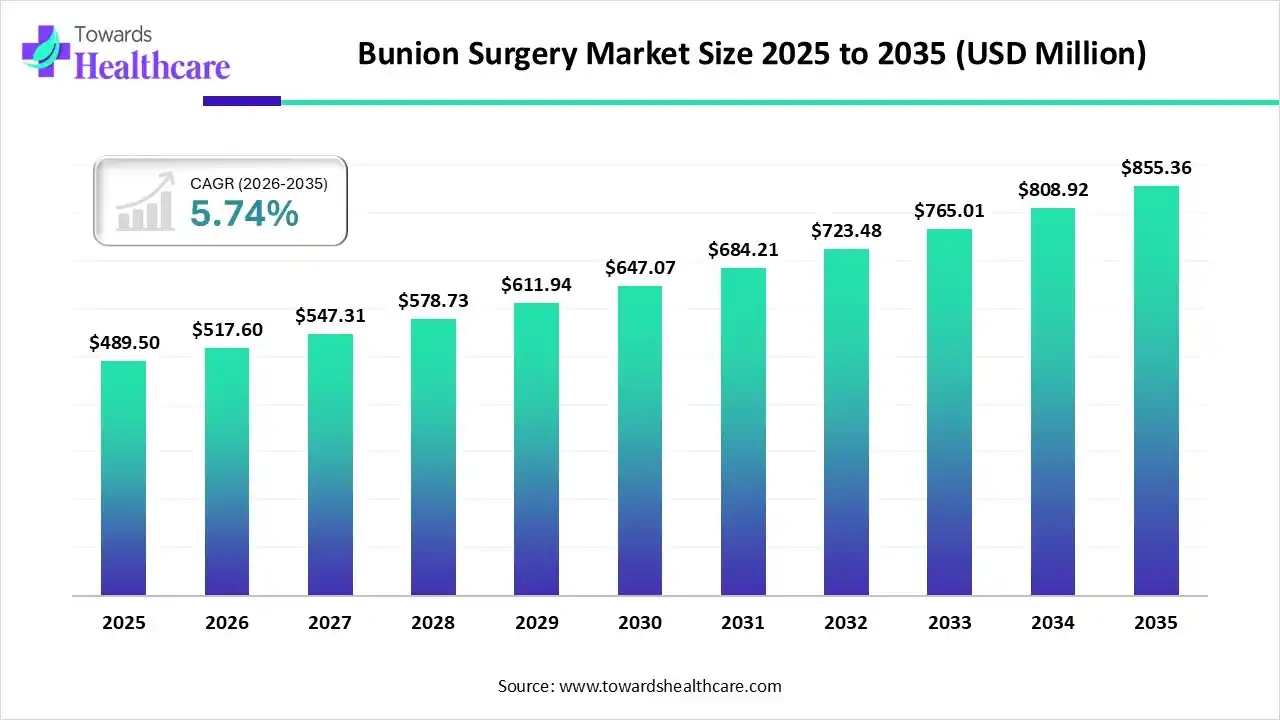

The global bunion surgery market size was estimated at USD 489.5 million in 2025 and is predicted to increase from USD 517.6 million in 2026 to approximately USD 855.36 million by 2035, expanding at a CAGR of 5.74% from 2026 to 2035.

Globally rising cases of the geriatric population, sports injuries, and other associated incidences, such as arthritis. For these cases, the healthcare professionals are fostering rigorous solutions, like minimally invasive surgery, and advanced AI-powered approaches.

Firstly, the bunion surgery market covers a procedure that corrects a hallux valgus deformity, i.e. a bony bump at the base of the big toe. This significant procedure and overall market expansion are driven by a rise in the geriatric population, accelerating bunion cases, which are associated with footwear/lifestyle/sports, and ongoing breakthroughs in implants and minimally invasive techniques (MIS). However, healthcare professionals are leveraging 3D surgical planning and correction, such as Lapiplasty, which considers the bunion as a 3D deformity by correcting the unstable joint at the base of the big toe instead of just removing the visible bump.

Furthermore, the expansion of the bunion surgery market is significantly propelled by the increasing prevalence of hallux valgus among aging demographics and the growing preference for outpatient procedures in ambulatory surgical centers. Patients increasingly seek out advanced, specialized implants, such as titanium plates and bioresorbable screws, that promise reduced recovery times and a lower risk of bunion recurrence. Additionally, rising disposable incomes, expanded healthcare coverage, and extensive awareness campaigns regarding the long-term benefits of early orthopedic intervention are accelerating adoption rates globally.

The respective market has been bolstering the adoption of AI algorithms through the strengthening of pre-operative planning software, patient-matched surgical guides, and robotic assistance, which ensures higher precision and potentially rapid recovery times. Recently, Johnson & Johnson MedTech introduced the VIRTUGUIDE system. This patient-matched solution utilises AI software for the selection of the most appropriate, patient-specific Virtual Alignment and Correction (VAC) Guide for a Lapidus procedure (a type of bunion surgery).

Exploration of Tailored Surgical Planning & Implants

The era is increasingly demanding for customized solutions, including the development of 3D models for surgeons to practice and establish patient-specific surgical guides or implants.

Spurring Fourth-Generation MIS

Innovative methods, such as extra-articular transverse osteotomies, are allowing multi-directional correction with stable fixation.

Shifting Towards Robotic Assistance

The globe is immensely stepping into the promotion of robotic-assisted surgery, which enables more intricate movements with raised precision, potentially resulting in minimal complications.

| Key Elements | Scope |

| Market Size in 2026 | USD 517.6 Million |

| Projected Market Size in 2035 | USD 855.36 Million |

| CAGR (2026 - 2035) | 5.74% |

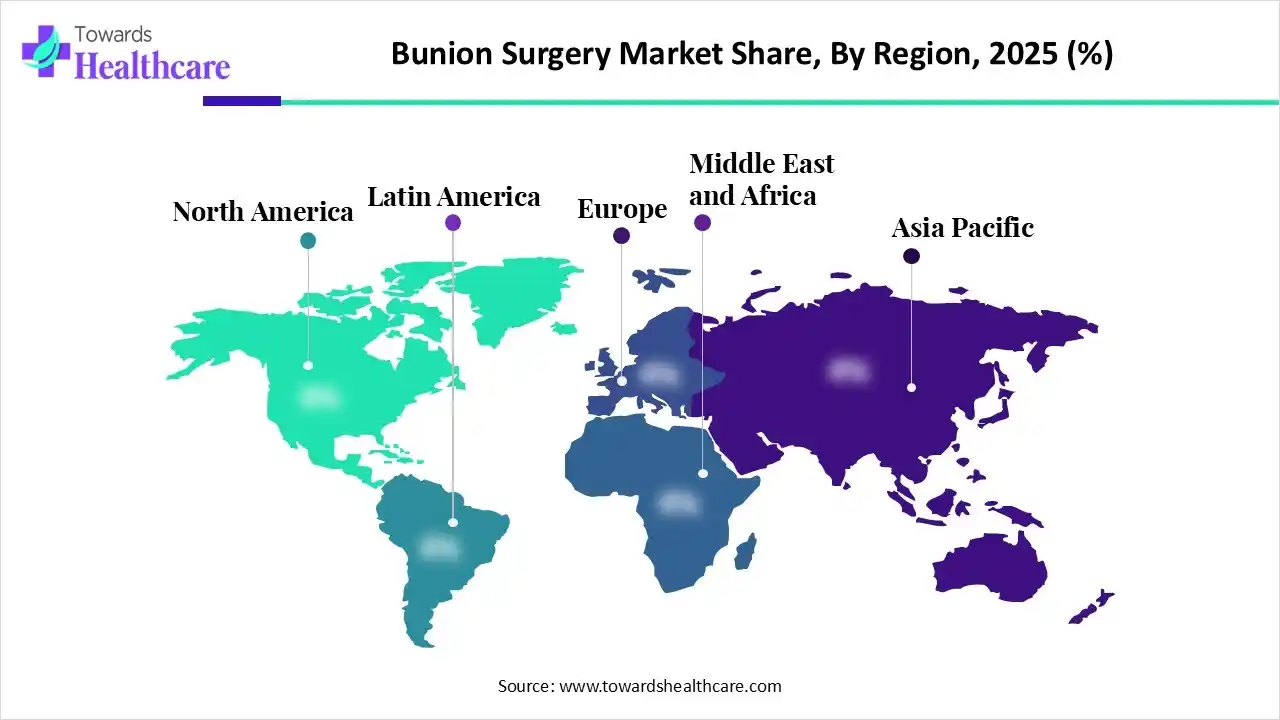

| Leading Region | North America by 45% |

| Key Applications | Bunion correction, hallux valgus reconstruction, osteotomy procedures, Lapidus procedures, minimally invasive bunion surgery (MIS), foot realignment surgery |

| Primary End Users | Hospitals, Ambulatory Surgery Centers (ASCs), Orthopedic Clinics, Podiatric Surgery Centers |

| Key Growth Drivers | Rising bunion prevalence, aging population, increasing adoption of minimally invasive surgery, improved fixation implants, faster recovery technologies |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Patient Type, By Surgery Type, By End-User, By Region |

| Top Key Players | Stryker Corporation, Johnson & Johnson Services, Inc., Zimmer Biomet Holdings, Inc., Smith & Nephew plc, Paragon 28, Inc., CONMED Corporation, Enovis Corporation, Medartis AG, Orthofix Medical Inc, Exactech, Inc. |

| Segments | Shares % |

| Correction Systems | 60% |

| Implants & Accessories | 40% |

Which Product Type Led the Bunion Surgery Market in 2025?

In 2025, the correction systems segment captured the dominating share of 60% of the market. It has significant advantages, like highlighting the root cause of the deformity, enhanced stability, quicker recovery, and a reduced chance of the bunion returning. Globally rising adoption of Lapiplasty procedures, which leverages specialized, single or dual low-profile titanium plates for accurate rotation and stabilization of the first metatarsal bone into its correct anatomical position. The latest advanced Percuplasty Percutaneous 3D bunions correction system facilitates precise 3D correction with cosmetically appealing incisions.

Implants & Accessories

Moreover, the implants & accessories segment is anticipated to expand fastest. Instead of traditional implants, surgeons are encouraging "smart" implants coupled with sensors to transmit real-time data on mechanical stress, movement, and healing growth. The market is transforming utilization of biomaterials, especially magnesium alloys, which are naturally dissolvable in the body after the bone has healed, and also combats the need for a second hardware removal surgery.

| Segments | Shares % |

| Adults patients | 70% |

| Pediatric patients | 30% |

How did the Adults Patients Segment Dominate the Bunion Surgery Market in 2025?

Primarily, the adults patients segment held the biggest share of 70% of the market in 2025. Specifically, 18-65+ aged people are suffering from bunions, which is fueled by diverse lifestyle factors, sports injuries, joint degeneration and age-related conditions, including arthritis. However, they are broadly demanding advanced minimally invasive techniques, sophisticated fixation devices, and the use of robotic-assisted technology.

")

Pediatric Patients

The pediatric patients segment will expand notably. The worldwide increase in congenital/developmental concerns, sports injuries, improper footwear, and rising awareness are propelling the growth of bunion surgery. A key solution comprises a transverse extra-articular metatarsal osteotomy using two cannulated screws united with an Akin osteotomy. Whereas, DePuy Synthes unveiled the TriLEAP Lower Extremity Anatomic Plating System for bunionectomies and osteotomies in complex pediatric foot fractures and deformities.

| Segments | Shares % |

| Traditional Surgery | 60% |

| Minimally Invasive Surgery | 40% |

Which Surgery Type Led the Bunion Surgery Market in 2025?

In 2025, the traditional surgery segment registered dominance in the market by 60% share. This surgical type is well-developed and widely successful for correcting severe or complex bunion deformities where MIS might not satisfy. This often includes an osteotomy, which needs a larger incision (inches long) to access the joint, discard the bony prominence, i.e. exostectomy, and reposition the misaligned bones.

Minimally Invasive Surgery

Whereas the minimally invasive surgery segment is predicted to witness rapid expansion. Modernized MIS emphasises raising precision, boosting recovery, and lowering recurrence rates through sophisticated instrumentation, 3D planning technologies, and refined surgical methods. The leading firms are putting efforts into progressing procedure-specific hardware and tools, like the PROstep MIS Lapidus by Stryker, and specialized burrs, which accelerate the safety and efficiency of minimally invasive procedures.

| Segments | Shares % |

| Hospitals | 55% |

| Orthopaedic Clinics | 30% |

| Ambulatory Surgical Centers | 10% |

| Others | 5% |

Why did the Hospitals Segment Lead the Market in 2025?

The hospitals segment captured the largest share of the bunion surgery market by 55% share in 2025. These are prominent end-users, which provide skilled surgeons and the availability of different techniques, such as exostectomy, osteotomy, and arthrodesis for correction. Alongside, they are focusing on improvements in post-operative care, with the adoption of multimodal pain management and strengthened rehabilitation programs that support early mobilization.

Orthopaedic Clinics

In the future, the orthopaedic clinics segment is anticipated to expand at a rapid CAGR. A rise in the burden of deformities, demand for better outcomes, and broadening awareness are assisting the expansion of these clinics. Additionally, clinics are fostering the use of next-gen implants, surgical tools, and AI-driven strategies. Also, they are shifting towards a single, dual-zone neutral pitch screw construct, which offers extensive stability for healing, with a streamlined procedure.

")

North America held the largest share of 45% of the market in 2025, due to the ongoing breakthrough in surgical techniques, such as MIS, robust implants, and escalating instances of related issues, especially arthritis. Furthermore, the region is embedding novel "same-day" protocols that often enable patients to initiate gentle range-of-motion exercises within days and return to light activity in 4–6 weeks.

U.S. Market Trends

However, the U.S. was a major contributor to the market, as it is promoting cloud-driven platforms and pre-operative software, for example, Johnson & Johnson's Virtue Guide system, which is employed in digital planning of surgeries and monitoring post-operative progress, ultimately allowing tailored care and raising patient involvement.

Canada Market Trends

In Canada, installment of bunion corrective surgeries has adapted favourably to the growing number of foot deformities, the number of aged individuals requiring assistance with their foot deformity, and the availability of orthopedic care. The prevalence of minimally invasive surgery options such as correctional devices, technology for faster recovery periods, and room for improvement in postoperative procedures has shown significant growth over the last few years in this area.

Mexico Market Trends

As a developing market for bunion corrective surgery, Mexico is expected to see continued growth due to an increase of health care facilities, the rising awareness of foot health, and greater accessibility to orthopedic care. The growing need for a correctional procedure to treat bunions, combined with modern and innovative surgical procedures provided by both public and private health care facilities, will add to the growth of the bunion surgery market in Mexico.

Asia Pacific is estimated to expand fastest in the bunion surgery market by 15% share, as the region is experiencing the expedited expansion of medical infrastructure, accelerating healthcare spending, primarily in Japan, South Korea, and Southeast Asia. Besides this, APAC is widening the use of AI in pre-operative evaluation and surgical planning. Whereas, AI-enabled solutions are exploring the analysis of patient-specific data from imaging to implement proper surgical techniques.

Japan Market Trends

Japan is predicted to expand at a rapid CAGR with substantial advancements in the surgical area. They have robust healthcare facilities, such as Foot Clinic Omotesando, The Clinical and Research Institute for Foot & Ankle Surgery, and Marugame Orthopedic Clinic. They are executing diverse approaches, particularly innovation in advanced, cutting-edge minimally invasive orthopedic treatments.

India Market Trends

Increasingly diagnosed hallux valgus has created additional demand for corrective foot surgery in India, leading to an expanding market for bunion surgery in that country. The growing number of patients who receive available orthopedic care, along with an increase in expenditures for health care services, and access to newer, advanced forms of surgery, is supporting future growth of the bunion corrective surgery market in India.

China Market Trends

Bunion surgical procedures are in high demand in China because of an increase in the elderly population and more research being done on foot deformities. Awareness about the potential to correct the conditions in your feet is increasing, and with more technology available to perform bunion surgery, there will continue to be a high demand for these types of procedures in the future.

The European bunion surgery market is growing share of 30% due to an aging population, rising prevalence of hallux valgus, and advancements in surgical techniques. Minimally invasive surgery (MIS) is gaining popularity for its smaller incisions, reduced tissue damage, less postoperative pain, and faster recovery. The shift towards outpatient procedures is accelerating this trend. As the population ages, orthopedic issues like hallux valgus increase, driving demand for surgery. Additionally, factors like rheumatoid arthritis, obesity, and poor footwear choices contribute to more foot deformities. New implant designs and robotic systems enhance surgical outcomes and reduce recurrence rates.

Germany Market Trends

Germany dominates the European market, generating the highest revenue due to its robust healthcare system, high prevalence of foot disorders, and a thriving medical tourism sector. The aging population and common foot deformities like hallux valgus increase the demand for surgical options. Renowned for its advanced medical facilities and high-quality orthopedic care, Germany has highly skilled, board-certified surgeons specializing in orthopedic surgeries. The country is also a hub for orthopedic innovation, offering specialized procedures such as Scarf osteotomy and minimally invasive Chevron-Akin techniques. Furthermore, Germany hosts numerous research institutions and prioritizes advanced implants and robotic-assisted technology, particularly in the rapidly growing implants and accessories sector, driven by innovations in titanium implants and corrective technologies.

Netherlands Market Trends

The Netherlands has continued to develop a strong demand for bunion correctional surgeries in its country due to the number of patients being treated who suffer from disorders associated with foot deformities and due to their general availability of health care services. Growth for bunion corrective surgery has seen an increase with the use of minimally invasive surgery methods and postoperative protocols in place to achieve optimal outcomes for the patient and to develop the bunion surgery market in the Netherlands.

U.K. Market Trends

In the UK there is an increased demand for bunion surgery because of a significant increase in the elderly population and people are becoming more aware of the availability of corrective surgeries for foot deformities. The increases of new minimally invasive techniques as well as more advanced surgical instruments are leading to better patient outcomes with improved access to orthopedic surgery.

South America is expanding in the bunion surgery market due to improved healthcare infrastructure, increased patient awareness of advanced treatments, and a rising demand for minimally invasive procedures (MIS). Post-pandemic, the region is seeing a surge in technology investments, a higher incidence of foot problems, and a growing need for specialized orthopedic care. The pandemic highlighted healthcare gaps, prompting a focus on enhancing hospital facilities, particularly in orthopedics. The popularity of advanced minimally invasive procedures, like endoscopic and robotic techniques, is driving market growth due to shorter hospital stays and better outcomes. Better access to healthcare and more specialized orthopedic centers, along with various surgical and non-invasive treatment options, are supporting this trend.

Brazil Market Trends

Brazil has established itself as a leader in the Latin American market, offering high-quality orthopedic care at lower prices than in North America or Europe. The country's prominence in minimally invasive surgical (MIS) techniques is driven by several key factors. Globally, Brazil is recognized for its expertise in specialized surgeries, particularly orthopedics, with internationally accredited hospitals featuring advanced technology in major cities like São Paulo and Rio de Janeiro. Brazil excels in percutaneous surgery for hallux valgus correction, with MIS techniques that involve smaller incisions, leading to quicker recovery, reduced postoperative pain, and earlier weight-bearing, making them attractive to patients. The Brazilian orthopedic implant market is supported by a strong domestic manufacturing sector, including companies like MDT, GMReis, and Baumer, which produce advanced, cost-effective, locally sourced implants.

Argentina Market Trends

Bunion surgery is becoming more available in Argentina due to an increase in orthopedic consultations and greater public awareness of having corrective surgery on their feet. In addition, as people age, they want to receive effective treatment for their bunions due to the pain associated with the condition as well as difficulty walking.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Treace Medical Concepts, Arthrex, Paragon 28 | Develop innovative bunion correction techniques and surgical technologies |

| Product Manufacturers | Stryker, Zimmer Biomet, DePuy Synthes, Smith+Nephew, Acumed | Manufacture implants, fixation systems, screws, plates, and surgical instruments |

| Service Providers | Hospital Systems, Orthopedic Centers, ASC Networks | Perform bunion correction procedures |

| Platform Providers | Treace Medical Concepts, Enovis, Paragon 28 | Offer integrated bunion correction platforms combining implants, instruments, and procedural workflows |

| CROs/CDMOs | Limited relevance | Bunion surgery is device-driven rather than CRO-dependent |

| Software Vendors | Enovis, Stryker, Zimmer Biomet | Surgical planning, imaging integration, and digital orthopedic workflow tools |

| Research Institutions | American Orthopaedic Foot & Ankle Society (AOFAS), Mayo Clinic, Hospital for Special Surgery | Clinical research and procedure advancement |

| End-User Industries | Hospitals, Ambulatory Surgery Centers, Orthopedic Surgery Practices | Primary adoption and utilization centers |

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 60% | 28% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services Related to Keyword |

| Stryker Corporation | Portage, Michigan | USA | Leading orthopedic implant manufacturer with dedicated foot & ankle portfolio | PROstep MIS Lapidus, foot & ankle fixation systems |

| Zimmer Biomet Holdings, Inc. | Warsaw, Indiana | USA | Global leader in orthopedic reconstruction and foot surgery solutions | Foot & ankle implants, fixation devices |

| DePuy Synthes (Johnson & Johnson MedTech) | Raynham, Massachusetts | USA | Strong orthopedic platform with extensive bunion-related fixation systems | Foot and ankle reconstruction systems |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services Related to Keyword |

| Treace Medical Concepts, Inc. | Ponte Vedra, Florida | USA | Pure-play bunion surgery leader and creator of Lapiplasty technology | Lapiplasty, Adductoplasty, Nanoplasty, Percuplasty |

| Paragon 28, Inc. | Englewood, Colorado | USA | Specialized foot and ankle company with dedicated bunion portfolio | Hallux valgus correction systems |

| Enovis Corporation | Wilmington, Delaware | USA | Strong extremities and foot & ankle reconstruction business | Foot and ankle reconstruction implants |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services Related to Keyword |

| Extremity Medical, LLC | Parsippany, New Jersey | USA | Dedicated extremity reconstruction company | Bunion fixation and forefoot reconstruction systems |

| Medartis AG | Basel | Switzerland | Growing orthopedic extremity specialist | Foot and ankle fixation solutions |

| OSSIO Ltd. | Woburn, Massachusetts | USA | Innovative bio-integrative fixation technology provider | Bio-integrative implants used in bunion procedures |

By Product Type

By Patient Type

By Surgery Type

By End-User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar