Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

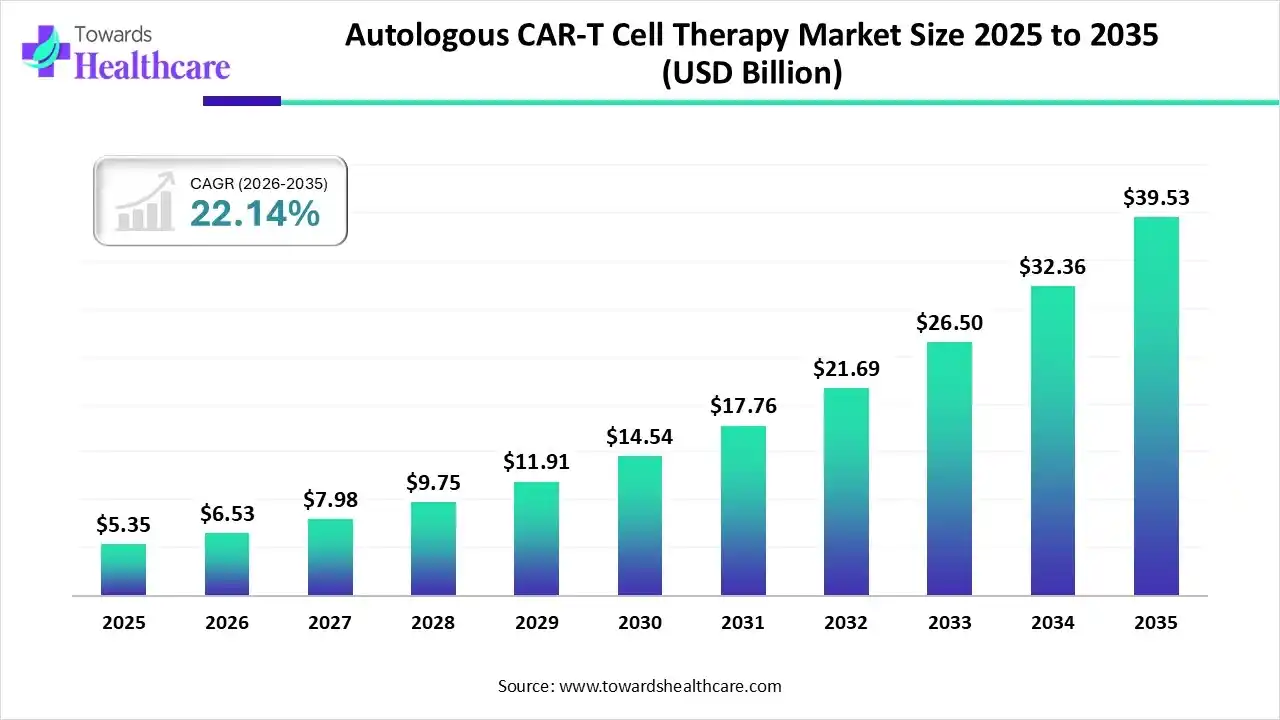

The global autologous CAR-T cell therapy market size was estimated at USD 5.35 billion in 2025 and is predicted to increase from USD 6.53 billion in 2026 to approximately USD 39.53 billion by 2035, expanding at a CAGR of 22.14% from 2026 to 2035.

The growing incidence of cancer globally is increasing the demand for autologous CAR-T cell therapies. This is driving their innovations, development, AI integration, and launches, promoting market growth.

The autologous CAR-T cell therapy market is driven by increasing hematologic malignancies and expanding regulatory approvals. The autologous CAR-T cell therapy refers to the cancer immunotherapy, developed by genetically modifying the patient's T-cells to identify and target the cancer cells in the body. These therapies are being used in the treatment of different types of hematologic cancers.

There is a rise in the use of AI in the autologous CAR-T cell therapy market for the identification of the target, which helps in the development of these therapies with target-specific action. They also help in the optimization, manufacturing, and designing of next-generation therapies. It is also being used for the management of their toxicity and dosage, to enhance their safety and efficacy.

Expanding Applications

Due to the proven efficacy of the autologous CAR-T cell therapies in the treatment of hematologic cancer, their application in the treatment of other cancer types is increasing, promoting their R&D activities.

Growing Technological Advancements

Different types of automated and closed system bioreactors are being developed, which are enhancing the manufacturing process of the autologous CAR-T cell therapies, enhancing their production rates.

Blooming Innovations

The companies are focusing on the development of autologous CAR-T cell therapies with enhanced safety and efficacy, as well as developing novel drug delivery technologies, to enhance their target-specific action.

| Key Elements | Scope |

| Market Size in 2026 | USD 6.53 Billion |

| Projected Market Size in 2035 | USD 39.53 Billion |

| CAGR (2026 - 2035) | 22.14% |

| Leading Region | North America by 43% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By End-Use, By Therapy Development Phase, By Region |

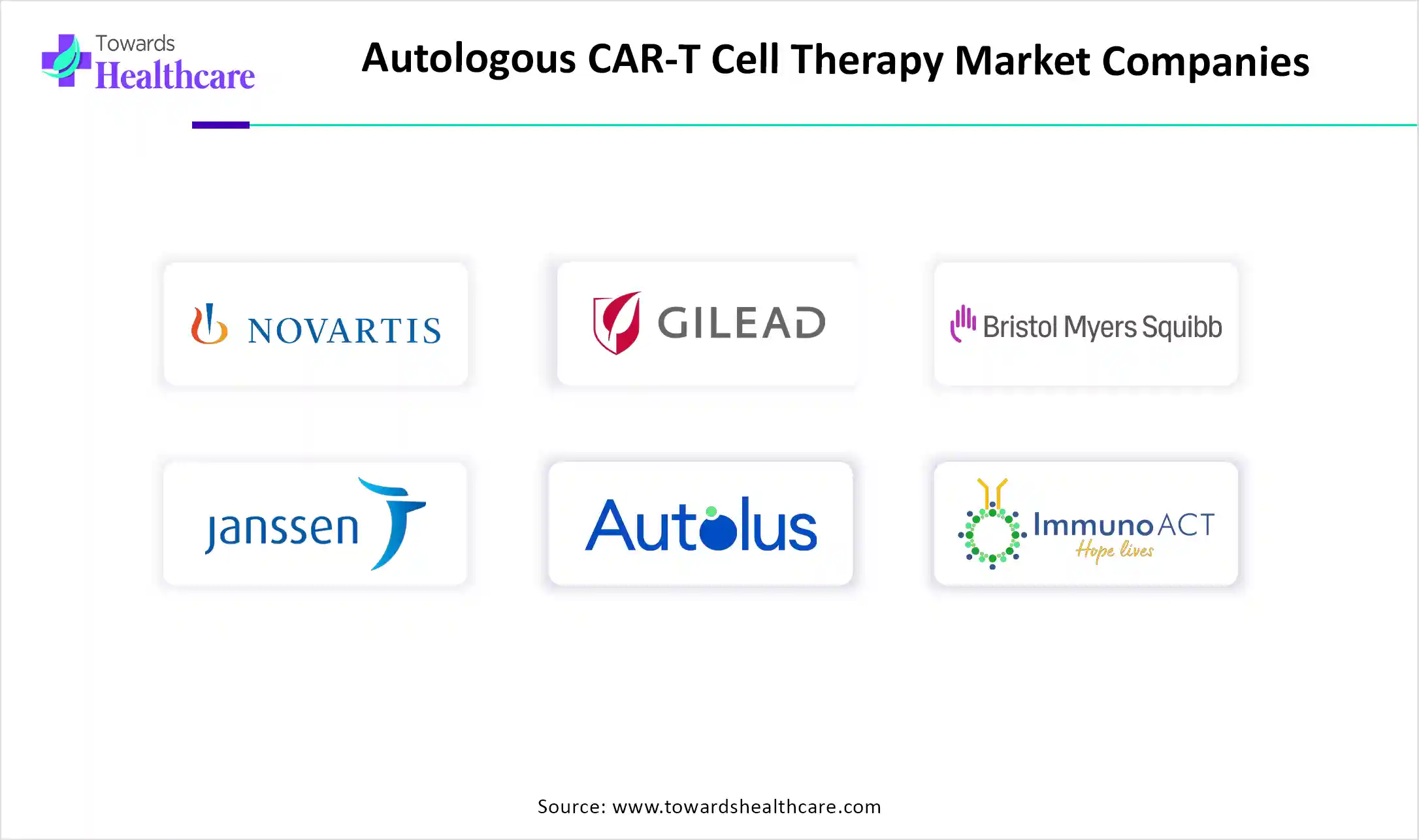

| Top Key Players | Novartis, Gilead Sciences, Bristol Myers Squibb, Janssen, Autolus Therapeutics, ImmunoACT, Legend Biotech, CARsgen Therapeutics, JW Therapeutics, bluebird bio |

| Segments | Shares % |

| CD19-Directed CAR-T Cell Therapy | 52% |

| BCMA-Directed CAR-T Cell Therapy | 30% |

| Other Antigen-Directed CAR-T Cell Therapy | 18% |

Why Did the CD19-Directed CAR-T Cell Therapy Segment Dominate in the Market in 2025?

The CD19-directed CAR-T cell therapy segment led the autologous CAR-T cell therapy market by 52% share in 2025, due to its targeting specific action on B-cell leukemias. Their enhanced success rates also increase their use, where the growth in the patient volume also increases their demand and adoption rates.

BCMA-Directed CAR-T Cell Therapy

The BCMA-directed CAR-T cell therapy segment is expected to show the highest growth during the upcoming years, due to its growing success rates. Additionally, increasing interest in multiple myeloma treatment is also increasing their use and innovations, where their growing pipeline is also driving their demand.

| Segments | Shares % |

| Acute Lymphoblastic Leukemia | 30% |

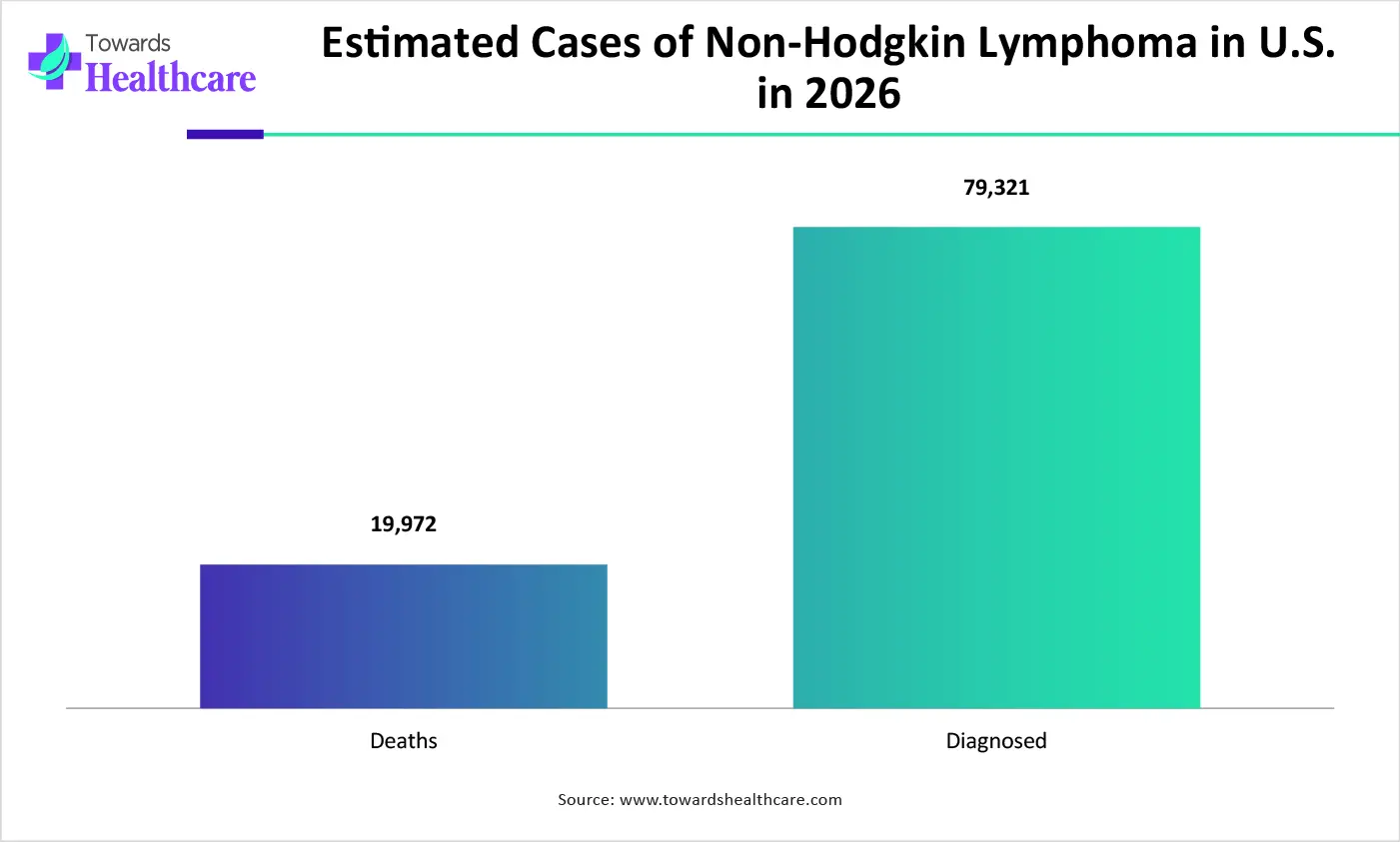

| Non-Hodgkin Lymphoma | 26% |

| Multiple Myeloma | 18% |

| Chronic Lymphocytic Leukemia | 14% |

| Other Hematologic Malignancies | 12% |

How Acute Lymphoblastic Leukemia Segment Dominated the Market in 2025?

The acute lymphoblastic leukemia segment held the dominating share in the autologous CAR-T cell therapy market by 30% share in 2025, driven by the proven success rates of the autologous CAR-T cell therapies. Moreover, their target-specific action on CD19 expression and increased approvals also enhanced their use.

Chronic Lymphocytic Leukemia

The chronic lymphocytic leukemia segment is expected to show rapid growth during the upcoming years, due to growing incidence rates. This is increasing the use of autologous CAR-T cell therapies, where their expanding pipeline and the development of combination therapies are also increasing their acceptance rates.

| Segments | Shares % |

| Hospitals | 58% |

| Specialty Clinics | 27% |

| Research Institutes | 15% |

What Made Hospitals the Dominant Segment in the Market in 2025?

The hospitals segment led the autologous CAR-T cell therapy market by 58% share in 2025, due to growth in patient volumes. The presence of well-developed infrastructure and reimbursement policies also attracted the patients. Moreover, they also offered continuous monitoring and compliance with regulatory standards, which increased the patient outcomes.

Specialty Clinics

The specialty clinics segment is expected to show the highest growth during the predicted time, due to the growing number of outpatients. At the same time, they also offered affordable and advanced autologous CAR-T cell therapies, which attracted the patients. Additionally, flexible scheduling and skilled personnel are also increasing their preference.

| Segments | Shares % |

| Preclinical | 34% |

| Phase I | 18% |

| Phase II | 20% |

| Phase III | 14% |

| Approved | 14% |

Which Therapy Development Phase Type Segment Dominated the Market in 2025?

The preclinical segment held the dominating share in the autologous CAR-T cell therapy market by 34% share in 2025, due to growth in the autologous CAR-T cell candidates. The growth in the R&D activities in institutes and industries also increased their participation in this phase to evaluate the product's safety, applications, and efficacy.

Phase II

The phase II segment is expected to show rapid growth during the predicted time, due to the rapid expansion of the autologous CAR-T cell therapy pipeline. The companies are actively participating in this phase to enhance and accelerate the launch of their products with different types of applications.

North America dominated the autologous CAR-T cell therapy market by 43% share in 2025, due to the presence of a well-developed R&D infrastructure. This increased the development and innovations of the autologous CAR-T cell therapies, along with their early adoption. Moreover, the presence of advanced healthcare systems also increased their adoption and approval rates, which contributed to the market growth.

U.S. Market Trends

The presence of advanced industries and healthcare in the U.S. is increasing the development of autologous CAR-T cell therapies. The growing healthcare investments and expanding applications are also increasing their innovations, where the faster approval rates are also encouraging their advancements.

Asia Pacific is expected to host the fastest-growing autologous CAR-T cell therapy market by 20% share during the forecast period, due to the growth in cancer cases. The expanding healthcare sector is also increasing the adoption of advanced treatment options, like autologous CAR-T cell therapies. Furthermore, growing government support and increasing R&D activities are also enhancing their innovations, promoting market growth.

China Market Trends

Due to the presence of a large population, there is an increase in the number of patients with lymphoma, leukaemia, and myeloma in China, which is increasing the use of autologous CAR-T cell therapies. Moreover, the expanding biotechnology ecosystem and its application are also increasing their development, which is backed by new investments.

Europe is expected to grow significantly in the autologous CAR-T cell therapy market by 26% share during the forecast period, due to the presence of advanced industries and the healthcare sector. This is increasing their production, innovations, and availability, enhancing their adoption rates. Additionally, growing health awareness is also increasing their demand, enhancing the market growth.

UK Market Trends

The UK consists of well-developed healthcare systems, which increases the use of autologous CAR-T cell therapies for the treatment of growing cases of lymphoma. The presence of reimbursement policies is also increasing their use and accessibility, which is increasing R&D activities, driving their innovations.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Autologous CAR-T Cell Therapies |

| Novartis | Basel, Switzerland | Kymriah |

| Gilead Sciences | California, U.S. | Tecartus and Yescarta |

| Bristol Myers Squibb | New Jersey, U.S. | Abecma and Breyanzi |

| Janssen | New Jersey, U.S. | Carvykti |

| Autolus Therapeutics | London, UK | Aucatzyl |

| ImmunoACT | Navi Mumbai, India | NexCAR19 |

| Legend Biotech | New Jersey, U.S. | Carvykti |

| CARsgen Therapeutics | Shanghai, China | Zenvorcabtagene autoleucel |

| JW Therapeutics | Shanghai, China | Relmacabtagene autoleucel |

| bluebird bio | Massachusetts, U.S. | Abecma |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Application

By End-Use

By Therapy Development Phase

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar