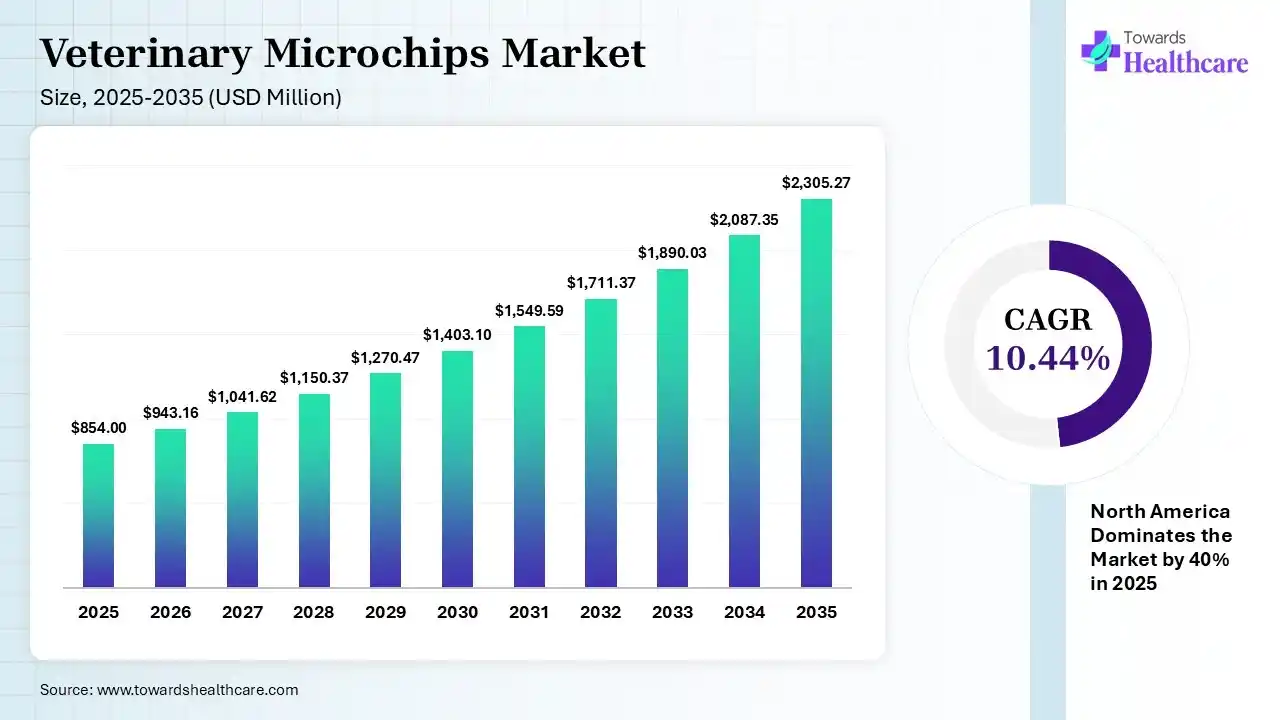

The global veterinary microchips market size was estimated at USD 854 million in 2025 and is predicted to increase from USD 943.16 million in 2026 to approximately USD 2305.27 million by 2035, expanding at a CAGR of 10.44% from 2026 to 2035.

The global development is driven by a rise in pet ownership, increasing awareness regarding pet safety, and the enforcement of mandatory government regulations. Organizations are focusing on promoting pet identification technologies, aided by GPS-RFID, and also leveraging AI algorithms.

")

Primarily, the adoption of tiny, rice-sized, passive RFID transponders that are injected under a pet’s skin to facilitate permanent, secure identification is termed the veterinary microchips market. The comprehensive market development is driven by the enforcement of compulsory microchipping for dogs and cats across several countries, with rising emphasis on pet humanization & safety. Besides this, the globe is encouraging higher pet adoption & raised veterinary care standards, which ultimately bolsters the use of microchipping.

A prominent AI role includes the analysis of data generated from implanted sensors to find clear indicators of disease, like temperature, heart rate, & respiratory changes. Moreover, smart sensors are supporting the monitoring of behaviour & crucial signs in estimating issues before symptoms lead to severe & offer tailored veterinary care. Data generated by AI can be coupled with faster & accurate veterinary imaging & diagnostics.

Rolling out Digital Data Integration & Digital ID

Nowadays, microchips are highly connected to entire cloud-based platforms that store medical records, vaccination histories, & owner contact information, which makes it easier for vets & shelters to handle patient data.

Pushing Optimized Reader/Scanner Technology

The market is increasingly executing new scanners that feature advanced technology, such as long-range reading capabilities, Bluetooth connectivity, & cloud integration, to allow for immediate lookup of pet information.

Promoting Hybrid GPS-RFID Solutions

Research activities are broadly posing standard RFID chips, along with the unification of GPS technology into miniature, implantable forms, which facilitates real-time location tracking, especially for premium pets.

| Table | Scope |

| Market Size in 2026 | USD 943.16 Million |

| Projected Market Size in 2035 | USD 2305.27 Million |

| CAGR (2026 - 2035) | 10.44% |

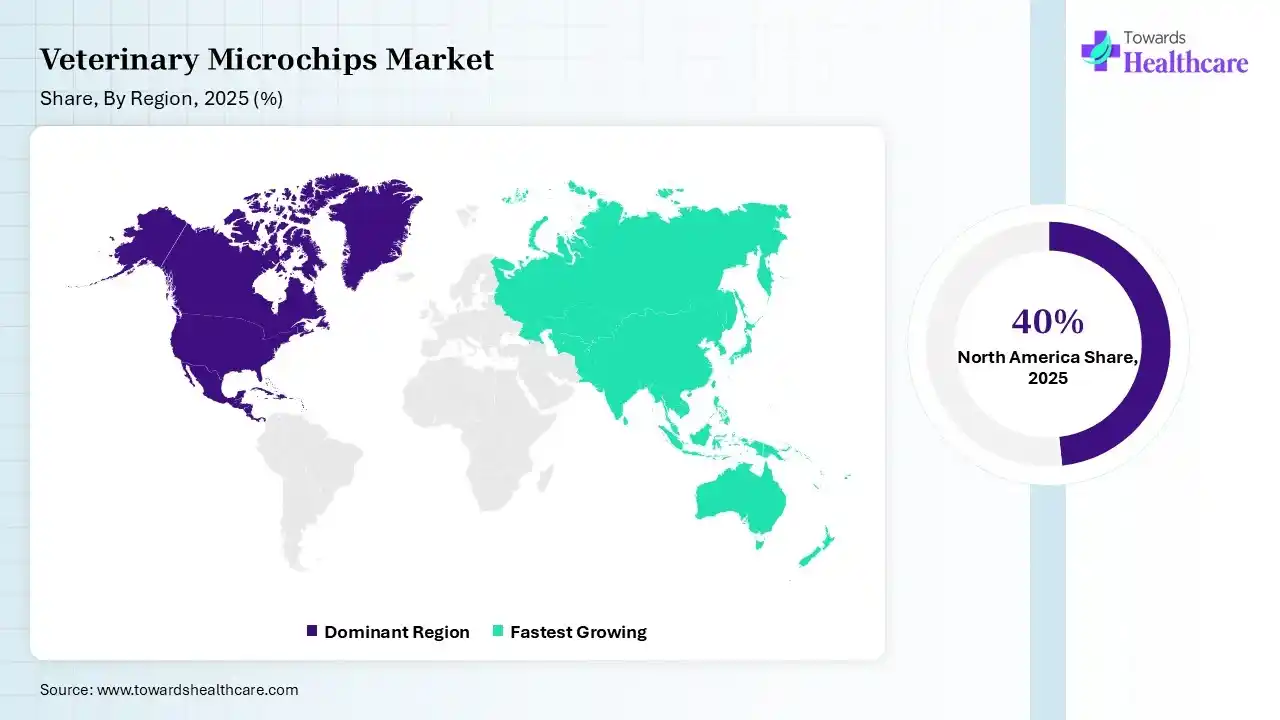

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Technology Type, By Animal Type, By End-User, By Application, By Region |

| Top Key Players | Merck & Co., Inc., Peeva Inc, Virbac, ID Tech, Dipole RFID, Trovan Ltd., Wuxi Fofia Technology Co., Ltd , Avid Identification Systems, Inc, Datamars, Pethealth Inc |

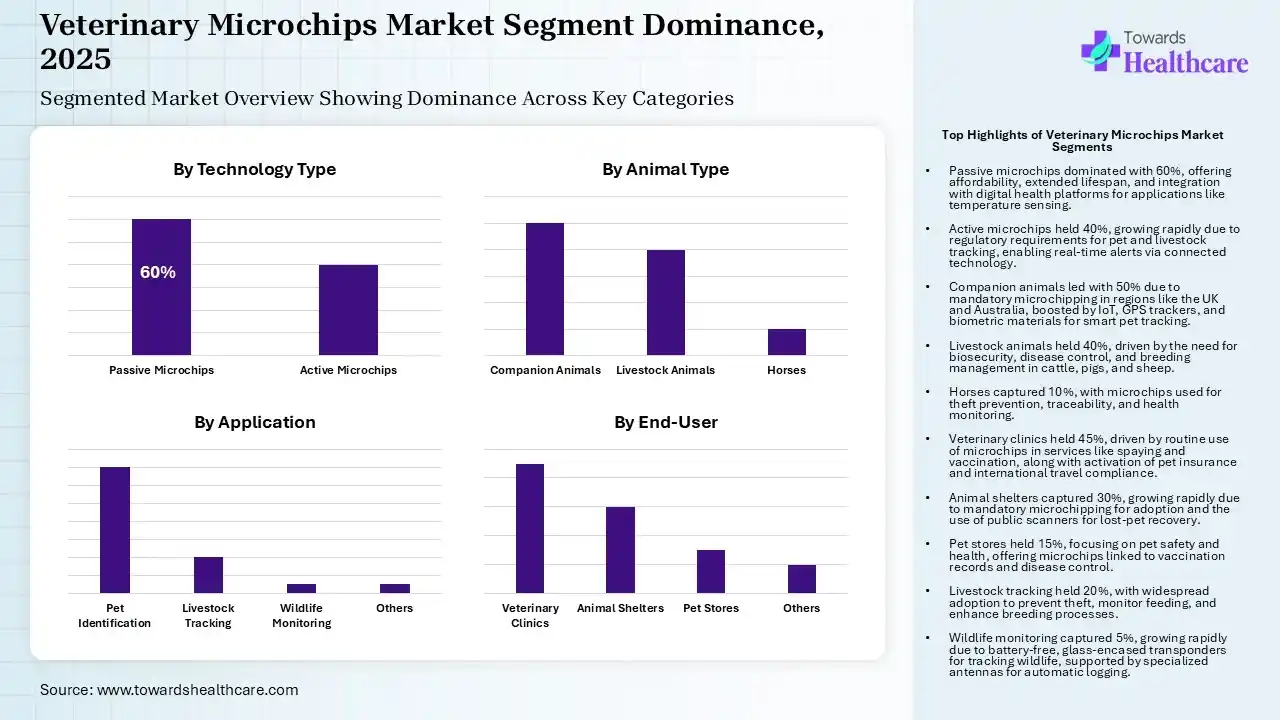

The Passive Microchips Segment Led the Market in 2025

| Segment | Share 2025 (%) |

| Passive Microchips | 60% |

| Active Microchips | 40% |

In 2025, the passive microchips segment dominated with 60% share of the veterinary microchips market, due to the affordability of passive RFID chips to develop & have an extended operational life. The latest thermochips are leveraging biosensors to record the animal’s subcutaneous temperature. Immersive innovations are fostering temperature-sensing technology, advanced polymer coatings, & integration with digital health platforms.

However, the active microchips segment captured the second-largest share of 40% of the market and is expected to grow at the fastest CAGR of 9.5% during the forecast period. This is mainly propelled by the enforcement of regulations by governments, which need microchips for pets & livestock to boost tracking & disease surveillance. These microchips can rigorously find abnormalities as they occur & further facilitate immediate alerts to pet owners, farmers, & vets through connected technology, such as mobile apps.

The Companion Animals Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Companion Animals | 50% |

| Livestock Animals | 40% |

| Horses | 10% |

The companion animals segment captured 50% largest share of the veterinary microchips market in 2025. Across several regions, like the UK & parts of Australia, are actively executing mandatory cat microchipping, which drives the need for microchips. Gradually, the market is spurring integrated IoT, GPS trackers & superior biometric materials, which surges the reliability & adoption of smart pet tracking measures.

")

The livestock animals segment held 40% of the second-largest share of the market. Key recipients are cattle, pigs, and sheep due to the growing beef production, breeding enhancement, and fostering health monitoring & handling breeding records. Emerging advances are emphasizing optimization of biosecurity, disease control, & customized farming, with exploration of miniaturization, biocompatibility, & smartphone integration, which impels microchipping.

The horses segment captured 10% revenue share of the market in 2025. The adoption of microchips is fueled by a focus on theft prevention & enhanced traceability for breeding & health monitoring. The worldwide efforts are demonstrating the application of implanted microchips to track the location of the colon & cecum in horses to robust recognition of colic, & also activities are showing increased retention & low inflammatory response.

The Veterinary Clinics Segment Was Dominant in the Market in 2025

| Segment | Share 2025 (%) |

| Veterinary Clinics | 45% |

| Animal Shelters | 30% |

| Pet Stores | 15% |

| Others | 10% |

In 2025, the veterinary clinics segment held 45% biggest share of the veterinary microchips market. Many well-developed clinics are using microchipping in routine services, like spaying, neutering, or vaccination, increasing the convenience for owners & improving clinic revenue. Numerous veterinarians are implementing verification of microchip numbers to activate pet insurance policies & for international travel, as certain countries mandate ISO-compliant chips for entry.

However, the animal shelters segment captured 30%, the second-largest share of the market in 2025, and is estimated to achieve the fastest CAGR of 6.2% during 2026-2035. Numerous shelters are serving as prominent adoption hubs where microchipping is mandatory before releasing animals to new owners, which develops continuous institutional demand. The global shelters are widely utilizing or offering access to public-accessible scanners to rapidly reunite found pets, like incentives with domestic fire departments or rescue groups.

The pet stores segment held 15% revenue share of the market, due to surging focus on pets as family members, which results in increased expenditure on preventative health & safety measures. These stores are expanding their applications by connecting the chip’s unique ID to vaccination records & health history, coupled with disease control, especially in high-density areas or for travel.

The Pet Identification Segment Led the Market in 2025

| Segment | Share 2025 (%) |

| Pet Identification | 70% |

| Livestock Tracking | 20% |

| Wildlife Monitoring | 5% |

| Others | 5% |

In 2025, the pet identification segment held the largest share of 70% of the veterinary microchips market. The segmental dominance is propelled by the inclusion of mandatory pet identification regulations, escalating pet humanization, & strengthened lost-pet recovery awareness. Most of the advanced, smart microchips are highly linked to digital platforms to store vaccination records, owner contact information, & medical histories.

The livestock tracking segment held 20% share of the market in 2025, with the emergence of mandatory government regulations. The widespread producers are employing these microchips and trackers to lower animal theft, monitor feeding, and enhance breeding, with minimal manual tagging labor.

Whereas the wildlife monitoring segment captured 5%, and is expected to grow at the fastest CAGR of 6.8% during the predicted time. This mainly explores small glass-encased transponders under the skin, which need no batteries & also facilitate a lifespan that raises the animal’s lifetime. For this kind of monitoring, organizations are executing specialized antennas at food hoppers, nest boxes, or burrows that automatically log the identity of passing or interacting animals.

")

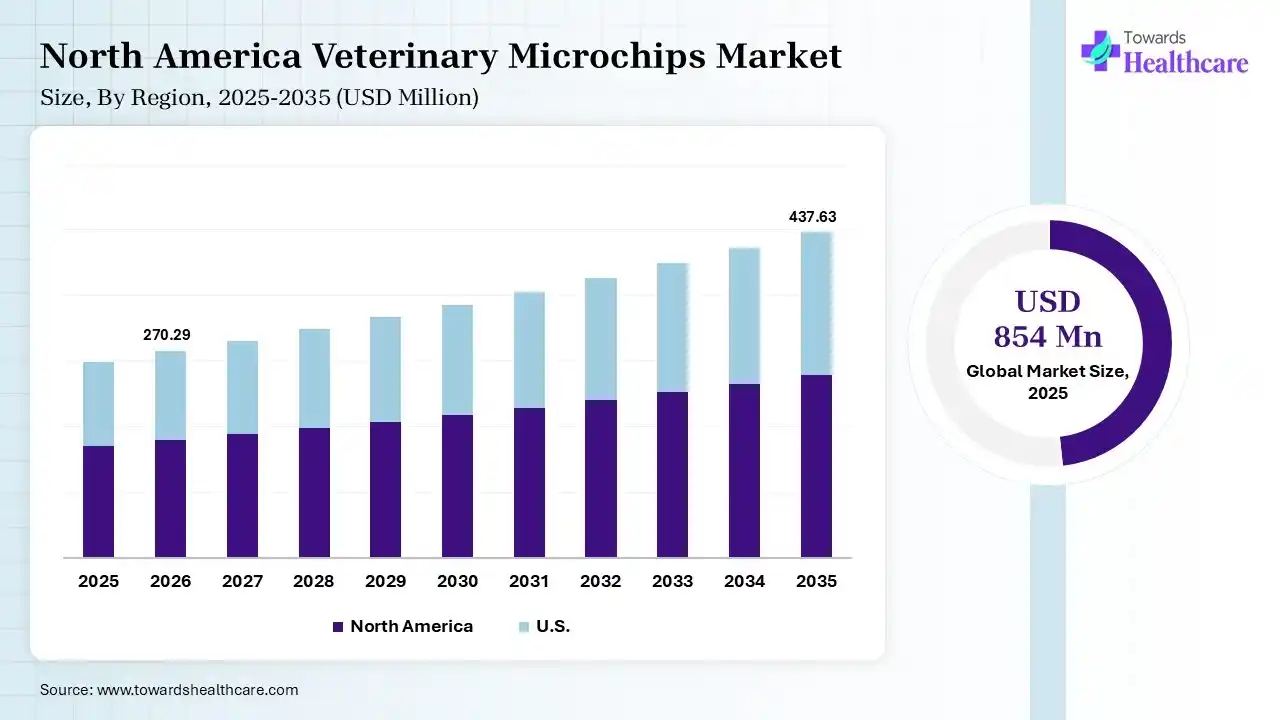

With a 40% of dominating share, North America led the veterinary microchips market. This regional dominance is fueled by the higher pet ownership, i.e., nearly 94 million households owned at least one pet in 2025. Also, the regional government & local regulations are fostering the need or spurring microchipping for pet registration, travel, & breeding. Alongside, notable efforts cover the Canadian Horse Identification Program (CHIP) introduced by Equestrian Canada for centralizing & standardizing microchipping for horses.

U.S. Market Trends

On the other hand, the U.S. market has implemented the United States Equestrian Federation (USEF), which necessitates all horses in licensed competitions to be microchipped with a 15-digit ISO 11784/11785 compliant chip.

For instance,

Asia Pacific held 20% share of the veterinary microchips market in 2025, and is predicted to expand at 7.0% CAGR. This is primarily surging with the expansion of economic development, specifically in China & India, which has escalated the number of companion animals &emphasis on pet health. Alongside, China is transforming awareness regarding pet safety, with increased demand for chip technology to precisely track & find pets.

India Market Trends

India is anticipated to expand rapidly, as it is executing mandatory licensing, like the Greater Chennai Corporation (GCC), which made microchipping & licensing mandatory for all pet dogs and cats. Also, the Municipal Corporation of Delhi has secured significant funds in its 2026-27 budget for a huge program that emphasises microchipping & vaccinating approximately 25,000 to 1 million community dogs to foster extensive rabies monitoring.

R&D

Regulatory Approvals

Veterinary Support & Services

| Company | Description |

| Merck & Co., Inc. | This firm facilitates products through its HomeAgain brand for companion animals & Allflex Livestock Intelligence for livestock. |

| Peeva Inc | Its offerings include a centralized pet microchip registry & pet medical records database. |

| Virbac | This company offers veterinary microchips, especially through its BackHome electronic identification system. |

| ID Tech | A leader focuses on a comprehensive range of RFID-based veterinary microchips & animal identification products. |

| Dipole RFID | Its offerings cover glass microchips designed for implantation in pets, livestock, & other animals. |

| Trovan Ltd. | They have classified their products into ROVAN UNIQUE (read-only) & TROVAN FDX-B (ISO-compliant). |

| Wuxi Fofia Technology Co., Ltd | It is a key producer of ISO-compliant & ICAR-certified veterinary microchips. |

| Avid Identification Systems, Inc | This company explored AVID FriendChip & the PETtrac Recovery Network. |

| Datamars | A firm specializes in ISO-compliant microchips, high-performance scanning technology, & a 24/7 registration/recovery service. |

| Pethealth Inc | This facilitates a complete set of identification products & services for veterinarians, shelters, and pet owners. |

Strengths

Weaknesses

Opportunities

Threats

By Technology Type

By Animal Type

By End-User

By Application

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar