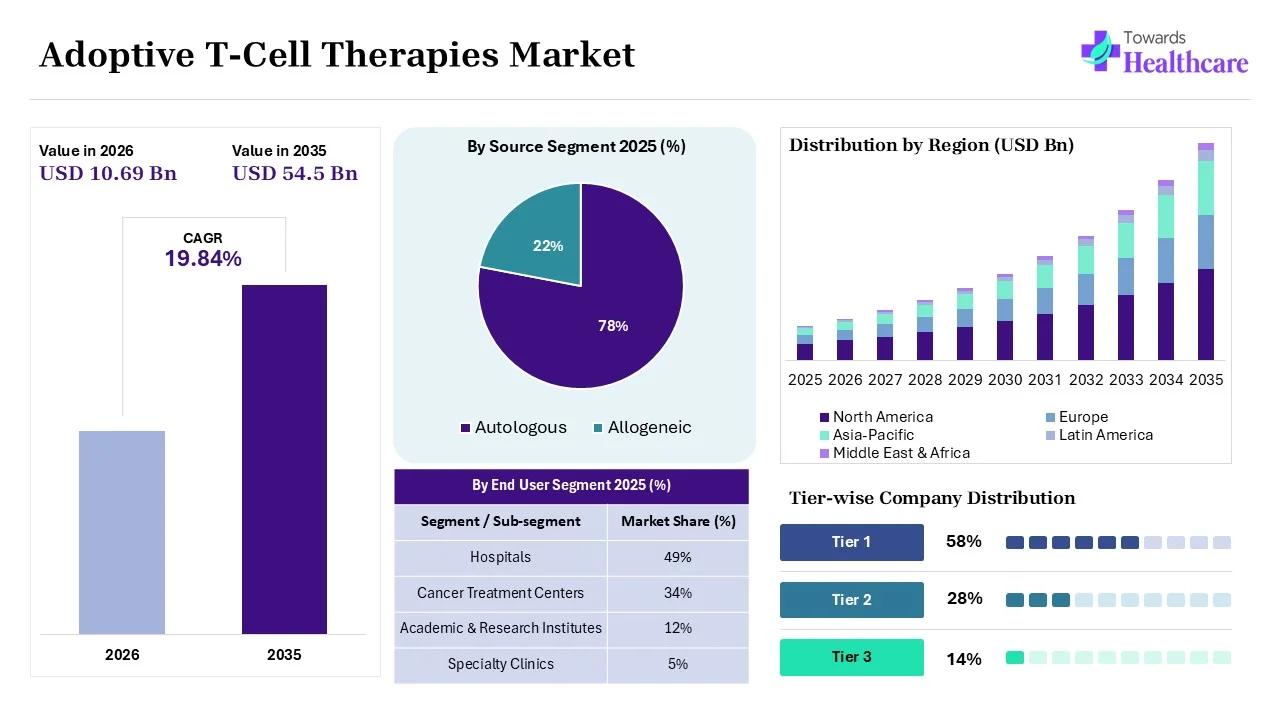

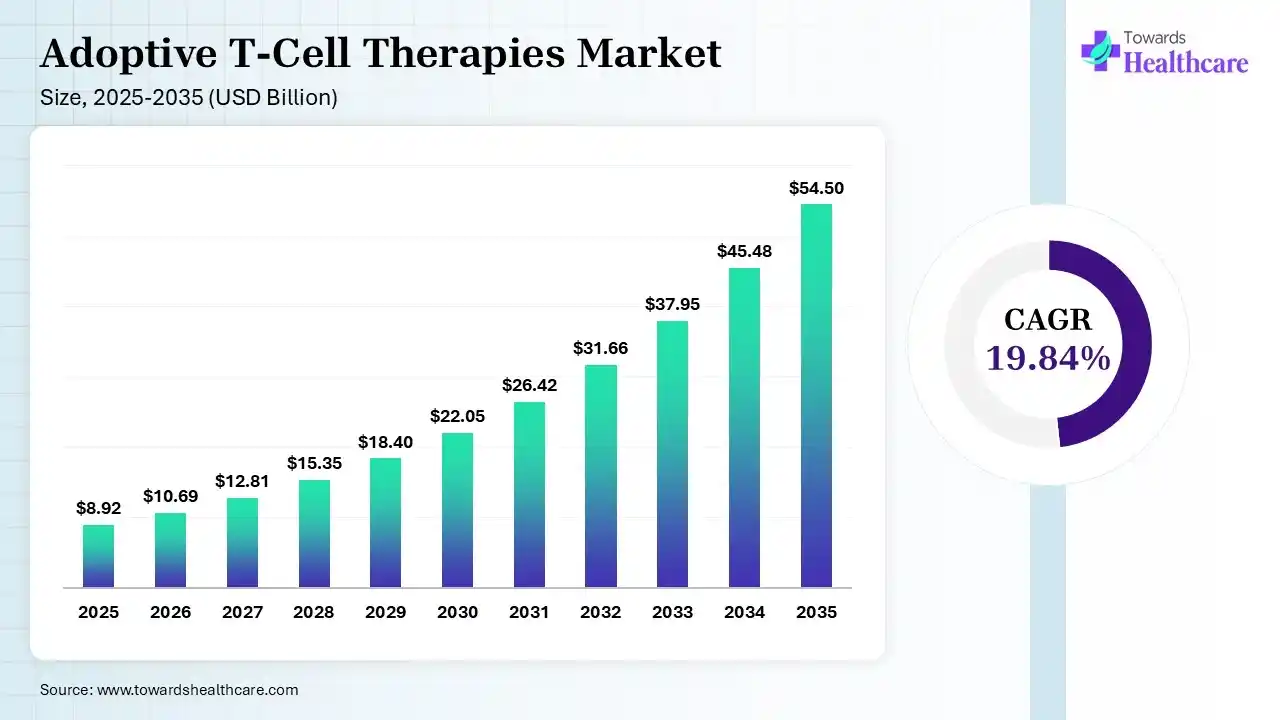

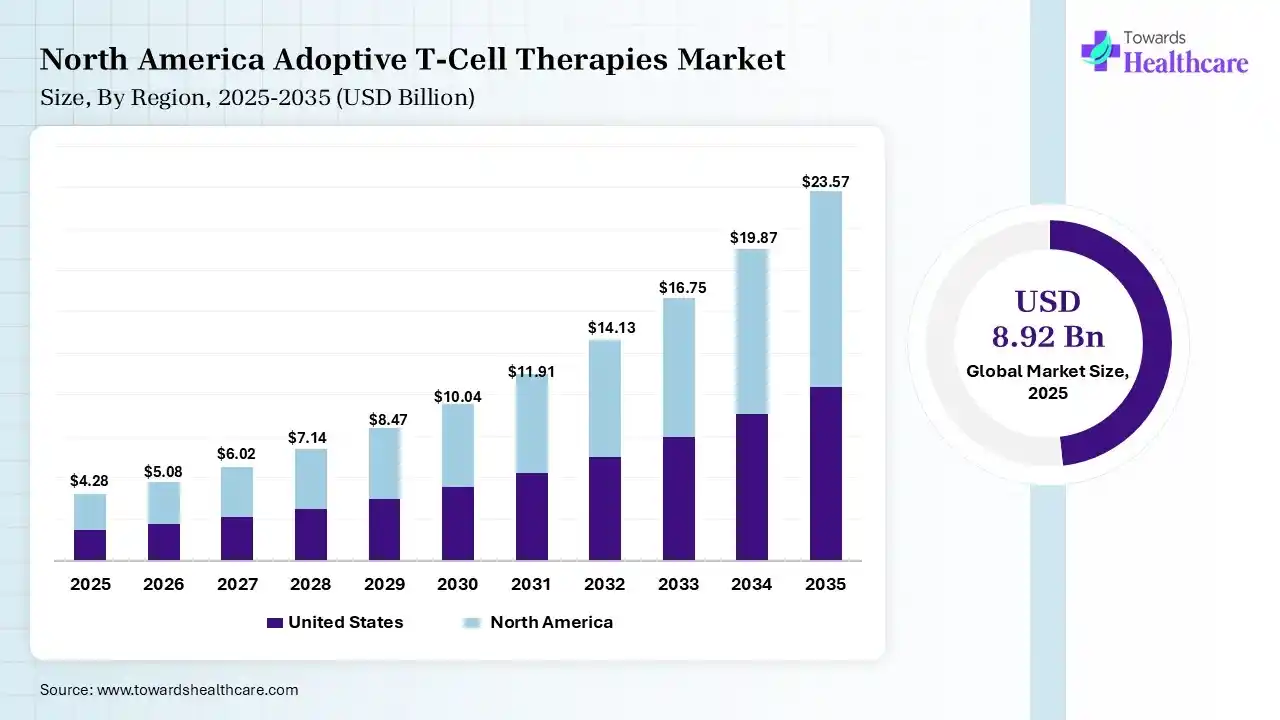

The global adoptive T-cell therapies market size is calculated at USD 8.92 billion in 2025, driven by growth in cancer burden. The market continues to grow in 2026 due to the expanding pipeline, technological advancements, and demand for off-the-shelf cell therapies. It is expected to reach USD 54.5 billion by 2035 as continued healthcare expansion, AI integration, and government support accelerate market expansion. North America accounted for 48% of the market in 2025 due to its robust reimbursement support, rise in approved therapies, and high R&D investments.

")

Introduction to Adoptive T-Cell Therapies

Adoptive T-cell therapies encompass cellular immunotherapies utilizing T lymphocytes to promote the immune system to target cancer cells. They are used to target multiple blood cancers and solid tumors, where a rise in the adoption of major therapy platforms such as CAR-T cell therapies, TCR-T cell therapies, tumor-infiltrating lymphocyte therapies, utilizing natural and modified T-cells, is also driving the market expansion.

Evolution of Cellular Immunotherapy

The growth in scientific advancements, genetic engineering, and precision medicine has transformed adoptive T-cell therapies over the years. The evolution of adoptive T-cell therapies began in 1960, which highlighted antigen-specific T cells for immunological roles, followed by harnessing the immune cells as a therapeutic modality in the 1970s. 1980s marked significant advancements in IL-2 purification and production, setting the stage for the development of adoptive T-cell therapies. In the 1990s, studies explored naturally occurring, ex vivo-cultured cell populations such as TILs and LAKs; in 1991, the first efforts to identify and clone both shared and mutated tumor-associated antigens recognized by T cells were reported. Furthermore, in 2002, enhanced in vivo proliferation, persistence, and tumor infiltration of adoptively transferred T cells were demonstrated by Dr. Steven Rosenberg's team.

Current Market Landscape

The adoptive T-cell therapies market is driven by increasing incidences of cancer, growing R&D investments, expanding pipeline, and technological advancements in gene editing. The rise in industry collaborations, investments, and acquisitions is driving the advancements in adoptive T-cell therapies. Additionally, this expanding industry maturity is propelling the launch of new adoptive T-cell therapies globally, where their active participation is also driving the development of next-generation T-cell therapies offering multiple antigen targeting action.

Shift Toward Personalized Cellular Immunotherapies

The growth in the use of personalized medicine is influencing therapy development and patient-specific treatment approaches. Their enhanced treatment efficacy, improved target-specific action, and reducing off target effect, driving their demand.

Expansion of Next-Generation Gene-Engineered T-Cell Platforms

Expanding innovations, including CAR-T evolution, TCR-T therapies, armored CARs, logic-gated CARs, and gene-editing technologies, are accelerating the advancements in adoptive T-cell therapies. They help enhance their applications, tumor targeting capabilities, and minimize the risk of toxicity.

Growing Investment in Off-the-Shelf Cell Therapies

A rise in allogeneic platforms is attracting investment due to scalability and manufacturing advantages. Moreover, their lower treatment cost has improved patient access, and rapid treatment initiation has increased their adoption rates.

Artificial Intelligence Supporting Cell Therapy Development

The role of AI in drug discovery, biomarker identification, manufacturing optimization, and clinical trial management is increasing, driving its adoption for adoptive T-cell therapies development. It also helps in predicting treatment outcomes, identifies potential adverse effects, and supports personalised treatment planning.

Increasing Global Cancer Burden

Rising cancer incidence worldwide is driving the demand for advanced immunotherapies. This drives the adoption of adoptive T-cell therapies for target-specific action, where growing awareness is also encouraging their use.

Growing Success of Commercial CAR-T Products

Regulatory approvals and favorable clinical outcomes support the expansion of CAR-T products. Their enhanced clinical efficacy, success rates, and survival outcomes are also promoting the development of next-generation products.

Continuous Innovation in Cell Engineering Technologies

Advancements in gene editing, synthetic biology, and manufacturing automation are fueling the adoptive T-cell therapies innovations. The advancements in these technologies are accelerating the discovery, development, and launch of new adoptive T-cell therapies globally.

High Manufacturing and Treatment Costs

The high cost associated with manufacturing processes involving cell collection and engineering reduces their adoption. Similarly, high treatment costs with reimbursement challenges also limit their accessibility.

Complex Manufacturing and Supply Chain Requirements

Multi-step production processes, logistics, and quality control challenges act as the major barrier in the market. They slow down product development and delay their market availability.

Safety Concerns and Treatment-Related Toxicities

Cytokine release syndrome, neurotoxicity, and other clinical concerns reduce the use of adoptive T-cell therapies, which in turn affects their commercialization.

Expansion into Solid Tumor Treatment

The growth in solid tumors represents the largest future commercial opportunity, which drives the demand for adoptive T-cell therapies. High unmet need drives their expansion, and growing regulatory approvals are creating new opportunities.

Development of Universal Cell Therapies

commercial potential of allogeneic and off-the-shelf products is prompting their advancement. Their reduced manufacturing times, lower production cost, and improved scalability are also supporting their rapid expansion.

Emerging Markets Offering Untapped Growth

With a growing cancer burden, investments are expanding opportunities across Asia-Pacific, Latin America, and the Middle East. Additionally, growing healthcare infrastructure and R&D activities are also propelling their innovations.

Tumor Resistance and Antigen Escape

Biological barriers affect treatment effectiveness by limiting the effectiveness of adoptive T-cell therapy and increasing chances of treatment failure.

Regulatory Complexity Across Global Markets

Differences in approval pathways and compliance requirements slow down the regulatory approvals of the adoptive T-cell therapies.

Reimbursement and Market Access Challenges

Pricing, payer acceptance, and healthcare affordability issues reduce access to and adoption rates of adoptive T-cell therapies.

Complete Industry Ecosystem Overview

Biotechnology companies, pharmaceutical manufacturers, CDMOs, hospitals, regulators, research institutions, and technology providers are actively participating in the market growth by continuously focusing on R&D, acquisitions, and new product launches.

Stakeholder Mapping

Different types of stakeholders such as academics, biotech and pharma companies, CDMOs, technology providers, and hospitals are driving next-generation adoptive T-cell therapies development, commercialization, and adoption strategies.

Strategic Partnerships Driving Innovation

A rise in licensing agreements, co-development partnerships, and academic collaborations is promoting the development of advanced adoptive T-cell therapies, driving integration of new technologies, expanding their commercialization, accelerating their clinical trials, and approval rates.

Research and Discovery Stage

Clinical Development

Manufacturing and Commercial Production

Treatment Delivery and Patient Monitoring

Evolution of CAR-T Cell Technologies

Technological advancements across successive CAR generations are driving the development of next-generation CAR-T therapies. They are being utilized to improve therapy efficacy, enhance safety, and expand their applications.

Progress in TCR-T Cell Development

Growing innovations in intracellular antigen targeting are improving the target-specific action. The growing focus on enhancing T-cell receptor-specificity is also driving innovations, where companies are also focusing on targeting intracellular tumor antigens.

CRISPR and Advanced Genome Editing

Genome editing improves efficacy and safety, which are creating new opportunities for adoptive T-cell therapies. They also help in enhancing genetic modification and reducing the risk of unwanted reactions.

Synthetic Biology and Programmable Cellular Therapies

There is a rise in the development of personalized and multi-target therapies, which offer enhanced effectiveness and safety. This, in turn, drives the development of logic-gated CARs, switchable CARs, and smart immune cells, expanding innovations.

Manufacturing Automation and Digital Innovation

Growing investments and adoption are leading to a rise in the use of robotics, AI, digital twins, and automated production systems. They are being used to accelerate manufacturing, quality control, real-time monitoring, and commercialization.

Current Global Clinical Pipeline: It highlights ongoing clinical trials by therapy type and development stage.

For instance,

Emerging Therapeutic Targets: It focuses on products offering new antigen targets and disease indications.

For instance,

Pipeline Trends Across Hematologic and Solid Tumors: It covers recent innovation activity between blood cancers and solid tumors.

For instance,

Global Regulatory Environment

The global regulatory environment focuses on the regulatory frameworks governing cell therapies. They help in maintaining the safety, efficacy, and quality standards of adoptive T-cell therapies.

Expedited Approval Programs

The expedited approval programs encompass breakthrough designation, priority review, and accelerated approval pathways. They facilitate faster product access and address unmet medical needs.

Reimbursement Trends

Reimbursement trends focus on growing payer models, value-based reimbursement, and pricing considerations. They help in enhancing access to the newly approved adoptive T-cell therapies.

Current Manufacturing Models

Current manufacturing models for adoptive T-cell therapies encompass centralized and decentralized manufacturing.

Raw Material and Component Supply Chain

The raw material and component supply chain of adoptive T-cell therapies involves vectors, culture media, reagents, and manufacturing equipment.

Cold Chain and Distribution Challenges

Cold chain and distribution challenges of adoptive T-cell therapies revolve around logistics requirements for cell therapy transportation.

Manufacturing Capacity Expansion

Manufacturing capacity expansion of adoptive T-cell therapies highlights investments in new production facilities and automation.

Current Therapy Pricing Landscape

The current therapy pricing landscape focuses on current pricing trends across commercial products.

Cost Structure Analysis

The cost structure analysis focuses on costs associated with manufacturing, logistics, clinical, and commercialization.

Factors Influencing Future Pricing

Factors influencing future pricing encompass a wide range of parameters such as automation, scale, and market competition.

Primary End-User Demand Assessment

The primary end-user demand assessment analyses demand across hospitals, cancer centers, and research institutions.

Patient Adoption Trends

Factors influencing patient acceptance and treatment selection are involved in patient adoption trends.

Physician Adoption and Referral Patterns

Physician adoption and referral patterns include clinician preferences and treatment decision-making.

Competitive Positioning of Leading Companies

Among the companies based on pipeline strength, approvals, manufacturing, partnerships, and geographic presence, Gilead Sciences led the market, where Bristol Myers Squibb was its closest competitor, and Johnson & Johnson also maintained its position.

Strategic Benchmarking Matrix

Gilead Sciences, Bristol Myers Squibb, and Johnson & Johnson dominated the market due to a rise in innovation capability, commercial readiness, manufacturing scale, and R&D investments.

Innovation Leadership Analysis

The companies leading technological advancement included Gilead Sciences, Bristol Myers Squibb, Johnson & Johnson, and Novartis AG.

| Table | Scope |

| Market Size in 2026 | USD 10.69 Billion |

| Projected Market Size in 2035 | USD 54.5 Billion |

| CAGR (2026 - 2035) | 19.84% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapy Type, By Antigen Target, By Indication, By End User, By Source, By Target Population, By Manufacturing Type, By Region |

| Top Key Players | Gilead Sciences, Bristol Myers Squibb, Johnson & Johnson Novartis AG, Iovance Biotherapeutics, Autolus Therapeutics |

")

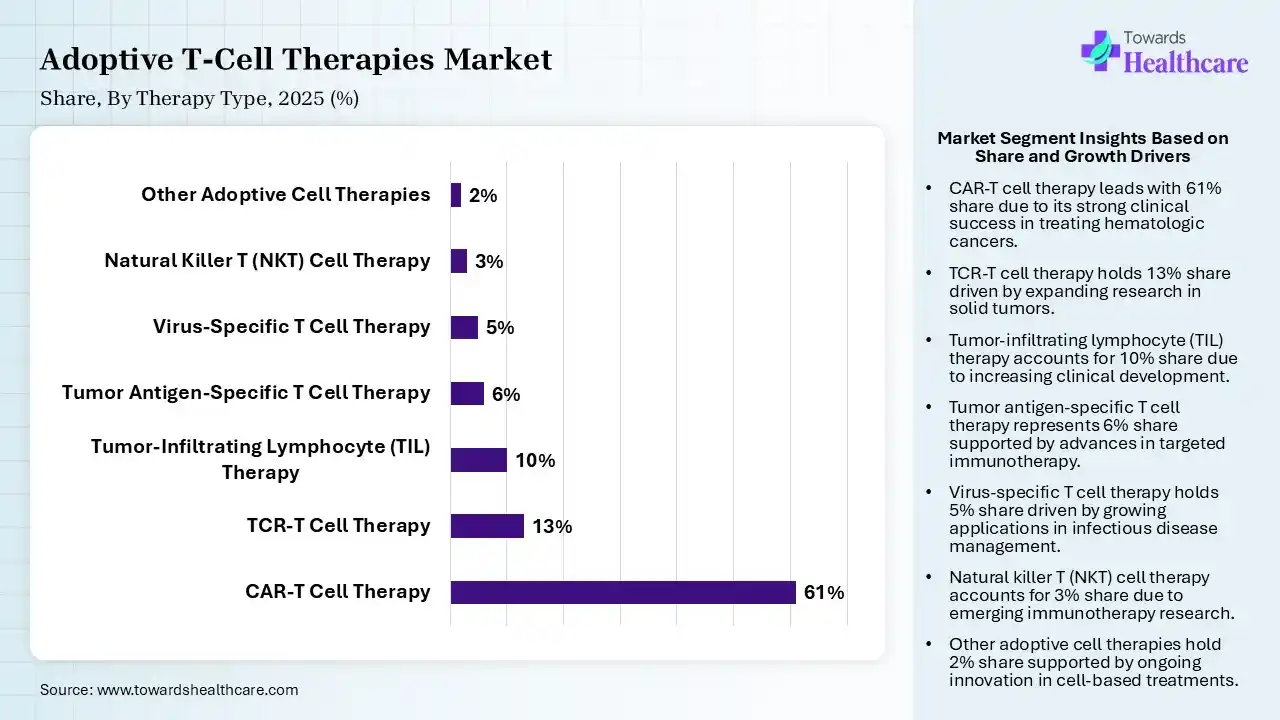

| Segment | Share 2025 (%) |

| CAR-T Cell Therapy | 61% |

| TCR-T Cell Therapy | 13% |

| Tumor-Infiltrating Lymphocyte (TIL) Therapy | 10% |

| Tumor Antigen-Specific T Cell Therapy | 6% |

| Virus-Specific T Cell Therapy | 5% |

| Natural Killer T (NKT) Cell Therapy | 3% |

| Other Adoptive Cell Therapies | 2% |

The CAR-T Cell Therapy Segment Dominated the Adoptive T-Cell Therapies Market With 61% in 2025

The CAR-T cell therapy segment led the market with a 61% share in 2025, due to the largest number of approved products. Projected to grow to 6.47 billion in 2026. Forecasts suggest it will reach approximately US$ 30.72 billion by 2035, registering a CAGR of 18.9% during the period. Expansion of reimbursement policies also supported their commercialization. Continuous innovation also improved treatment outcomes.

The TCR-T cell therapy segment held the second-largest share of 13% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 25.2% during the forecast period, driven by growing focus on solid tumors. Enhanced TCR engineering also expands target range. Increasing clinical pipeline also accelerates their adoption.

The tumor-infiltrating lymphocyte (TIL) therapy segment held 10% of the adoptive T-cell therapies market share in 2025, due to growing regulatory approvals increasing confidence. Strong efficacy in melanoma also drives their utilization. Manufacturing improvements reduce turnaround time, promoting their rapid production.

The tumor antigen-specific T cell therapy segment held 6% of the market share in 2025, driven by increasing interest in precision immunotherapy. Growing clinical collaborations also expand their development. Improved antigen discovery also supports pipeline growth.

")

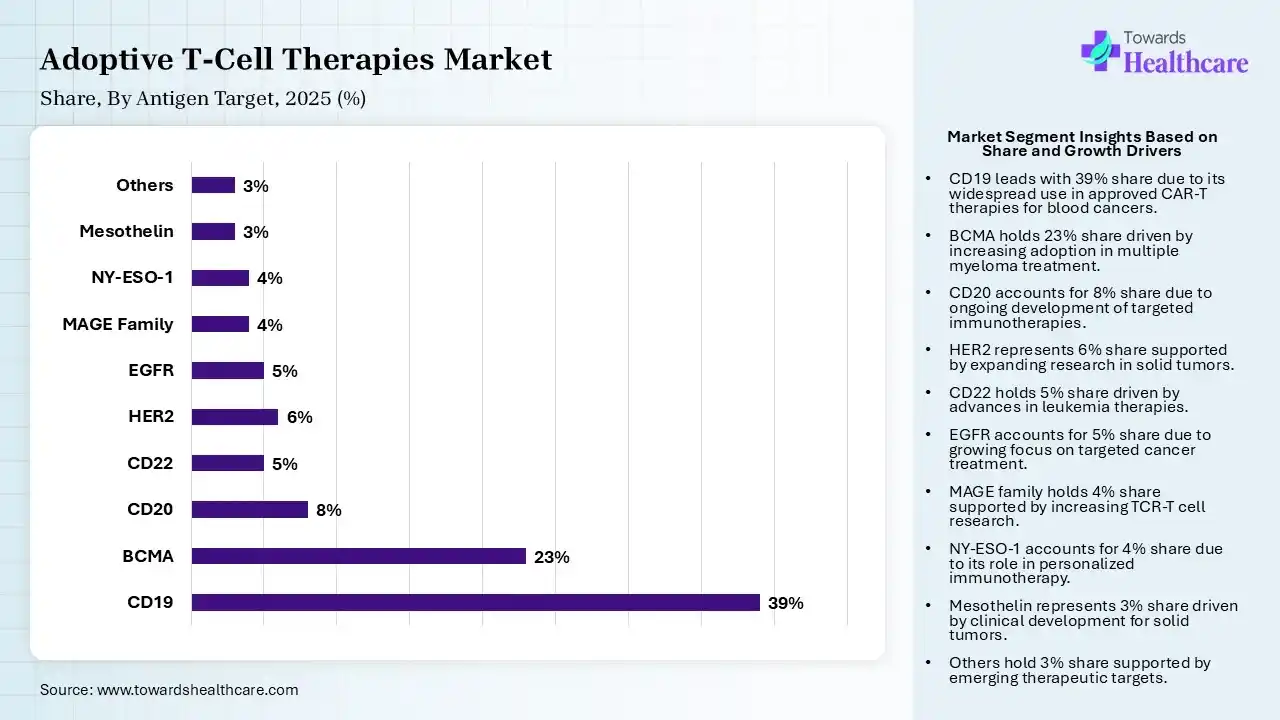

| Segment | Share 2025 (%) |

| CD19 | 39% |

| BCMA | 23% |

| CD20 | 8% |

| CD22 | 5% |

| HER2 | 6% |

| EGFR | 5% |

| MAGE Family | 4% |

| NY-ESO-1 | 4% |

| Mesothelin | 3% |

| Others | 3% |

The CD19 Segment Dominated the Adoptive T-Cell Therapies Market With 39% in 2025

The CD19 segment accounted for the highest revenue share of 39% of the market in 2025, driven by widespread use in approved CAR-T therapies. Strong lymphoma and leukemia indications also sustained their demand. Continued label expansion also supported its growth.

The BCMA segment held the second-largest share of 23% of the market in 2025, due to multiple myeloma incidence increasing its adoption. New product launches also strengthened market presence. Clinical evidence continues to improve, increasing its use.

The CD20 segment held 8% of the adoptive T-cell therapies market share in 2025, driven by expanded lymphoma research supporting development. Combination approaches also improve efficacy. Pipeline activity remains strong, expanding the innovations.

The HER2 segment held 6% of the market share in 2025 and is expected to show the highest growth with a CAGR of 24.5% during the forecast period, due to rapid advancements in solid tumor targeting. Improved safety profiles encourage trials. Expanding precision oncology also increases opportunities.

")

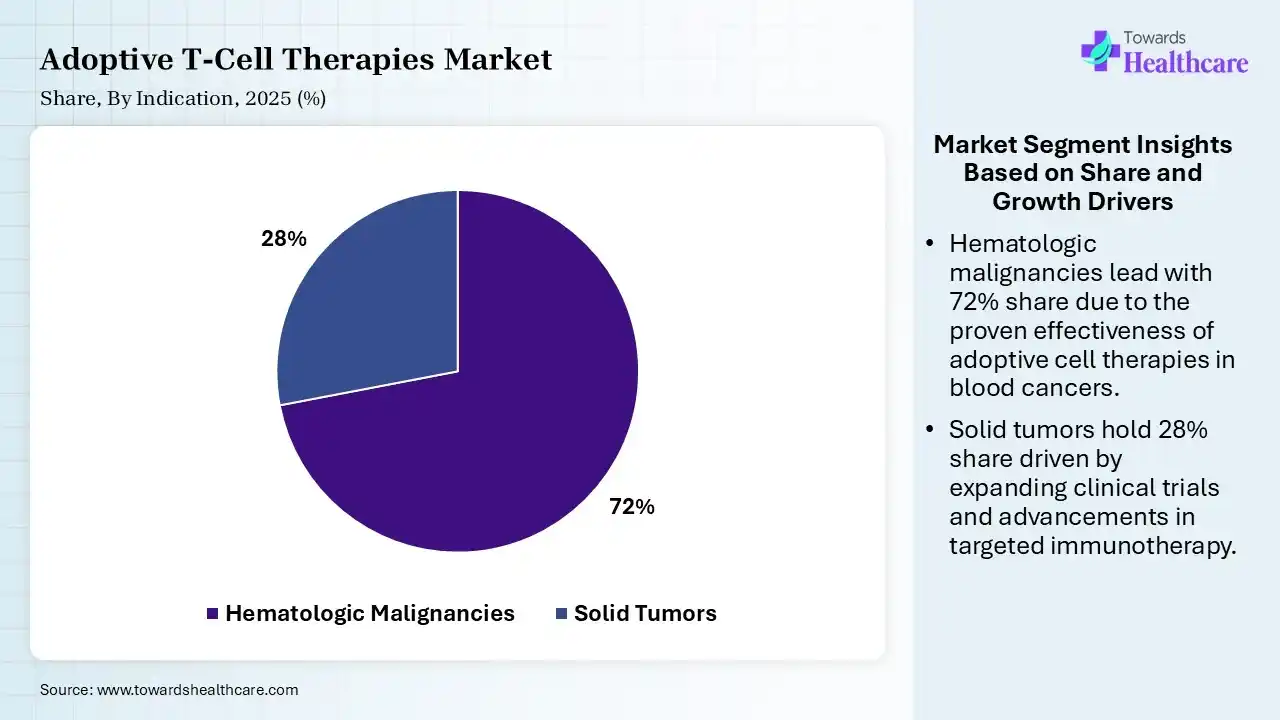

| Segment | Share 2025 (%) |

| Hematologic Malignancies | 72% |

| Solid Tumors | 28% |

The Hematologic Malignancies Segment Dominated the Adoptive T-Cell Therapies Market With 72% in 2025

The hematologic malignancies segment held a major revenue share of 72% of the market in 2025, as the majority of commercial therapies address blood cancers. Favorable clinical outcomes also supported widespread adoption of adoptive T-cell therapies. Expanding approvals also strengthened their demand.

The solid tumors segment held the second-largest share of 28% of the market in 2025 and is expected to expand rapidly with a CAGR of 24.70% during the forecast period, driven by intensive research addressing unmet needs. Improved cell engineering is also enhancing the efficacy of adoptive T-cell therapies. Expanding clinical trials also accelerate their adoption.

")

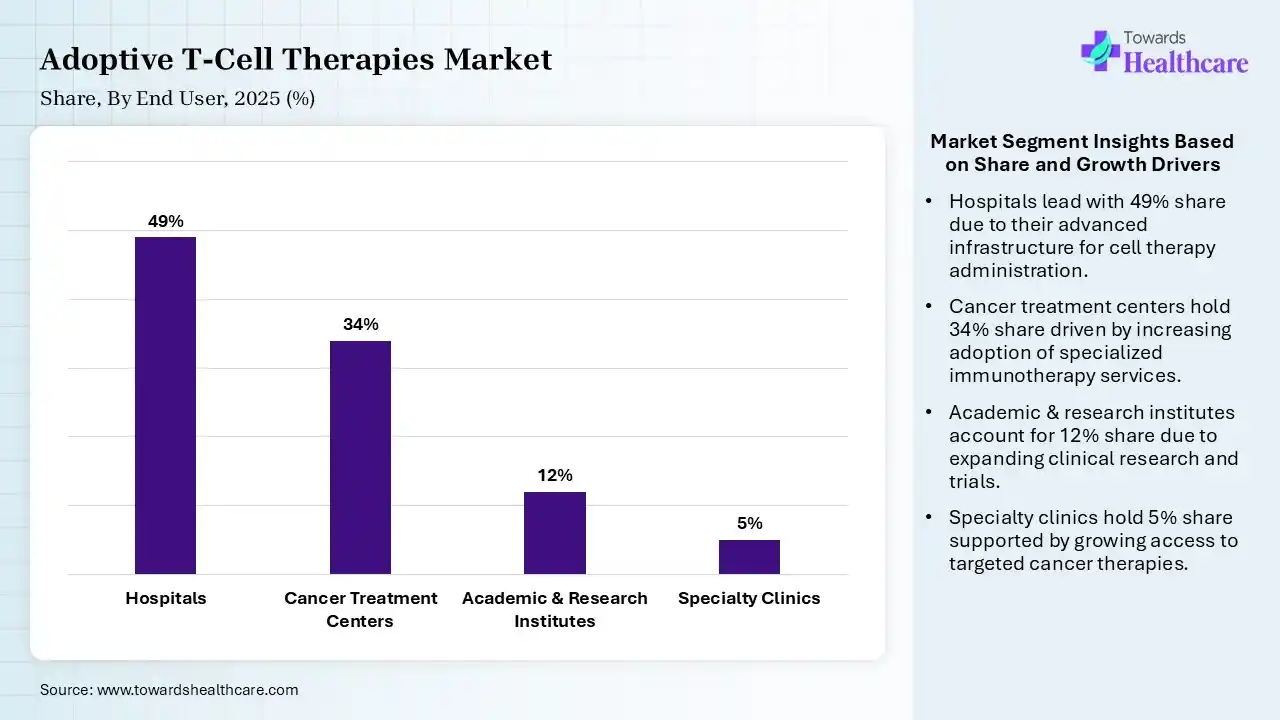

| Segment | Share 2025 (%) |

| Hospitals | 49% |

| Cancer Treatment Centers | 34% |

| Academic & Research Institutes | 12% |

| Specialty Clinics | 5% |

The Hospitals Segment Dominated the Adoptive T-Cell Therapies Market With 49% in 2025

The hospitals segment contributed the biggest revenue share of 49% of the market in 2025, driven by advanced infrastructure, which supported adoptive T-cell therapies administration. Multidisciplinary oncology teams improved outcomes. Reimbursement systems favored hospital delivery.

The cancer treatment centers segment held the second-largest share of 34% of the market in 2025 and is expected to gain the highest share with a CAGR of 21.6% during the forecast period, due to specialized expertise increasing patient referrals. Dedicated cell therapy units improve efficiency, increasing their use. Expanding treatment capacity also drives their growth.

The academic & research institutes segment held 12% of the adoptive T-cell therapies market share in 2025, driven by early-stage trials supporting innovation. Government grants are expanding research activities. Academic-industry partnerships are also strengthening adoptive T-cell therapies development.

The specialty clinics segment held 5% of the market share in 2025, due to growing outpatient care supporting expansion. Better patient monitoring also improves outcomes. Increasing specialist availability also boosts adoptive T-cell therapies utilization.

")

")

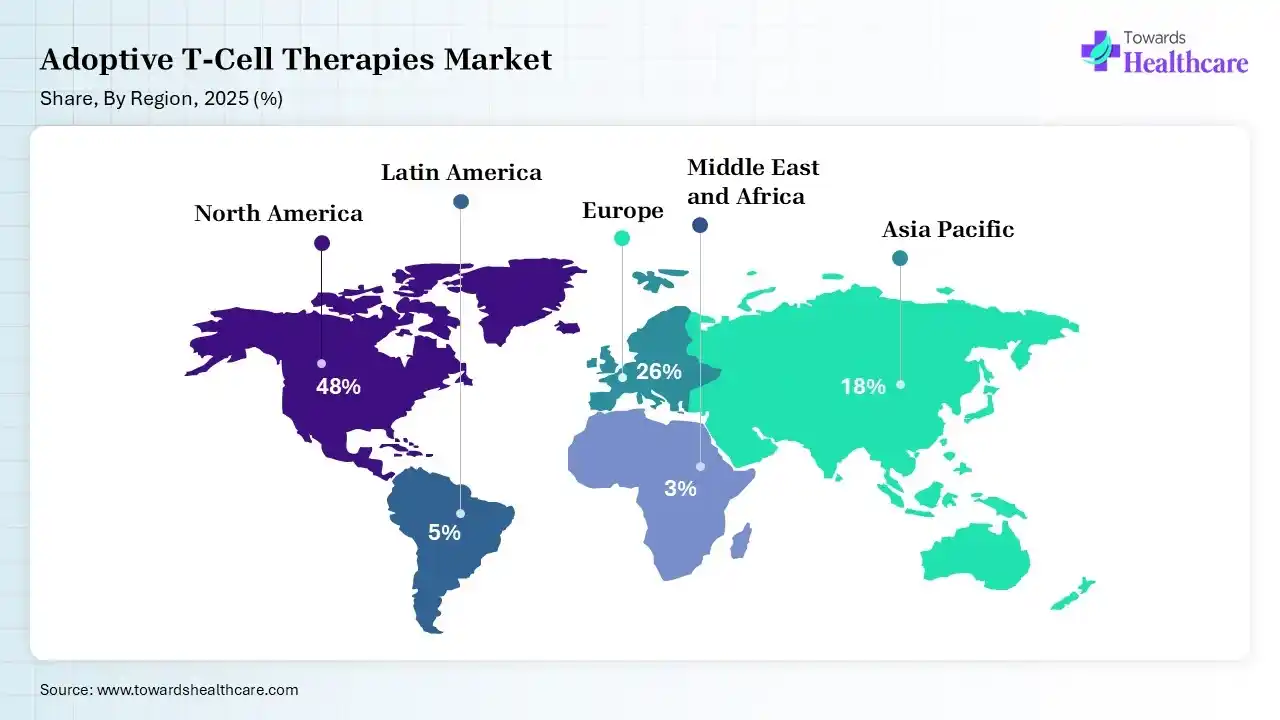

North America dominated the market with 48% in 2025, due to the largest commercial market with strong reimbursement. A high number of approved therapies also supported demand, where significant R&D investments accelerated innovation. Growth in regulatory support also accelerated clinical trials, which encouraged the development of new adoptive T-cell therapies, where growth in the incidence of cancer cases also increased their use. The presence of well-developed healthcare infrastructure also increased their adoption, which contributed to the market growth.

US Market Growth

U.S. held a 42% share of the adoptive T-cell therapies market in 2025, driven by an extensive clinical pipeline. Strong regulatory support and the presence of a leading biotechnology ecosystem also increased the development of adoptive T-cell therapies. Growth in investments and cancer burden also increased innovations and demand, where advancements in healthcare infrastructure and institutes also promoted these advancements. Presence of cutting-edge technologies also accelerated the development of next-generation adoptive T-cell therapies.

Mexico Market Growth

Mexico held a 2% share in the adoptive T-cell therapies market in 2025 and is expected to grow with the highest CAGR of 19.30% during the studied years, due to rapid healthcare modernization increasing access to adoptive T-cell therapies. Growing clinical collaborations are also expanding their availability, while growing oncology investments are also supporting their advancements. A rise in health awareness is also driving the demand for precision medicines, where expanding government support is also increasing their accessibility.

Europe held a 26% share of the market and is expected to grow significantly during the forecast period, due to growing reimbursement coverage supporting commercialization. Advanced healthcare infrastructure also improves accessibility to adoptive T-cell therapies, where increasing regulatory approvals also drive their demand. The presence of well-established biotechnology and pharmaceutical companies is also increasing their innovations, where a rise in investments is also supporting their expansion. Moreover, growing cancer treatment centres and cancer burden are also increasing their adoption, enhancing the market growth.

Germany Market Growth

Germany held a 7% share in the adoptive T-cell therapies market in 2025, driven by strong oncology infrastructure. High research investment and broad hospital adoption also increased the demand for adoptive T-cell therapies. Well-established research institutes and companies supported by government funding also accelerated the development of these therapies. At the same time, growth in strategic collaboration and cancer cases also contributed to the growth of the development of personalized therapies.

The rest of Europe held a 5% share in the adoptive T-cell therapies market in 2025 and is expected to witness the fastest growth with a CAGR of 19.20% over the forecast period, due to continuous regional expansion. Rising healthcare investments and improving cell therapy infrastructure are also driving the adoption of adoptive T-cell therapies. Growing health awareness and cancer prevalence are also driving their demand, where expanding clinical trials and collaborations are also supporting their innovations. Increasing government support is also supporting their innovations and adoption rates.

Asia Pacific held a 18% share of the market in 2025 and is expected to grow at the fastest CAGR of 24.10% during the forecast period, due to a large patient population, which supports a rise in demand. Rapid biotechnology investments are also accelerating innovation, while growing government initiatives strengthen manufacturing capabilities. Expanding healthcare infrastructure and clinical trials are also increasing their adoption rates, where growing awareness is also promoting their use. Increasing healthcare expenditures and manufacturing capabilities are also driving their advancements, promoting market growth.

China Market Growth

China held a 7% share of the adoptive T-cell therapies market in 2025, driven by an extensive CAR-T pipeline. Strong domestic manufacturing and favorable regulatory reforms also enhanced the adoption rates of adoptive T-cell therapies. A large cancer patient population also increased their use, where growth in clinical activities also increased patient innovations. Growth in collaboration and manufacturing capabilities also accelerated their development and commercialization. Regulatory support and high healthcare investments also enhanced their expansion.

India Market Growth

India held a 2% share in the adoptive T-cell therapies market in 2025 and is expected to expand rapidly with a CAGR of 26% in the coming years, due to growing local CAR-T commercialization. Rising healthcare investment and expanding cost-effective manufacturing capabilities are also driving their rapid production. Growing health awareness and government initiatives are also increasing their demand and accessibility, where a rise in the cancer population is also driving the demand for personalized therapies. Rapid expansion of healthcare infrastructure is also supporting the adoption of advanced cancer treatment options.

Latin America held a 5% share in the market in 2025 and is expected to show lucrative growth during the forecast period, due to improving cancer care infrastructure. Rising healthcare investment also supports the adoption of adoptive T-cell therapies, where growing clinical collaborations also expand their access. The growing cancer burden is also driving a shift towards emerging therapies, where healthcare expenditure is promoting the development of next-generation adoptive T-cell therapies. A rise in government support and favourable regulatory frameworks are also propelling the market expansion.

Brazil Market Growth

Brazil held a 2.50% share in the adoptive T-cell therapies market in 2025 and is expected to gain the highest market share with a CAGR of 20.50% during the forecast period, driven by the largest regional oncology market. Growth in the biotechnology ecosystem and clinical trials also increased the launch of new adoptive T-cell therapies. Expansion of healthcare infrastructure, government support, and healthcare expenditure also increased their availability; where growth in collaboration led to a rise in CAR-T cell therapies innovations. Large patient volume also contributed to their increased adoption rates.

The rest of Latin America held a 1.50% share in the adoptive T-cell therapies market in 2025, due to continuous regional healthcare modernization. Improving access to advanced therapies is also driving the adoption of adoptive T-cell therapies, where expanding international collaborations are fueling their advancements. Increasing cancer burden and healthcare investments are propelling the development of new adoptive T-cell therapies, while rises in specialized cancer centres are increasing their adoption. Growing government initiatives are also supporting their innovations.

MEA held a 3% share in the market in 2025 and is expected to show notable growth during the forecast period, due to increasing government investment in oncology. Specialized hospitals are expanding their services, and a rise in international partnerships also improves accessibility of adoptive T-cell therapies. Growing adoption of immunotherapies, personalized therapies, and precision medicine is also encouraging their usage, where increasing cancer incidences are also fueling their demand. Improving regulatory frameworks and expanding industries are also actively participating in market expansion.

Suadi Arabia Market Growth

Saudi Arabia held a 1% share in the adoptive T-cell therapies market in 2025, driven by a rise in vision-driven healthcare investment. Oncology capacity expansion also increased the adoption of adoptive T-cell therapies, where growth in precision medicine initiatives also increased their demand. A rise in cancer treatment centres also increased their use, where a shift towards personalised therapies promoted their innovations. Growth in government initiatives and investments also expanded collaboration, leading to a rise in next-generation adoptive T-cell therapies launches.

Rest of MEA held a 0.7% share in the adoptive T-cell therapies market in 2025 and is expected to show the fastest growth with a CAGR of 20.50% over the forecast period, due to healthcare modernization, which supports adoption of adoptive T-cell therapies. Regional oncology program expansion and increasing cell therapy awareness are also driving their advancements. Increasing healthcare investments are also fueling their innovations, where rising collaborations are also supporting their expansion. A rise in patient population is also increasing their adoption rates, where favourable government support is increasing their accessibility.

| Companies | Headquarters | Solutions |

| Gilead Sciences | Foster City, U.S. | Yescarta and Tecartus |

| Johnson & Johnson | New Brunswick, U.S. | Carvykti |

| Bristol Myers Squibb | New York, U.S. | Breyanzi and Abecma |

| Novartis AG | Basel, Switzerland | Kymriah |

| Iovance Biotherapeutics | Califronia, U.S. | Amtagvi |

In April 2026, after the announcement of a definitive agreement between Eli Lilly and Company and Kelonia Therapeutics, Executive Vice President and President of Lilly Oncology, Jacob Van Naarden, stated that "Autologous CAR-T therapies have meaningfully improved outcomes for patients with various cancers, but significant manufacturing, safety, and access barriers mean that only a fraction of eligible patients actually receive them. Kelonia's in vivo platform has the potential to change that by delivering rapid, durable responses in a far simpler, off-the-shelf format."

| Company | Recent Product Launches | Recent Partnerships and Collaborations | Manufacturing Expansion Strategies |

| Gilead Sciences | Anito-Cel | Definitive agreement to acquire Arcellx | $32 billion U.S. investment to redefine its role in the biopharmaceutical industry |

| Bristol Myers Squibb | Breyanzi | Acquisition of Orbital Therapeutics | $40 billion in the U.S. to expand its research and manufacturing presence |

| Johnson & Johnson | Carvykti | Contract manufacturing collaboration with Novartis | $1 billion investment in a next-generation cell therapy manufacturing facility |

| Company Overview | Financial Performance | Product Portfolio | R&D Pipeline | Recent Strategic Developments |

| Novartis AG | Net sales FY 2025: 54532 USDm2 | Kymirah | AAA601, AAA614, AAA603, AAA617, AAA817 and ABL701 | Agreement to acquire Myricx Bio |

| Iovance Biotherapeutics | Full year 2025 total product revenue of ~$264 million | Mtagvi | IOV-3001 | Cooperative Research and Development Agreement (CRADA) with Dr. Steven Rosenberg |

| Autolus Therapeutics | Net product revenue of $23.3 million | Aucatzyl | AUTO8, AUTO9 | Autolus signed a strategic CAR T cell therapy collaboration with BioNTech |

Revenue Forecast Through 2035

Growth in cancer burden, investment, collaboration, and technological advancements will drive market expansion and future growth trajectory

Future Technology Roadmap

Growth in the development of next-generation innovations likely to shape the industry expansion.

Emerging Business Models

Rise in the demand for decentralized manufacturing, platform technologies, and service-based opportunities will drive new opportunities.

Long-Term Strategic Opportunities

The high-growth investment areas, underserved markets, and innovation hotspots are likely to sustain their standing for a long period of time.

Recommendations for Biotechnology Companies

Growth in the use of adoptive T-cell therapies will offer strategic priorities for product development and commercialization.

Recommendations for Investors

The market growth will lead to attractive investment themes, emerging technologies, and risk considerations.

Recommendations for Healthcare Providers

Rapid expansion of infrastructure development, treatment capacity, and patient access strategies will drive the demand for adoptive T-cell therapies.

Recommendations for Policymakers and Regulators

The growing clinical activities will improve regulatory efficiency, reimbursement, and innovation support.

By Therapy Type

By Antigen Target

By Indication

By End User

By Source

By Target Population

By Manufacturing Type

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar