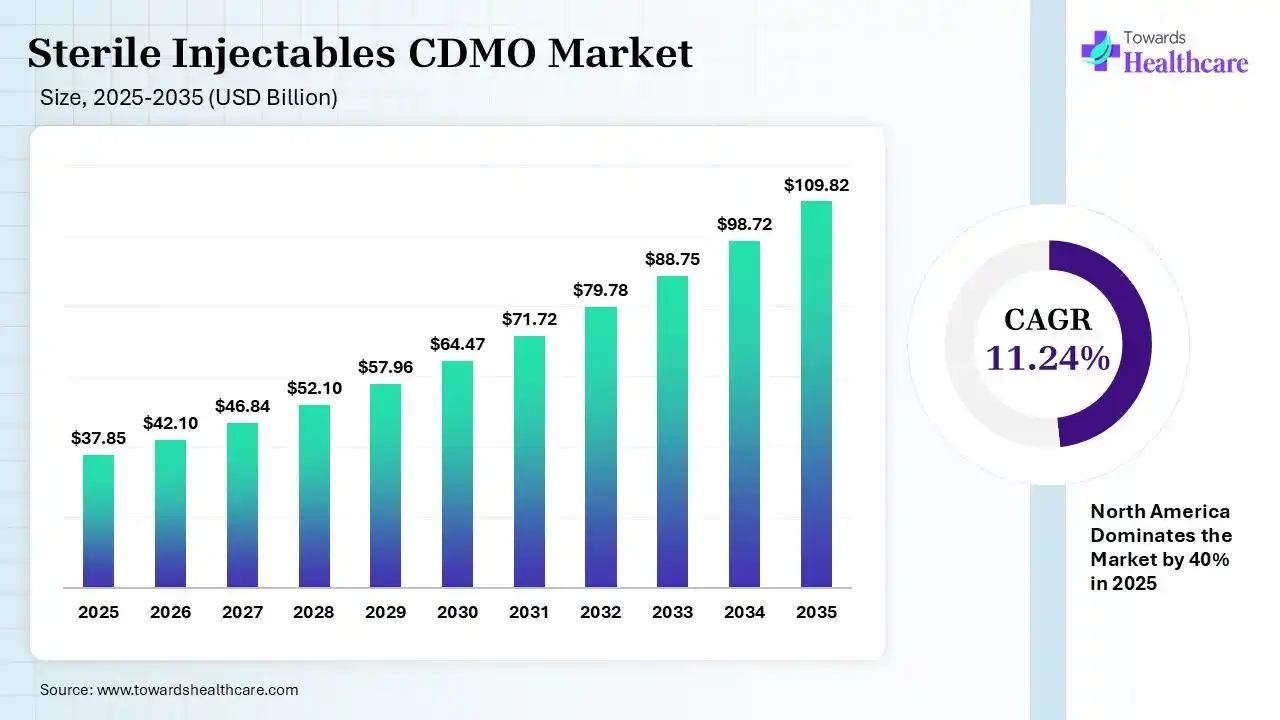

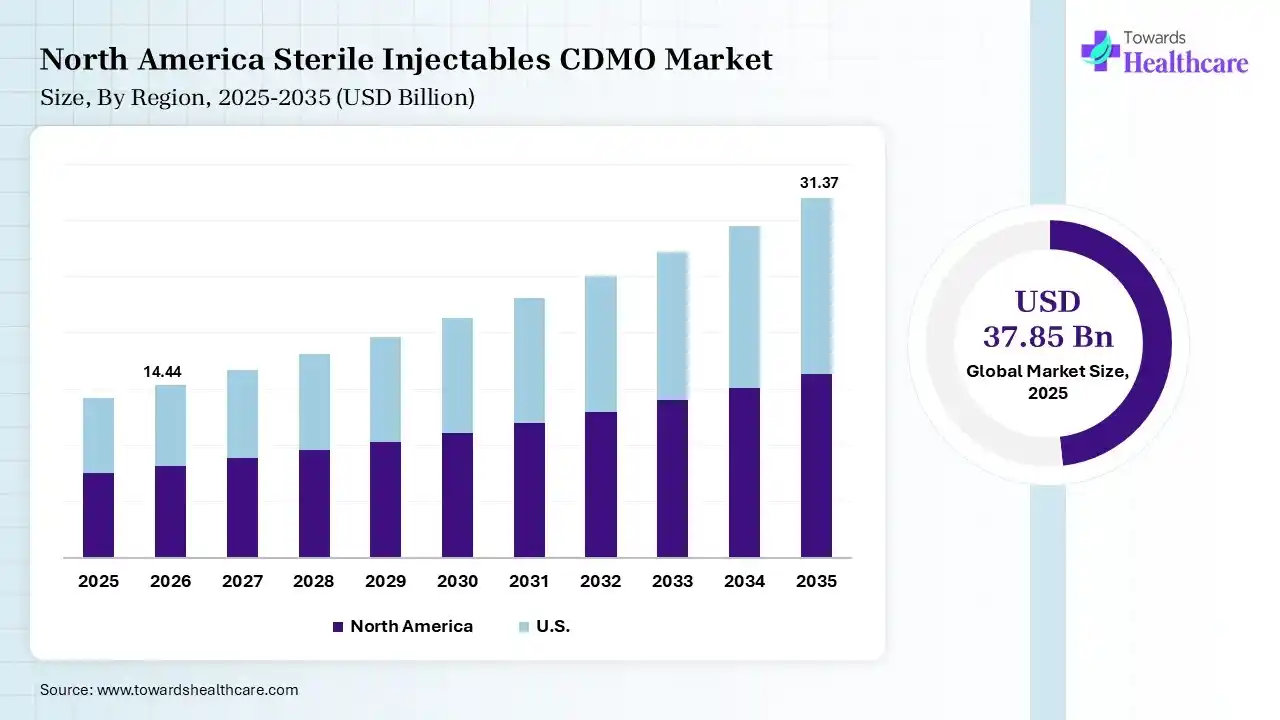

The global sterile injectables CDMO market size was estimated at USD 37.85 billion in 2025 and is predicted to increase from USD 42.1 billion in 2026 to approximately USD 109.82 billion by 2035, expanding at a CAGR of 11.24% from 2026 to 2035. The market is growing strongly as drugmakers outsource complex sterile drug manufacturing, driven by rising demand for biologics, cost optimization, and stricter quality/regulatory requirements.

")

A sterile injectable CDMO is a contract development and manufacturing organization that specializes in producing sterile injectable drugs for pharmaceutical companies, handling formulation, production, and packaging under strict quality standards. The sterile injectables CDMO market is witnessing strong growth as pharmaceutical and biotech companies increasingly outsource complex drug manufacturing to save costs, reduce risks, and speed up product launch. Surging demand for biologics, biosimilars, and advanced therapies, along with strict quality and regulatory requirements, drives reliance on specialized CDMOs. Capacity limitations in internal facilities further accelerate global adoption, making these partners essential for efficient sterile injectable production.

Artificial intelligence can significantly impact the sterile injectable CDMO market by optimizing drug formulation, streamlining manufacturing processes, and improving quality control through predictive analytics. AI-enabled automation reduces human error, enhances batch consistency, and accelerates development timelines. Additionally, it supports regulatory compliance and process monitoring, allowing CDMOs to increase efficiency, lower costs, and meet growing demand for complex biologics and advanced sterile therapies.

Rise of Biologics and Advanced Therapies

Growing demand for complex biologics, biosimilars, and gene/cell therapies drives CDMOs to expand sterile injectable capabilities, offering specialized aseptic processing and advanced formulation expertise to meet industry needs.

Integration of Digital and AI Technologies

Adoption of AI, machine learning, and process automation enhances production efficiency, quality control, and regulatory compliance, enabling CDMOs to deliver faster, safer, and more cost-effective sterile injectable solutions.

Global Expansion and Strategic Partnerships

Increasing outsourcing and capacity constraints push pharmaceutical companies to collaborate with CDMOs worldwide, leading to strategic alliances, facility expansion, and investments in emerging markets to support global sterile drug demand.

| Table | Scope |

| Market Size in 2026 | USD 42.1 Billion |

| Projected Market Size in 2035 | USD 109.82 Billion |

| CAGR (2026 - 2035) | 11.24% |

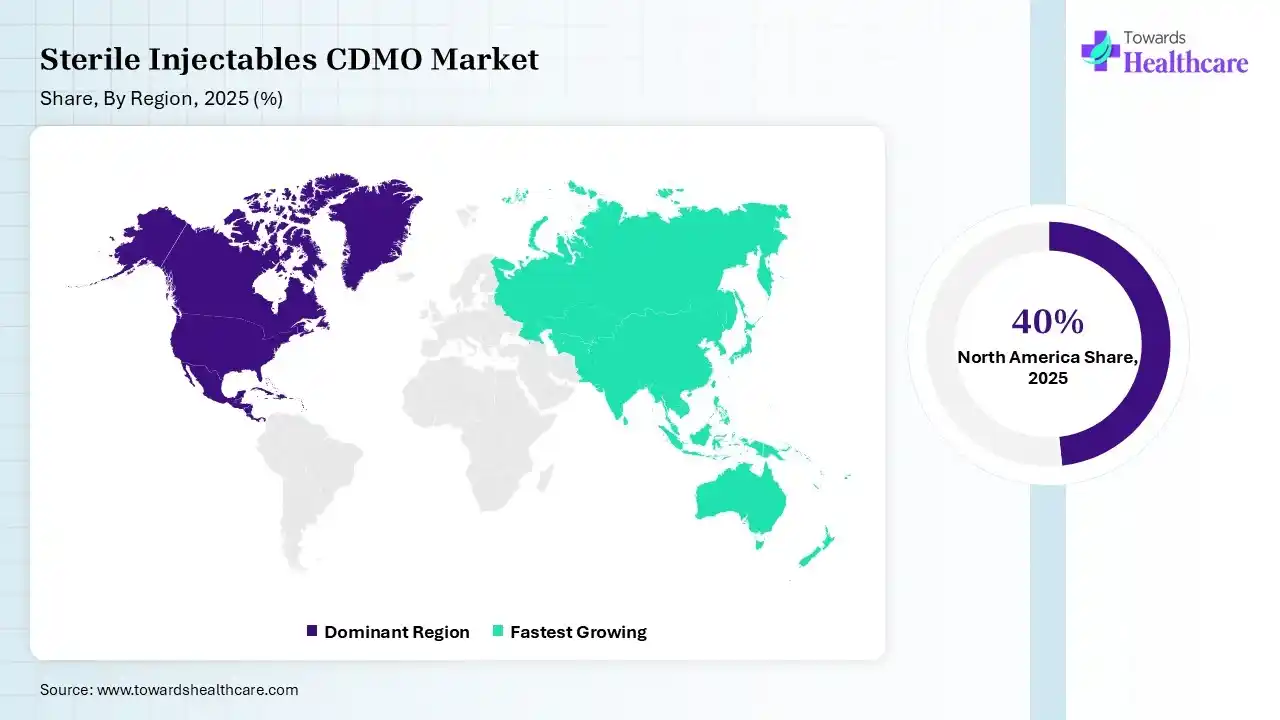

| Leading Region | North America by 40% |

| Key Applications | Biologics, Monoclonal Antibodies (mAbs), Vaccines, Oncology Drugs, Cell & Gene Therapies, Peptides, Biosimilars, Critical Care Injectables |

| Primary End Users | Pharmaceutical Companies, Biotechnology Companies, Emerging Biopharma Firms, Specialty Drug Developers |

| Key Growth Drivers | Biologics expansion, injectable drug demand, outsourcing trends, fill-finish capacity shortages, regulatory complexity, growth of biosimilars |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Formulation Type, By End-User, By Development Phase, By Mode of Delivery, By Region |

| Top Key Players | Boehringer Ingelheim GmbH, Baxter BioPharma Solutions, Vetter Pharma, Recipharm AB, Aenova Group, Fresenius Kabi, FAMAR Health Care Services |

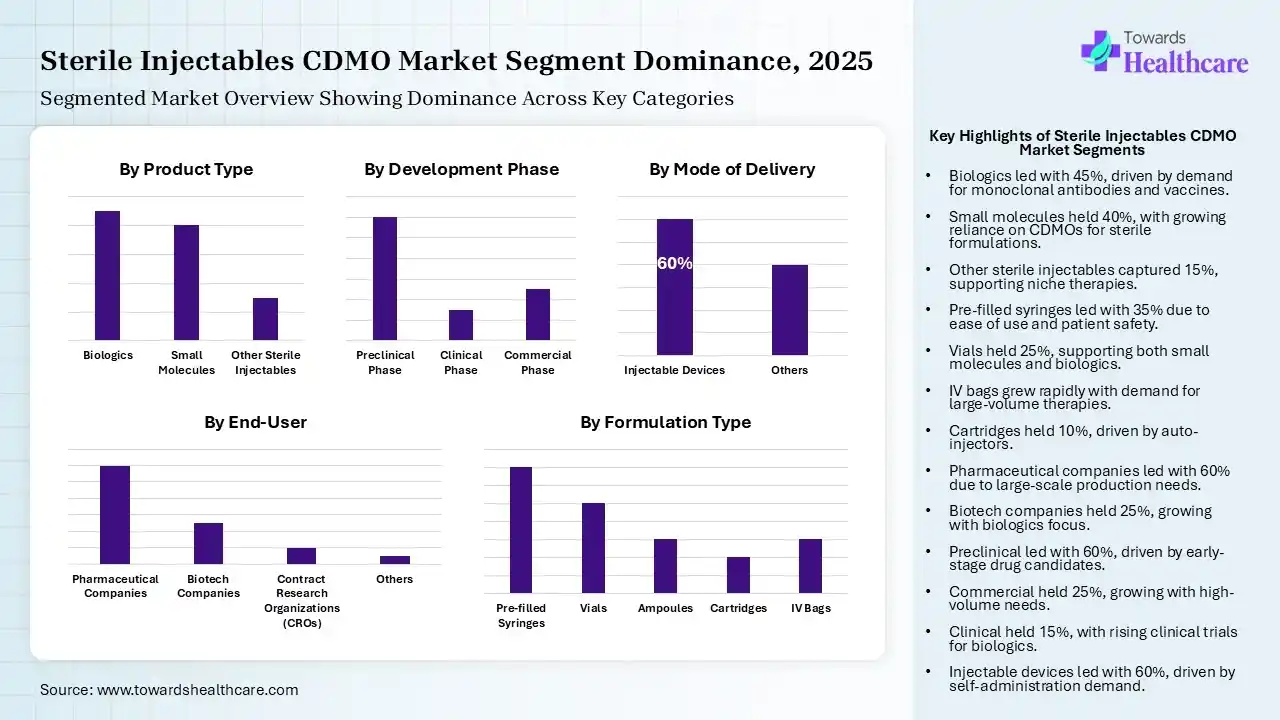

The Biologics Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Biologics | 45% |

| Small Molecules | 40% |

| Other Sterile Injectables | 15% |

The biologics segment dominated the sterile injectables CDMO market with shares of 45% in 2025 and is estimated to grow at the fastest CAGR of 10% due to the rising demand for complex therapies like monoclonal antibodies and vaccines. Their intricate manufacturing requirements and strict aseptic standards make outsourcing to specialized CDMOs essential, ensuring quality, compliance, and faster time-to-market for pharma and biotech companies.

The small molecules segment held the second-largest market share of 40% in 2025 due to their extensive use in conventional therapies and chronic disease treatments. Despite being less complex than biologics, their sterile formulation and manufacturing require specialized facilities and strict regulatory compliance. Pharmaceutical companies increasingly outsource these processes to CDMOs, benefiting from scalable production, consistent quality, and faster time-to-market, sustaining strong demand for small molecule injectables.

The other sterile injectables segment held the largest market share of approximately 15% in 2025 due to niche therapies, rare disease treatments, and emerging injectable formulations. Although smaller in volume than biologics or small molecules, these products require highly specialized aseptic manufacturing and regulatory expertise. Pharmaceutical companies rely on CDMOs for efficient production, quality assurance, and timely market delivery, supporting steady growth in this specialized segment.

The Pre-filled Syringes Segment Led the Market in 2025 with the Largest Share

| Segment | Share 2025 (%) |

| Pre-filled Syringes | 35% |

| Vials | 25% |

| Ampoules | 15% |

| Cartridges | 10% |

| IV Bags | 15% |

The pre-filled syringes segment led the sterile injectables CDMO market with a 35% share in 2025 due to ease of use, enhanced dosing accuracy, and improved patient safety. Their ready-to-administer design reduces contamination risks, supports efficient administration, and is preferred by healthcare providers, promoting CDMOs to prioritize production of pre-filled injectable formulations to meet rising global demand.

The vials segment held the second largest share, with 25%, in 2025 due to their versatility in storing both small molecules and biologics. They support multi-dose therapies, maintain stability, and comply with stringent sterility standards, making them a preferred choice for manufacturers. CDMOs continue to produce vials to meet global injectable demand efficiently.

The IV bags segment held a market share of 15% in 2025 and is expected to be the fastest-growing segment with a CAGR of 10% due to rising demand for large-volume therapies, including fluid replacements, parenteral nutrition, and intravenous drug delivery. Their flexibility, safety, and ease of administration make them essential in clinical settings. Pharmaceutical companies increasingly rely on CDMOs for sterile, compliant, and scalable manufacturing of IV bag formulation to meet global demand.

The ampoules segment captured 15% share of the market in 2025 due to their ability to ensure a fully sealed, contamination-resistant environment, making them ideal for sensitive and single-dose formulations. They offer excellent stability and cost-effectiveness, especially for generic injectables. Additionally, their simple design and strong barrier protection continue to support demand among CDMOs for reliable sterile packaging solutions.

The cartridges segment held the highest market share of 10% in 2025 due to growing demand for advanced drug delivery systems like pen injectors and auto-injectors. They enable accurate dosing, improving patient auto-injectors. They enable accurate dosing and improved patient convenience. Their strong compatibility with biologics and self-administration trends is driving CDMOs to expand sterile cartridge manufacturing capabilities.

The Pharmaceutical Companies Segment held a dominant position in the Market in 2025

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 60% |

| Biotech Companies | 25% |

| Contract Research Organizations (CROs) | 10% |

| Others | 5% |

The pharmaceutical companies segment dominated the sterile injectables CDMO market with shares of 60% in 2025 due to their large-scale production needs and expanding injectable drug pipelines. They increasingly rely on CDMOs to handle complex sterile manufacturing, reduce operational costs, and meet strict regulatory standards while focusing on core activities like drug discovery and commercialization.

The biotech companies segment held the second-largest market share of 25% in 2025 and is estimated to achieve the fastest CAGR of 10% due to their growing focus on biologics, biosimilars, and advanced therapies requiring sterile injectable formats. Limited in-house manufacturing capabilities and high development costs drive them to partner with CDMOs for specialized expertise, scalable production, and regulatory compliance, supporting their market expansion.

The contract research organizations (CROs) segment captured a 10% share of the market in 2025 and is growing due to increasing outsourcing of early-stage drug development and clinical trials services. CROs collaborate with CDMOs for a seamless transition from research to sterile manufacturing, reducing timelines and costs. Their expanding role in integrated development services and rising demand for complex injectable therapies are driving steady growth in this segment.

The Preclinical Phase Segment held the Largest Market Share in 2025

| Segment | Share 2025 (%) |

| Preclinical Phase | 60% |

| Clinical Phase | 15% |

| Commercial Phase | 25% |

The preclinical phase segment held the largest sterile injectables CDMO market share of 60% in 2025 due to the high volume of early-stage drug candidates requiring formulation and testing. Pharmaceutical and biotech companies rely on CDMOs for specialized sterile development, cost-efficiency, and rapid screening, enabling them to advance promising injectable therapies efficiently into clinical trials.

The commercial phase segment held the second largest share of 25% in 2025 and is estimated to grow at the highest CAGR of 11% due to large-scale production needs for approved sterile injectable drugs. Pharmaceutical and biotech companies rely on CDMOs for high-volume manufacturing, consistent quality, and regulatory compliance. Outsourcing helps reduce capital investment while ensuring uninterrupted supply, supporting strong demand for CDMO services in the commercial stage.

The clinical phase held a dominant position in the market share of 15% in 2025 due to increasing clinical trials for injectable drugs, especially biologics and specialty therapies. CDMOs support this phase with sterile manufacturing, smart-batch production, and regulatory compliance. Their expertise helps ensure a timely supply of trial materials, driving demand during clinical development stages.

The Injectable Devices Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Injectable Devices | 60% |

| Others | 40% |

The injectable devices segment dominated the sterile injectables CDMO market with shares of 60% in 2025 due to rising demand for self-administration and patient-friendly drug delivery systems. Devices such as auto-injectors and pens improve dosing accuracy, safety, and compliance. CMDOs support their complex assembly and sterile filling requirements, driving strong adoption across biologics and disease treatments.

The others segment held the second-largest market share of 40% and is expected to grow at the highest CAGR of 12% during 2026-2035 in 2025 due to the continued use of conventional delivery such as syringes and infusion systems. These options remain widely adopted for hospital-based treatments and emergency care. Their reliability and cost-effectiveness are supported by CDMOs for large-scale sterile production.

")

North America dominated the sterile injectables CDMO market with a 40% share in 2025 due to its advanced pharmaceutical infrastructure, strong presence of leading drug manufacturers, and high adoption of biologics and innovative therapies. The region benefits from well-established regulatory frameworks, significant R&D investments, and early adoption of advanced manufacturing technologies. Additionally, the increasing outsourcing trend and strong demand for sterile injectable drugs further support the region’s market leadership.

U.S. Market Trends

The U.S. leads the sterile injectables CDMO market due to its strong pharmaceutical and biotechnology ecosystem, advanced manufacturing capabilities, and high R&D investments. The presence of major pharma companies and specialized CDMOs supports large-scale sterile production. Additionally, stringent regulatory standards, early adoption of advanced technologies, and growing demand for biologics and complex injectables further drive market leadership.

Asia Pacific is seen to grow at a CAGR of 12% during the forecast period, and it also held a considerable share of 20% of the market in 2025 due to expanding pharma manufacturing capacity, lower production costs, and increasing outsourcing from global companies. Rapid growth in biologics demand, improving regulatory standards, and strong government support are accelerating market expansion. Additionally, a skilled workforce and rising healthcare investments are positioning the region as a preferred hub for sterile injectable development and manufacturing.

India Market Trends

India is expected to witness the fastest CAGR due to its strong cost advantage, expanding pharmaceutical manufacturing base, and increasing outsourcing from global companies. Government support, improving regulatory compliance, and the availability of skilled professionals are accelerating growth. Additionally, rising investments in biologics and sterile infrastructure, along with strong export capabilities, are positioning India as a key player in the global sterile injectables CDMO market.

| Ecosystem Segment | Key Participants | Role in Ecosystem |

| Technology Providers | West Pharmaceutical Services, SCHOTT Pharma, Gerresheimer, Stevanato Group | Provide syringes, vials, cartridges, closures, and containment technologies |

| Product Manufacturers | Large pharma and biotech companies | Develop injectable drug products |

| Service Providers | Sterile manufacturing specialists | Analytical testing, formulation, process development |

| Platform Providers | Automated aseptic manufacturing technology suppliers | Fill-finish, isolators, robotics, serialization |

| CROs/CDMOs | Vetter, Recipharm, PCI Pharma Services, Simtra, Catalent, Siegfried | End-to-end development and manufacturing |

| Software Vendors | SAP, MasterControl, Veeva Systems | Manufacturing execution, quality management, compliance |

| Research Institutions | Academic medical centers and translational research institutes | Early-stage injectable therapy development |

| End-User Industries | Pharmaceuticals, Biotechnology, Cell & Gene Therapy, Vaccines | Outsource sterile manufacturing activities |

Clinical Trials

Regulatory Approvals

Packaging and Serialization

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 29% | 13% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Vetter Pharma | Ravensburg, Baden-Württemberg | Germany | Global leader in aseptic fill-finish and prefilled syringe manufacturing with strong biologics focus | Sterile fill-finish, syringes, cartridges, commercial manufacturing |

| Simtra BioPharma Solutions | Bloomington, Indiana | USA | Former Baxter BioPharma Solutions; one of the largest dedicated sterile injectable CDMOs | Sterile injectables, lyophilization, aseptic manufacturing |

| Recipharm AB | Stockholm | Sweden | Major global CDMO with broad sterile injectable network | Fill-finish, formulation development, sterile manufacturing |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| PCI Pharma Services | Philadelphia, Pennsylvania | USA | Significant investments in sterile fill-finish and drug-device services | Sterile fill-finish, injectable packaging |

| Recipharm | Stockholm | Sweden | Strong European sterile injectable manufacturing network | Aseptic filling, biologics manufacturing |

| Siegfried Holding AG | Zofingen | Switzerland | Expanding injectable manufacturing footprint globally | Sterile drug products, aseptic manufacturing |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Bora Pharmaceuticals | Taipei | Taiwan | Growing global sterile injectable CDMO through acquisitions and expansion | Sterile fill-finish, injectable manufacturing |

| INCOG BioPharma Services | Fishers, Indiana | USA | Rapidly expanding biologics and injectable capacity | Biologics manufacturing, fill-finish |

| Grand River Aseptic Manufacturing | Grand Rapids, Michigan | USA | Specialized sterile injectable contract manufacturing | Aseptic filling, vial and syringe manufacturing |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Formulation Type

By End-User

By Development Phase

By Mode of Delivery

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar