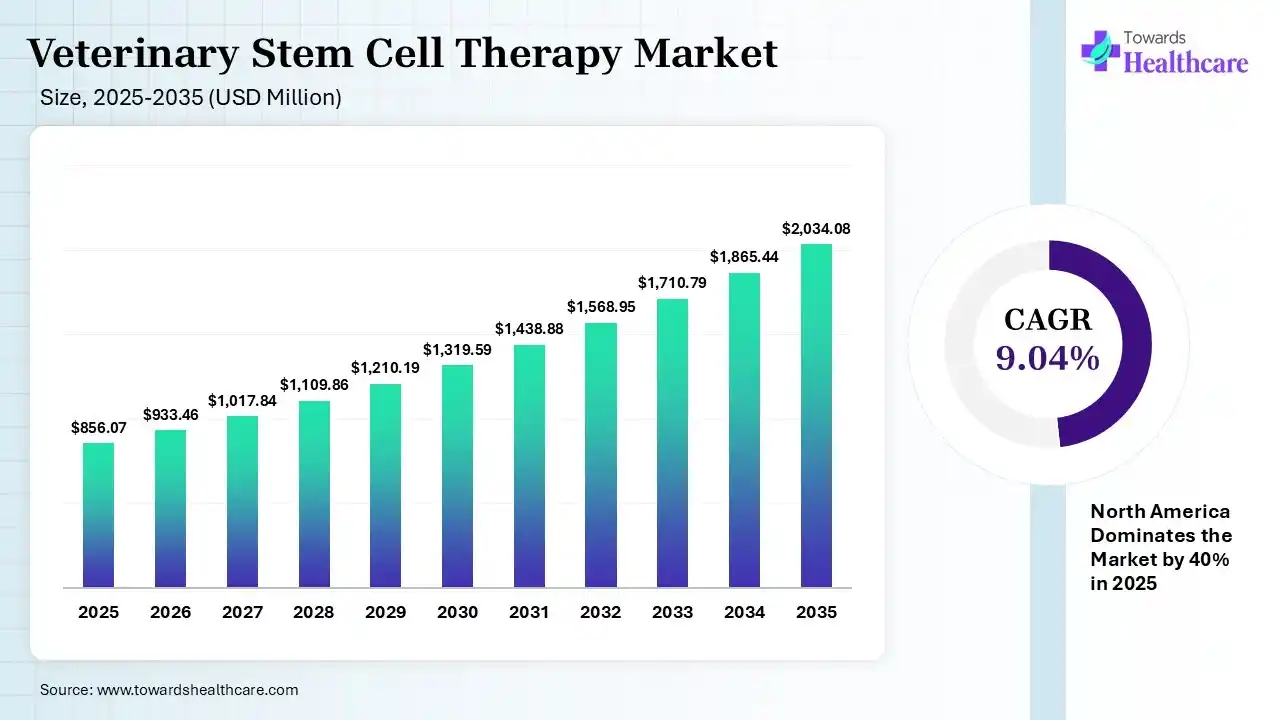

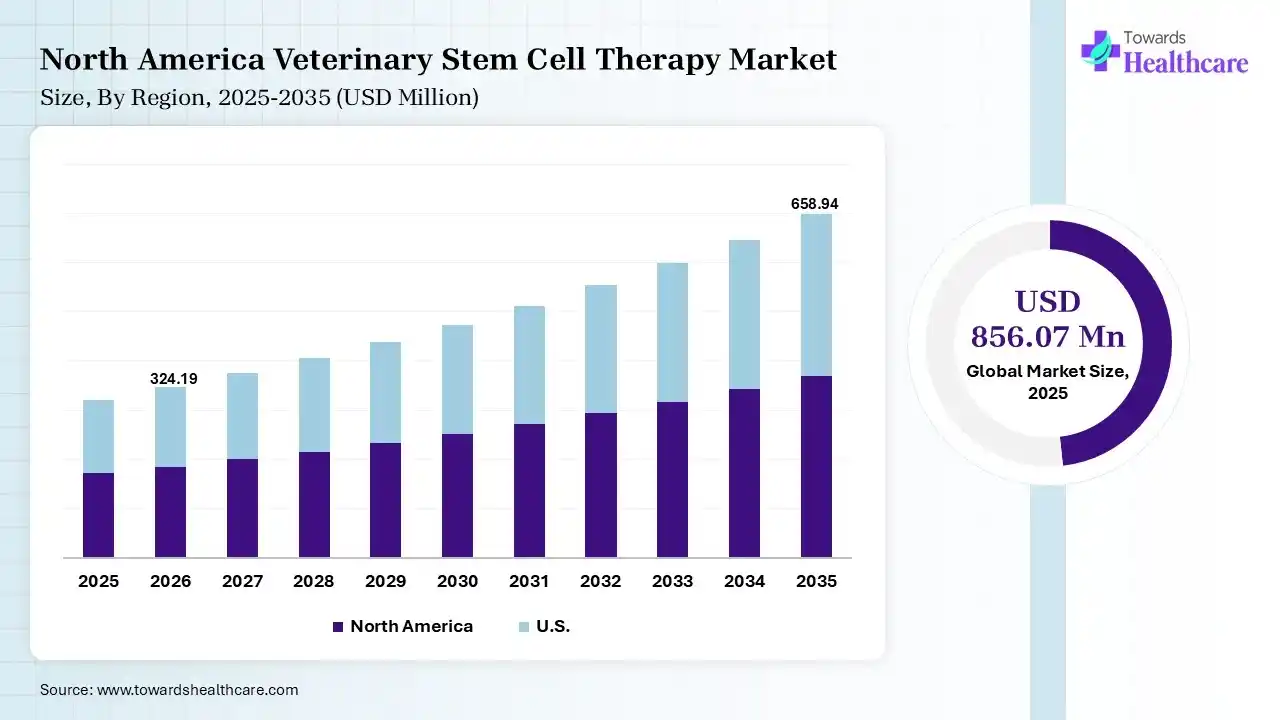

The global veterinary stem cell therapy market size was estimated at USD 856.07 million in 2025 and is predicted to increase from USD 933.46 million in 2026 to approximately USD 2034.08 million by 2035, expanding at a CAGR of 9.04% from 2026 to 2035.

The growing pet health awareness is increasing the adoption of veterinary stem cell therapies. The growing advancements in the veterinary R&D activities, rising pet ownership, and launch of new regenerative medications are also enhancing the market growth.

")

The veterinary stem cell therapy market is fuelled by the growing prevalence of chronic and degenerative conditions and a shift towards pet humanization. The veterinary stem cell therapy refers to the treatment options utilizing stem cells for the treatment, regeneration, and repair of damaged organs or tissues in animals. These therapies are used for the treatment of various chronic diseases in animals, where they treat the disease by regeneration, healing, or immune modulation.

AI plays an important role in the veterinary stem cell therapy market as it helps in the optimization of cell culture conditions, enhancing the yield and quality of the product. It also helps in the detection of new drug molecules and targets, where it also promotes the development of personalized stem cell therapies. It also helps in identifying the success and recovery aspects associated with these therapies.

Growing R&D Activities

The growth in R&D activities is driving the development of new veterinary stem cell therapies with enhanced safety and efficacy, where the growth in government funding is also increasing their innovations and accelerating their clinical trials.

Expanding Pet Healthcare

The growing health awareness among pet owners is fuelling the pet healthcare spending, promoting the adoption of advanced treatment options like regenerative therapies, which in turn is creating new opportunities for veterinary stem cell therapies.

Blooming Collaborations

To offer safe, effective, personalized, and affordable treatment options to the animals, new collaborations among the research institutions, veterinary clinics, and biotech firms are being formed, where their growing integration with telemedicine is also increasing the availability of veterinary stem cell therapies.

| Table | Scope |

| Market Size in 2026 | USD 933.46 Million |

| Projected Market Size in 2035 | USD 2034.08 Million |

| CAGR (2026 - 2035) | 9.04% |

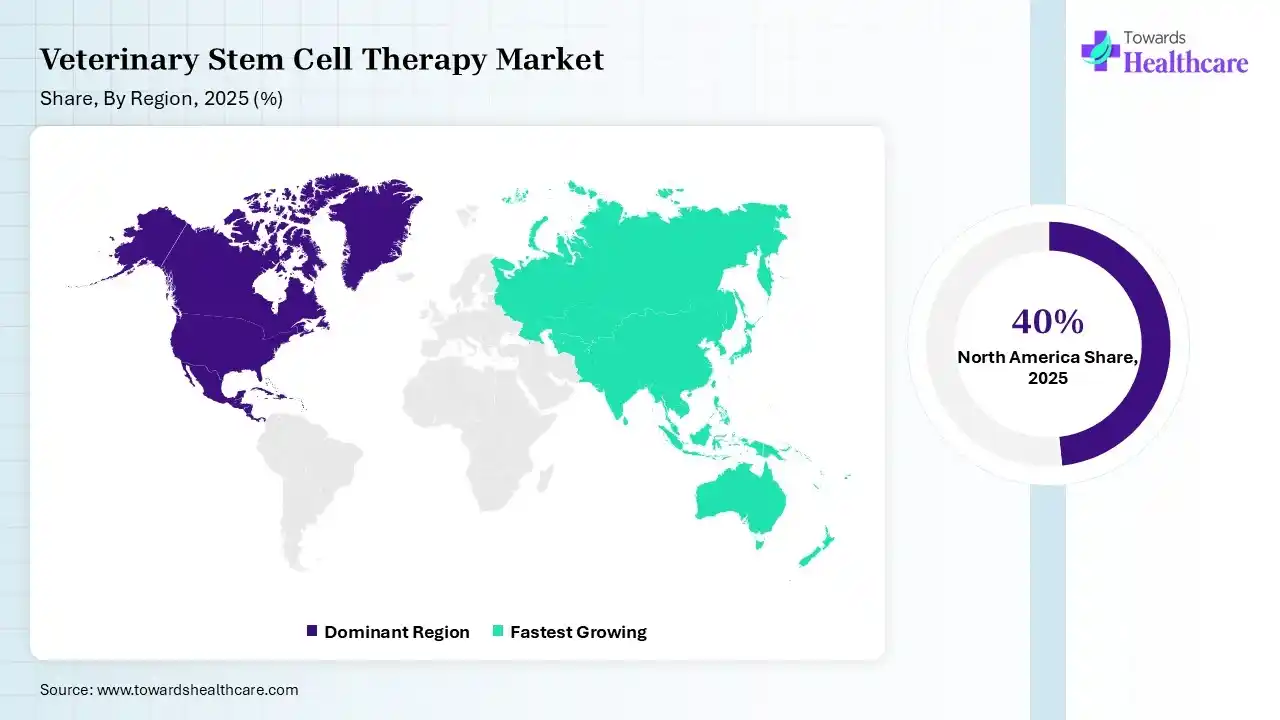

| Leading Region | North America by 40% |

| Key Applications | Osteoarthritis, Tendon & Ligament Injuries, Musculoskeletal Disorders, Wound Healing, Inflammatory Conditions, Neurological Disorders |

| Primary End Users | Veterinary Hospitals, Specialty Animal Clinics, Equine Centers, Veterinary Research Institutions |

| Key Growth Drivers | Rising pet ownership, increasing spending on companion animal healthcare, growing prevalence of osteoarthritis in pets, advances in regenerative medicine, expansion of veterinary specialty care |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By End User, By Region |

| Top Key Players | VetStem Biopharma, Boehringer Ingelheim, Magellan, Regeneus (Cambium Bio), Vetbiobank, StemcellX, Escondido, Ee.Uu., Aye, Belguim, Leawood, U.S., Osaka, Japan |

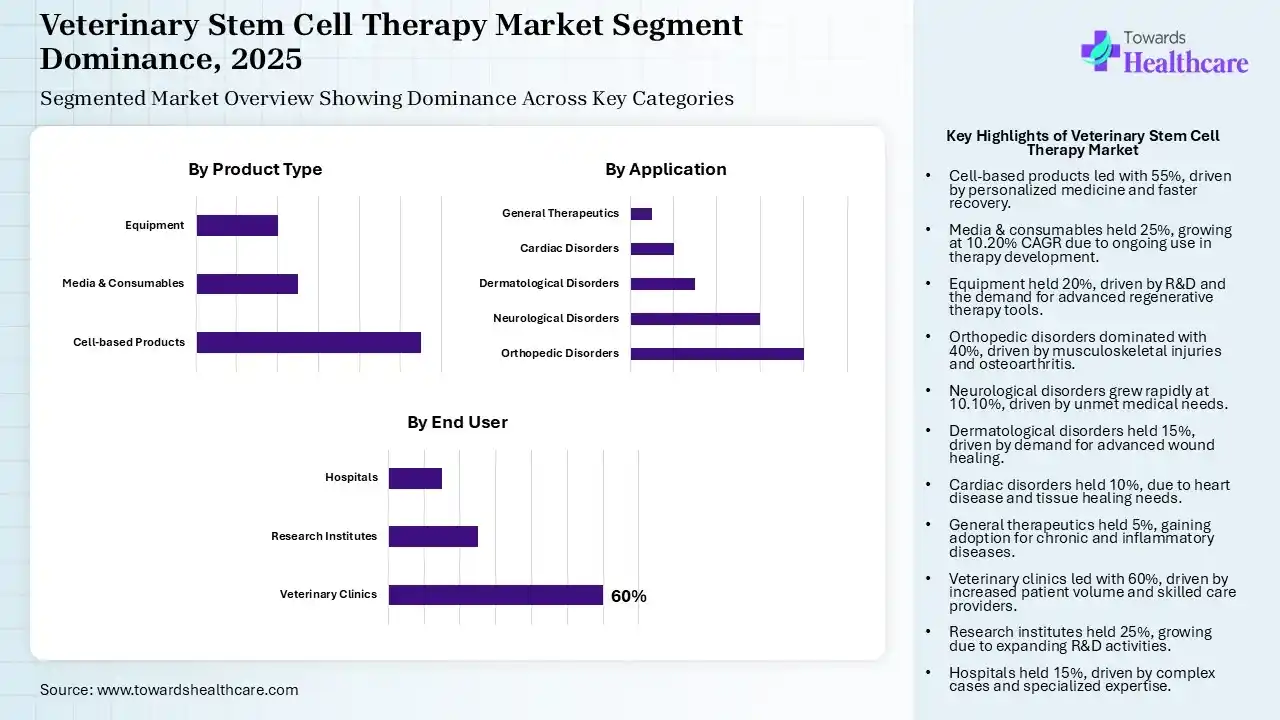

The Cell-based Products Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Cell-based Products | 55% |

| Media & Consumables | 25% |

| Equipment | 20% |

The cell-based products segment held the largest revenue share of 55% of the veterinary stem cell therapy market in 2025, due to growth in the demand for personalized medicines. The enhanced effectiveness and targeted action also increased their use. Their faster recovery and improved safety profile also promoted their acceptance rates.

The media & consumables segment held the second-largest share of 25% of the market in 2025, and is estimated to grow at a CAGR of 10.20%, driven by the repeated use in the development of every therapy. The growing advancements in the culture media development are also increasing their demand. Additionally, the growing development of new veterinary stem cell therapies is also increasing their use.

The equipment segment held 20% share of the market in 2025, due to growing R&D activities and clinical trials of the stem cell therapies. The expanding regenerative therapy centres and in-house stem cell process facilities are also increasing their use. The growing demand for advanced equipment is also increasing its adoption rates.

The Orthopedic Disorders Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Orthopedic Disorders | 40% |

| Neurological Disorders | 30% |

| Dermatological Disorders | 15% |

| Cardiac Disorders | 10% |

| General Therapeutics | 5% |

The orthopedic disorders segment contributed the biggest revenue share of 40% of the veterinary stem cell therapy market in 2025, due to growth in the musculoskeletal injuries and osteoarthritis. This increased the use of stem cell therapy to promote cartilage repair and overcome joint disease. Moreover, their affordability promoted their use over the surgeries.

The neurological disorders segment held the second-largest share of 30% of the market in 2025, and is estimated to grow at the fastest rate of 10.10%, due to their growing incidence. The high unmet medical need also increased the use of veterinary stem cell therapy. Additionally, their enhanced effectiveness and growing R&D activities are also increasing their use.

The dermatological disorders segment held 15% share of the market in 2025, due to growing demand for advanced wound healing therapies. This is increasing the use of veterinary stem cell therapy for the treatment of a wide range of skin conditions. Furthermore, the growing skin diseases and advancements in stem cell therapies are also increasing their use.

The cardiac disorders segment held 10% share of the market in 2025, due to growing heart disease in animals and limited heart tissue healing solutions. Additionally, poor conventional therapy and high mortality rates are also increasing the use of veterinary stem cell therapy. The growing focus on myocardial injury repair is also driving their innovations.

The general therapeutics segment held 5% share of the market in 2025, due to growing applications of stem cell therapy in inflammatory conditions. Their ability to treat complex and chronic disease are also increasing their adoption rates. Their growing advancements and expanding use in tissue repair are also increasing their use.

The Veterinary Clinics Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Veterinary Clinics | 60% |

| Research Institutes | 25% |

| Hospitals | 15% |

The veterinary clinics segment accounted for the highest revenue share of 60% of the veterinary stem cell therapy market in 2025, and is estimated to grow at the highest CAGR of 8.40%, as they were considered the primary point-of-care options. The growth in the patient volume and availability of skilled veterinarians has also increased their preference. Increased availability of stem cell services also increased their use.

The research institutes segment held the second-largest share of 25% of the market in 2025, due to expanding stem cell R&D activities. The growing investments and funding are also accelerating the development of new veterinary stem cell therapy. The growing collaborations, technological advancements, and expanding applications are also driving their innovations.

The hospitals segment held 15% share in the market in 2025, driven by the expanding applications in the treatment of various animal diseases. The growing complex cases and high treatment volume are also increasing their use. Furthermore, the presence of expertise and specialized equipment is also attracting the pet owners.

")

North America dominated the veterinary stem cell therapy market with 40% in 2025, due to a growth in pet healthcare spending and pet ownership. The presence of well-developed veterinary infrastructure also increased the use of veterinary stem cell therapy. Additionally, growth in their orthopaedic diseases and adoption of advanced technologies also increased their use and innovations, which contributed to the market growth.

U.S. Market Trends

The growing willingness of the pet owner to invest in advanced therapies like veterinary stem cell therapy in the U.S. is increasing, driving their rapid adoption. This is promoting the development of new regenerative medicines, where their growing collaborations are also accelerating these researches. Furthermore, advanced veterinary infrastructure is also enhancing the availability of these therapies.

Asia Pacific is seen to grow at a CAGR of 9.40% during the forecast period, and it also held a considerable share of 15% of the veterinary stem cell therapy market in 2025, due to growing pet ownership and disposable income. The expanding veterinary infrastructure and their health awareness are also increasing the adoption of veterinary stem cell therapies. Expanding R&D activities and government initiatives are also increasing their use, enhancing the market growth.

China Market Trends

The growing pet ownership in China is increasing the demand for advanced treatment options for their growing chronic and orthopedic disorders. The expanding awareness, disposable incomes, and veterinary infrastructure are also increasing the adoption of veterinary stem cell therapies. Additionally, growing R&D activities and investments are also increasing their use.

Europe is expected to grow significantly in the veterinary stem cell therapy market during the forecast period, due to the presence of advanced veterinary infrastructure. The growing pet health awareness and increasing pet ownership are also increasing the adoption of veterinary stem cell therapies. The growing chronic diseases, expanding R&D activities, and increasing collaborations are also fueling their innovation, which is promoting the market growth.

Due to the large pet ownership in the UK, the pet healthcare spending is increasing, driving the adoption of veterinary stem cell therapies. The presence of advanced veterinary clinics and the launch of new veterinary stem cell therapies are also increasing their adoption rates. Growing orthopaedic diseases and growing awareness are also increasing their demand.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | VetStem, Gallant, Animal Cell Therapies | Develop stem-cell isolation, preservation, and regenerative medicine technologies |

| Product Manufacturers | Ardent Animal Health, VetStem, Cell Therapy Sciences | Manufacture veterinary stem cell-based therapeutic products |

| Service Providers | Veterinary Specialty Hospitals, Equine Clinics | Administer stem cell therapies and patient management |

| Platform Providers | Gallant, VetStem Biopharma | Cell banking and stem cell processing platforms |

| CROs/CDMOs | Charles River Laboratories, Inotiv | Support preclinical research and translational development of veterinary regenerative therapies |

| Software Vendors | IDEXX Laboratories, Covetrus | Practice management and treatment monitoring solutions supporting regenerative medicine programs |

| Research Institutions | University of California Davis, Colorado State University, North Carolina State University, Cornell University | Conduct clinical studies and translational veterinary stem cell research |

| End-User Industries | Companion Animal Care, Equine Healthcare, Livestock Research | Utilize stem cell therapies for disease treatment and performance recovery |

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 60% | 28% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| VetStem Biopharma | Poway, California, USA | USA | Pioneer and market leader in veterinary stem cell therapies with thousands of treated animals | Autologous Stem Cell Therapy, PrecisePRP, Cell Banking |

| Gallant | San Diego, California, USA | USA | Leading allogeneic stem cell developer focused exclusively on veterinary regenerative medicine | Off-the-Shelf Stem Cell Therapies, Cell Banking |

| Ardent Animal Health | Lehi, Utah, USA | USA | Commercial regenerative medicine company serving companion animals | Stem Cell Processing & Regenerative Therapies |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| EquiStem LLC | New York, New York, USA | USA | Specialized provider focused on equine stem cell therapies | Equine Stem Cell Treatments |

| MediVet Biologics | Nicholasville, Kentucky, USA | USA | Regenerative medicine provider serving veterinary clinics globally | Stem Cell and PRP Systems |

| Magellan StemCells | Melbourne, Victoria, Australia | Australia | Commercial veterinary regenerative medicine company with international reach | AdiPC Stem Cell Therapies |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| PetStem Biotech | Seongnam | South Korea | Emerging stem cell therapy developer for companion animals | Canine Stem Cell Therapeutics |

| Celavet Inc. | Daejeon | South Korea | Developing veterinary cell therapy technologies | Veterinary Cell Therapy Products |

| AniCell Biotech | Seoul | South Korea | Specialized veterinary regenerative medicine developer | Stem Cell-Based Veterinary Treatments |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Application

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar