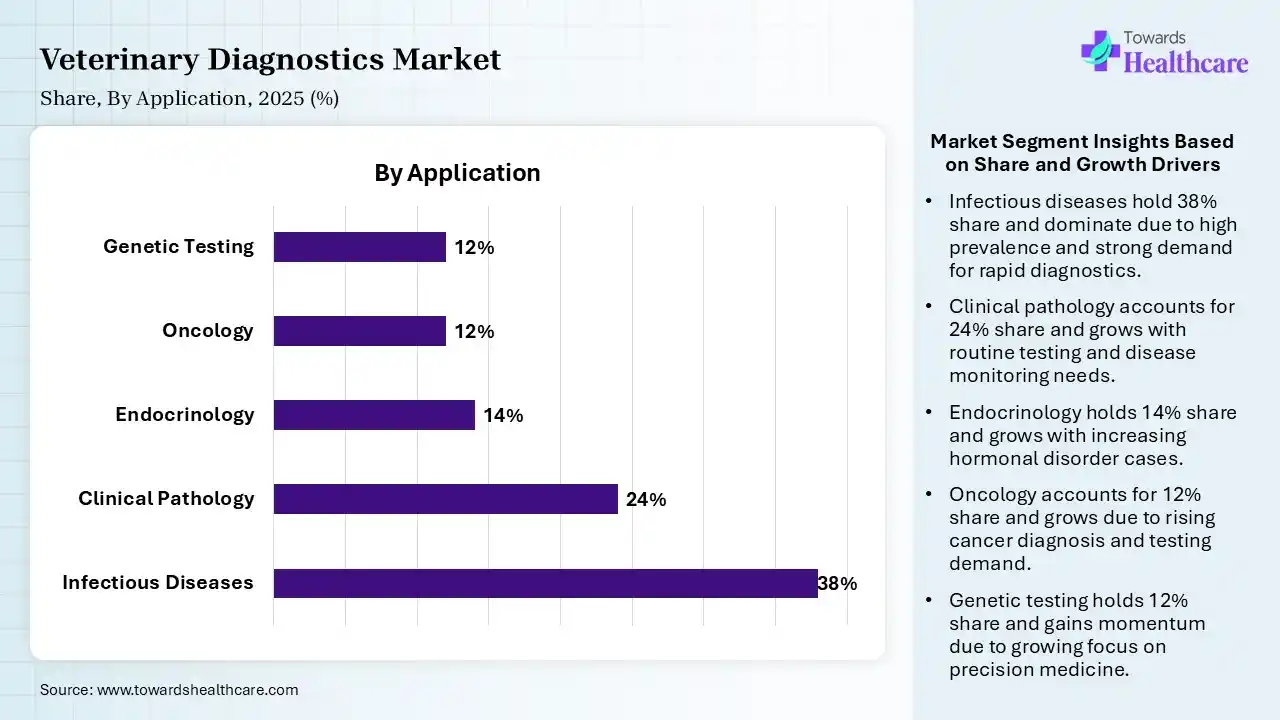

| Segment | Share 2025 (%) |

| Infectious Diseases | 38% |

| Clinical Pathology | 24% |

| Endocrinology | 14% |

| Oncology | 12% |

| Genetic Testing | 12% |

The Infectious Diseases Segment held a Dominant Position in the Market in 2025

The infectious diseases segment led the veterinary diagnostics market with a share of 38% in 2025 due to the high prevalence of bacterial, viral, and parasitic infections in both companion and livestock animals. Early and accurate diagnosis is essential to prevent disease spread, reduce mortality, and ensure effective treatment. Rising concerns over zoonotic disease transmission and increasing focus on preventive animal healthcare continue to drive strong demand for this segment.

The clinical pathology segment held the second-largest share of 24% of the market in 2025 and is expected to grow at the fastest CAGR of 8.80% in the market during the forecast period due to its essential role in routine animal health assessment and disease diagnosis. Tests such as blood counts, urine analysis, and tissue examinations are widely used to detect metabolic, organ-related, and systemic disorders. Increasing demand for preventive screenings, regular wellness checkups, and accurate treatment monitoring in veterinary practice continues to support strong segment growth.

The endocrinology segment held 14% of the veterinary diagnostics market share in 2025 due to the increasing prevalence of hormonal and metabolic disorders such as diabetes, thyroid dysfunction, and adrenal diseases in companion animals. Rising pet ownership, greater awareness of chronic disease management, and the need for regular hormone testing are driving demand. Improved diagnostic capabilities and routine wellness screening in veterinary practice are further supporting the steady growth of this segment.

The oncology segment held 12% share in 2025 and is expected to grow at the fastest CAGR of 10.70% in the market during the forecast period due to the rising incidence of cancer in companion animals, particularly dogs and cats. Increasing awareness of early cancer detection, growing use of advanced imaging and biopsy diagnostics, and higher spending on specialized veterinary care are driving demand. Advancements in precision diagnostics and treatment planning are further accelerating segment growth.

")

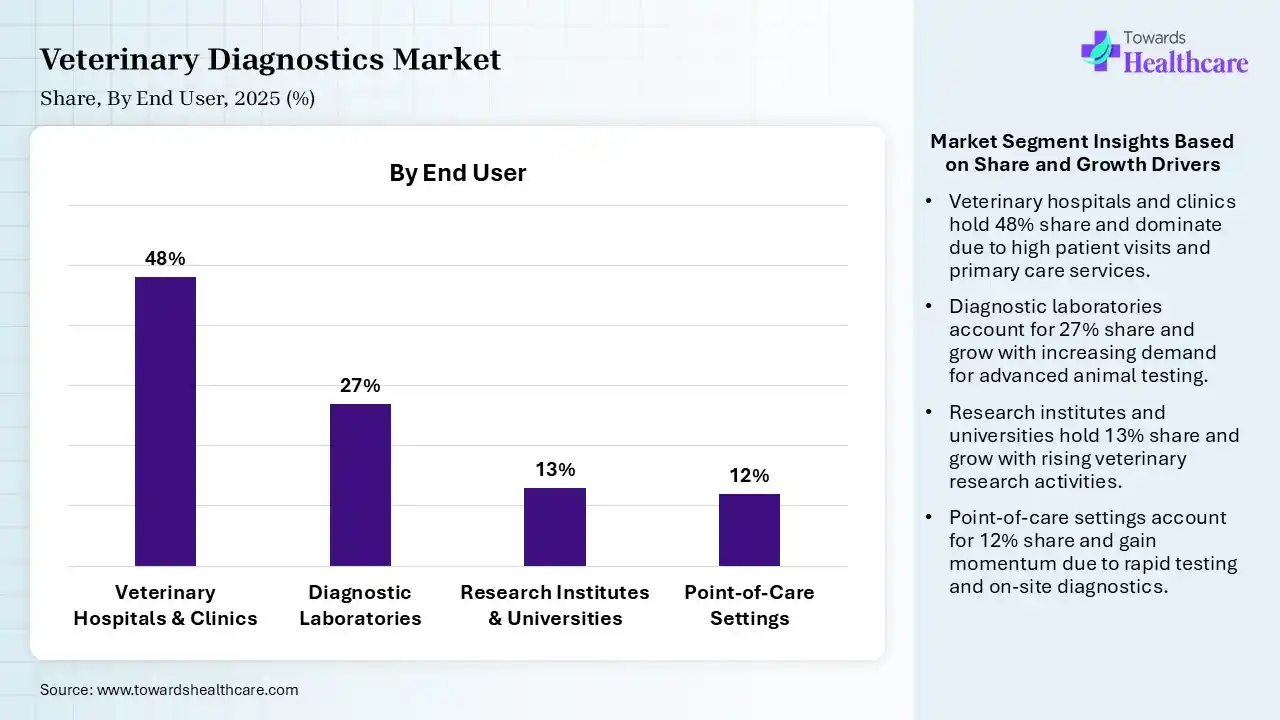

| Segment | Share 2025 (%) |

| Veterinary Hospitals & Clinics | 48% |

| Diagnostic Laboratories | 27% |

| Research Institutes & Universities | 13% |

| Point-of-Care Settings | 12% |

The Veterinary Hospitals & Clinics Segment Dominated the Market in 2025

The veterinary hospitals & clinics segment held a dominant share of 48% in 2025 due to the high volume of animal visits for routine checkups, disease diagnosis, treatment, and emergency care. These facilities are equipped with advanced diagnostic instruments and skilled professionals, enabling rapid and accurate testing. Rising pet healthcare spending, growing awareness of preventive care, and increasing demand for specialized veterinary services further strengthened the segment’s leading market share.

The diagnostics laboratories segment held the second-largest share of 27% of the veterinary diagnostics market in 2025 due to the high volume of clinical visits for routine checkups, high-volume, and accurate testing services for veterinary hospitals and clinics. These laboratories support advanced diagnostics such as molecular testing, pathology, and biochemistry analysis. Increasing demand for precise disease detection, centralized testing facilities, and faster turnaround of complex test results continues to drive strong segment growth.

The research institutes & universities segment held 13% of the veterinary diagnostics market share in 2025 due to increased investment in veterinary disease research, animal health studies, and the development of advanced diagnostic technologies. These instruments play a key role in epidemiological surveillance, collaborations with pharmaceutical and biotechnology companies, along with a growing focus on zoonotic disease prevention, are further supporting steady segment growth.

The point-of-care settings segment held 12% share in 2025 and is expected to grow at the fastest CAGR of 10.50% in the market during the forecast period due to increasing demand for rapid, on-site diagnostic testing and immediate clinical decision-making. Portable diagnostic devices offer faster results, improved convenience, and reduced dependency on centralized laboratories. Rising adoption in veterinary clinics, emergency care, and field settings is further accelerating growth and expanding access to timely animal healthcare services.

")

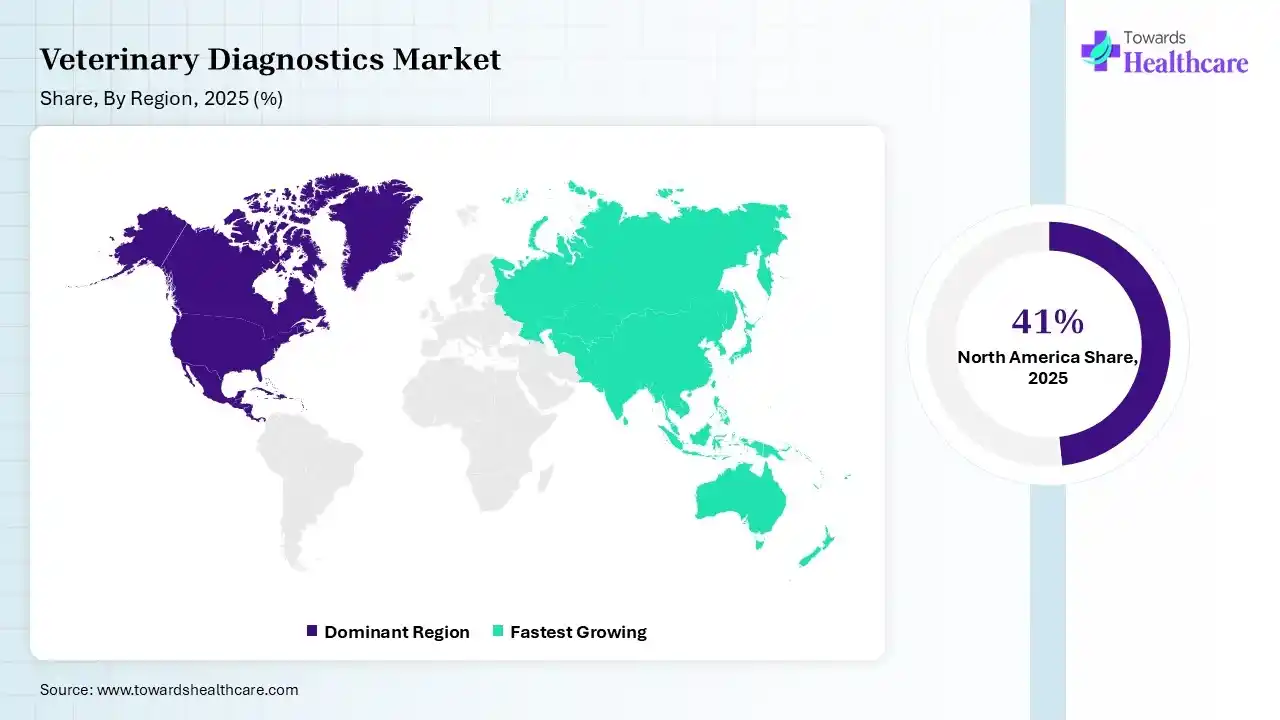

North America dominated the veterinary diagnostics market with a share of 41% in 2025 due to high pet ownership, advanced veterinary healthcare infrastructure, and strong spending on animal health services. The region benefits from early adoption of advanced diagnostic technologies, growing awareness of preventive pet care, and a well-established network of veterinary hospitals and laboratories. The rising prevalence of animal diseases and the strong presence of key market players further support regional growth.

U.S. Market Trends

The U.S. veterinary diagnostics market is growing due to rising pet adoption, increasing expenditure in companion animal healthcare, and strong demand for early disease detection. Advanced veterinary infrastructure, widespread use of molecular and point-of-care diagnostics, and growing awareness of preventive care are driving market expansion. Additionally, increasing cases of chronic and infectious diseases in animals continue to support sustained growth.

Canada Strengthens Leadership in Advanced Veterinary Diagnostics

Canada veterinary diagnostics market is witnessing significant growth due to the increasing pet ownership, rising livestock health management, and growing awareness of early disease detection. Advanced veterinary healthcare infrastructure, widespread adoption of molecular diagnostics, point-of-care testing, and strong investments in animal health research are accelerating market expansion. Additionally, supportive government initiatives for animal welfare and food safety continue to drive information and demand for advanced veterinary diagnostic solutions.

Asia Pacific held 20% of the total market share and is anticipated to grow at the fastest CAGR of 11% in the veterinary diagnostics market due to rising pet ownership, expanding livestock populations, and increasing awareness of animal health. Rapid improvements in veterinary infrastructure, growing disposable income, and higher demand for preventive diagnostics are driving growth. Additionally, increasing focus on zoonotic disease control and expanding access to veterinary services further support regional expansion.

India Market Trends

India is expected to grow at the fastest CAGR in the veterinary diagnostics market during the forecast period due to increasing investment in animal healthcare, rising incidence of infectious diseases in livestock, and growing adoption of advanced diagnostic technologies. Rapid urbanization, improving access to veterinary services, and strong demand for better disease monitoring in the dairy and poultry sectors are further contributing to robust market expansion.

China Accelerates Veterinary Diagnostics Through Rapid Innovation

China veterinary diagnostics market is growing significantly due to the expanding companion animal population and rising prevalence of infectious animal diseases. Strong investments in veterinary healthcare infrastructure, rapid adoption of molecular diagnostics and point-of-care testing, and continued advancements in domestic diagnostic technologies are fueling market growth. Additionally, government initiatives focused on animal disease surveillance and food safety are strengthening demand for advanced veterinary diagnostic solutions.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | IDEXX Laboratories, Zoetis, Thermo Fisher Scientific, Virbac | Develop diagnostic technologies, analyzers, testing platforms |

| Product Manufacturers | IDEXX Laboratories, Zoetis, Heska, Neogen, Randox | Produce diagnostic instruments, kits, reagents, consumables |

| Service Providers | Antech Diagnostics, IDEXX Reference Laboratories, VPG | Laboratory testing and diagnostic services |

| Platform Providers | IDEXX, Zoetis, Covetrus, Heska | Veterinary software and diagnostic workflow platforms |

| CROs/CDMOs | Charles River Laboratories, Inotiv, Labcorp Drug Development | Veterinary research and animal health testing support |

| Software Vendors | IDEXX, Covetrus, Zoetis, ezyVet | Practice management and diagnostic data platforms |

| Research Institutions | Cornell University College of Veterinary Medicine, UC Davis School of Veterinary Medicine, Royal Veterinary College | Veterinary diagnostic research and innovation |

| End-User Industries | Companion Animal Care, Livestock Farming, Veterinary Hospitals, Research Organizations | Adoption and utilization of veterinary diagnostic solutions |

R&D

Clinical Trials

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| IDEXX Laboratories | Westbrook, Maine | USA | Global market leader with extensive diagnostic portfolio and reference lab network | VetLab analyzers, SNAP tests, reference laboratory services |

| Zoetis | Parsippany, New Jersey | USA | Major animal health company with rapidly expanding diagnostics division | Vetscan analyzers, rapid diagnostics, imaging solutions |

| Antech Diagnostics | Fountain Valley, California | USA | One of the largest veterinary laboratory service providers globally | Pathology, molecular diagnostics, imaging services |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Heska Corporation | Loveland, Colorado | USA | Established veterinary diagnostics specialist | Hematology, chemistry analyzers, imaging solutions |

| Virbac | Carros | France | Strong veterinary healthcare and diagnostic portfolio | Diagnostic tests, companion animal health products |

| Randox Laboratories | Crumlin, Northern Ireland | UK | Expanding veterinary diagnostics offerings globally | Veterinary diagnostic reagents and analyzers |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Embark Veterinary | Boston, Massachusetts | USA | Leader in canine genetic diagnostics | DNA testing and hereditary disease screening |

| MiDOG Animal Diagnostics | Ann Arbor, Michigan | USA | Specialized oncology diagnostic innovator | Cancer detection and pathology diagnostics |

| VolitionRx | Henderson, Nevada | USA | Developing blood-based cancer diagnostics for animals | Nu.Q Vet cancer testing platform |

In July 2026, "With MiDOG Parasite-Only Testing, we are giving clinicians a focused way to look deeper when parasite insight is the priority. This launch reflects our continued commitment to making advanced molecular diagnostics more practical, accessible, and clinically useful for veterinary teams”, said Dr. Janina Krumbeck, PhD, CEO of MiDOG Animal Diagnostics.

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Technology

By Animal Type

By Application

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar